We’ve been doing quite a few individual REIT level posts of late because of the sharp drop in REIT prices.

So for this week I wanted to take a step back.

Let’s look at the broader macro picture for the economy and financial markets.

And let’s talk about how the next 12 months might play out for financial markets.

What are the possible paths, what are the big risks, and how to position as investors.

This was a Premium article written for FH Premium subscribers (formerly Patreon) in early November.

Quite a few of you have asked for a “preview” into FH Premium content.

So I decided to release this article for all readers, to give you insights into how I am approaching 2024 from a macro perspective.

If you find content like this helpful, do sign up for FH Premium for timely and updated content like this.

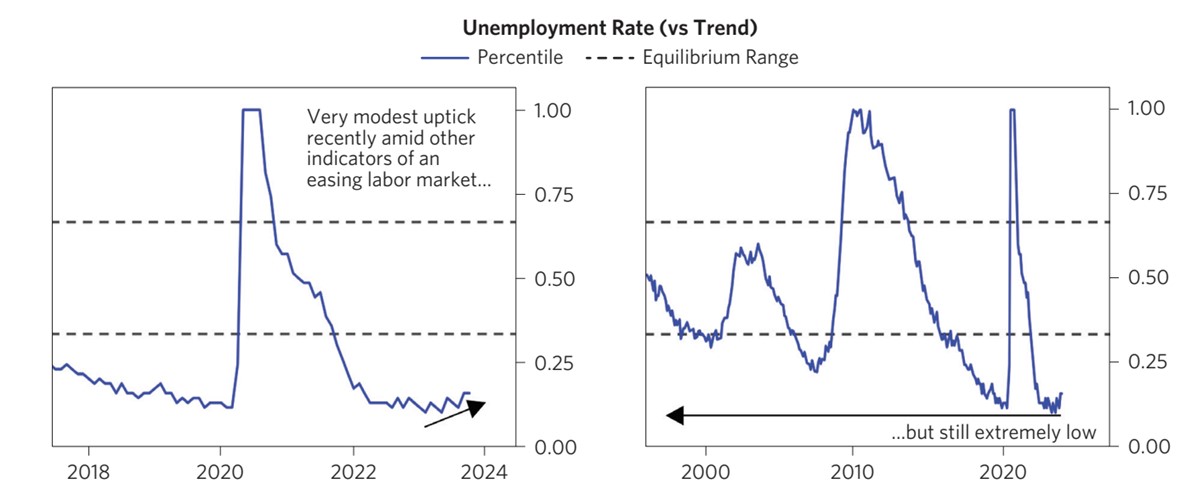

Singapore is impacted by both US and China

Now Singapore is unique because we are impacted both by the US and China.

US because US interest rates determine Singapore interest rates heavily (and fund flow).

China because China’s economic slowdown will impact the entire Asia region (and consequently Singapore).

So let’s take some time to discuss both.

What are the known unknowns for the global economy?

Let’s start with the known unknowns.

These are risk factors that we can already see in play today, but we don’t know exactly how they will play out the next 12 months.

Broadly, there are 3:

