After it was announced that CPF-SA would be closed for investors at age 55.

It got me thinking.

Before this there was the whole 1M65 movement.

The idea that you and your spouse can save up $1 million in your CPF combined, before the age of 65 (as early as 45).

And if you park that $1 million in CPF-SA, you’re earning $40,000 a year, or $3,333 a month completely risk free after 55.

Well, that strategy has gone out the window now that CPF-SA is closed at 55.

But with that $1 million – are we able to invest to generate a passive dividend income of $5,000 or more?

With CPF-SA out of the picture – how to invest to replace that passive dividend income?

Crunching some simple numbers.

To get $5,000 a month in dividend income off $1 million.

That’s $60,000 a year in dividend, or a 6% dividend yield.

Is this possible?

Buy REITs, dividend stocks, or property for $5000 a month dividend income?

Let’s start from the top.

The options available are broadly:

- Property

- REITs / Dividend Stocks

Let’s start with every Singaporean’s favourite – property

Can you generate $5,000 a month in passive dividend income with $1 million in property?

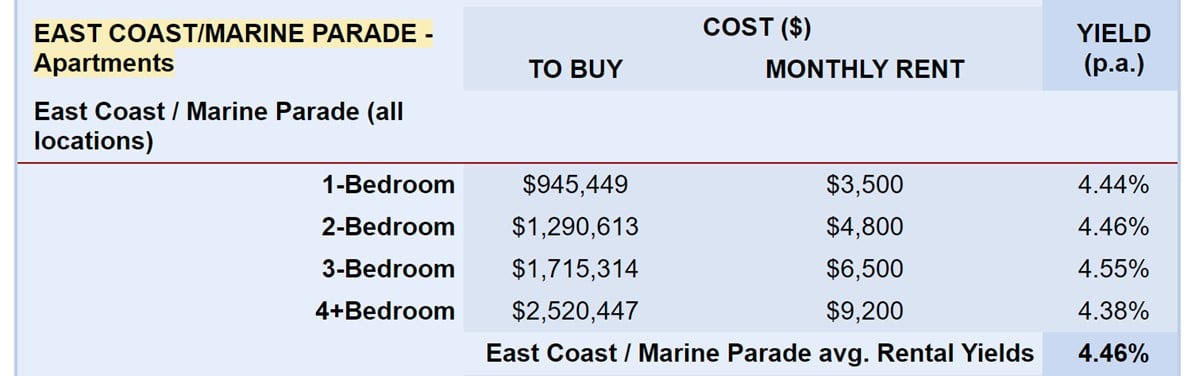

I came across a very interesting article that combed through all the rental data in Singapore from PropertyGuru and SRX, to calculate the average rental yield.

Their conclusion:

“Average gross rental yields in Singapore stands at 4.63% (Q1, 2024).”

