Keppel Infrastructure Trust is a position that I picked up in 2023.

And I’ve been frankly quite impressed by how the Business Trust has performed since then, to the point where I’ve been looking to add to my position.

With the recent announcement that Keppel Infrastructure Trust is buying an Australian bus company, and doing an (not small) equity fundraise to fund the acquisition – I just might get that opportunity.

This is a FH Premium article written on 5 Feb, and has not been updated since (I am releasing it given quite a few of you have asked about Keppel Infrastructure Trust).

For updated views since then, do sign up for FH Premium.

You get access to premium content like this, my personal stock / REIT watchlist, and my full personal portfolio (with updates when I buy/sell positions).

Keppel Infrastructure Trust buys a bus company?!

Imagine my shock when I woke up this morning only to find that Keppel Infrastructure Trust was buying a bus company.

For a moment, I thought the announcement of Comfort Delgro had landed in my inbox by mistake.

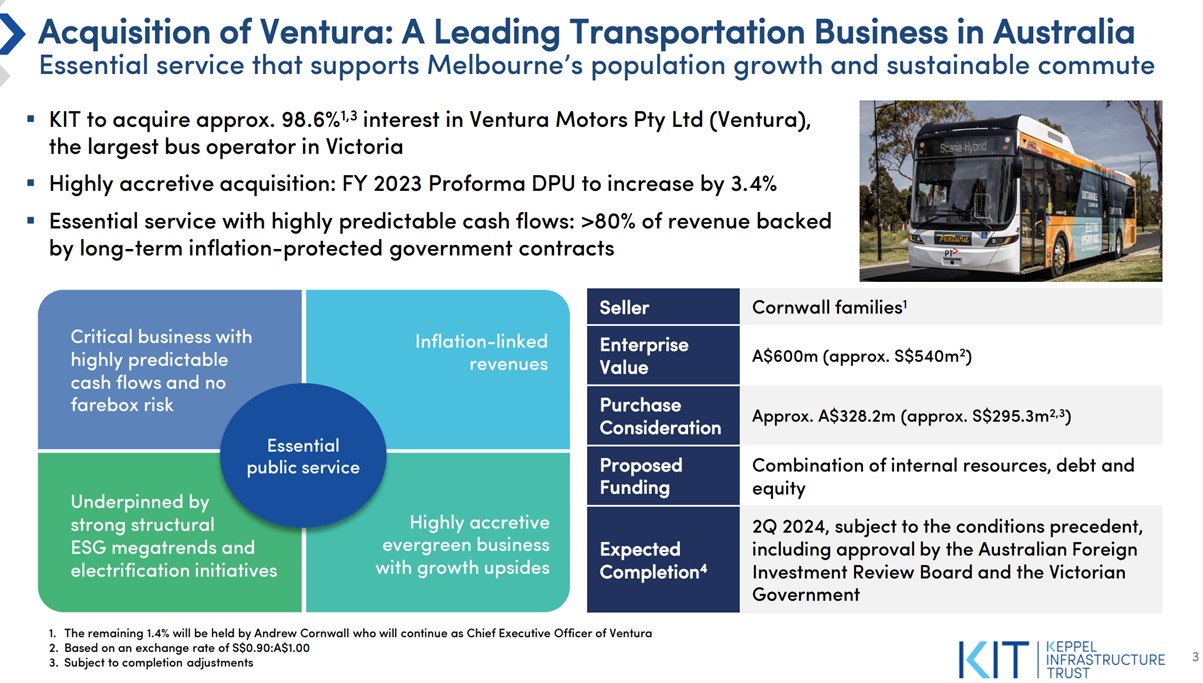

Why would an infrastructure trust look to buy an Australian bus company for $600 million AUD?

In fact the more I read, the more perplexed I got.

Keppel Infrastructure Trust was indeed spending $540 million SGD to buy a bus company in Victoria, Australia.

They are buying a 98.6% stake too, which means the family selling to them is effectively cashing out, and doesn’t really have a lot of incentive to stay on to help manage longer term.

Why the heck is Keppel Infrastructure Trust buying a bus company?!

I’ve extracted the acquisition slides below for your reading pleasure.

And yes, logically I understand the appeal of the deal, it being DPU accretive on a 10 year contract blah blah blah.

