Keppel DC REIT is one of those REITs that I know a lot of Singapore investors love.

But me – I never really saw the appeal of this data centre REIT.

I always found Keppel DC REIT to be very richly valued.

And in real estate sometimes it doesn’t matter how great the real estate is – if you buy it at the wrong price you’re still going to lose money.

Well, since the 2021 peak – Keppel DC REIT has dropped almost 45%.

And since its high of $2.3 just in July this year – Keppel DC REIT has dropped 25%+.

Of which much of the decline came last week (2.00 to 1.72).

At this price, it pays close to a 6% dividend yield.

So I figured let’s do a deep dive – would I buy Keppel DC REIT after the drop in share price?

Keppel DC REIT pays a 5.8% dividend yield (6% trailing yield)

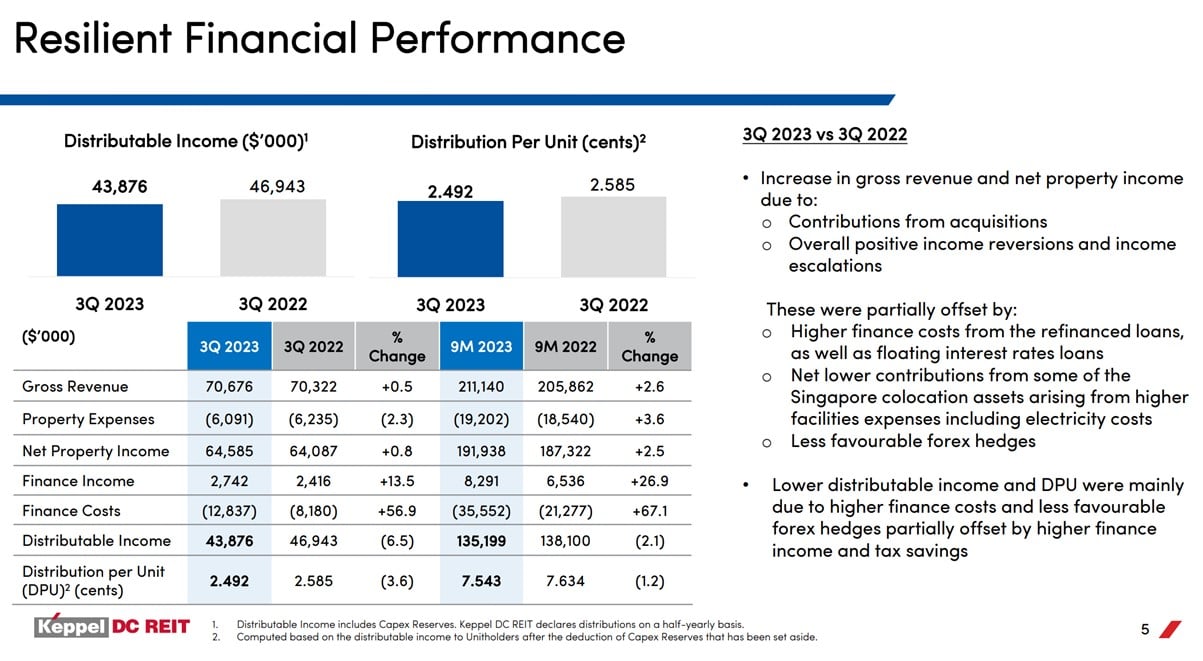

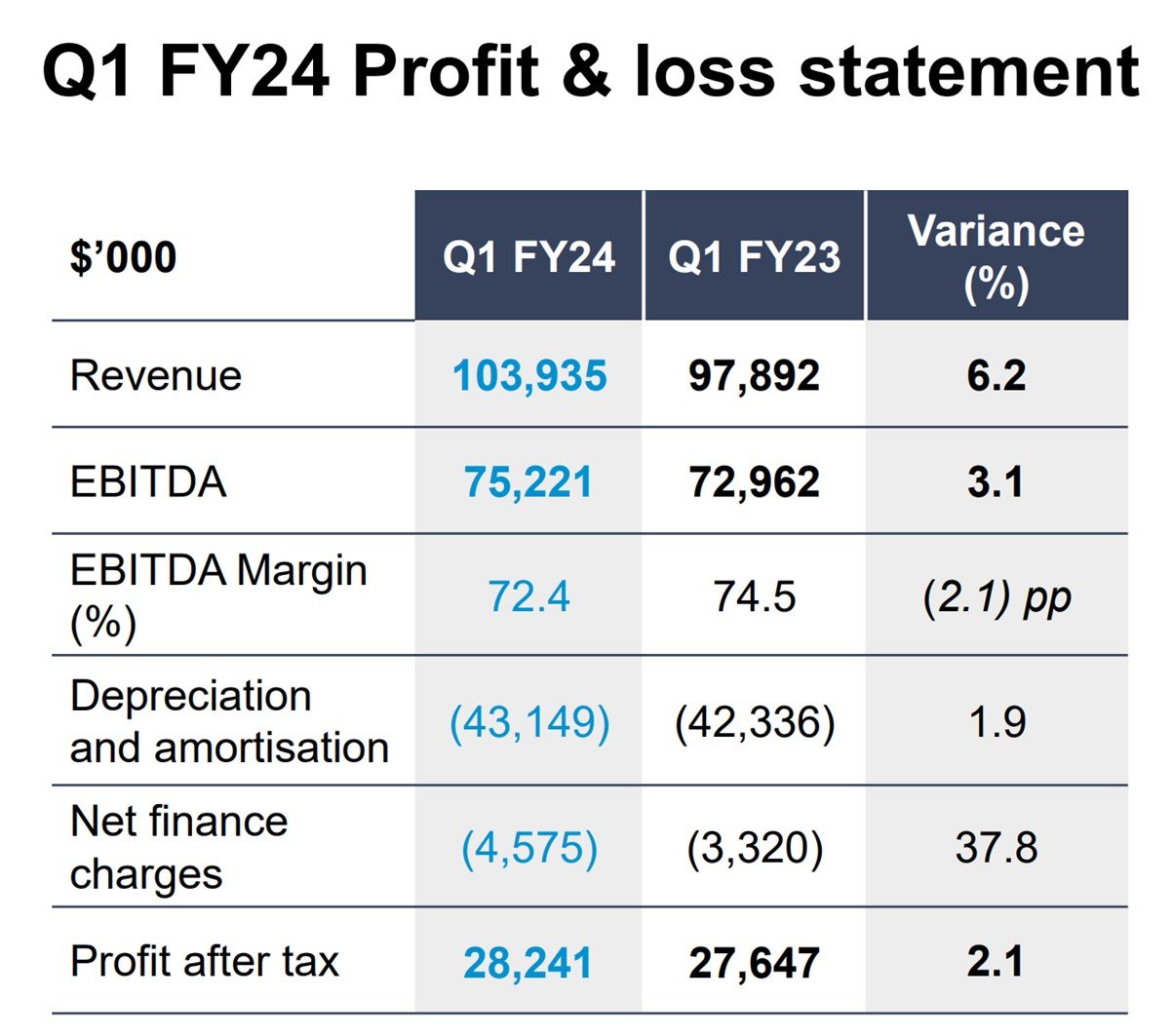

Financial results are not too bad.

Gross Revenue is up 0.5% year on year.

But DPU is down 3.6% year on year because… you guessed it – higher finance costs due to higher interest rates.

If you annualise the latest Q3 DPU, you get a dividend yield of about 5.8% (trailing yield about 6%).