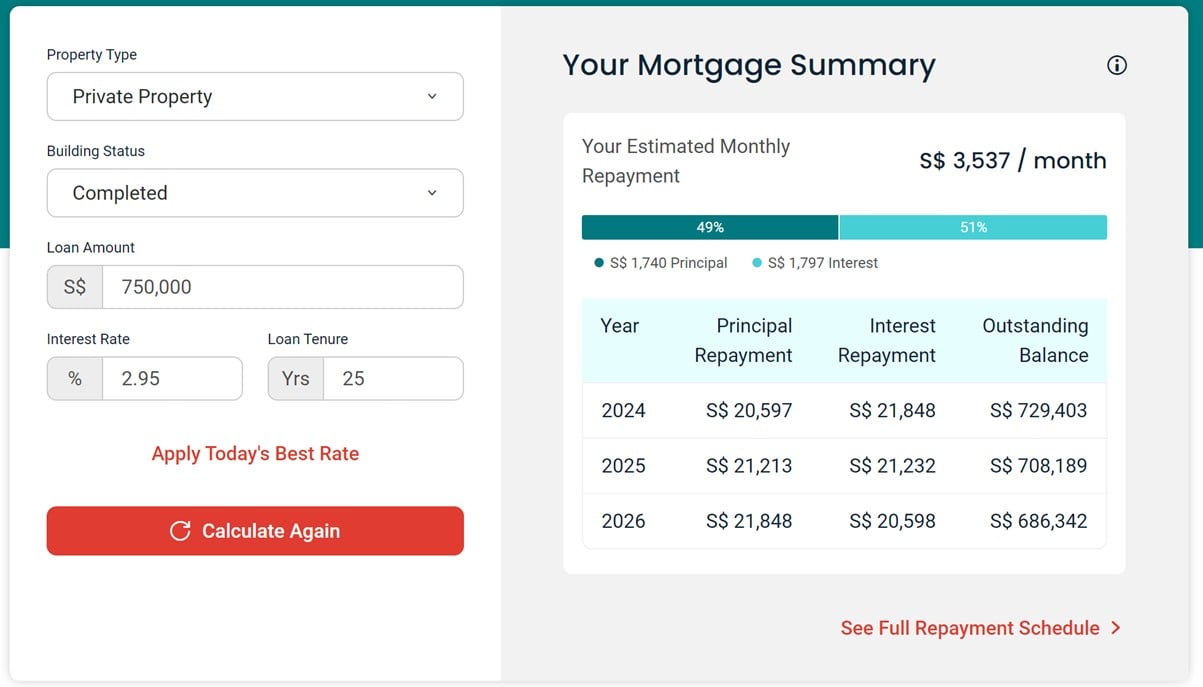

This means that if you invest $1 million into a Singapore residential property, you’ll get a gross rental yield of about $46,000 a year or $3850 a month.

Now I am assuming you are buying without mortgage – because if you have to take a loan you’re looking at $3500 a month in repayments which means there’s basically nothing left after.

But note that the numbers above are gross rental yields – before taxes, repair costs, maintenance costs, estate agents fees etc.

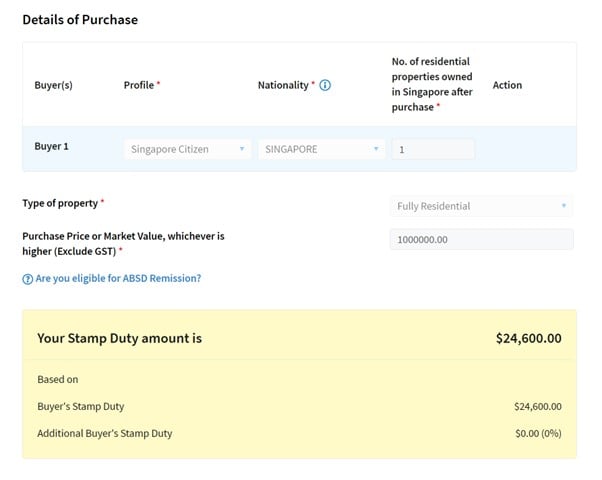

And don’t forget buying a $1 million property today will incur $24,600 in stamp duty costs.

Let’s say we minus off the stamp duty and 15% of the rental income for expenses (this is the amount allowed for by IRAS).

That works out to about $38,000 a year or $3160 a month.

That’s an effective dividend yield of 3.8%, which is actually worse than what you would have done under the previous CPF-SA regime.

So… Property is not a good choice for passive dividend income?

Of course, there are exceptions.

If you are great at spotting undervalued properties, maybe you can get a higher rental yield.

You can also argue that rental will go up over time.

But I would say this goes both ways as well.

Yes rentals are very high today – but they were much lower just a couple of years ago.

Are you able to say for certain that as a retiree over the next 20 – 30 years.

Rentals will stay high forever, and never dip?

At an effective dividend yield of 3.8% and no cash leftover, you’re not buffering in a lot of margin of safety if things go wrong.

So I would say property works if:

- You buy young and let it compound over time.

- But if you starting late – you need a big sum to start with (for a margin of safety)

If you have $2 million to buy an investment property, you’re looking at close to $6,000 a month in rental income, which is much more comfortable.

How to earn $5000 a month in passive dividend income – with dividend stocks / REITs?

So property may not be the best choice for what we want here.

What about REITs and dividend stocks?

REITs / Dividend Stocks are volatile – How much liquid cash to hold?

The big difference with REITs and Dividend Stocks, is that they are volatile.