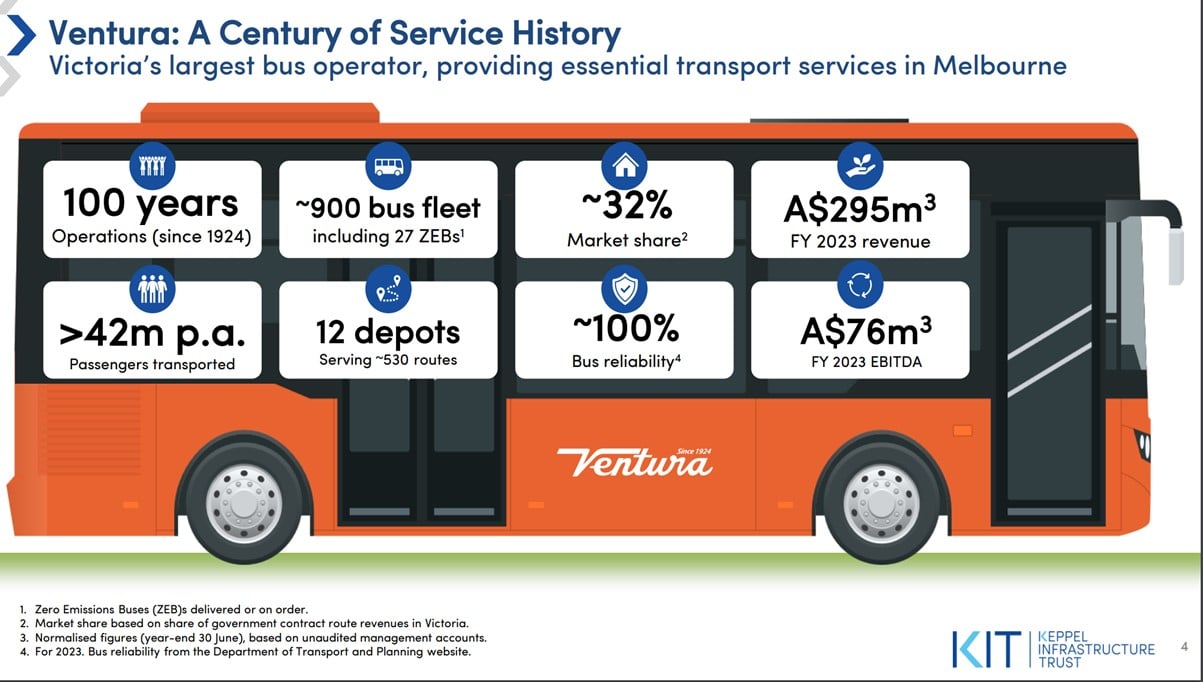

But the key question in my mind – what the heck is the competitive advantage of Keppel Infrastructure Trust, owning a bus company in Australia?

If this were Comfort Delgro maybe I get the story.

If this were Keppel Intrastructure buying a rubbish disposal company in Australia maybe I get the story.

But a bus company in Australia is about as operational and local as it gets.

It’s a tough business, without any real long term economic moats. And not to mention all the headache from having to deal with local labour markets, manage local stakeholders, bid for renewal contracts and so on.

Keppel Infrastructure Trust’s expertise so far seems to lie in infrastructure assets (think chemicals, rubbish, electricity generation, water so on).

A bus company, I’m really not sure where the competitive advantage lies.

I know the numbers look good, but I’m truly not a fan of this deal.