- Slowing US economy

- Israel-Hamas conflict

- US 2024 Elections

Slowing US economy

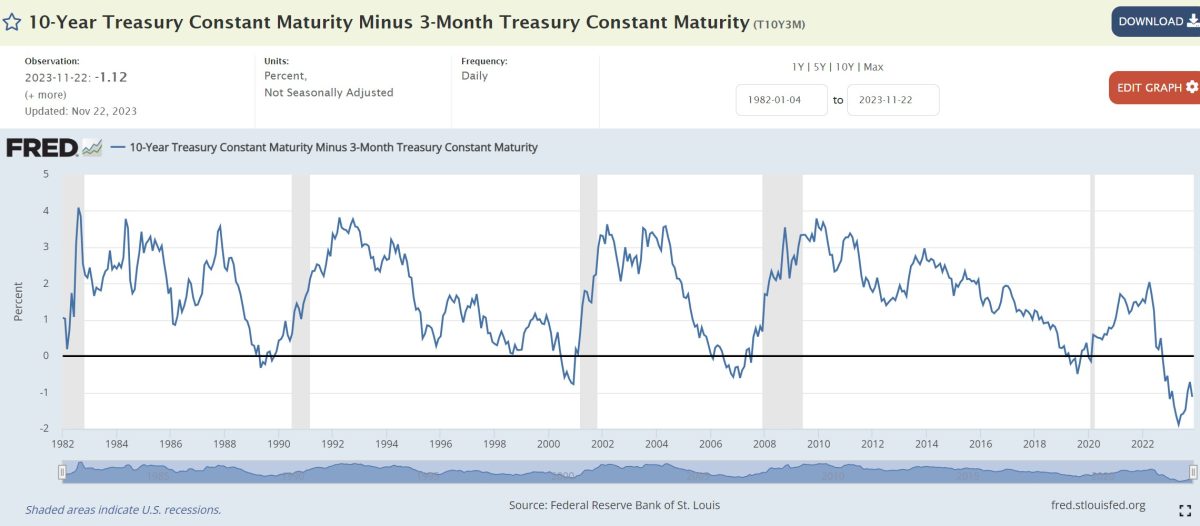

It’s still relatively early days, but leading indicators do point towards early stages of an economic slowdown, that is likely to hit around Q4 – Q1.

Timing wise this is broadly in line with my previous forecasts, and the yield curve timing of 6 – 12 months after re-steepening of the 3s10s yield curve.

Most of the data backing this up is soft in nature (for eg. Company earnings guidance, management forecasts being lowered etc – as you would expect given that the slowdown still lies ahead).

Some data points include:

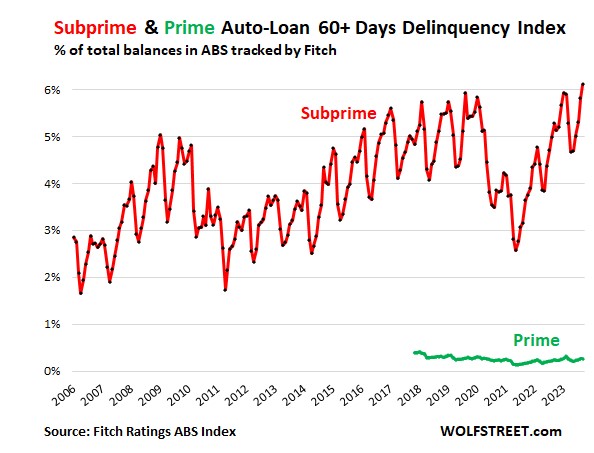

- US subprime auto and credit cards issuers reported significant declines in Q3 profit, due to higher loan loss provisions

- Auto loan delinquency hitting pre-COVID highs

- Luxury sales peaked in 2Q 2021 and have been going down since (globally). Recent earnings calls have pointed towards further slowdown ahead

- Management is guiding down on forward earnings due to uncertain impact of higher rates (eg. Tesla guided for lower EV sales moving forward)

Don’t forget it always starts at the fringes with the weakest consumers and spreads from there.

Q3 GDP growth was likely the peak in US economic growth, the only question now is how much the US economy will slow down by in the next 12 months.

And that point is still not very clear, as it will depend very much on (1) Federal Reserve actions, and (2) US government fiscal stimulus in an election year.

If Feds / US govt stimulate early in the face of slowing growth, that will produce a very different outcome from one where Feds / US govt focus on combatting inflation even in the face of slowing growth.

Israel-Hamas conflict

I’ve talked about Israel-Hamas a fair bit in recent articles, so I won’t belabour the point.

Base case, I still don’t think this will escalate into a regional conflict.

But war is by its nature unpredictable.