Unlike with private property, price swings are huge.

If you’ve been investing for a while, I’m sure you understand what I mean.

Sometimes DBS goes to $35, pays a 6% dividend yield, and investors can’t get enough of the stock.

And before you know it DBS goes to $17, there is a dividend cut, and investors can’t sell fast enough.

As a retiree investing over a 20 – 30 year period, stock prices going down is a virtual certainty.

So if you want to put retirement money into REITs / Dividend Stocks, the big question to ask is:

How much cash do you hold?

The role of cash is to help you tide through the volatility.

If stock prices drop, or there is a dividend cut, or if you need some cash for emergency expenses – that cash is a godsend.

How would I do invest $1 million in REITs / Dividend stocks for passive dividend income?

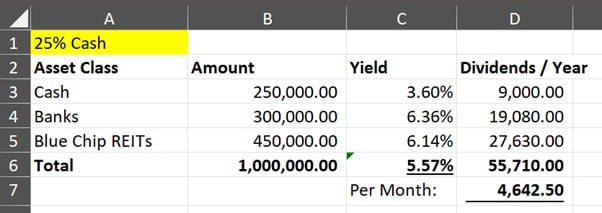

I came up with a hypothetical dividend portfolio with the following asset allocation split:

- 25% cash

- 30% Banks (40% of portfolio ex cash)

- 45% REITs (60% of portfolio ex cash)

That works out to $4,642 a month in dividend income (effective dividend yield of 5.57%).

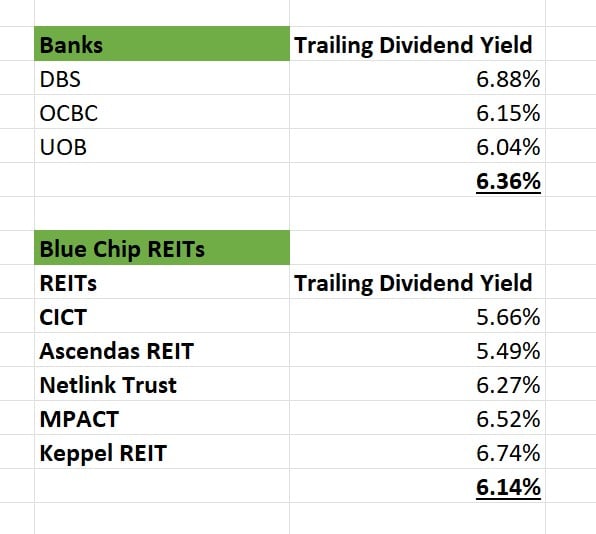

You may ask how did I derive the yields for the bank / REIT portfolio?

Well for the bank portfolio I assumed equal split among the 3 local banks:

- DBS

- UOB

- OCBC

For the REITs portfolio I split it among 5 blue chip REITs:

- CapitaLand Integrated Commercial Trust (CICT)

- Ascendas REIT

- Netlink Trust

- Mapletree Pan Asia Commercial Trust (MPACT)

- Keppel REIT

And dividend yield is based on past 12 months, so no doubt it will go up (or down) moving forward.

What are the main risks with a dividend portfolio like that in retirement?

The way I see it, there are 2 key criticisms with this dividend portfolio.

Some may argue that a portfolio with 75% allocation to REITs / dividend stocks is waaaay too risky in retirement.

What if there is a recession, and the REITs / Stocks drop 30%, and there is a dividend cut?

On the flip side – some may argue that if you’re going to put 75% into REITs / dividend stocks, you might as well do it right.

And that the average yield of 5.57% is too low for the risk you are taking on.

I guess that’s how the world works – can’t please everyone all the time.

So with the base portfolio above, let’s try to split into 2 different portfolios:

- Higher risk dividend portfolio with higher dividend yield

- Lower risk dividend portfolio with less allocation to stocks / REITs

A higher risk dividend portfolio with higher dividend yield?

What if I want to take on a more risk, for higher dividend income?