Price to Book for Keppel DC REIT

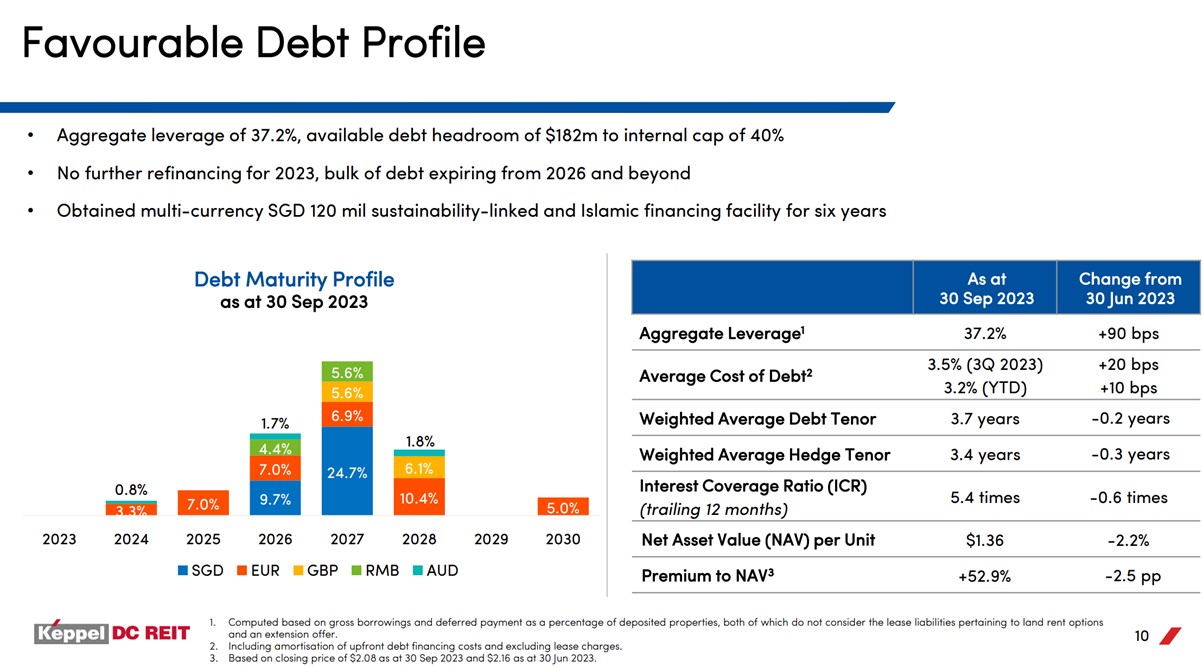

NAV is $1.36, which is down 2.2% from last year.

At this price, Keppel DC REIT trades at 1.25x book value.

What I like about Keppel DC REIT?

There’s been a lot of doom and gloom around REITs of late.

So let’s start with the good stuff for a change.

What I like about Keppel DC REIT.

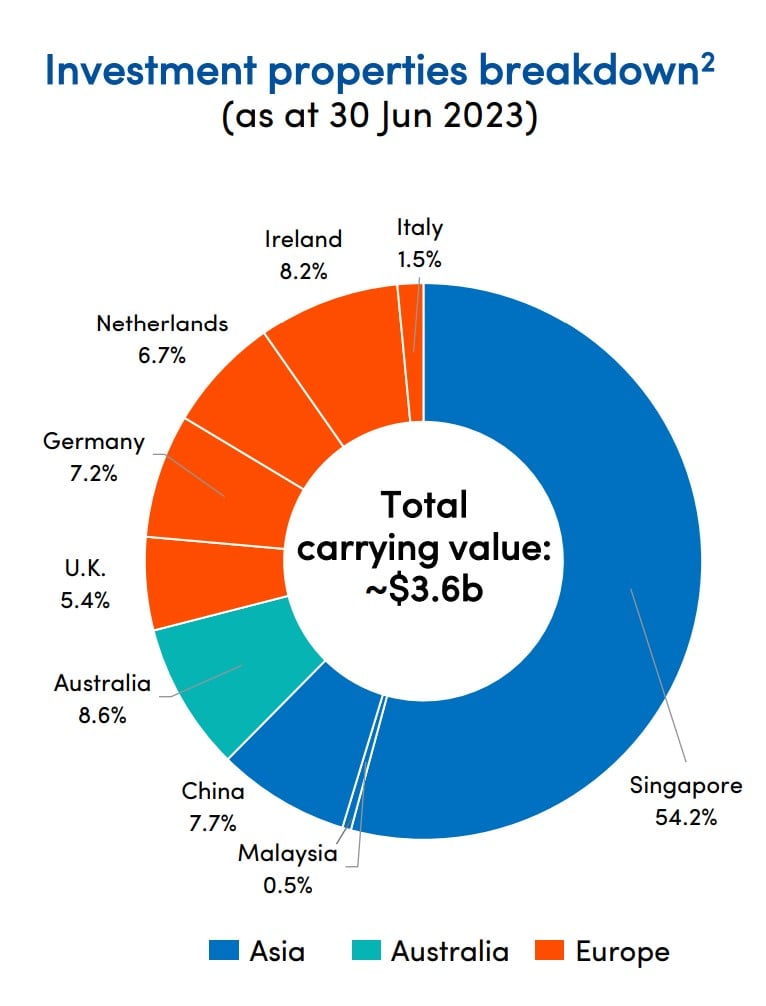

54% exposure to Singapore Data Centres

Unlike other data centre REITs like Mapletree Industrial Trust or Digital Core REIT which hold US data centres.

Keppel DC REIT is heavily exposed to Singapore data centres – 54.2% of the asset base is Singapore.

Singapore Data Centre are very valuable due to a lack of supply – DC Moratorium

Now Singapore Data Centres are valuable because there is a lack of supply.

The reason being that since 2019, there was a moratorium on new data centres in Singapore.