Every day that goes by, with a ground invasion by Israel, with images of conflict being broadcasted globally, and with all that US firepower concentrated in the Middle East, you just cannot rule out a miscalculation here.

If there is a regional escalation, then all bets are off – in such an event the price of oil can rise materially, and impact inflation and economic growth.

This is a low probability event, but with big consequences for global markets if it materialises.

US 2024 Elections

And to top it all off, you have a 2024 US election.

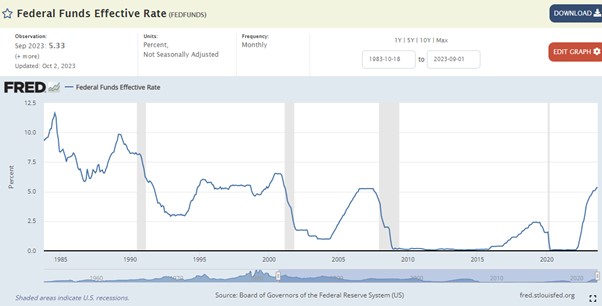

The problem now is that despite running record fiscal deficits, and despite interest rates being at 5.5%, the US government shows no signs of cutting spending.

If they continue to spend heavily into an election year, this could keep economic growth chugging along (due to government spending).

However, this deficit needs to be funded via the issuance of more Treasuries, which could send long term interest rates even higher (which is not good for financial assets).

What are the unknown unknowns for the global economy?

Contrast that to unknown unknowns, which are risks that you may not be able to predict specifically until it materialises.

For eg. In 2008 the subprime contagion was a known unknown, but Lehman going bankrupt in Sep 2008 was the unknown unknown that set it all off.

By its very nature, we don’t know what we don’t know in this category.

But what we do know, is that interest rates went from 0% the past decade, to 5.5% in the fastest Fed hiking cycle in the past 40 years.

We’ve already seen Silicon Valley Bank, UK Gilts, crypto, US commercial real estate etc break – it remains to be seen what else will break from the rapid tightening cycle.

How will the next 12 months play out?

Based on what we know today, it is likely that inflation will come down to the 3% range, and economic growth will slow, by the first half of 2024.

The question then is what happens after that.

Here I see 2 possible scenarios:

- Scenario 1 – Hard landing

- Scenario 2 – Slow Grind Down

Scenario 1 – Hard Landing

Under this approach, US economic growth weakens in Q4 – Q1.

The Feds don’t cut interest rates despite slowing economic growth.

We also don’t see big fiscal support from the US government.

Higher rates will slowly take their toll on the US economy, further impacting economic growth.

Under this scenario you could see a normal run of the mill recession (run of the mill being more like 2000 rather than 2008, which was unprecedented).

The exact impact will vary across industries, but by and large you may see 20 – 30% earnings declines and peak to trough stock declines.

Given that this is a recessionary outcome, stocks won’t bottom until the economy bottoms out, which is typically 12 – 24 months after Fed interest rate cuts.

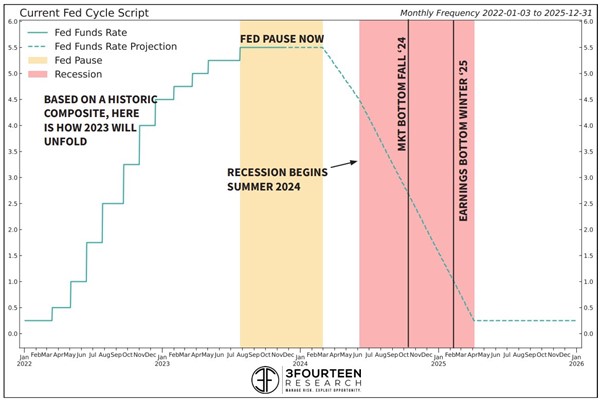

There’s a nice chart below that shows what typically happens in a hard landing (this is averaging the recessionary outcomes over the past 40 years, and gives you an idea of how it would play out if the averages hold).