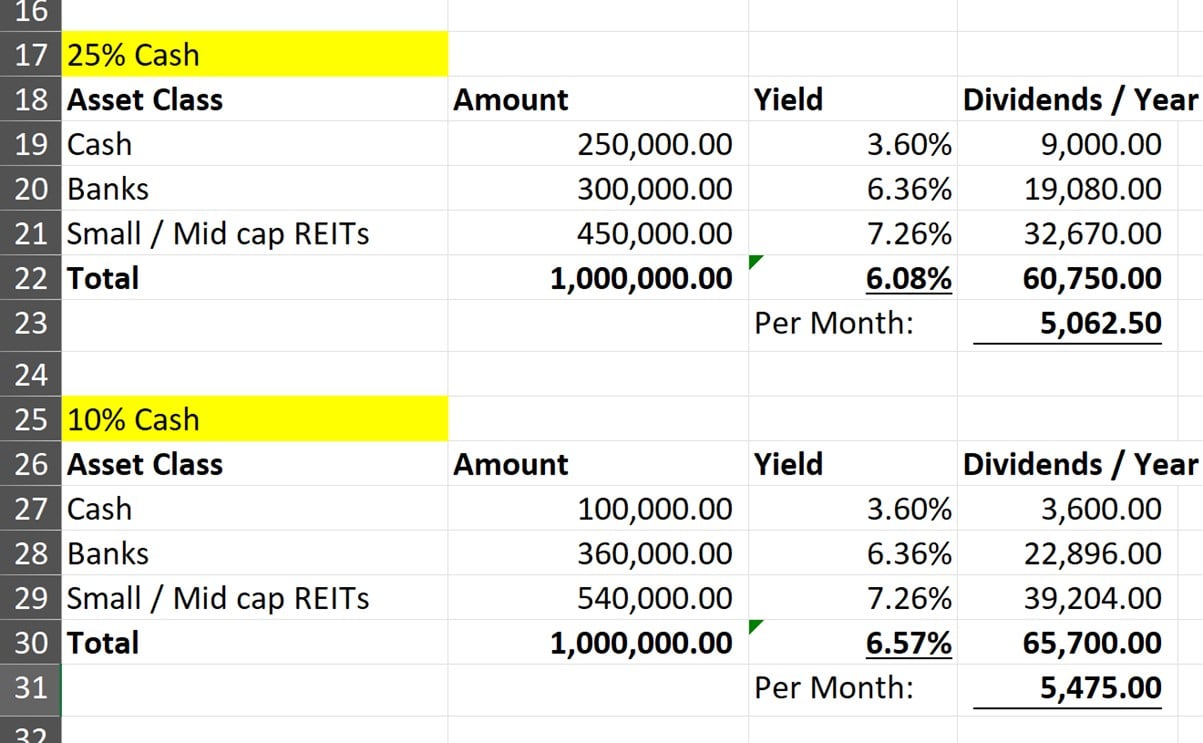

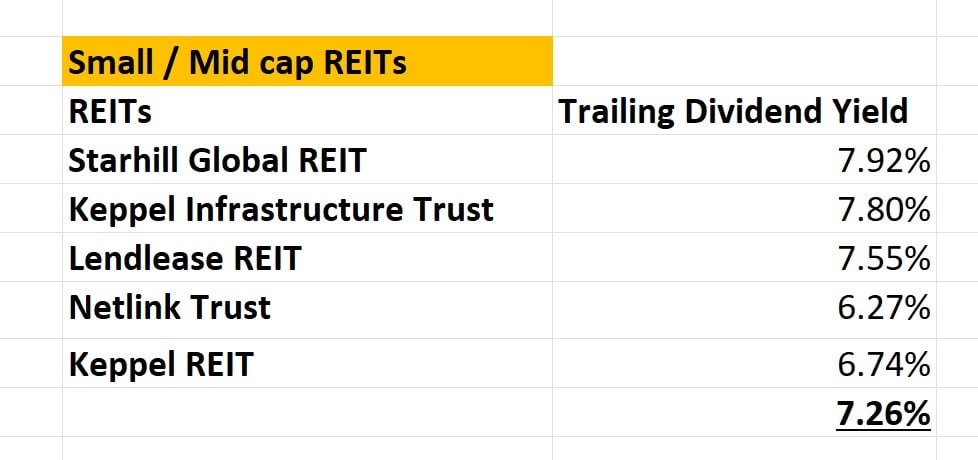

Instead of buying blue chip REITs, let’s go with the small to mid cap REITs.

