So I received this very interesting question from a reader:

Dear Financial Horse…

I’m asking on behalf of a friend…

43 years old male, married with two kids, 5 n 3 years old. Zero debt. Paid off residential mortgage some six years back.

Has 730,000 sgd cash- 650k in fixed deposit this year earning 27k interest for this year. Another 50k liquid cash buffet to buy stocks.

Another 90k in stocks, singtel (bought at 3.75) n keppel Corp (bought at 7.25)…should be netting 4k interest…

Minimum annual expenses for my household plus personal expenses 36k pa..

Needs 50k to have buffer for savings n maybe travel nearby maybe.

..

Wife working n has abt 400k cash n stocks I suppose…

Can retire?

His wife is asking him to continue working. He wants to quit…

Can or cannot? How to generate 50k pa Minimum like this? Possible to quit?

Retire and live off dividend income? How realistic is this?

I know that a lot of investors like the idea of investing in a dividend portfolio and living off the dividend income.

I’ve always thought that investors underestimate the risks of such an approach.

But in any case – let’s run the numbers and see if this is workable.

For obvious reasons, nothing in this article should be taken as financial advice.

Total assets the reader has

To sum up, the reader has:

- $730,000 cash

- $90,000 stocks

- $400,000 in wife’s stocks and cash

Yearly Expenses of the reader + Ideal dividend income

The reader mentioned that he needs a minimum of $36,000 a year for household and personal expenses ($3,000 month).

Ideally though, he wants $50,000 a year for savings and travel.

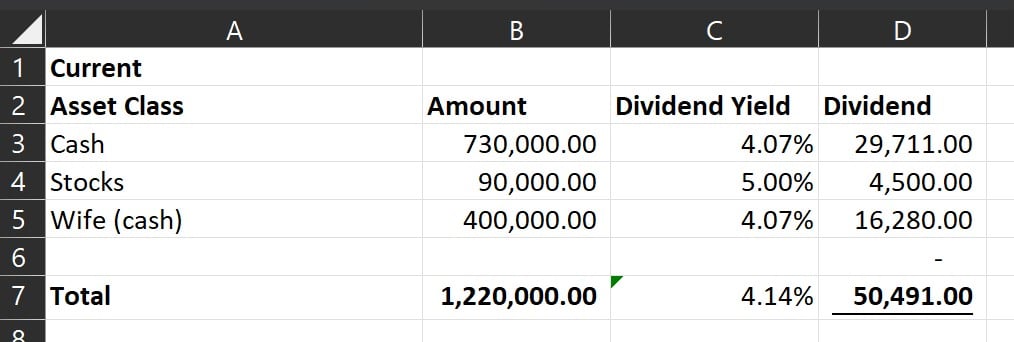

Dividend Income of a conservative portfolio

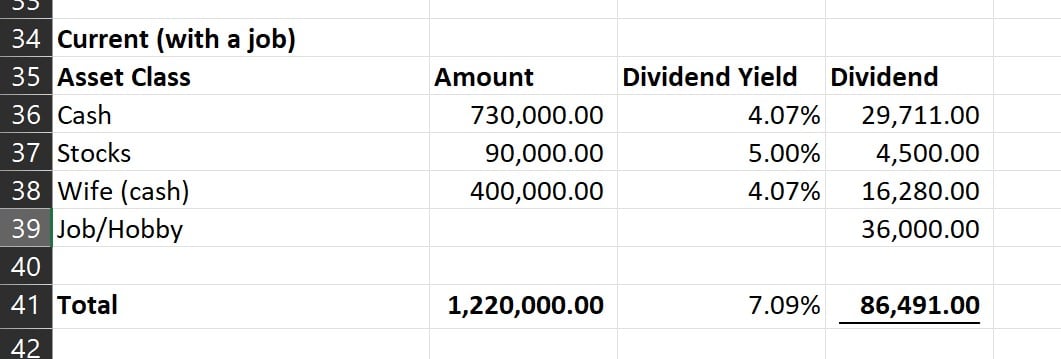

Conservatively speaking, let’s say:

- His $730,000 cash goes into T-Bills and earns 4.07% (latest T-Bills yield)

- His $90,000 stocks earns an average of 5% yield

- His wife’s $400,000 goes into T-Bills and earns 4.07%

I’ve run the numbers below.

It works out to $50,000 a year in dividend income.

That’s basically the reader’s annual target right there.