What I would add, is that if this is going to be a typical hard landing outcome.

Then be very wary of the first 0.5% – 0.75% of interest rate cuts.

The first 0.5% – 0.75% of interest rate cuts usually results in strong market performance – as the market sees interest rates go down while economic growth remains strong (for eg. the market performance the past few weeks as long end rates dropped 0.5%).

It is the next 0.5% – 0.75% of cuts that causes problems – as they come when economic growth is slowing, and market worries about recession more than interest rates.

Scenario 2 – Slow Grind down

The main argument against the hard landing outcome.

Is that most of the data we rely on today are based on the past 40 years.

And the past 40 years was a singular regime of low inflation, where the solution to every economic recession was to cut interest rates.

And you may point out that today’s world is very different due to inflationary factors arising from:

- East-West decoupling

- COVID disrupting global supply chains, labour flows etc

- Massive fiscal stimulus from governments

- Historically tight labour markets

- Green energy transition

In every cycle market participants always think that “this time is different”.

But given the unprecedented nature of today’s world, I think there is a good argument that this cycle is indeed different.

Bridgewater in their research (here and here) paints the most plausible alternative to the hard landing that I have seen.

What Bridgewater thinks may happen in the next 12 months, is:

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

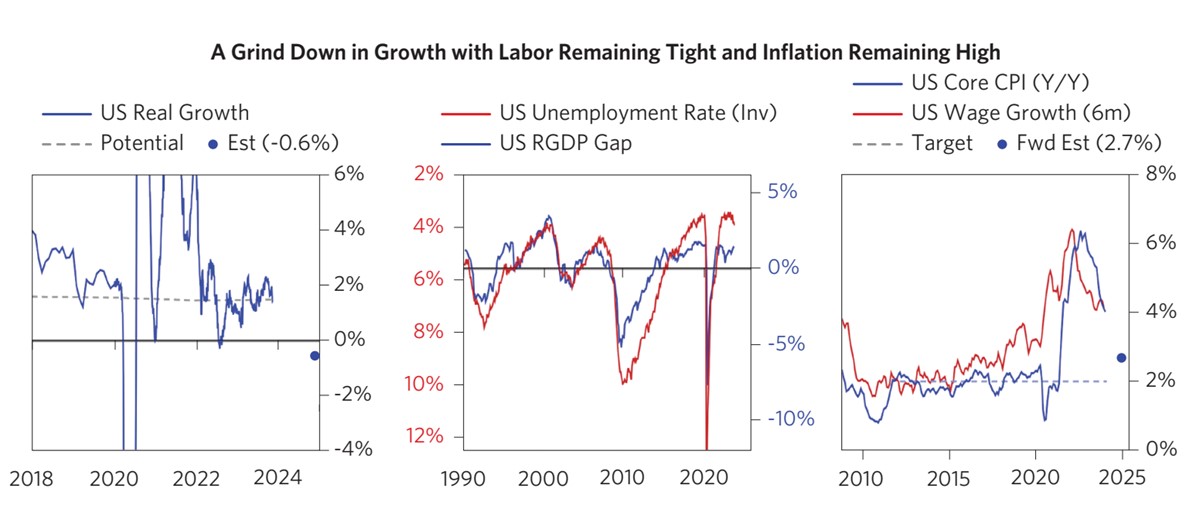

Slower real growth (but no collapse in economic growth)

Bridgewater expects higher interest rates to grind on household and corporate cash flow, resulting in slower real growth (estimated -0.6%).

But they do not expect an outright collapse in economic growth (like 2000 or 2008), because:

- the labour market remains tight, and

- employment income does not collapse from current levels.

Sidenote that a recession is defined as negative real (inflation adjusted) growth. So when inflation is running at 3%, you can have an economy growing at 2% and still be in recession, but for all intents and purposes the economy is still growing at a slow rate (nominal).