Sure, there is much more risk / volatility with these REITs.

But hopefully the dividend yield would compensate.

Assuming equal split between:

- Starhill Global REIT

- Keppel Infrastructure Trust

- Lendlease REIT

- Netlink Trust

- Keppel REIT

That’s a trailing dividend yield of 7.26%, which is more than a percentage point higher than the blue chip REIT portfolio (at 6.14%).

Plugging this in at 25% cash, we get a dividend yield of $5062 a month (dividend yield 6.08%).

Hey not too bad, we’ve hit our goal of $5,000 a month.

In fact if you really wanted to juice it further.

And you were willing to drop your cash allocation to only $100,000 (10% of the portfolio).

The dividend yield would go up further to $5,474 a month (dividend yield 6.57%).

The amount of money you start with is vitally important

I feel kinda stupid saying this.

But with the analysis above – the amount of money you start with is just a game changer.

Let’s say you had $3 million.

Even with the 25% cash option above, you’re getting a cool $15,000 a month in dividend income.

Whereas if you had only $500,000.

Even if you run the higher risk option with 10% cash, you’re only getting $2737 a month in dividend income.

The more money you have, the more optionality you have, and the less risk you need to take.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Lower risk dividend portfolio with less allocation to stocks / REITs

What if we wanted to take less risk?

Given how high interest rates are these days, Bonds / Fixed income would be the natural option.

What about Bonds / Fixed Income? Dividend yield of about 5%ish?

If I wanted to build a diversified bond portfolio today, bond funds would be the natural option.

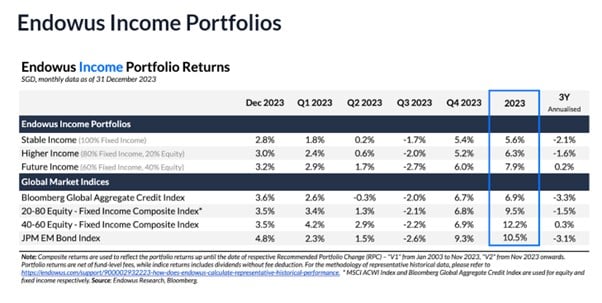

There are many options out there, but let’s use the Endowus Income fund as an example.

The 100% fixed income portfolio returned 5.6% in 2023:

But note that the returns are before Endowus fees.

After fees you’re probably looking at 5.1% dividend yield.

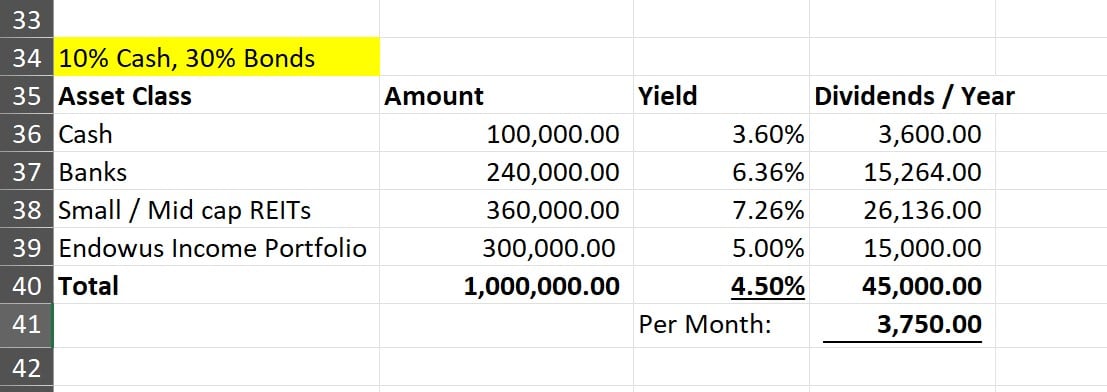

If we put 10% into cash and 30% into bonds (basically a 60/40 between stocks and bonds respectively).

We get a monthly dividend of $3750 (dividend yield of 4.50%)

Is the 5.6% dividend yield from bonds sustainable?

If you look at the bond portfolio returns closely.