Data centres suck up a lot of energy, and Singapore did not want to place undue stress on the domestic energy infrastructure – hence no new data centres could be built the past few years.

This meant that anyone holding onto existing data centre assets in Singapore, was holding pure gold because of this artificial scarcity.

Moratorium has been lifted though

That said, the data centre moratorium has since been lifted.

But so far at least, it looks like the approval for new data centres is very limited:

“The IMDA stressed it was granting the right to build fresh capacity on a provisional basis only. It says it plans to allocate more capacity over the next 12 to 18 months. But the problem is the limited scale of this exercise – just 80MW. Although this is a pilot, and further expansion is supposedly on the way, it is not a big increment in a city with more than 1000MW in installed data center capacity.”

So far at least, it doesn’t look like the floodgates for new data centres are being opened.

It looks more like a mild increase in supply.

Which hopefully, *shouldn’t* cause too big an impact on Singapore data centre prices.

Keppel as an established Data Centre operator

The thing about data centres is that they’re not like a mall where you just clean it up and lease it out, and focus on getting tenant mix right.

Data centres are quite technical buildings, you need to focus on getting the right specifications in terms of rack space, cooling systems, backup power and so on.

The way I see it, you cannot divorce data centre ownership from the technical expertise required to run it (this is problematic for REITs like Mapletree Industrial Trust which may not have such capability).

The benefit with Keppel DC REIT, is that in Keppel you have a Sponsor with the expertise to build and operate data centres.

Don’t underestimate the importance of this in my view.

Why has Keppel DC REIT’s share price been impacted?

So… why the big drop in Keppel DC REIT?

The way I see it, it comes down to 3 reasons (leaving aside the obvious point of higher interest rates):

- Financial Difficulty of Keppel DC REIT’s big tenant

- Potential Dilutive Acquisition by Keppel DC REIT

- Institutional Sales

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Financial Difficulty of Keppel DC REIT’s big tenant?

Here’s what DBS Research has to say:

“The spotlight has now turned to KDC REIT as the income contribution from the three data centres in Guangdong will account for approximately 10%-11% of their revenues. Many questions have emerged regarding the potential impact on KDC REIT should Neo Telemedia face financial difficulties or even bankruptcy in the worst-case scenario. As the Guangdong data centres (DCs) are master-leased to Neo Telemedia, KDC REIT lacks visibility into the assets’ utilisation but continues to receive full rental payments.”

More information on Neo Telemedia:

Neo Telemedia, the master lessee of KDC REIT’s data centres made a net loss in 1HFY2023 for the six months ended June… Neo Telemedia reported a loss of HK$123.7 million or a loss per share of 1.3 HK cents for the six months to June 30. This compared with a net profit of HK$40 million in 1HFY2022. Interestingly, Neo Telemedia recorded both positive operating cash flow and free cash flow.

However, on the bank loans and debt front, Neo Telemedia has some HK$842.7 million of loans (of which HK$548 million are bank loans) categorised as current liabilities, which are generally payable within a year.

According to the financial report for 1HFY203, Neo Telemedia states that HK$500.4 million of loans were guaranteed by property, plant and equipment (PPE) with net book value of HK$161.9 million. Neo Telemedia has HK$14 million in cash and its net assets stood at HK$836 million.

According to DBS, a worst-case scenario involving Neo Telemedia’s bankruptcy could potentially have a maximum 16% impact on DPU.

“However, it’s important to note that Neo Telemedia has maintained current rental payments and has not indicated any payment delays,” DBS adds.

If you recall, one of Mapletree Industrial Trust and Digital Core REIT’s tenant went bankrupt recently, and the reaction on the share price was not kind.

Given that data centre REITs are prized for their stability, it’s possible that the uncertainty over Neo Telemedia has contributed to the recent sell-off.