This is a very conservative dividend portfolio – already generates $50,000 a year dividend income

I’m sure you would agree that the numbers above are fairly conservative.

We’re assuming that the $1.1 million in cash just goes into 6 month T-Bills that yield 4.07% risk free.

While the stocks earn an average 5% yield, which is very achievable today just by buying a mix of DBS/UOB/OCBC, and some blue chip REITs like CICT or Ascendas REIT.

And even running these relatively conservative numbers, we already get $50,000 a year.

Exactly in line with his stretch goal of $50,000 a year dividend income.

Not too bad at first glance.

What is the biggest risk of this dividend portfolio?

The way I see it, there’s 2 massive risks with this portfolio:

- Refinancing risk

- Expenses going up

Refinancing risk of the dividend portfolio

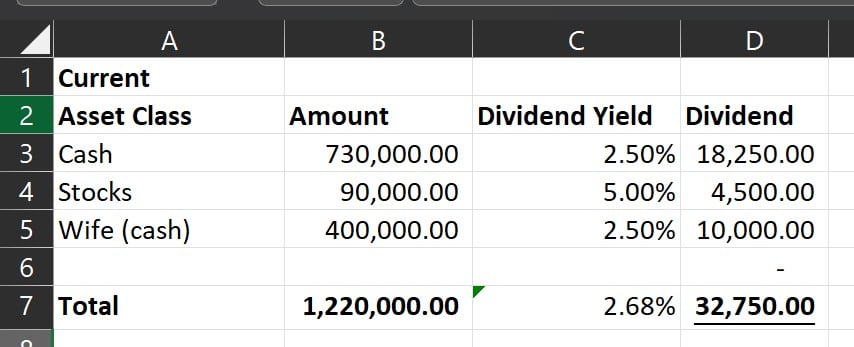

$1.1 million in cash goes into T-Bills with a 6 month maturity.

This means that you need to refinance 90% of the portfolio every 6 months.

Sure, maybe interest rates in 6 months are at 4.5% and you party like a king.

But what if interest rates go down to 2.5%?

Suddenly you’re looking at $32,000 a year in dividend income, well below what you require for living expenses.

So this is a massive risk of putting 90% of your portfolio into short term, 6 month instruments.

And personally I expect this to be a problem the next couple of years – I don’t see short term interest rates staying at these levels for too long.

Expenses going up for a dividend investor?

The other one of course, is expenses going up.

Life expectancy in Singapore is 83.

If you’re going to retire at 43.

You’re probably looking at having to support yourself for the next 40 years.

And don’t forget the 2 kids.

Maybe $36,000 a year today is enough.

But what if inflation hits?

