So I received a very interesting question from a FH Premium subscriber:

Dear Financial Horse,

My wife and I are PRs and plan to retire in a few years in Singapore and I would appreciate your guidance on developing a sound investment strategy for our retirement needs.

Current Financial Situation:

- Expected monthly retirement expenses:

-

- Fixed costs (condo, car, maid, utilities): $10,000 SGD

- Discretionary (travel – kids in overseas universities, entertainment): $7,000 SGD

- Total: $17,000 SGD

- CPF: Expected to cover $4,200 SGD of fixed costs

- Current Investment portfolio:

Investment Preferences:

- Passive investment

- Minimize FX risk

- Open to investing globally, but cognizant of US market growth dominance

Specific Questions:

- Given our financial situation and retirement goals, what asset allocation strategy would you consider?

- How can we best manage the FX risk associated with the USD-denominated stock, particularly in the context of our retirement timeline?

- What ETFs would be suitable for achieving our goals, considering our preference for passive investing?

I understand that the Google stock is subject to a 40% US Estate Tax upon my death, which adds complexity to an already challenging situation. If your expertise lies outside this area, I completely understand and will seek guidance from a US tax advisor.

Please note this is NOT Investment Advice

Do note that I have amended some details above to protect the privacy of the FH Premium subscriber.

And please – nothing in this article should be taken as specific investment advice.

I am sharing some high level thoughts on what I would do in a similar situation – but the ultimate decision on how to invest has to be made by each investor.

Expenses of the Investor ($154,000 a year)

The investor’s expenses are:

- Fixed costs (condo upkeep, car, maid, utilities): $10,000 SGD

- Discretionary (travel – kids in overseas universities, entertainment): $7,000 SGD

- Total: $17,000 SGD

But his CPF is expected to generate $4,200 a month.

So that leaves a shortfall of $12,800 a month to be generated from the investment portfolio.

That’s $153,600 a year, but let’s just round it up to $154,000 a year.