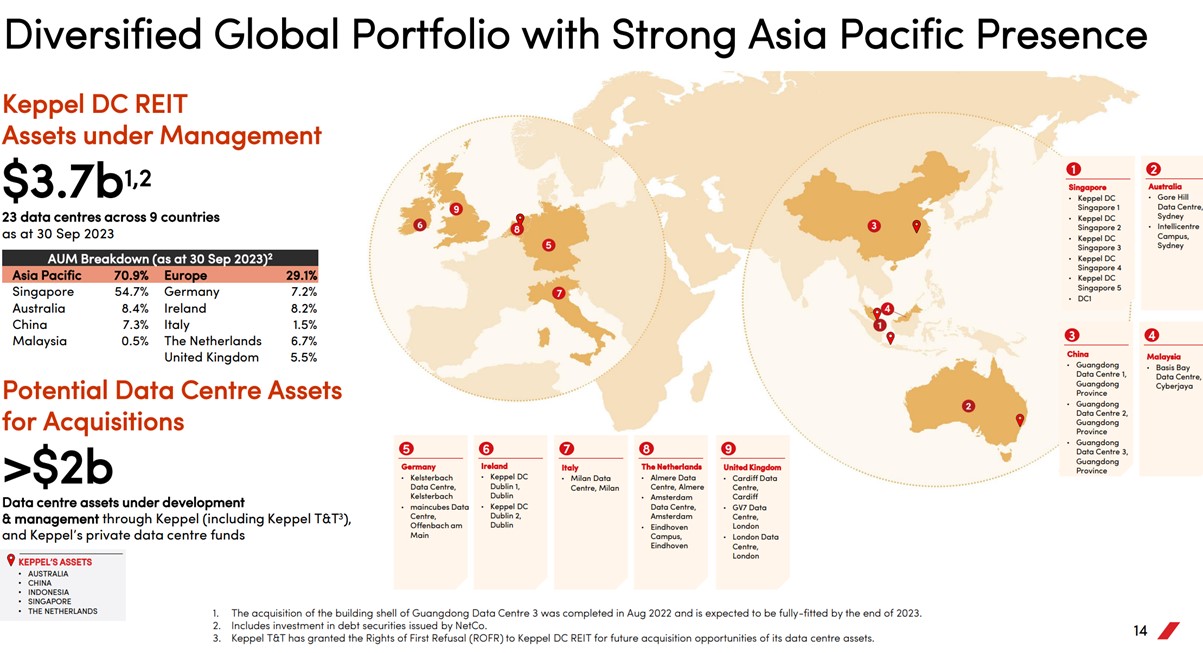

Potential Dilutive Acquisition by Keppel DC REIT?

The Edge has some interesting reporting on this next point:

… according to analysts at a KDC REIT briefing, two assets in that $2 billion pipeline are either stabilised or close to stabilisation. These are Keppel DC Singapore 7 (KDC SGP 7) and Huailai DC in Beijing.

Citi has a description of KDC REIT’s acquisition strategy, and its details may have further unnerved the market, albeit unwittingly. Citi says given that most of sponsor’s existing assets are operationally ready, going forward KDC REIT can work more closely with sponsor on acquisitions.

Within the pipeline shown in the slide, Citi highlighted KDC SGP 7 in Singapore, which was completed this year and ramping up is in process. “On track for stabilisation”, Citi says.

Huailai DC in Greater Beijing is completed, and “ramp-up can be potentially quite fast”, Citi says.

The point here, is that in Keppel DC REIT’s latest financial results, they included the following 2 slides, which talks about:

- A big pipeline of assets, many of which are already stabilised or close to stabilisation (market speak for being ready to be injected into the REIT)

- Keppel DC REIT’s long track record of growing through acquisitions

The theory then, is that the market put two and two together and freaked out about the possibility of a big acquisition.

And given that current leverage is 37%, any big acquisition is likely to either push leverage to very high levels, or require some form of equity fundraise.

And boy… you do not want to do an equity fundraise in this market.

For what it’s worth I thought this point was a bit of a stretch.

But it goes to show how jittery the market is these days, where even talk of an equity raise can spook investors.

Just take a look at Lendlease REIT.

Institutional Sales?

Remember how I talked last week about blue chip REITs selling off strongly due to *possible* heavy selling from the big institutional players?

If you ask me, I think some of that is in play here as well.

You can see how last week’s sell-off was on incredibly high volume.

Why exactly this is the case is not so clear.

You can argue it is due to the points above.

Or you can argue it is due to the general macro climate and risk off.

Who knows.

Whatever the case – it looks like some big players were selling down their stakes last week – and that at the very least should make you slightly cautious.

Will I buy Keppel DC REIT?

So let’s put it altogether.

You’re buying a data centre REIT with 54% exposure to Singapore, 7% exposure to China, and about 30% exposure to Europe.

You’re paying 1.25x book value, and getting a 5.8% dividend yield.

Revenue growth is flat, while DPU growth is negative (low single digits).

There are some risks overhanging the stock – notably the potential bankruptcy of a big tenant, possible acquisitions, and heavy institutional selling.

And of course don’t forget the generally unfavourable climate of interest rates potentially staying high for a while.

