2 months ago, I wrote on article on whether it was time to sell DBS Bank stock.

My conclusion then, was that I would consider selling if:

- 10 year Treasury crossed 2.5%

- US yield curves inverted

DBS was $36.5 back then.

Well, DBS Bank stock is $34.3 today.

And the 10 year treasury is 2.66%, and both yield curves have inverted.

Both my sell signals are triggered, so… Is it finally time to sell DBS Bank stock?

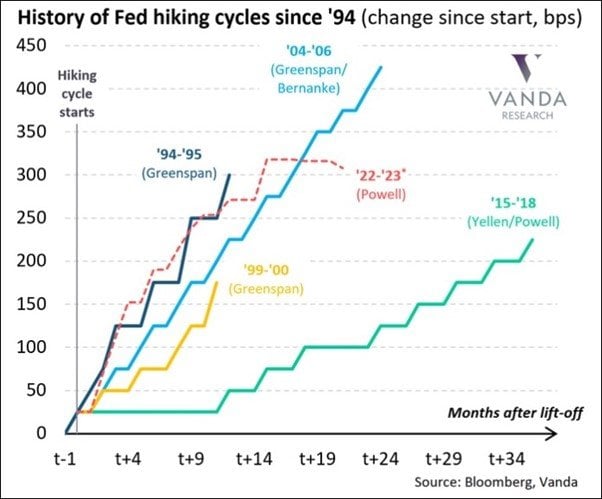

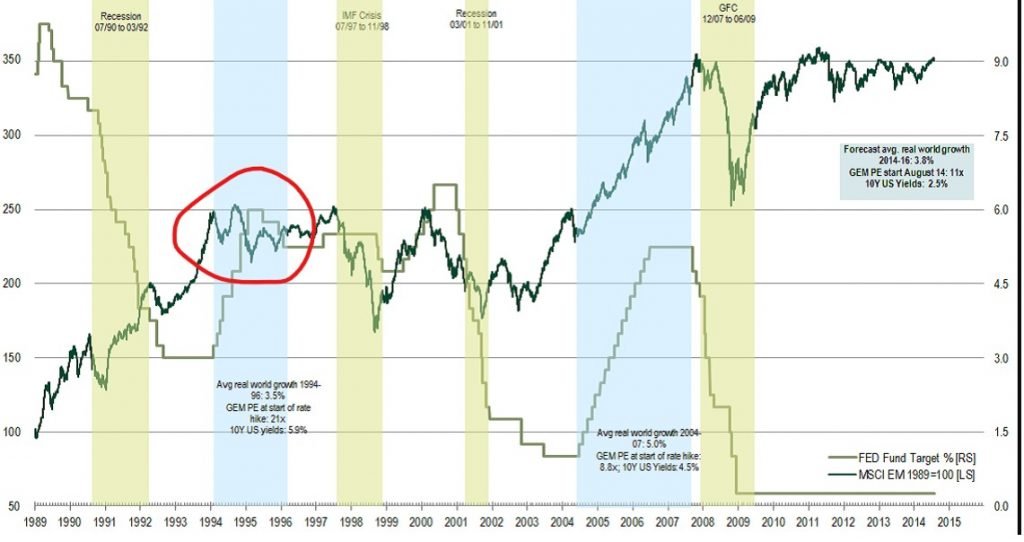

DBS Bank Stock peaks 4 – 8 months before US interest rates

If you look at the 20 year history of DBS, you’ll find that DBS usually tends to top out about 4 – 8 months before the peak in US interest rates.

Red arrow is the cycle top for DBS, and blue arrow is the top in US interest rates.

So if you want to trade DBS stock, you need to watch out very closely for the turning point in US interest rates.

And there, the signs are very worrying.

Yield Curve Inversion

The 2 key yield curves are the 2s10s, and the 5s30s.

Both have inverted:

Why is this important?

Historically speaking, every time the yield curve inverts, it starts the clock on a recession in the next 1 – 2 years.

BUT – taking a step back… in March 2020 we had the shortest market crash ever, followed by the fastest recovery.

Then we had a very short and hot 2 year business cycle.

And now we’re going into the fastest rate hike cycle in 25 years.

So what I’m trying to say, is that this business cycle has been very hot and very fast.