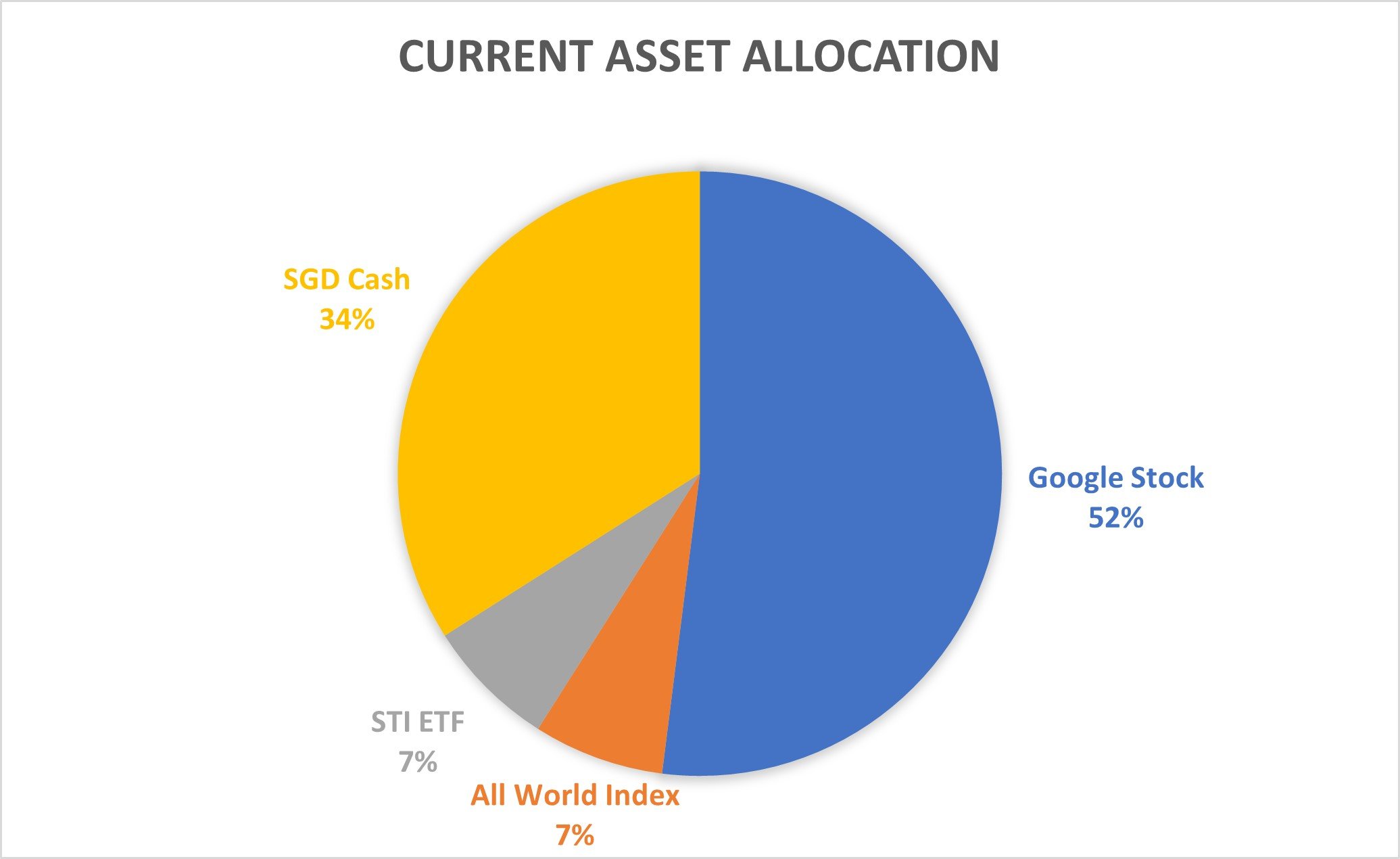

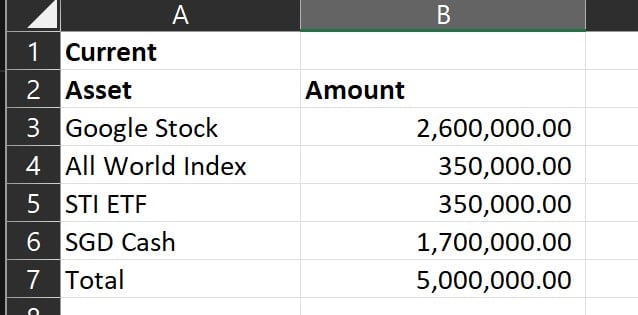

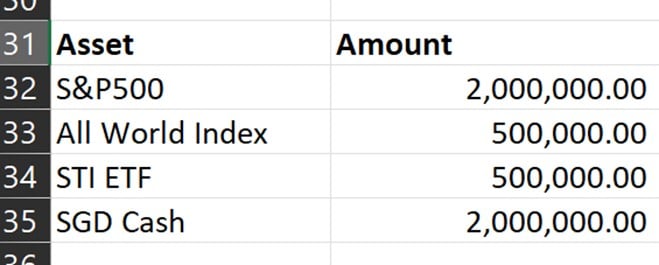

Current Asset Allocation of the Investor ($5 million SGD)

Based on the details provided, I have summarized his current asset allocation below:

52% of your net worth in one stock… is a lot…

The first point that jumped out at me with the pie chart above.

Is the whopping 52% allocation of investible net worth into 1 stock.

Concentrating your net worth makes sense if you want to get rich

Now I do not doubt for one second that running 52% allocation to a single stock (Google) has helped this investor in his wealth building journey.

Here’s the chart of Google below.

It’s up a whopping 5x over the past 10 years.

But what if you are already rich?

There’s an age old saying in investing.

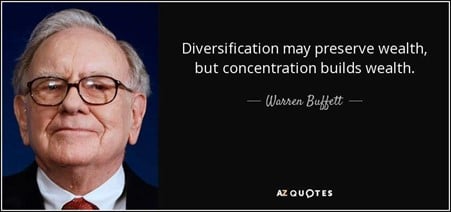

“Concentrate to get rich, diversify to stay rich”.

Here’s the saying in a different form by Warren Buffett:

Getting rich, vs staying rich are different things

I suppose the key question here for the investor.

Once you have amassed $5 million in investible wealth.

You are a few years away from retirement.

Your yearly expenses total $154,000 – which means that if you chuck the full $5 million into T-Bills at 3.7%, you get $185,000 a year with no risk, more than what you need for your expenses.

Given all of the above – do you still need to concentrate your wealth into 1 stock in this way?