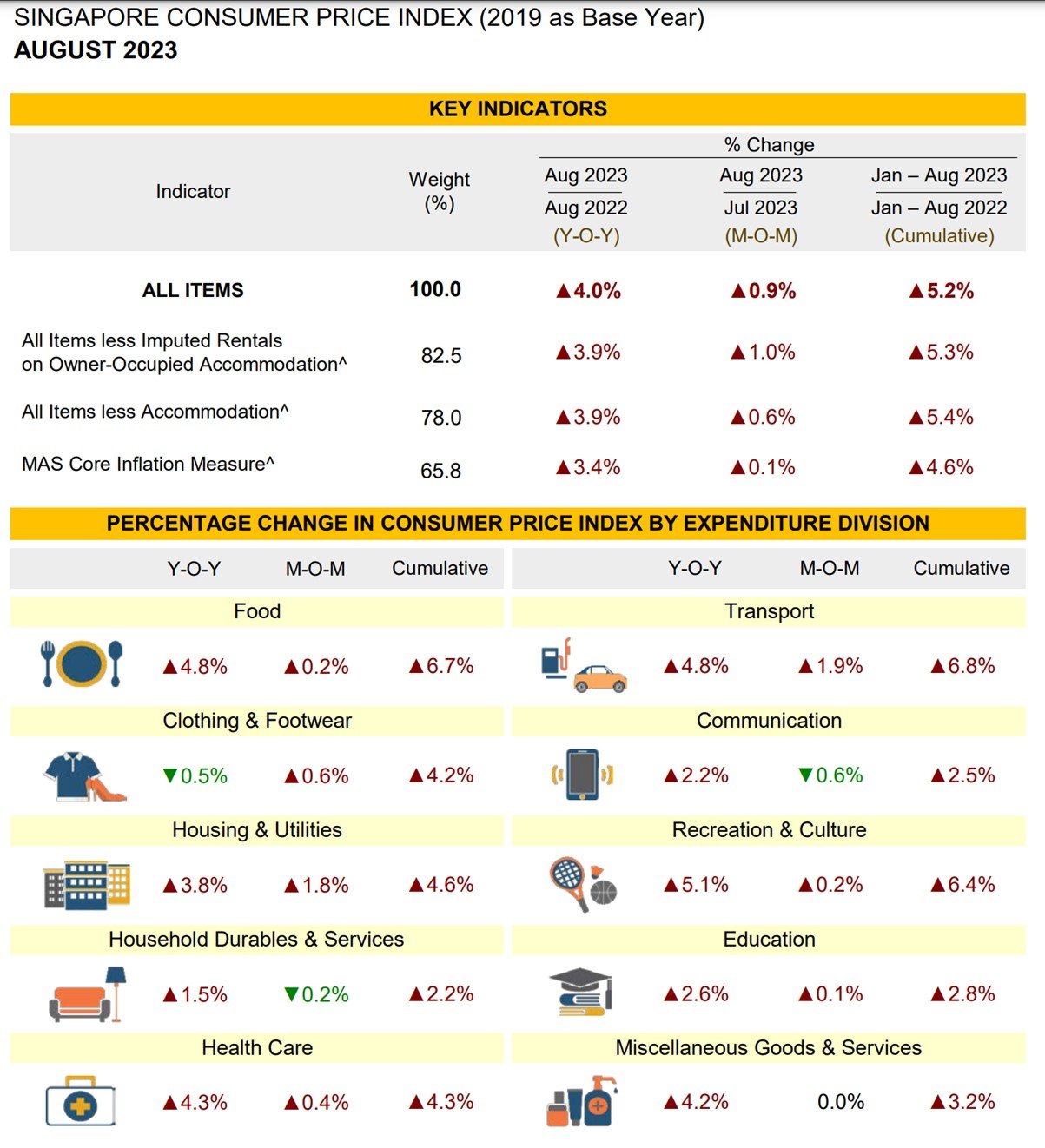

I’ve extracted the latest CPI (inflation) numbers below.

You’re looking at 5.2% year to date inflation (vs last year).

5.2% increase in the average cost of living!

Okay, you may argue that last year was a one-off because of COVID, and this won’t happen going forward.

Let’s say we conservatively assume a 3% inflation rate over the next 20 years.

Compounded.

This means that your $36,000 a year living expenses today.

Will be $65,000 in 20 years time – at 63.

So now you’re at 63, with another 20 years to go.

And the portfolio is only generating $50,000 in income, because remember you’re just buying short term cash instruments like T-Bills with no growth potential.

Where’s the other $15,000 going to come from?

How to solve these problems?

So how do we solve these problems?

Simply put, we need to:

- Increase the duration of the investments – avoid refinancing risk every 6 months

- Build in growth into the portfolio – the dividend should grow over time to match inflation

Both carries risk.

If you increase the duration, and pick investments that can grow over time.

By it’s very nature you are buying more speculative investments.

This also increases the costs if you’re wrong.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

If I were to do it? Low risk dividend portfolio?

But let’s say you gave me $1.22 million.

Forced me to build some kind of dividend portfolio to live off.

How would I do it?