Which means the timelines for everything needs to be accelerated.

If you think you have another 1 – 2 years before things break, then well… that’s a very big if.

10 year Treasury yield at 2.66% – Why is this important?

Back in Feb, 2.5% was my line in the sand for the 10 year Treasury.

My thinking was that 2.25% was the cycle top back in 2018.

If you assume a slight overshoot, then 2.5%+ should be cycle top this time around.

At the same time – Fed’s estimate of the neutral rate is 2.4%.

If you assume 25bp to 50 bps overshoot, then the top should be 2.65% – 2.9%

10 year hit 2.66% this week.

So…whatever way you slice it, the 10 year Treasury (and yield curve) is sending a warning signal of late stage cycle.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

How does this affect DBS Bank Stock?

Okay big picture – banks suffer when (1) interest rates drop, and (2) economic growth slows.

Singapore interest rates are tied to US interest rates because of the impossible trinity (MAS gives up control of interest rates).

And given how exposed Singapore’s economy is, I think that if global economic growth slows, Singapore will not be immune.

What if DBS Bank Stock does not drop?

So… what needs to happen, such that interest rates do not go down, and economic growth does not stall?

2 scenarios I can think of:

- Powell’s soft landing

- Stubbornly high inflation

Powell’s soft landing

Easy one first.

The possibility that Jerome Powell can pull off the impossible – the fastest rate hike cycle in 25 years, to tame the hottest inflation in 40 years, without triggering a recession.

In this scenario, sure, DBS bank may drop 10-20%, but without aggressive rate cuts and recession on the other side, I don’t think the downside will be that big.

In such a scenario it would probably make sense to just hold onto DBS.

How likely is this?

The only time in recent history the Feds managed to hike without a recession was in 1994.

There – we had a very fast rate hike cycle, but there was no massive recession or market crash.

So it is not without precedence.

Hard yes, but not impossible.

Stubbornly high inflation

And the more tricky one – what if despite all the rate hikes, inflation just refuses to go away?

What if Larry Fink is right that we are moving into a period of deglobalisation?

And that the path forward is one of persistent supply chain disruptions, and stubbornly elevated inflation.

Will governments step in with fiscal stimulus?

Ever since COVID governments have discovered the power of fiscal stimulus.

They’ve realised that in a world where you can print money, there’s no need to go through economic pain, ever.

But the world is never so convenient.

If money is unlimited, this simply moves the limiting factor elsewhere.

And as we are seeing, that factor is increasingly becoming commodities.

You can print money, but you cannot print oil.

Or fertiliser.

Or copper.

If we go down this path, commodity prices may go even higher.

If inflation stays high, the Feds cannot ease monetary policy.

The result may be stagflation – high interest rates, high inflation, low / negative economic growth.

Do you want to own DBS Bank in stagflation?

Truth be told – it will probably still do better than alternatives like growth stocks.

But will DBS stock outperform say gold, commodities, or physical real estate in stagflation?

I frankly don’t know the answer to this one.

If you sell DBS Bank stock, what to do with the money?

Which brings us to the big question.

If one is to sell DBS bank now.

Where does the money go?

I see 3 big options:

- Cash

- Commodities

- Growth stocks/REITs

If you go into Cash – you are doing market timing.

You are saying that a big market crash is going to come, I’m going to cash, and I will use the cash to buy DBS back cheaper next year.

If you go into Commodities – you are betting on the stagflation / stubborn inflation scenario.

You are saying that hey inflation is going to be a real problem, and my commodities are going to outperform DBS Bank in this scenario.

If you go into growth stocks/REITs – you are betting that the Feds will be able to tame inflation, and move back into easy monetary policy.

And we party like it’s the 2010s, where FAANG, REITs and tech does well.

(Okay I get that there’s a slight nuance with REITs because being backed by physical real estate, they can do well in inflationary scenarios. But REITs short term are still very sensitive to interest rates.)

Is it time to sell DBS Bank Stock?

A lot of people ask this question like it’s a yes no answer.

But in investing, it’s sometimes more to do with how much you make when you are right, vs how much you lose if you are wrong.

What is the downside of selling here?

The downside of selling DBS Bank here, is the dividend + capital gains from now until the point where you buy back in.

Let’s say you go to cash for 1 – 2 years.

