So the latest Singapore Savings Bonds are out!

And the interest rates are absolutely terrible.

You’re looking at 2.84% for the first 6 years, and 2.97% over 10 years.

I’ve been getting quite a few questions on this.

Namely – have interest rates peaked?

And if so, should you be locking in interest rates at these levels?

For example… an 18 month fixed deposit at 4.2%?

There’s a lot more than meets the eye with this question.

3 key points that I wanted to address:

- Why are Singapore Savings Bonds Interest Rates going down?

- Have interest rates peaked (or will they go back up)?

- Should you lock in an 18 month Fixed Deposit at 4.2% instead? Or 4.20% T-Bills?

Basics: Interest Rates on the latest Singapore Savings Bonds are terrible

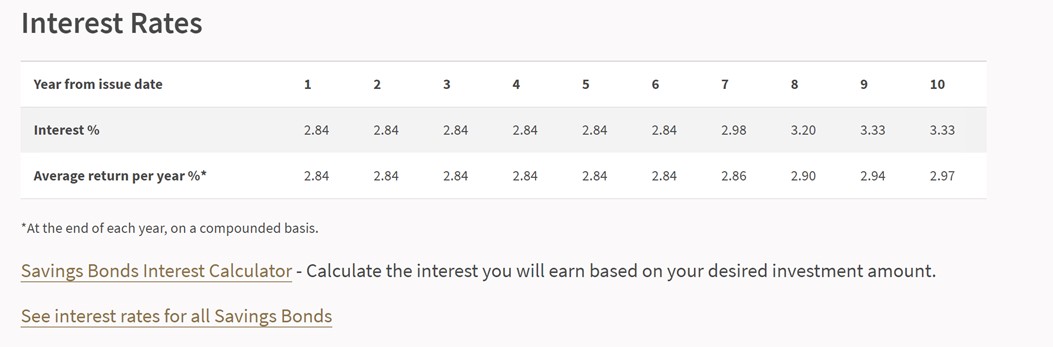

Interest rates for the latest Singapore Savings Bonds below.

You’re looking at 2.84% flat for the first 6 years.

Before finally stepping up to 2.97% after 10 years.

By contrast, last month’s Singapore Savings Bonds (which was already terrible).

Started at 2.95% for the first year and stepped up to 3.26% over 10 years.

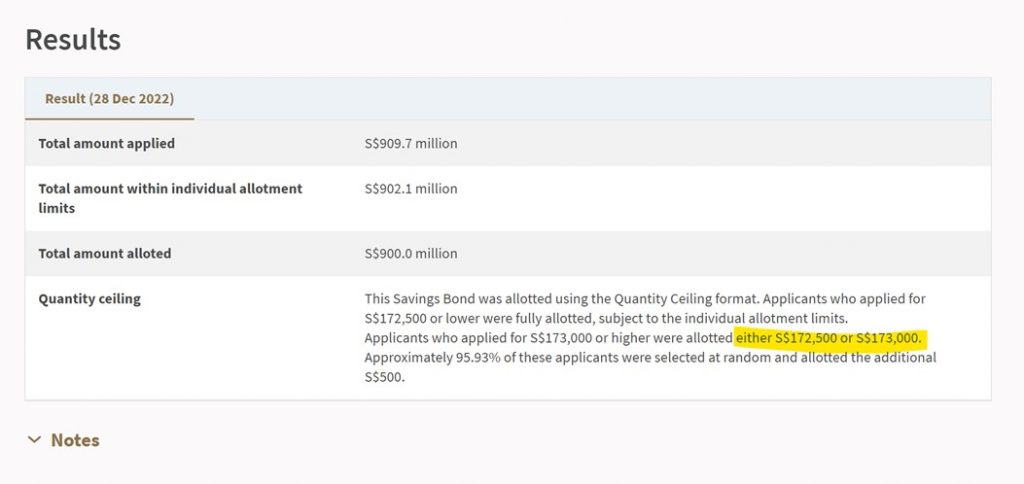

But you will probably get full allocations

If there’s one good thing – it’s that you’re probably going to get very meaningful allocations.

Last month saw allotments of up to $173,000 per person.

That’s almost enough to fill up the full $200,000 quota at one go.

The amount offered is slightly lower this month at $700 million ($900m last month).

But I think with the lower interest rates, you’ll still be looking at very meaningful allotment.

Those of you still holding onto Singapore Savings bonds from pre-2022, this is your opportunity to redeem everything and swap out for the new Singapore Savings Bonds.

Yes interest rates are not amazing, but they are still better than anything from pre-2022.

Reminder that you can redeem the existing Singapore Savings Bonds and apply new bonds in the same month (as long as you have the cash on hand to apply).

Why are Singapore Savings Bonds Interest Rates going down?

Simple answer – Singapore Savings Bonds track the average interest rates of the previous month.