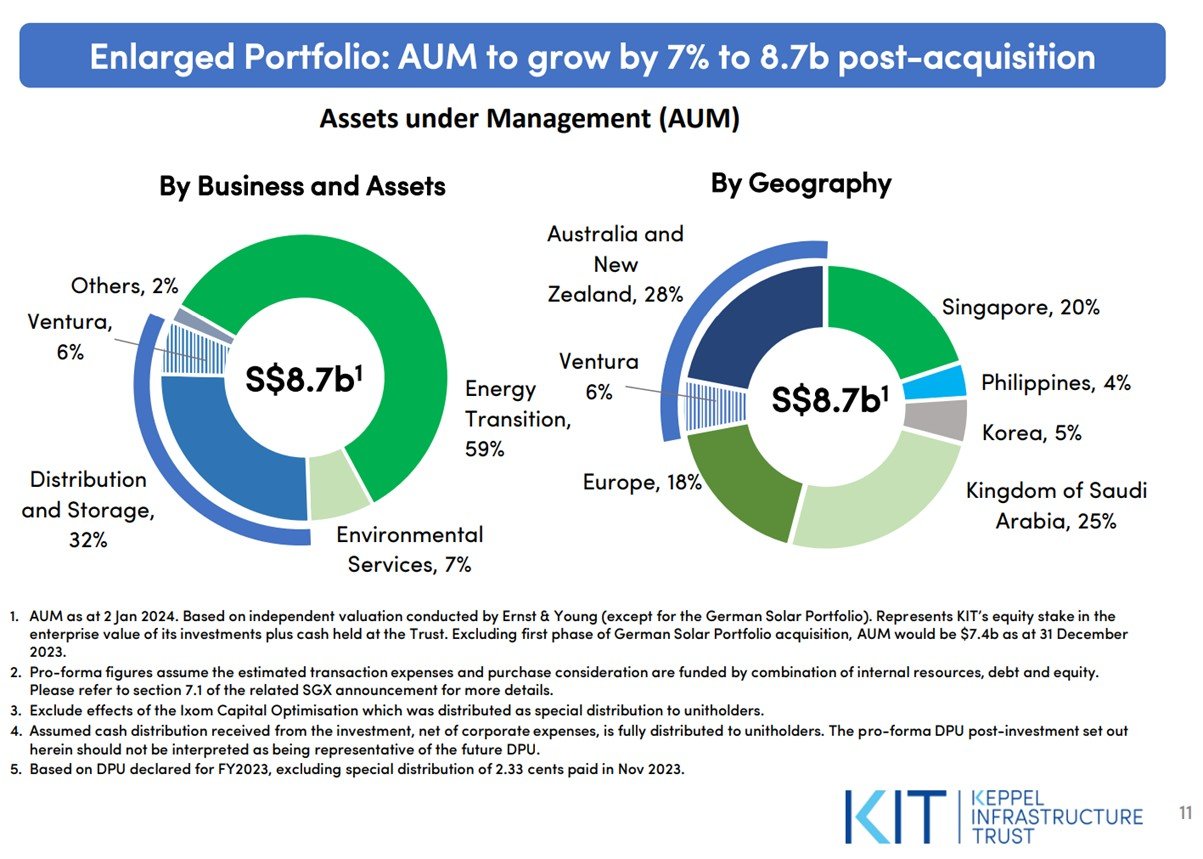

On the bright side… this is only 6% of the AUM

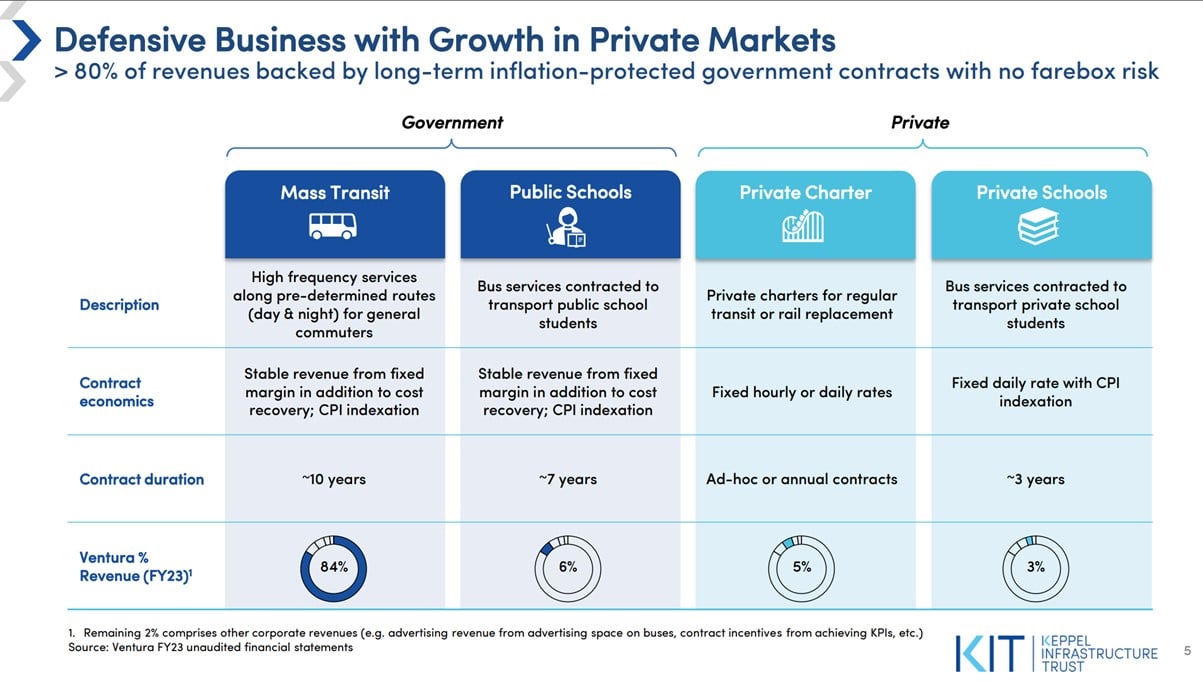

On the bright side, this acquisition only makes up 6% of Keppel Infrastructure’s asset base.

So it’s not like Mapletree Pan Asia Commercial