You’re missing out on about 5% worth of dividends, and maybe 10-15% capital gains?

Don’t forget DBS is at 1.6x book value here, so the upside is not that high too.

Which means that if everything goes well, you only lose 20% of potential gains by selling DBS here, give or take.

What is the upside of selling here?

What if you are right?

If the market is right and the Feds are hiking into a big economic slowdown, losses for banks could be quite horrendous.

But of course, the exact amount you make depends on how big the decline is, and how effective you are in buying the bottom.

And at this point in time, I would not be confident calling how big the decline for DBS would be if things do play out as feared.

Much will depend on the pace of economic slowdown and interest rates.

Ballpark numbers – If DBS drops to the $20s range the next 2 years, and recovers to $35 in time.

The buy and hold approach would have 0% returns (excluding dividend).

The timing approach would make about 30-60% returns (excluding dividend).

It really depends on your individual asset allocation

There’s no denying we are very late in the business cycle.

Over the next 12-24 months, there is a real risk something breaks, and there is real risk of a recession (or at least an economic slowdown).

But it is by no means a done deal. Feds have shown us in 1994 that you can hike without a recession.

The more I explore this question, the more I find that the answer needs to be tied back to individual risk appetite and asset allocation.

If you are very overexposed to risk assets, and your risk appetite is not high, it may make sense to dial back.

But if you are very heavy in cash, and your risk appetite is high, it may not make sense to dial back any further.

If you get what I mean…

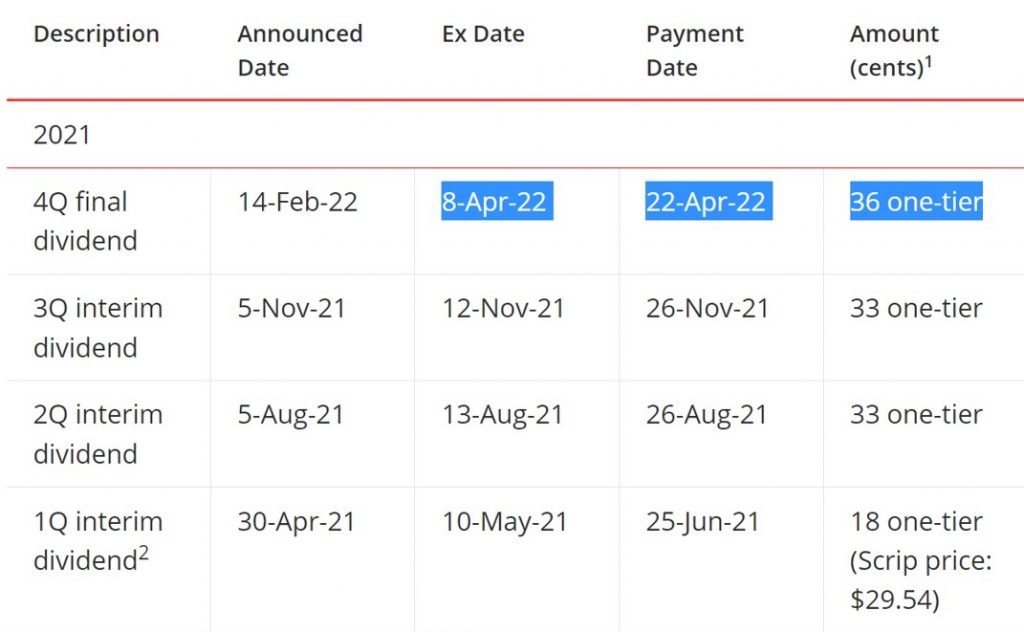

DBS went ex-dividend

Funnily enough, DBS went ex-dividend literally yesterday on 8 April 2022.

The dividend was only 36 cents, and yet DBS tumbled a whopping 96 cents.