In other words – do you want to take on risk for the chance to get even richer, or do you decide that you are already rich enough, and want to switch to diversification to preserve the wealth?

Now for the record – there’s no right or wrong answer here.

For some people $5 million is more than they can dream of amassing.

For some people $5 million would barely even begin to satisfy their needs.

This question needs to be addressed personally, by each investor.

What is the number (of wealth) you need to hit – that after which you will think you have enough.

That’s really the biggest question that jumped out at me when I saw this net worth allocation.

When you run 52% allocation to 1 stock, all you need is a bad earnings miss from Google, or some unknown risk that comes to light, and you could be looking at significant destruction in net worth, and potentially a much less comfortable retirement.

All this makes sense when you are young and building wealth.

But when you are already rich, you may want to think about whether this is a risk worth taking.

What asset allocation strategy to generate $154,000 a year on $5 million?

Now of course you can just put the $5 million into risk free T-Bills.

At latest interest rates of 3.73%.

That’s $186,000 a year with zero risk, well above the $154,000 expenses required.

But the problem with a 100% cash portfolio is: (1) refinancing risk, and (2) lack of inflation hedge.

Buying 6 month T-Bills means that you need to refinance every 6 months, and who knows where interest rates will be in 6 months.

And a pure cash portfolio means that if inflation stays high over the next 20 – 30 years of your retirement, you could be looking at significant erosion of net worth.

So you do want some kind of equity exposure – the question is how much.

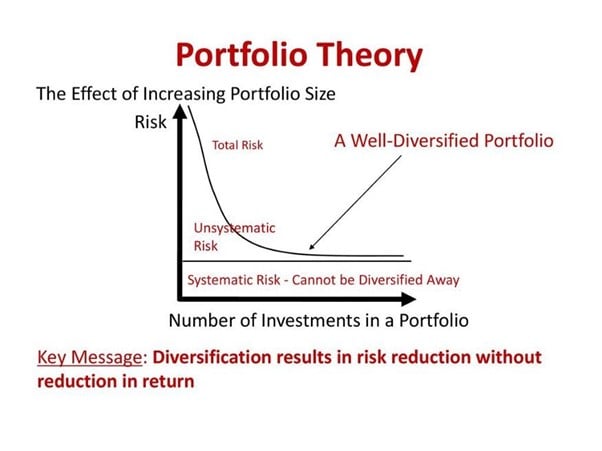

Diversifying to preserve wealth?