Is Keppel DC REIT a good buy?

It all goes back to price…

Don’t get me wrong.

I think Keppel DC REIT is a solid data centre REIT.

But the way I see it – no matter how good the real estate is, I will still lose money if I buy at the wrong price.

Over the past few years I never really thought of Keppel DC REIT as being “cheap”.

And while that is starting to change.

I’m not sure if I would buy Keppel DC REIT at today’s price just yet.

Technical Analysis suggests more downside?

Looking at the charts, the 2022 lows was $1.6, so if I were meaning to buy I would at least want to wait and see if it that support holds ($1.6 works out to a 6.2% dividend yield).

Note also how after last week’s massive sell-off.

There was huge relief buying earlier this week, which failed to hold, and the REIT ending the week at a new low.

This is not a good sign from a technical analysis point of view, and suggests you want to give the share price some time to play out first.

But whatever the case, markets are fluid and fast moving – as should investors.

This is what I think as of today, but I could easily change my mind on Monday and buy a big position if the news change.

As always – Patreons will get timely updates on what REITs I like, and what I choose to buy / sell.

Comparison between Keppel DC REIT and Netlink Trust – Is Netlink Trust the better buy here?

After looking at Keppel DC REIT.

I can’t help but make the comparison with Netlink Trust (owns the fibre networks in Singapore).

At $0.81, Netlink Trust pays a trailing dividend yield of 6.5%.

Market cap of $3.21b is actually higher than Keppel DC’s $3b

What’s more – leverage is a ridiculously low 23%, and you’re seeing low single digit growth in profit.

Between the two, does Netlink Trust look more attractive over Keppel DC REIT?

Love to hear what you think!

I just updated the Stock / REIT watchlist for Patreons last weekend, on the Stocks / REITs I am keen to pick up (and approximate target pricing).

With the recent sell-off some of the big blue-chip REITs are starting to look interesting for long term investors.

Full list on Patreon if you are keen!

– Get up to USD 2000 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 2000 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or inancial advisor.

Hi FH!

Full disclosure – I bought Netlink this week.

But I didn’t buy Keppel DC Reit, mostly because DC tenants seem to be going bust at regular intervals during this period. Just look at MIT. Hmm are DC tenants highly levered? It seems like not only you have to analyse the DC reit, but also look into the Reit’s tenants. Lol ????

Thanks for doing this! It looks like a solid Reit that needs to see a bit more downside in price to make it truly compelling (>7% yield to account for potential 16% drop in DPU?) What do u think?

Cheers

Mrs Pennies

https://pugsandpennies.substack.com

Like you said, it all goes back to price! At current price it’s prob a fair price, but the charts are not pretty, so at the very least I would like to give it some more time before making a decision.

On Netlink – been meaning to add too. I last sold out of Netlink around $1, been waiting to pick it up in the low 80s – exactly where it is now. But again the charts are not pretty, so I want to at least respect the charts for now and give it some time to play out too.

At these price it’s basically building a bond portfolio. 6%+ yield while you wait for the reversal in rates.

Concern about netlink trust is that it is funding their dividend through debt. Is it sustainable in the long run. And basically no growth beyond a certain point. Would love to hear your thoughts

Gearing is 23% though. If rates stay high, the other REITs are going to be impacted much more.

For netlink the high payout ratio is a concern. Wonder what’s your opinion on this?

I mean it’s def a concern. But qn is at 6.5% yield (about 3% spread vs 10 year) is that appropriately priced in?

I believe in the “time in the market> timing the market”. KDC was always expensive but was also growing heavily. It was expensive at 1.80, it was expensive at 2.00 and it still climbed to 2.3.

I don’t think it is wrong to start buying now and add even more if it gets even cheaper.

Netlink is not that attractive if you ask me due to the limited growth perspective. It is more like a bond.

Greetings from Germany

Fair enough, I understand your point. Let’s see how the price trades the next couple months.

I like Netlink exactly because it’s like a bond. It’s a 3% yield spread against the SG 10Y, as long as it pays that yield reliably, it’s good enough for me (at least for that portion of my portfolio).

If interest rates go down in the next 1 – 2 years, that could imply capital gains simply because of the lower risk free.

What is your take on CLINT? It also dropped heavily and is worth buying in my opinion.

India isn’t a market I follow closely, so not easy for me to comment. Real estate is quite a local business, not easy to invest without knowing the local real estate market / cycle.

aw man it climbed to 1.92, but there’s still some savings to be had… think i’ll put a small foot in door in case it cilmbs higher.