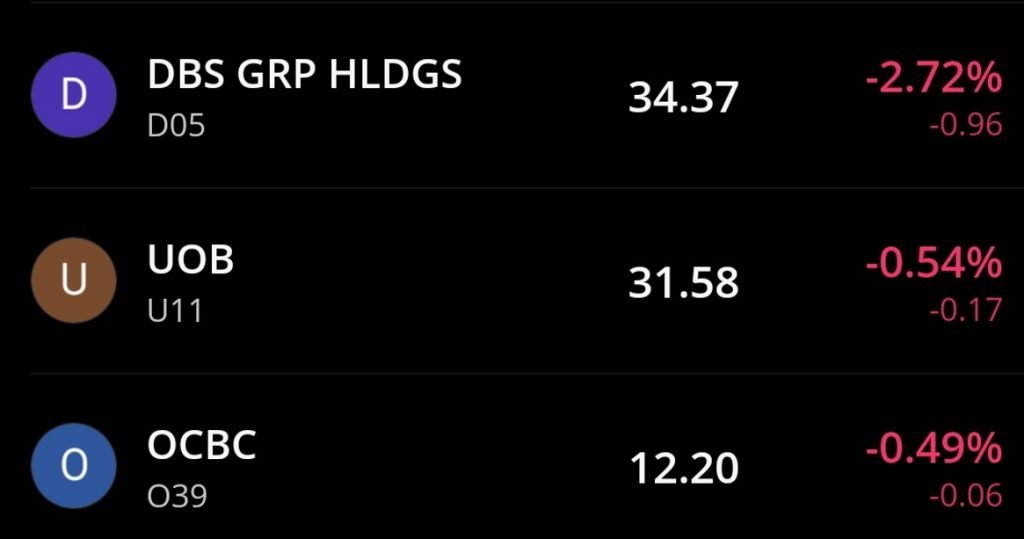

You can see the relative performance to UOB and OCBC below.

Seems like other investors have similar views, and have been waiting for the dividend to exit their positions.

Will I sell DBS Bank Stock now?

As always – my asset allocation is available on Patreon so do check it out if you’re keen.

I am holding elevated cash positions at the moment, so just holding on to DBS and riding through the cycle is an option.

That said, my 2 bank positions are DBS Bank and UOB Bank.

And I think that if we do get a strong rally from here, I might just start to trim those positions.

We are getting very late in the cycle, and risk-reward for holding onto banks has gotten less attractive.

I don’t see myself selling them completely, but trimming 10-30% of the position and reducing exposure may make sense.

My view at least.

And you can see my stock watch with regular updates on portfolio moves (including where I rotate into if I do sell DBS/UOB) on Patreon.

For what it’s worth though – I do think the decision to sell/hold needs to tie back to your asset allocation so there will not be a one size fits all answer.

But FH… I am buy and hold…

Just for the record, I know many of you are buy and hold investors.

In such a case, there is absolutely no action required at all.

DBS is a fantastic, long term stock, backed by Temasek.

You can hold it for 50 years through multiple business cycles, and pass it on to your children.

That is perfectly fine.

This analysis above was intended more for those who do want to trade DBS stock based on the business cycle.

Closing Thoughts: Market has gone crazy with rate hikes pricing

Market has gone absolutely bonkers with pricing in rate hikes of late.

They’re pricing in 9 hikes by December 2022.

And rate cuts to start as early as middle of 2023.

Working backwards, it means that the market doesn’t expect the current hiking cycle to last much more than 1 year.

Again – what did I say about a short and furious cycle?

So while the analysis above was done for DBS Bank Stock, you can do the same for any cyclical stock out there really.

UOB Bank, OCBC Bank. Semiconductors. Industrials.

Anything that is sensitive to the economic cycle.

Market is telling us that we are very late in the cycle, and it would be wise to heed that warning.

As always, this article is written on 9 April 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

$20 really? You expect DBS to drop to that level, just $4 above the COVID low? Seems a bit of a stretch to me.

No that is just an illustration. It is not easy to call how big the decline will be at this point in time. Much will depend on the events to come.

I have updated the article to clarify this is just a ballpark figure.

Cheers

I sold half of my DBS position and rebalanced into some beaten down REITs a couple of months ago. Decent profit from a very cyclical stock. No point being greedy.

Yes, am inclined to agree with this. 😉

Hi FH. Great post once again. Just want to comment on supply chain re-shoring and inflation. This is a long drawn out process, it’s not going to happen overnight like the pandemic did. So yes, price levels are going higher, but the Rate of change might not be undigestibile for monetary policy. I think the ‘endgame’ is clear, but the rate and pace of progression needs to be well thought through as well. So while Fink may be right, I think he might be wrong that factories can move overnight, and the CPI goes up 2% because volkswagen has a factory in Canada, or something liket that.