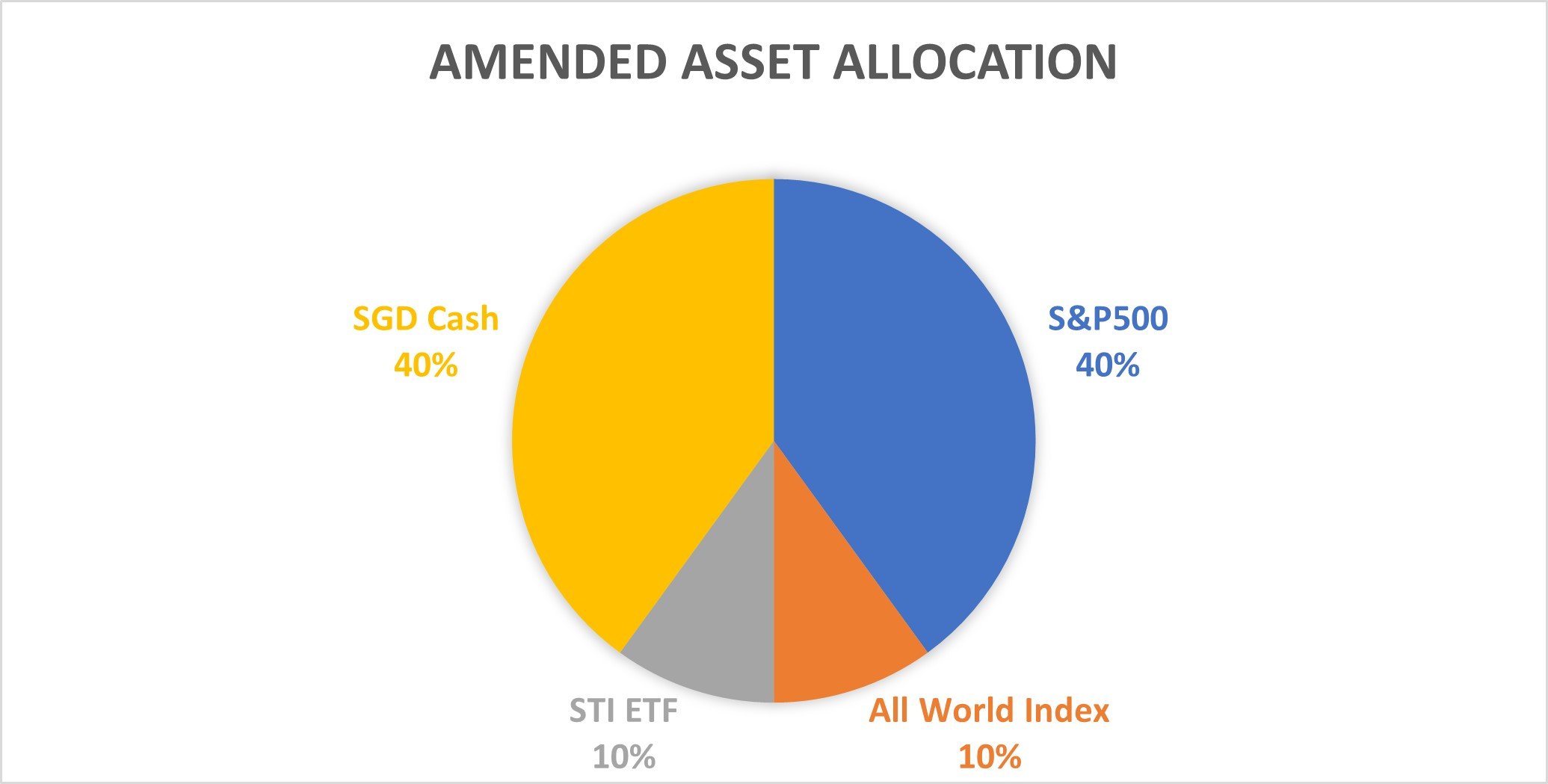

The simplest tweak to the portfolio is to diversify away the single stock risk.

Diversify the Google stock into a mix of the S&P500, All World Index, and the STI.

I made a simple tweak to the asset allocation below, to keep the passive ETFs the investor is comfortable with, and yet diversify away the single stock risk from Google.

What if you want skin in the game as an employee?

Of course you may say that you are working in Google and need to have some skin in the game, so I suppose the question to ask is how much skin in the game do you need here.

Based on that answer, you can then keep that amount of Google stock, and diversify the rest into the S&P500.

How to manage FX risk with the USD-denominated stock (given the retirement timeline)?

Now even with the amended portfolio above, it still runs about 40-50% exposure to US markets.

Which brings us to the second question raised by the investor.

As a Singapore investor, living in Singapore and spending in Singapore, but investing in the US markets.

How do you hedge USD FX risk?

20 years ago the USD/SGD pair was at 1.85.

Today it sits at 1.33, a whopping 30% depreciation in USD vs SGD.

If you’re investing over a 20 – 30 year retirement period, these are real issues to think about.

Diversify into SGD stocks?

The simple answer is to diversify into SGD stocks.

But c’mon.

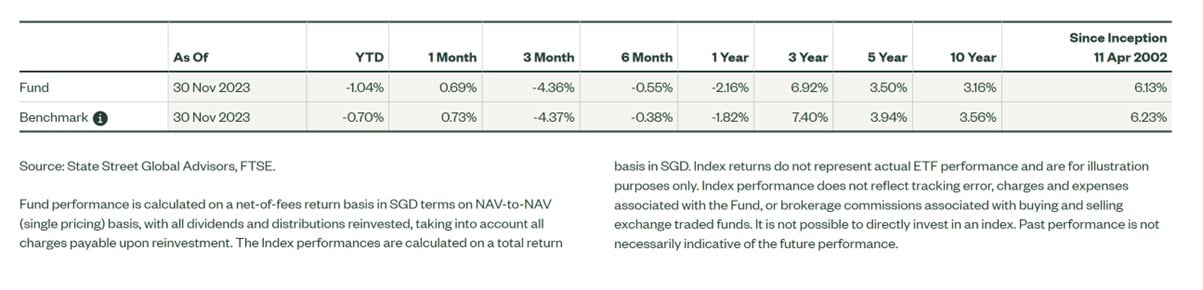

The STI ETF returned 4% last year, the S&P500 did 26%.