Sticky inflation in the 2-3% range

However given how tight labour markets are globally.

This small negative growth will not be sufficient to break labour inflation.

Bridgewater forecasts inflation to stay in the 2% – 3% range (2.7% estimate), despite a mild recession (-0.6% real growth).

Feds not able to slash interest rates (unlike typical recession)

Because of that.

Bridgewater believes this cycle to be fundamentally different from every other cycle the past 40 years.

In that the Feds will not be able to slash interest rates rapidly into a mild recession.

For the main reason that (a) economic conditions are not bad enough to justify large interest rate cuts, and (b) such cuts would allow for the return of inflation which has not been properly tamed.

So you may have a scenario where:

- Growth is flat and slightly negative

- Inflation remains in the 2 – 3% range

- Feds not able to cut interest rates meaningfully (only down to 4%+ rates)

Gun to my head, I think outside of a hard landing, this is probably the next highest probability outcome.

What do you want to own in each scenario?

I’ve gamed out how various asset classes perform under each scenario below:

|

|

Scenario 1 – Hard Landing |

Scenario 2 – Slow Grind down |

|

Cash |

Good |

Good |

|

Short duration bonds (<2 years) |

Good |

Average |

|

Long duration bonds (>10 years) |

Good |

Average |

|

REITs |

Depends on how bad recession gets |

Average (interest rates stay high, but you get yield) |

|

Tech |

Depends on how bad recession gets |

Bad (interest rates stay high, you don’t get yield) |

|

Cyclicals (eg. Banks, Industrials) |

Bad |

Average |

|

Commodities |

Bad |

Average |

|

Gold |

Good (due to risk-off) |

Average (interest rates stay high) |

To sum up:

- Cash does well in both scenarios, as you’re getting paid a decent yield, while having full flexibility to respond based on what happens next

- Bonds do very well in a hard landing if interest rates get slashed, but may not fare so well in a slow grind down if rates stay high / go higher

- REITs / Tech depend very much on the economy and interest rates

- Cyclicals like banks and commodities depend very much on the economy

- Gold does well in a hard landing risk off, but probably flat in a slow grind down

For specific insights into individual stocks / REITs I am keen to buy and target pricing, do check out the FH REIT & Stock Watch.

What about China?

I was asked my views on China recently.

This was my response:

“I think the way I see it is that China is going through a secular deleveraging of the economy.

The underlying problem is structural – they have too much real estate debt (and too much reliance on real estate growth).

That is not sustainable, and they need to transition into more sustainable forms of growth. Via consumption, higher value add manufacturing etc.

That’s exactly what they’re doing today, but this takes time. Years at least.

And in the meantime, these new avenues of growth will not offset the hole from real estate.

Inevitable conclusion is that unless China decides to whip out massive stimulus (I don’t see this as likely), China will go through a few years of slower economic growth as they manage this transition.”

Incidentally, I was reading a research report by Bridgewater and they seem to share a similar view:

China is in the midst of a secular deleveraging that will likely take many years to work through at the same time as domestic and international political risk have risen markedly. After the initial bounce in growth earlier this year from the pivot away from zero-COVID, growth has slowed. Policy makers are transitioning the economy toward a consumption-driven model of growth. Overall, growth remains weaker than desired, as the debt overhang in the property sector remains a significant drag, employment growth has been modest, and savings rates have risen. Low inflation rates imply that policy can remain accommodative, but the prioritization of deleveraging some sectors and avoiding excessive leveraging up in others has limited the aggressiveness of the stimulus so far. Looking forward, we expect policy to remain easy but restrained. That said, the increase in risk and likelihood of slower growth are well discounted across the equity, bond, and currency markets.

Because this is a centrally managed economy, a big crash like Lehman will probably not be allowed to happen.

But there is no shortcut to the restructuring to be undertaken for the economy, which is why the China economy is likely to remain slow for a couple of years.

How to position as Singapore investors?

To sum up the above.