Also, any considerations on long term treasury? Because after the QT spike, which is happening right now, long rates for sure are going to fall as growth begins to slow down. And the next easing cycle will bring rates back to the floor.

That’s an interesting point, thanks for raising this. Whatever the case, I think we can agree that the inflation outlook here is very uncertain! Huge range of possibilities.

TLT is interesting. I think at some point in the cycle it could be a good trade, but the timing is crucial. I still think now is too early for the long bonds trade, I would want treasury yields to go even higher before I pull the trigger on that one.

Nice analysis again, FH!

What is your take on banks in general going forward? Rising interest rates mean rising NIM and greater profits for banks but recession means lower profits. So is banking as a sector in general still attractive to invest in? I am not referring to local banks which I think are all already fully valued but banking in general globally.

Trying to think whether it makes sense to invest more in the sector in an inflationary environment.

Good question. I think whatever one’s view on banks, we need to acknowledge that the uncertainty level has gone up, and the range of possibilities (esp around inflation) is quite high.

I think if you take a mid term view, say 3 – 5 years, banks should still do well. Higher rates, higher inflation, that’s a good set of macro conditions for banks.

Where it’s tricky is the short term. 1 – 2 years. If we do get a recession/slowdown, that could hit bank earnings.

That said, if the idea is to bet on inflation, commodities might be a cleaner trade, and with potentially more upside as well. At current P/B levels of banks, frankly can’t see them doubling from here anymore. But of course commodities have their own problems as well, and may suffer if we do have a recession.

Thanks for the great analysis.. When you mentioned commodity, does entering into counters like Wilmar or Olam in line with that hypnosis?

Thanks for the kind words – yes, those will count as well.

You mentioned you own DBS and UOB, ever though of trimming DBS and adding some OCBC? In time of uncertainty, cash is king, are you uncertaint now? 🙂

Yes, I think the next 12 months are very uncertain, the range of possibilities here is very high. High inflation, fast hiking cycle, QT, and high frequency indicators showing a slowing economy are a very volatile mix.

Not a bad idea to position more defensively at least in the short term.

Interesting idea about trimming DBS and adding OCBC. But that’s more of a stock level analysis. If the macro analysis here plays out, both DBS and OCBC should benefit (or suffer) equally.

Why is yield curve inverted, 2-year is at 2.54% and 10-yr at 2.71%?

Yes the yield curve inverted briefly and then steepened.

Dear FH

Thanks

I would say that there are no safe and more rewarding options as alternatives if you sell the local banks and want to redeploy the proceeds

Most of the “well managed” local REITS are already up with compressed yields and have limited upside from here

In the event of a 2023 recession, they will also fall despite inflationary forces as general sentiment, reduced disposable incomes and other issues will come into action

Staying in cash and trying to speculate on lower entry points is prone to not only execution risk except for the highly disciplined but also not advisable with inflation and loss of dividends etc

DBS trades at a premium to the other two always and although 1.6 P/B is historically high, there are simply no equally safe alternative options. OCBC under 12 at a P/B of 1 is an option if you want to ‘rebalance ‘ your bank allocation or even to add and UOB slightly lower is a buy

I will be precisely doing this and will not hesitate to add to my three banks as they will do well

As regards commodities, a significant pullback in oil is an opportunity but hard commodities have already run up and they will correct significantly if there is a recession. The war will end and soft commodities will fall back as well

To put it in a nutshell, stating the course and adding to banks will be what I do and a barbell approach of naturally hedging with Oil and REITS , when they drop with back to back FED hikes, is a reasonable strategy

Regards

Garudadri

Thank you Garudadri, this is a fantastic comment as always.

I do agree with the points you have raised. I am sitting on a comfortable cash buffer at the moment, so if we do have an economic slowdown / recession I do have the dry powder to make buys.

And like you said, there is the risk of getting too cute with cutting DBS positions, only to have no better place to deploy the cash.

Thanks for raising this, it is good food for thought. I might just hold onto my bank positions, and add if there is indeed a decline.

Did you sell in the end? Your market timing has been very good so far.

Sadly I did not. I have enough cash positions set aside from selling other counters though that I decided just to hold onto my DBS positions for now.