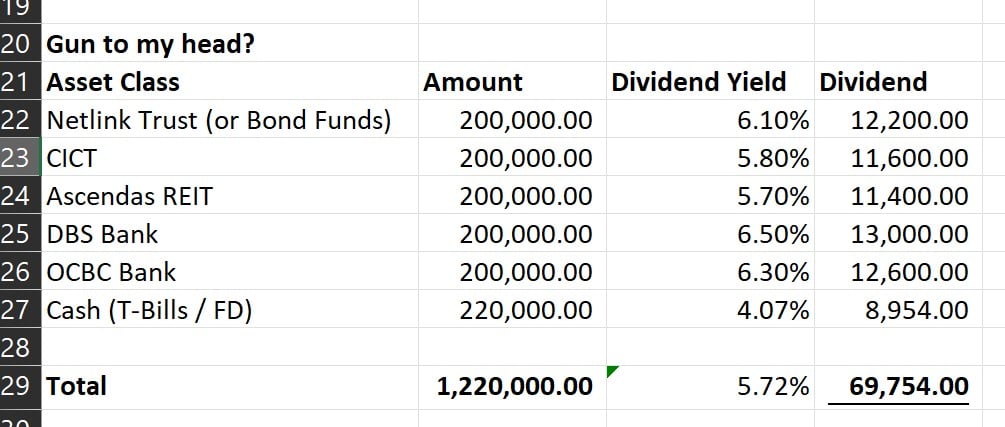

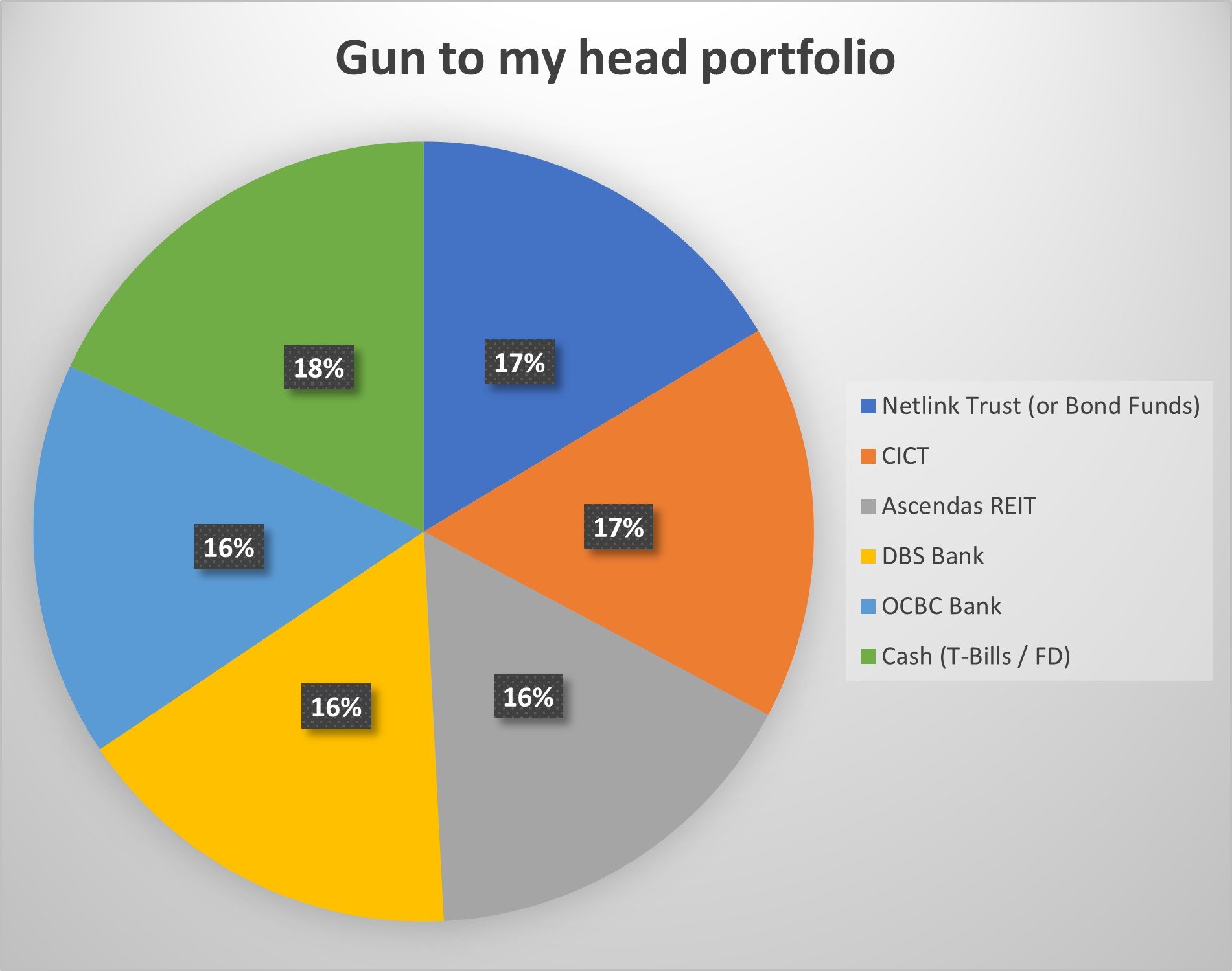

I’ll probably want to keep it simple, and stick to big names with strong balance sheets (limits the downside if you’re wrong).