The problem with the STI ETF is that while you solve FX risk, the returns are much less than stellar.

10 year annualized returns are a miserable 3.16%.

Of course, you can try to outperform the STI with stock picking, but the investor wants a passive buy and hold strategy.

There’s no escaping the US markets, as a Singapore investor?

You have to recognize that the past 10 years (or should I say the past 40 years), the overwhelmingly best stock market to be invested in by far is the US.

The US stock market dominates global indices.

Even if you buy an all world stock index, 60% of that exposure is US markets.

Long story short.

As the investor himself pointed out, as a Singapore investor you cannot afford to not have exposure to the US market.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

What asset allocation would I run, to manage FX risk?

For what it’s worth, there are no easy answers to this question.

If you’re holding USD stock, it cushions the FX risk because if USD goes down, the stock price *should* go up.

But that is a big should, because you are assuming no decline in US dominance over the next 2 – 3 decades, and the world today is a very uncertain place.

Ultimately, it is about finding the right balance between USD and SGD stocks.

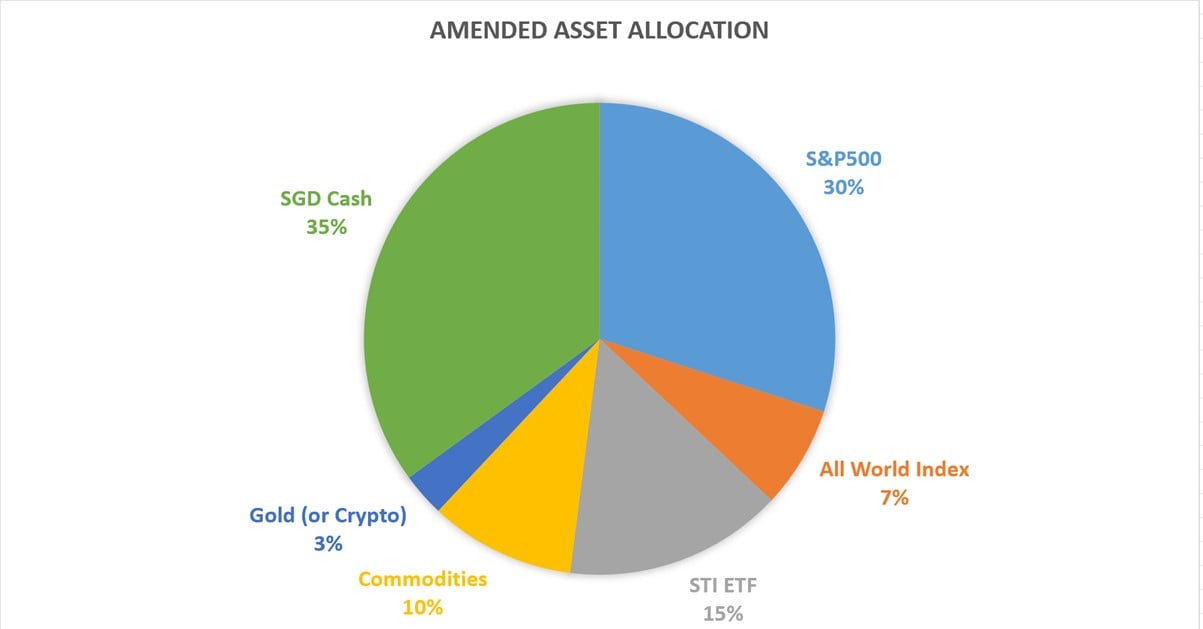

Personally for me, I would dial back the US exposure slightly, and move some of that cash into a more balanced portfolio spread across multiple asset classes, especially as I get closer to retirement.

The key asset classes missing from the portfolio are commodities and gold.

Both are useful to hedge against a more inflationary world, and any money printing.

This might be the asset allocation I would run, while keeping things simple:

Note that I included crypto as an option, but investors not comfortable with that exposure can use gold instead.

Assuming the $1.75 million cash is invested at a 3.5% yield (very achievable in this climate with low risk), you’re looking at $61,250 a year in interest.