Trust where 1 bad asset can ruin the entire REIT.

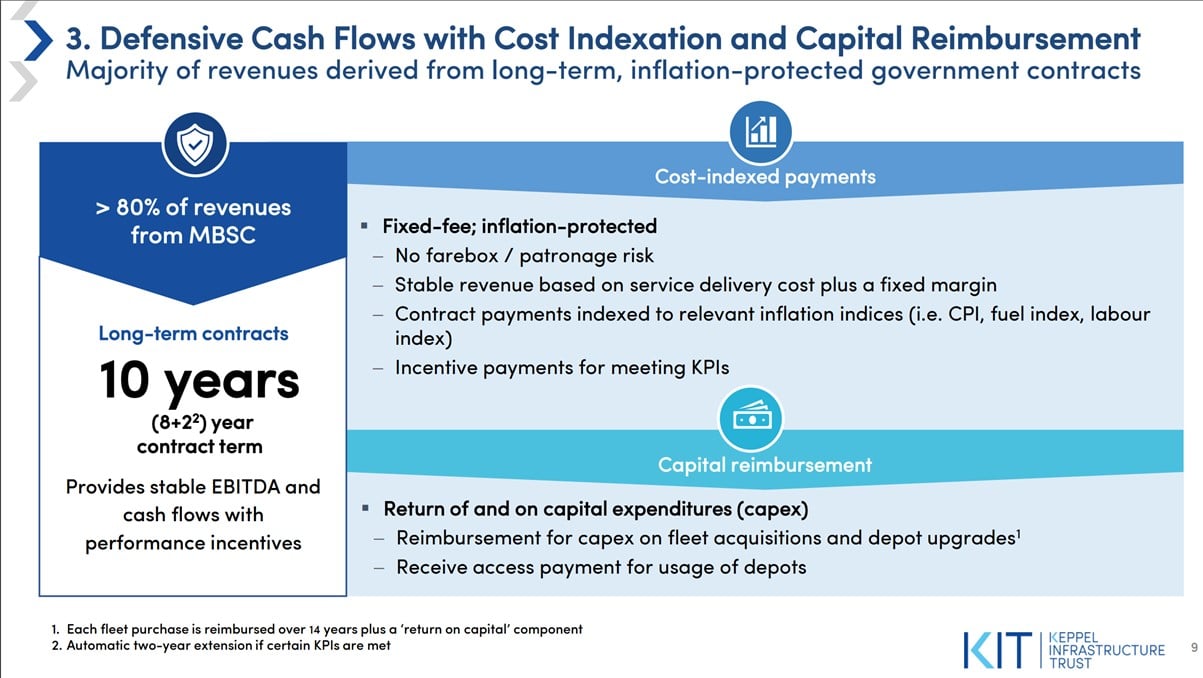

And because 84% of the revenue is locked into a 10 year contract on a cost plus basis.

Hopefully the room to (for lack of a better word) “screw up” in the short term is minimised.