The China economy is likely to remain weak for a couple of years, and unlikely to be the dynamo to rescue Asia (unlike after 2008).

US economy can go both ways depending on how policy makers react – either (a) US economy goes into a recession, or (b) growth slows down (without an outright collapse), resulting in interest rates staying high.

Elevated cash levels

In a climate like that, elevated cash levels continue to make sense for 2 reasons:

- You can get 4% risk free – this sets a high threshold for new investments

- As shared above, there is a lot of uncertainty over what happens next, and elevated cash provides you the flexibility to take advantage of what is to come (with little opportunity cost)

Dividend names may make sense for long term investors

For investors with a long term timeframe.

Who use cash and no leverage.

I think there are attractive prices out there on dividend players like REITs.

A lot of the REITs are trading at COVID lows (or in some cases below).

You’re getting 6%+ yields on big names like Ascendas REIT or CICT or Netlink.

7 – 8% yields on mid sized names like Keppel REIT, Starhill Global, Keppel Infrastructure etc.

That’s a 3 – 4% yield spread vs the risk free, that you are paid while waiting for the next phase of interest rate cuts.

But depending on which of the 2 scenarios we see above, this may not be the bottom for REITs, which is why you need to take a longer term perspective and not use leverage.

You do want to focus on primarily Singapore real estate, and strong sponsors with a good balance sheet, because you don’t know how long rates will stay high.

The full list of names I am looking at is on the FH Stock / REIT watchlist.