That means the rest of the $3.25 million portfolio just needs to hit a 2.85% return and the basic expenses are covered.

Not too bad really – although a 50% equity exposure is on the high side, and if it were me I would look to gradually reduce it (in favour of bonds) the further into retirement I get.

Follow up questions from FH Premium Subscribers

Following up on the Early Access article earlier today.

I received 2 great follow up questions from FH Premium subscribers that I thought really added colour to the discussion.

I set out the questions, and my responses below.

Hi FH, would you recommend the investor to build the ETFs over time or purchase one lump sum to hit the allocation. Let’s assume someone is 5 years to retirement.

So academic theory back tested over the past 100 years will tell you that lump sum outperforms dollar cost averaging.

But what academic theory cannot prepare you for, is how you feel when you buy $1 million of S&P500, and it drops 30% in value over the next 12 months (if you’re unlucky).

So there’s theory, and then there’s practice.

I would say for most retail investors that are looking to build a passive ETF portfolio.

If you are sophisticated and know what you are doing, and have nerves of steel – lump sum is fine.

For almost everyone else, dollar cost averaging may make more sense, simple because emotionally it is easier to handle.

In this case however, the situation is unique because the investor already has $2.6 million (52% of his investible portfolio) in Google stock.

So to avoid timing the market, I would say that if he sells X amount of Google stock with the intention of moving the money to the S&P500, then he should buy it soon (after selling the Google stock).

If you take that approach that hey the S&P500 is a bit expensive today, let’s wait 2 weeks for it to get “cheaper” before I buy.

Then you run the risk of the market going up in that 2 weeks and then you say let’s wait another 2 months and before you know it it’s a year.

So there is no right or wrong here, and it really depends on how sophisticated you are as an investor, and whether you are able to deal with it emotionally.

But generally speaking the above is how I would approach the issue.

Dear FH,

For your latest early access article for helping a premium reader on the 5mil assest allocation.

I was surprised that there is no Singapore dividend stock for him, is it because you totally avoid stock picking in the consideration due to his passive investment request?

I am thinking the current Singapore REITS stock or even Netlink trust which offer 6% dividends (which currently is and locked in once bought) consistently is worth to be allocated in as well and it would easily suit his passive income needs, on top of low FX risk and no US stock inheritance concern.

What do you think?

Now if you look at the STI ETF today.

It’s about 50% banks, and 20% real estate, and the rest is a mix of Temasek companies.

No doubt if you buy the 3 banks yourself, stock pick some REITs and dividend stocks, you could come up with a mix that outperforms the STI ETF.

It’s what I do myself, and I outperformed the STI ETF handily last year (full portfolio is available on FH Premium).

But it is clear that this investor wants a passive portfolio, and not wade into stock picking.

And that’s perfectly fine as well.

Let’s say instead of the STI ETF, you decide to buy DBS, UOB, OCBC, CICT, Ascendas REIT.

Now it’s 12 months later, and CICT looks expensive, while MPACT looks cheap.

Do you sell CICT and buy MPACT?

Once you go down this route of picking a few REITs or dividend stocks, it’s very hard to draw the line on where do you stop.

So because of that I kept this to pure ETFs only, with the intention to be pure passive and no stock picking.

But investors who want to try their hand at stock picking and outperforming the STI ETF – that’s what the rest of Financial Horse is about.

What ETFs would be suitable to achieve these goals (given preference for passive investing)?

The main ETFs to note are:

- S&P500 (iShares Core S&P 500 UCITS ETF (CSPX) is the Irish domiciled ETF for better tax treatment for Singapore investors)

- All World Index (Vanguard FTSE All-World UCITS ETF (VWRA) is the all world index the reader uses)

- STI ETF (ES3)

Really, if you just want to build a pure passive portfolio without touching stock picking, you wouldn’t need to venture very far from the 3 ETFs above.

If you want to overweight US tech you can throw in stuff like the NASDAQ (QQQ), or XLE for exposure to energy/oil, but if you don’t want to the above 3 will work just fine.