But in the longer term, I really have my concerns whether KIT is best placed to manage an Australia bus company.

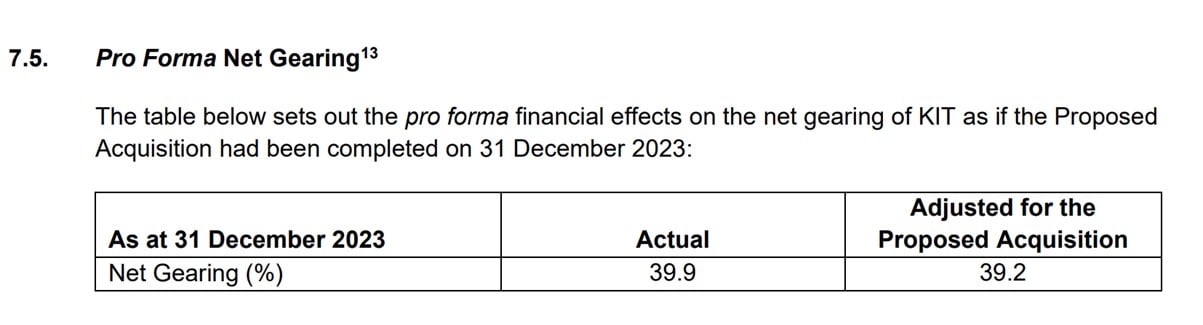

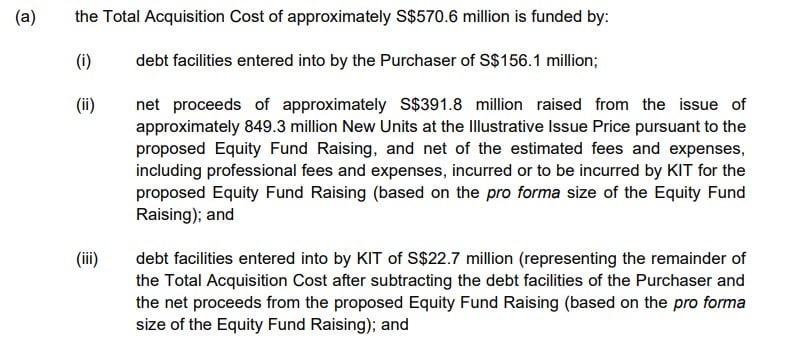

How will the acquisition be financed? Mix of debt and equity..

$156 million of that is in debt.

However they’ve run the numbers, and gearing will actually go down to 39.2% post acquisition.

What this means is that the rest of the $391 million is going to be funded via an equity fundraise:

Some back of the napkin numbers:

- Keppel Infrastructure Trust has a $2.87b market cap

- So the $391m equity fundraise is 13.6% of the current market cap

It’s not a huge equity raise, but it’s also not small.