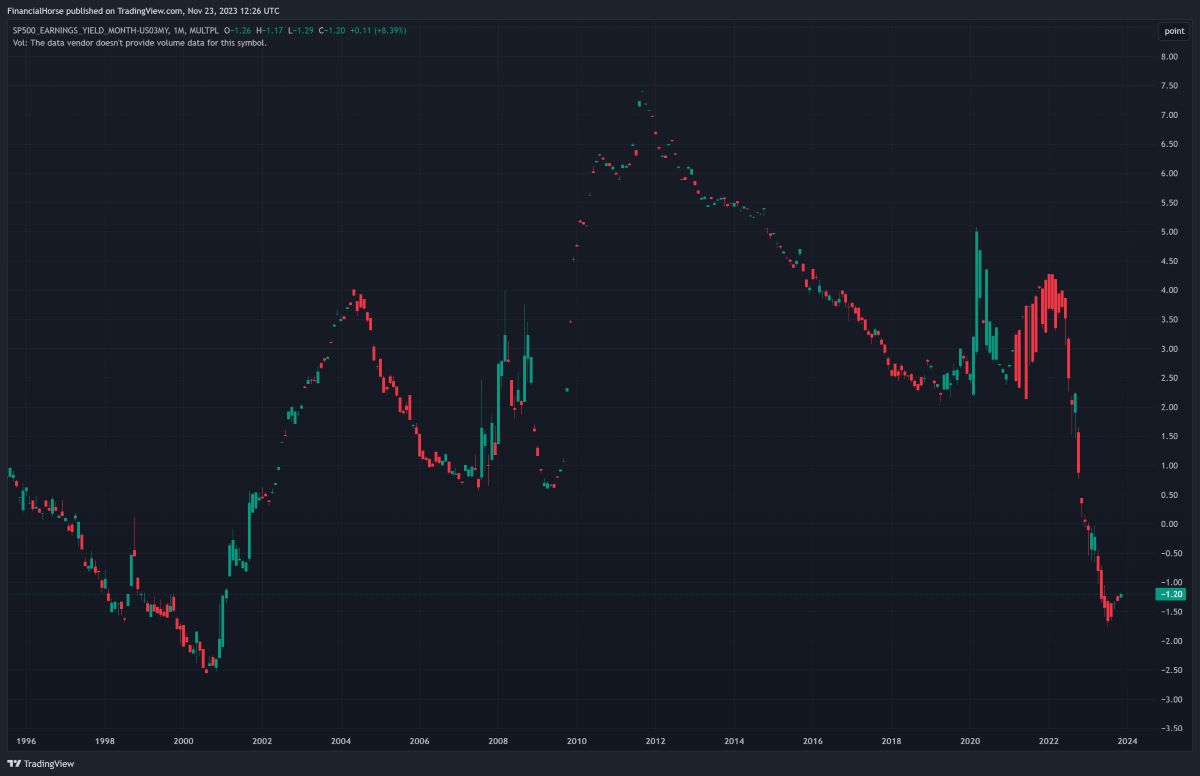

Equity risk premium too low

My main reservation with adding to equities in a big way here.

Is that equity risk premium remains too low given how high interest rates are.

The chart below shows S&P500 earnings yield minus 3 month US rates (a proxy for equity risk premium).

By this metric, stocks are the most overvalued they have been since 2000 – because they have not dropped in price despite the much higher interest rates.

And we gamed out the 2 scenarios above.

Either we get a recession and earnings come down – not good for stocks.

Or we avoid a recession and interest rates stay high – not good for stocks.

So unlike REITs / Fixed Income which have already seen a big sell-off due to higher interest rates.

I think stocks need to come down in price before they start getting attractive again.

But this is a 10,000 ft macro view.

No doubt there are pockets of opportunities within individual stocks / industries despite that overall macro outlook.

REITs, tech, AI, certain names in commodities, all look interesting enough to me.

The full list of names I am looking at is on the FH Stock / REIT watchlist.

This was a Premium article written for FH Premium subscribers (formerly Patreon) in early November.

Quite a few of you have asked for a “preview” into FH Premium content.

So I decided to release this article for all readers, to give you insights into how I am approaching 2024 from a macro perspective.

If you find content like this helpful, do sign up for FH Premium for timely and updated content like this.

WeBull Account – Get up to USD 5000 worth of shares (Best promo of 2023)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Hi FH,

Thanks for this interesting read! Have u seen the Goldman outlook?

I found it absorbing. They predict no recession. US stock valuations are also undemanding if you take out tech.

Asian and world valuations are below median.

Of course we know they are the vampire squid of banks in 2008. But it’s pretty smart and a nice break from our recession obsession!

Cheers,

Mrs Pennies

https://pugsandpennies.substack.com

Which outlook from Goldman in particular? There are quite a few.

Will definitely have a look as I love reading these macro pieces. That said I usually take the outlooks from the bulge brackets with a healthy pinch of salt. If your business model is based on convincing other investors to buy whatever investment you have to sell, it’s just bad business to have your research team calling for prices to go down. I don’t recall any of these shops calling for stock prices to go down in 2008’s outlook as well. 😉

At the end of the day, it’s just risk-reward. Sure maybe there’s no recession in 2024, but in that case which is the asset class that would give the highest upside? Whereas if we do get a recession, there are a lot of asset classes that look very juicy.

Lol, totally get it.

I forced myself to read the outlooks for the website. Otherwise… haha would rather do something else!

Most of the other bulge brackets calling for a recession.

Other than the GS Econs team.

OK, have a very merry Xmas to your team!

Hi FH,

You mentioned in the article that “stocks will not bottom until economy bottom.”

Could u kindly help me to understand this as I always hear is that stock market is forward looking about 6 months ahead of the economy? ie. which i thought market will bottom 6 months ahead of economy and will already be up when economy is in a reccesion ..

Thank you in advance!

kk Yau

The market will bottom when it is clear that the economy will bottom. In a financial crisis like 2008, it is not clear when the economy will bottom as it depends on how policy makers react. So for eg. in 2008 when the Feds/Treasury pumped in enough money to offset the deleveraging, that marked the start of the recovery for the economy, and so the market bottomed out there. Before that it wasn’t clear if policy makers would do enough to save the economy or if things would get worse, hence no bottom to the market.