You’ll find at 2023 was a great year – the bond fund returned 5.6%.

But 3 year annualised yield is an abysmal negative 2.1%.

The problem with buying a lot of bonds today, and holding for the next 20 – 30 years.

Is that you are basically making an assumption that interest rates will worst case stay around where they are today.

Because if interest rates move structurally higher for the next decade or two.

You may be looking at pretty poor returns for bonds.

What would I do for myself? How to earn $5000+ a month in passive dividend income?

The way I see it.

The fundamental problem with building a dividend portfolio today.

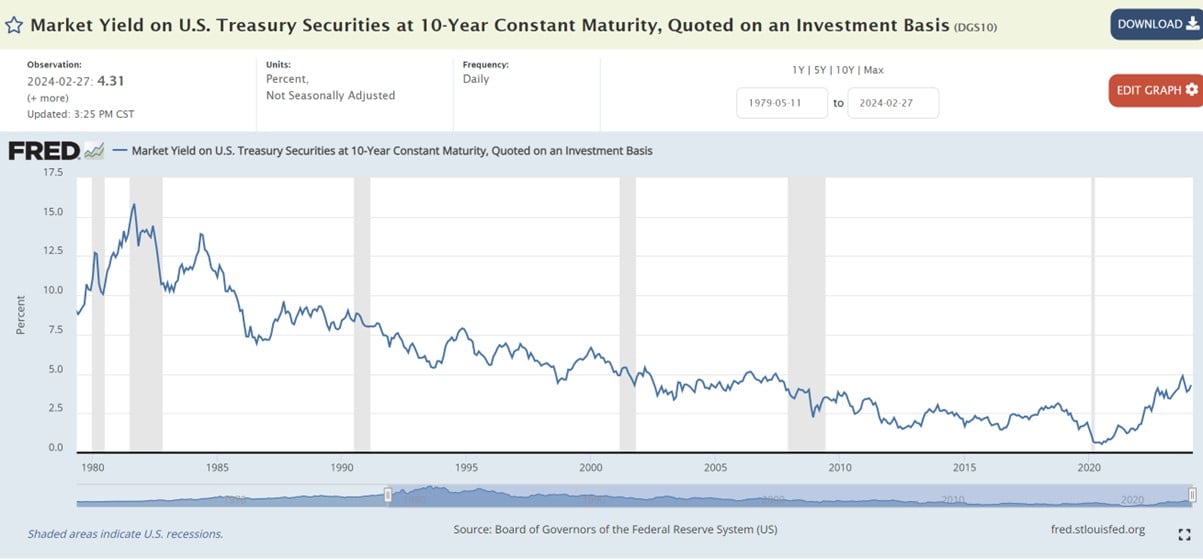

Is the fact that interest rates have been structurally going lower for the past 40 years.

And if you look at the chart below, you’ll realise that trend ended in 2020.

After 2020, for the first time in 40 years – interest rates have gone higher this cycle, than they went in the past cycle.

My view is that we are moving into a period of structurally higher interest rates, and structurally higher inflation.

And without the tailwind of interest rates going lower after every cycle.

That creates a fundamentally different climate for investing.

What are the options for Singapore dividend investors?

There are 2 potential solutions in my view:

- Become a more active investor

- Accept the higher volatility / lower returns

Either you become more active in your investing approach, and time the mini market cycles.

Or you just stay pure passive, and accept that the higher volatility / lower returns is the feature of this new regime (requires a retiree to hold more cash).

In fact you could even have it both ways.

Have one portfolio that is pure passive,

Another portfolio where you try to time the cycles.

Personally that’s the kind of approach I run, and you can see my full portfolio breakdown on FH Premium.

I also share the full list of REITs and Stocks I am keen to buy on FH Premium.

How would I do it? Which dividend portfolio would I use in retirement?

But I didn’t want to leave the article open ended, so let’s come back to the portfolios above.

If this were me?

Retiring with $1 million?

I don’t think $1 million is enough for the investment property option – $2 million would be much more comfortable.

Of the REITs / Dividend Stock portfolio – I think I would run the 25% cash option, with allocation to blue chip REITs.