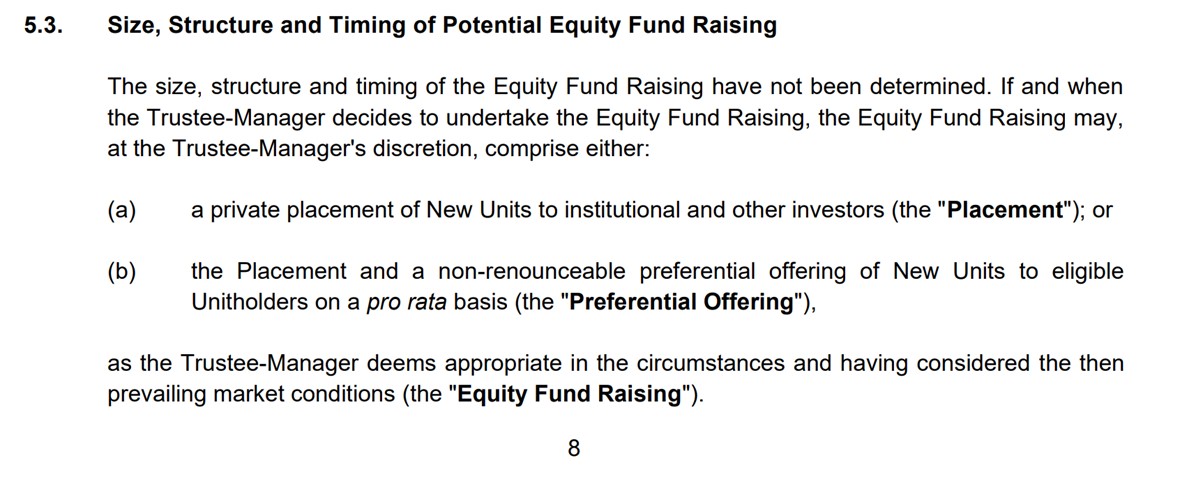

And Keppel Infrastructure may raise either via a private placement or a preferential offering.

If it’s a placement it means retail investors are going to be diluted, if it’s a preferential offering it means retail investors will need to cough up the cash.

Whatever the case, it looks like there will be price weakness for Keppel Infrastructure Trust going forward due to this equity fundraise, which could be interesting for long term investors who want to add.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Will I buy more Keppel Infrastructure Trust?

While I am not a fan of this deal.

All things considered, it is only going to make up 6% of the AUM, and the 10 year contract should limit near term downside.

And like I said, I’ve been impressed with how the rest the portfolio has performed the past year or so.

Keppel Infrastructure Trust seems to have built up an interesting collection of infrastructure assets that are more resilient to inflation, than the typical REIT.

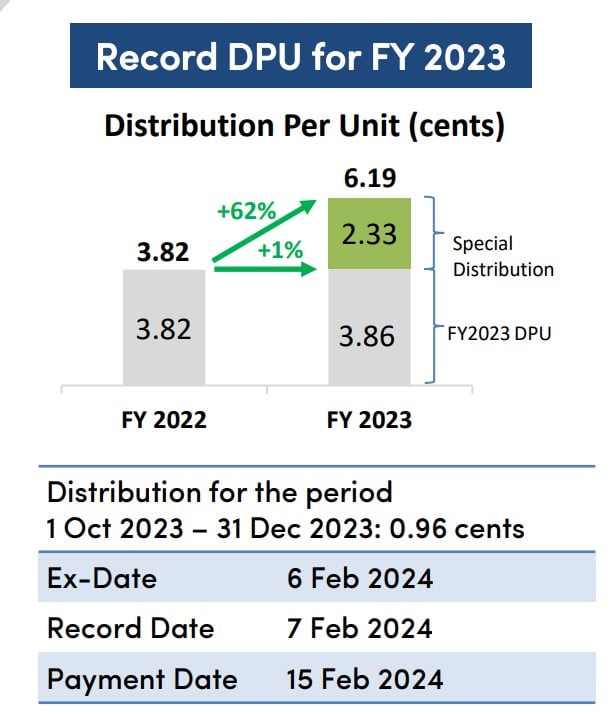

DPU wise, Keppel Infrastructure Trust is one of the rare few to have increased DPU from FY 2022 -> 2023, in a climate where almost all REITs were slashing DPUs.

This has very interesting diversification abilities from a portfolio perspective.

I can see the appeal of adding the 2 business trusts – Keppel Infrastructure Trust and Netlink Trust, to provide some diversification to a REIT portfolio.

What is the dividend yield of Keppel Infrastructure Trust?