I might go with something like the below (not financial advice):

That works out to a blended 5.65% dividend yield.

Or $69,000 a year in dividend income.

BUT – risk of dividend cut / capital loss is very real

The problem as you’ll note, is this.

Asset allocation is set out below.

Save for the 18% cash.

The remaining 82% of the portfolio is basically taking on some kind of equity risk.

A recession might get hairy… for dividend investors

If you get a recession, there is a very real risk of:

- Capital loss

- Dividend cut

Picture it this way.

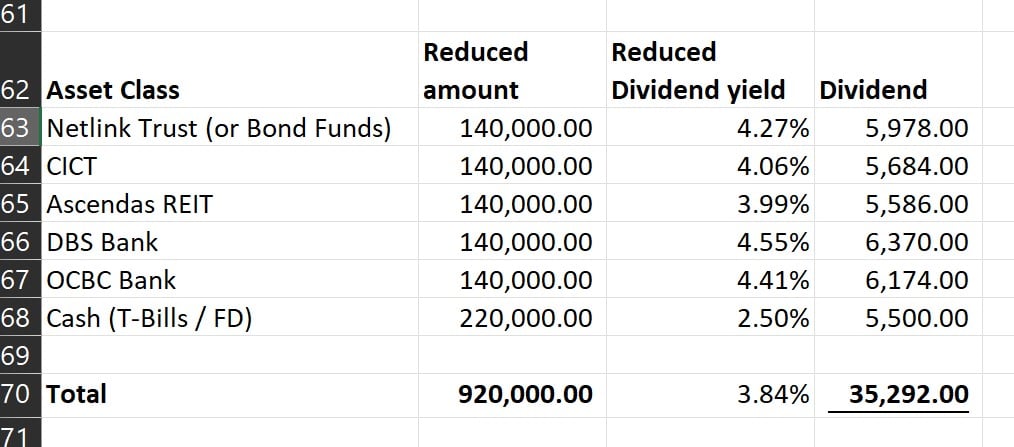

In 2024/2025, the Fed higher interest rates have finally triggered a recession.

This triggers a 30% drop in portfolio value – meaning the $1 million stocks is now worth $700,000.

At the same time interest rates get cut in the recession.

So T-Bills yields drop.

Because of the recessions, the DBS / OCBC also cut their dividends, as do the dividend stocks (let’s say a 30% dividend cut).

This is what the numbers look like now.

Portfolio value drops to $920,000 (from $1,220,000).

Dividend income drops to $35,000 (from $68,000).

How would you react in a scenario like that

Try to picture this happening to you.

How would you react in a scenario like that?

Do you know what to do next?

Do you sell everything and lock in the loss, to move into something safer?

Let’s say you decide to hold – and the recession only gets worse, and the stock prices continue to drop?

At what point do you start to panic?

In the long term, recessions / stock market panic is a certainty

Now over the course of a 40 year investing horizon.

Recessions are not merely a possibility.

They are an inevitability.

Assuming conservatively 1 recession every decade.

You need to last through at least 4 of the scenarios above – over the next 40 years.

Dividend based investing looks very different this decade vs last decade

A lot of dividend based strategies worked well over the past decade and a half – because interest rates were stuck at rock bottom.

This kept inflation low, and a REIT paying a 5.5% yield was basically paying a 4% spread vs the risk free (1.5% 10 year yield).

You’ll notice how many dividend investors the past 15 years basically went all-in after 2008, and bought REITs heavily from 2008 – 2018.

Which appreciated strongly in an era of zero interest rates, enough for them to retire and live off the dividend income today.

If you use the same tricks today…

Today, inflation sits at 5%

10 year interest rates sit at 3.5%

That’s just a complete sea change.

If you did the same thing investors did 15 years ago and expect the same results.

Well, I wish you all the best.

My personal view – dividend investors are underestimating the impact of higher interest rates on both (a) living expenses, and (b) asset prices / dividend income.

The solution in view, is either:

- Have a big margin of safety (a bigger portfolio to start with), or

- Embrace the volatility – Become a better/more active investor (not easy, and not for everyone)

Or… Build in a margin of safety

To illustrate this point.