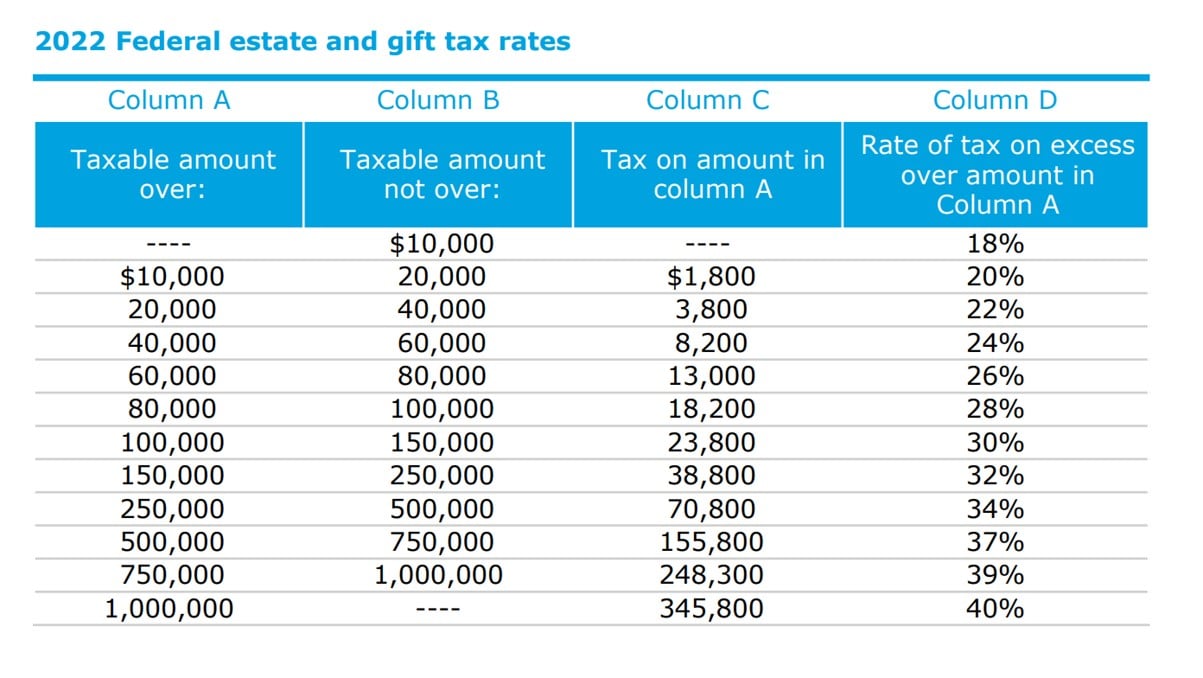

Estate Tax (Inheritance Tax) Issue

The final issue is the inheritance tax issue.

In case you don’t know, US stocks are subject to inheritance tax.

For non-US investors, the first $60,000 is tax exempt.

After the first $60,000, the inheritance tax is set out below:

You can see how this inheritance tax ramps up aggressively, to a top end rate of 40%.

For the investor with his $2.6 million in Google stock, he would be looking at close to a $1 million tax bill on passing.

That’s absolutely bonkers.

There are 2 simple solutions to US inheritance tax:

- Buy non-US assets

- Give away the assets before death

Buy non-US assets

A simple one is to hold non-US assets.

If you sell the US stocks and buy Singapore stocks for example, then there is no inheritance tax.

If you really want to stick with US stocks, you can actually do stuff like buy the Irish domiciled S&P500 (CSPX) to get around US inheritance tax (but please get specific tax advice as each investor’s situation may be slightly different).

Give away the assets before death

This other approach assumes you do not die suddenly or unexpectedly, and there is time to handle these matters in older age.

In which case you can gradually sell the US assets in your later years, and distribute to loved ones or spend as you deem fit.

Such that by the time of your passing, the amount of US assets is significantly reduced.

Of course, this requires a bit more effort and hassle, especially as this investor seems to prefer a more passive approach.

Now there are more complex tax avoidance solutions like trust structures and so on (including some that are less than legal).

But I don’t want to go too much into the nitty gritty, and do speak with a tax advisor for the more complex structuring.

Closing Thoughts: Getting Rich, vs Staying Rich

If you only take away one thing from this article.

Let it be this.

Concentrate wealth to get rich.

Diversify wealth to stay rich.

This is an age old wisdom in investing, and it remains ever so true today.

The tricky part is to understand what it means to be “rich”.

Some people would think $5 million in liquid assets is already enough to retire tomorrow and travel around the world.