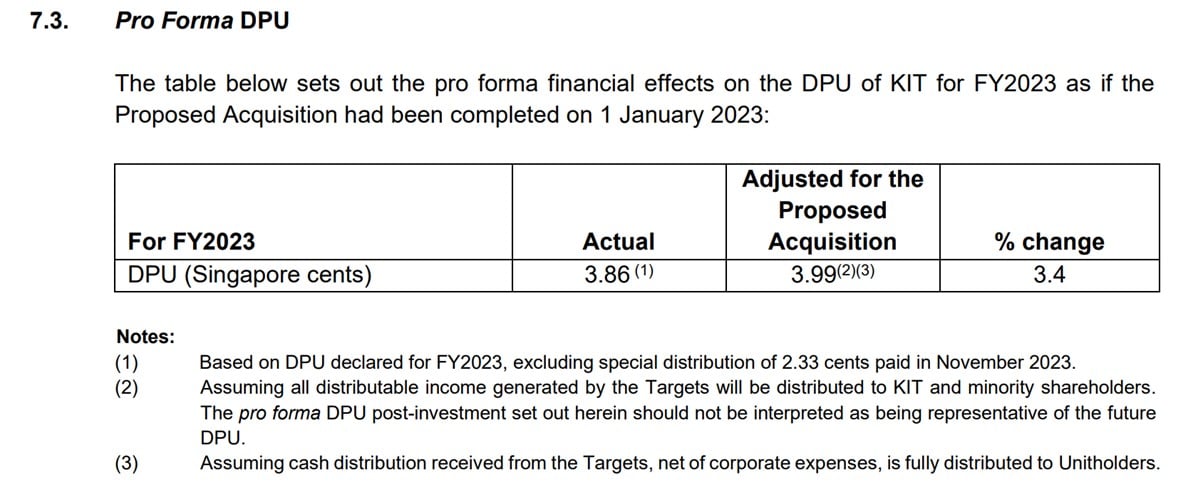

If you strip out the one-time special dividend, FY2023 DPU is 3.86.

Let’s say I pick it up at 48 cents, that’s about a 8% dividend yield.

In fact if you use the pro-forma DPU post-acquisition, DPU is 3.99 which is 8.3% at 48 cents.

Even factoring in some downside, you’re still looking at a 7% plus yield

Not too shabby – and I would have to take on significantly more risk to achieve the same yield via REITs, many of which are still reporting negative DPU numbers.

So that’s the appeal from a diversification perspective.

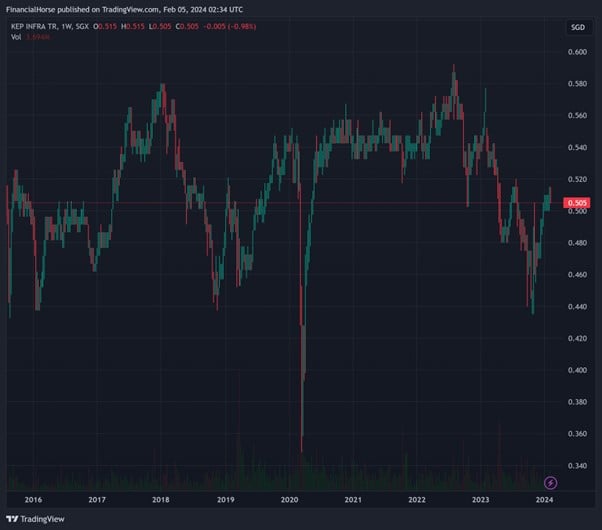

Technical analysis – What are the key price levels to watch for Keppel Infrastructure Trust?

In terms of key levels to watch.

The next key support is:

- 48

- Then 46

- Then 44 (cycle low hit in late 2023)

As always, you want to keep an open mind on price and let the market play itself out.

But even at 48 you’re looking at a 8%+ yield, which is not too bad frankly.

So I’ll let the equity fundraise play out for now, but I would be keen to add to my position at the right price.

As always – this article was written on 5 Feb 2024, and has not been updated since.

My updated views on Keppel Infrastructure Trust, and the price I buy/sell this business trust at (if at all), are shared on FH Premium.

This is a FH Premium article written on 5 Feb, and has not been updated since (I am releasing it given quite a few of you have asked about Keppel Infrastructure Trust).

For updated views since then, do sign up for FH Premium.

You get access to premium content like this, my personal stock / REIT watchlist, and my full personal portfolio (with updates when I buy/sell positions).

– Get up to USD 3000 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 3000 free shares.

You just need to:

- Fund SGD2000

- Maintain until 31 March

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Business infrastructure trusts like KIT and Netlink should be compared to utilities, not REITS. Infrastructure and licenses are for a limited period. The upfront capital invested in these is paid out as income over the life of the depreciating license and asset. Capital injections are needed to renew the infrastructure and license. Revenue is usually subject to controls in the license conditions. Like utilities.

Whereas REITs have land value beyond the building value, and the balance sheet NAV is a mix of land and buildings. If land is freehold, it does not go to zero at the end of the leasehold and does not need capital injection.

For these reasons, the yields on infrastructure trusts must be higher than REITs with some freehold land.

True, this is a good point. Appreciate the sharing.