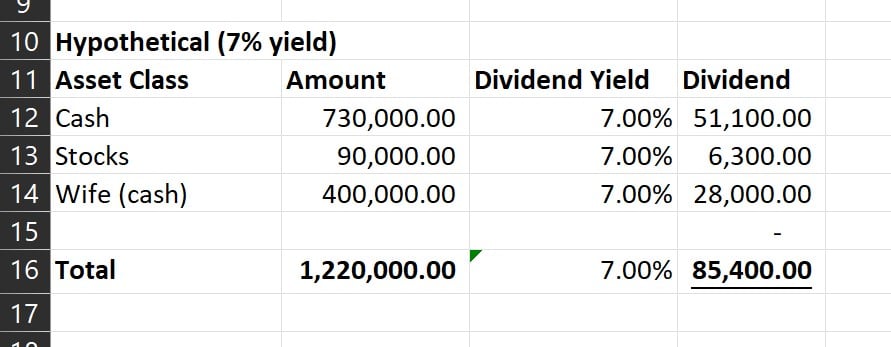

Let’s say you invest the $1.22 million into a 7% dividend portfolio.

Suddenly you’re looking at $85,000 a year in dividend income.

With a margin of safety like that, that’s a lot of room for expenses to go up the next decade or two.

Managing a 7% dividend portfolio for the next 40 years is not easy

The problem though, is that managing a 7% dividend portfolio is not so straightforward.

Most people think of it as buying a portfolio, forgetting about it, and collecting the income for the next 40 years.

Nothing could be further from the truth.

If your only stocks are Singtel (bought at 3.75) and Keppel Corp (bought at 7.25), I’m not so sure if you will be able to actively manage a dividend portfolio to generate 7% a year, for the next 40 years, as your sole source of income.

Would I do it? Retire with this dividend portfolio?

If I were in this reader’s shoes.

Would I retire today and live off the dividend portfolio?

The risks are very real, and include:

- Investments may not do well due to poor picks

- Expenses may go up (due to inflation or unforeseen circumstances)

- Recession causing the value of the investments to plunge and dividends to get cut

From a pure investment perspective, I don’t think the numbers work out well – there’s just not enough of a margin of safety.

But… what are the motivations of the reader to retire now?

But then again, I’m also not the reader, and I also don’t know what his motivations are for wanting to retire now.

Maybe he absolutely detests his job.

Maybe he wants to retire and spend time with his young children.

Maybe he wants to retire to start a business that he’s passionate about.

I have no clue.

So what I would say is this.

From an investment perspective, I think the numbers above are a bit tight.

You either want to have a bigger pot to start with, or you want to have a higher dividend yield (which requires more active investing due to the higher risk).

But there’s also the push factor.

If there is really a compelling need to make this work.

Then I suppose never underestimate human ingenuity.

Don’t forget that is a fully paid up house with no debt, so if things really get hairy that could come in handy too.

There is also always the option to cut expenses, or to work a part time job if things work out poorly.

How much would I want ideally?

I thought about it a bit more.

And I think the safe number here is $2.5 million.

Even if you invest that all at a 4% yield, that’s $100,000 a year.

Double the “ideal” expenses of $50,000 a year.

If things go wrong, you also have the option of withdrawing from the principal to fund living expenses.

But yes, I get that this is double of what this person has, and may or may not be realistic.

Which is why I brought up the motivations point above.

Is your push factor to leave your job, greater than the fear of running out of cash?

This article was written on 29 Sep 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 2000 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 2000 free fractional shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

I’d say the biggest financial risk he’s running is divorce. Most women generally don’t want their husband doing nothing and earning nothing.

Hahaha, well that’s for individual investors to decide for themselves what they want to do with their life!

With combine $1.2M , assume cash was $1M with 3.2% interest ( easily can find some safe haven product such as 1 year Tbill or insurance ),you can get around $32k per annum conservative. The other $200k stock earn you 5% dividend in which Singtel and Kep corp can match this number and earn you $10k per annum. Minimum you should have total $42k , with some adjustment ,to generate $50k should not be a problem. Financially you are ok but mentally , are you ready? Like my case, i only retire after i met both condition, financially on both of our saving and passive enough to cover us for the next 30 year ( excluded CPF and SRS withdrawal after 65 year old) and 2nd condition, both of us retire together which we are glad we able to meet it as if only 1 retire and the other still working , then don’t retire cause no point.

Agreed. Numbers aside, I would say to not underestimate the mental aspect.

Early retirement may not be for everyone!

Did the person mentioned how much cpf they have?

No not mentioned. This would be additional upside I suppose.