Reasoning being that for a retiree I’m not sure the additional risk is worth it to buy the small/mid cap REITs.

Better to just stick with blue chip REITs and play with grandkids or whatever it is I want to do in retirement.

And I think 10% cash is too low for a retiree.

You never know when the market will go into a downturn, and how long it takes for the market to recover.

In fact I may even think 25% cash is too low, and if the portfolio size were $2 million for example I might approach this quite differently.

But at $1 million, some trade-offs have to be made between safety and yield, to hit the target returns.

But hey that’s just me.

Would love to hear what you think!

This article was written on 1 March 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Just one question, how many Singaporeans has 1 million SGD in real assets or liquidity to invest for 5K per month of passive income or dividends so to speak. I appreciate your efforts and breakdown advices but the sums you computed is not practical for 80% of Singaporean.

This was supposed to be combined with the spouse, but I get your point.

Curious to hear – What would your suggestion be for this 80% of Singaporeans?

The article was meant for those who managed to hit 1M65 using your CPF. And there are others who have written about how to do this at the median Singapore income (which has since gone up). For example at https://blog.seedly.sg/1m65-1-million-by-65-cpf/.

“Before this there was the whole 1M65 movement. The idea that you and your spouse can save up $1 million in your CPF combined, before the age of 65 (as early as 45).”

Yes this is right, it is based loosely off the 1M65 thinking.

Nice post as always! One question. Do you think the portfolio is too concentrated towards Singapore stocks – mainly property and banks; both sensitive to the interest rate cycle. What are some options to achieve the same goals but with more diversification across geographies and sectors?

Yes I agree with this. There is a bit of hedge against interest rate risk though because rates down is good for REITs / bad for banks and vice versa. But if we have a bad recession both will do poorly.

The geographical allocation point is spot on though.

If you want more diversification, I would say throw in the S&P500, throw in commodities / energy, and throw in crypto / gold.

Once you do that however, the dividend yield will go down drastically. So for a retiree this will entail (a) selling off the principal for living expenses, or (b) having a much larger portfolio size to live off the yield.

Both are not straightforward to execute, so there is some nuance in this.

Another question regarding start points :).

So in your example, it is assumed the couple has $1 million in cold hard cash as a starting point.

However, for most Singaporeans (yourself included) to get to that $1 million, we probably had some mix of higher risk assets (eg. growth assets), mid risk assets (dividend yielding stuff), and low risk assets (cash, singapore savings bonds etc.).

At the point of “retirement” so to speak, what would you recommend we do with the “growth” part of the portfolio? Sell off entirely and buy dividend stocks? Hold it for capital appreciation and sell off part of it as time goes by “make up” for the income short fall?

I think I’ve mentioned this in another post in the past – but I think investors should run one strategy to build wealth, and another strategy to preserve wealth (once they hit the amount they are comfortable with).

To get to a million, you wouldn’t run a portfolio like this unless of course you already take on a lot of risk in your day job (eg. very commission based job, own business etc). You would want something much more growth focussed – stronger emphasis on US tech, crypto, timing the business cycles and so on.

The second qn – depends very much on risk appetite and also investor knowledge and portfolio size.

If you know what you’re doing, and have a large portfolio, I would say you keep the “growth” stuff in to hedge inflation (but prob dial back on the percentage).

But the growth stuff is volatile and requires timing the cycles, which not everyone is equipped or prepared to do so in retirement. For investors who want something pure passive it may make sense to just track an index like the S&P500 instead. Or if the portfolio is big enough, just go into fixed income/cash, or buy property.

Great comments though, appreciate it very much!

The calculation show cash @ 3.6% return. What’s the assumption? UOB One or something else?

I used T-Bills, and a slightly convervative number vs latest yields.

You may argue that over a longer period of time you may not be able to get 3.6% return on cash. And that’s a perfectly valid point.

Although the flipside is true also. If we are moving into a period of structurally higher interest rates, cash may return >3.6% going forward.

Eh… If you can get 1mio or like what you mentioned 2mio… You think you would probably know how to get 5k a month during retirement…

Fair enough haha. Doesn’t hurt to have extra/alternative suggestions I suppose, for those who already have 1-2m and know what to do with their money.