Some people think $5 million would not be enough to satisfy them.

There is no right or wrong here – only you can answer this question for yourself.

So I encourage all investors to think through this question in the new year.

What is the level of wealth you need to achieve… that if you hit this number tomorrow… you will be satisfied and say you have “enough”.

Or is this a number that will keep shifting over time?

The answer to this question, may have big implications for your investment strategy and the amount of risk to take.

In any case, you can check out my full portfolio to see how I am positioned in 2024, on FH Premium. I also share the REITs and Stocks that I am keen to pick up, and target prices.

This article was written on 5 Jan 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

– Get up to USD 5000 worth of shares (Best promo of 2023 – Now Extended)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Hi there. Nice post 🙂 couple of thoughts. For OP’s situation would you recommend a financial planner? Say someone fee-based like providend.

Also notice that there is no fixed income in the portfolio. And for a passive solution to income generation, how about the sing reit etfs?

Financial planner depends very much on who you can find, and also the investor himself. No right / wrong here.

Fixed income – of the cash allocation, you could make a case for diversifying a portion of that into longer duration bonds for a higher yield. But then it becomes more complex to manage, so it really depends on what you are going for.

REIT ETFs are not a great product because of all the fees and low liquidity. But I suppose it’s still better than nothing. The complexity is that the STI ETF already has decent enough allocation to real estate, so you will need to take that into account.

Hi FH

This is a very interesting article with many points to ponde. Love your comments that to create wealth, concentrate. Diversify once you have created wealth. I’m in the latter. It’s so true, at least for me. I would rather have a low risks portfolio than having to endure huge volatility and lose sleep in retirement. That’s just me. Sold all my US and HK stocks in 2020 and is now 100% in SG. Low return but peace of mind. Up and down 10% is something for me.

Keep the good articles coming. Old brain needs some exercise too. 🙂

Great blogpost but didnt answer the qns of getting 154k dividends to cover the shortfall after saying 5mil in t-bills arent viable during to inflation. The portfolio with overweight in US equities is unlikely to generate 154k dividends since thats an average of 3.1% div yield required on the 5mil portfolio

Yeah true, I didn’t expressly explain how I would deal with it in the article, so let me just clarify here.

With the 1.7m cash at a 3.5% yield average, you just need the rest of the portfolio to generate about 2.8%ish dividend / investment income.

That’s a fairly low bar, even below the 3% or 4% withdrawal rule that most investors use for retirement.

The bulk of the dividend income here will come from STI /commodities. The rest will have to come from capital gains / principal drawdown, which given that the amount is below 3% I thought it would be sustainable.

Haha thanks for the kind words!

Yes agree with this.

Investing is very much dependant on the individual.

Some people want to take big risks and high volatility to get rich, even at the risk of losing it. Some people are already rich, they just want to preserve the wealth and sleep well at night.

No right / wrong here, and love to hear that you’ve spent the time thinking about what works for you.

Well better from capital gain as diciden is subject to 30% withholding tax from uncle Sam.

If I were to worry, I would factor in the inflation, especially as someone in his late 50s or early 60, the life expectancy could still be long and in that 20 to 30 years to come, a mere 2% inflation will inflate your 17000sgd monthly cost 25000$ after 20years. Also old age care and medical cost might surge so you might even need to drain your principals if needed. Last but not the least we should give the dumb bell protofolio a thought and allocate some fund in risky yet potential asset eg. Cryptos, AI, etc.

Yes, not much point using US stocks for dividend plays due to the withholding tax.

Fair point. Although with the size of the portfolio I think it *should* be sufficient to address these issues.

Interesting post. May I ask what would be a good vehicle for the 500k commodities exposure?

Thanks!

Depends on what you’re going for. If you’re passive just a broad ETF like XLE for energy or XME for metals may work, if you’re active then really the world is your oyster.

Thank you for the interesting article. I’m somewhat in the middle, have build up some wealth and thus would like to preserve it to ensure not too much fluctuations. Can I check which brokerage would you recommend to purchase Irish domiciled S&P500 (CSPX)? I usually buy SPY on TD ameritrade but yes there is tax withholding. Thank you!

IBKR is worth looking at if you want to buy on the LSE: https://www.interactivebrokers.com.sg/en/index.php?f=47326&wid=1020000078