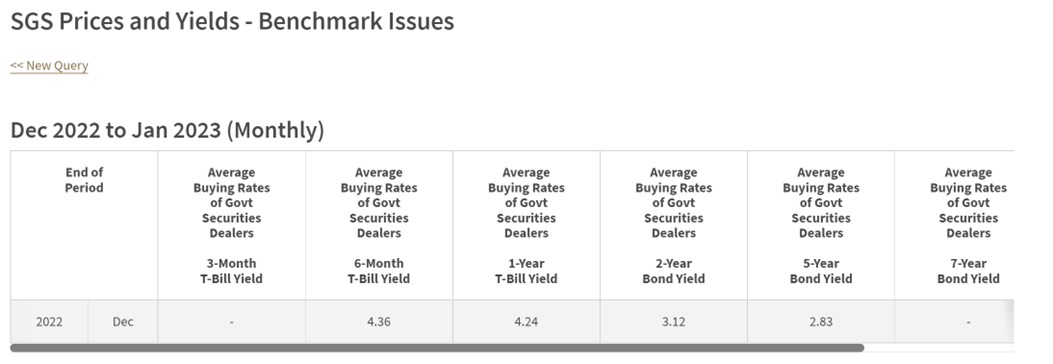

Here are the average interest rates on Singapore Government Securities for the month of December:

The 10 year interest rate is stuck at 2.83% – which explains why Singapore Savings Bonds are so low this month.

The slightly more technical answer is that Singapore Savings Bonds interest rates are smoothed out, such that the 1 year yield will never exceed the 2 year or 10 year yield.

Given the current inverted yield curve (where 1 year yield is way higher than 10 year), this is creating all kinds of funky issues.

But long story short – this tracks market interest rates.

So no, government is not trying to “kelong”.

The move in interest rates is mind blowing

Let’s take a step back.

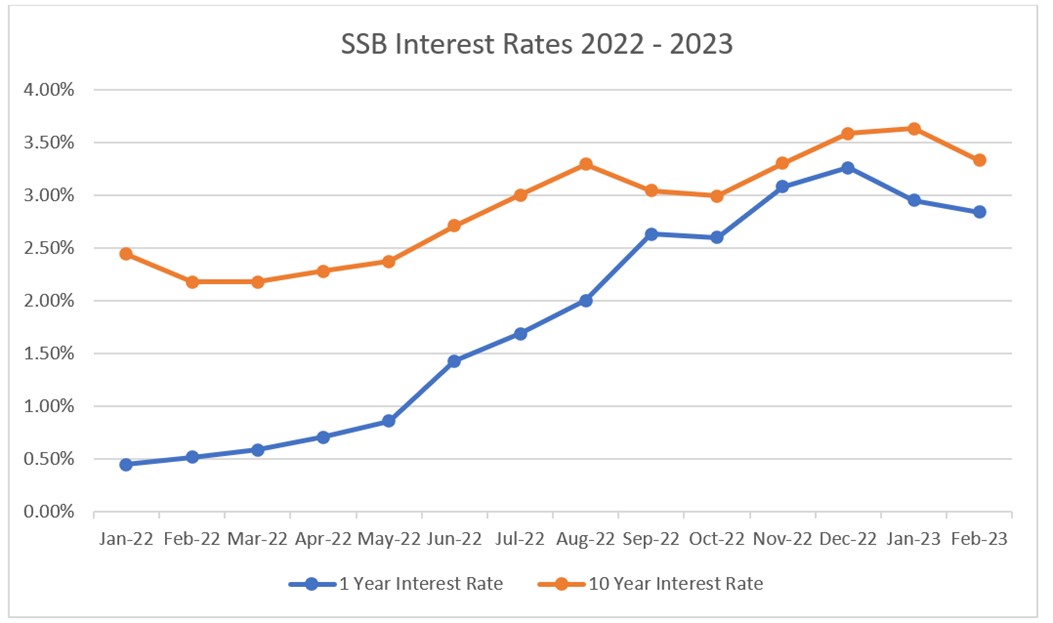

Just 1 year ago, in Jan 2022, 1 year Singapore Savings Bonds yielded only 0.45%.

1 year later and it jumps to close to 3%.

Unbelievable stuff.

By contrast the 10 year interest rate hasn’t moved as much – 2.44% a year ago, to 3.33% today.

I suppose the point here – is that don’t be too complacent about interest rates.

Whenever interest rates stay low, investors expect them to stay low forever.

And when interest rates go up (like now), investors expect them to stay up forever.

Have interest rates peaked (or will they go back up)?

Which brings us to the million dollar question.

Have interest rates peaked? Or will they go back up again?

And consequently – should you look to lock in interest rates at this level before they go down?

For eg. an 18 month fixed deposit with CIMB at 4.2%?

What does the market think?

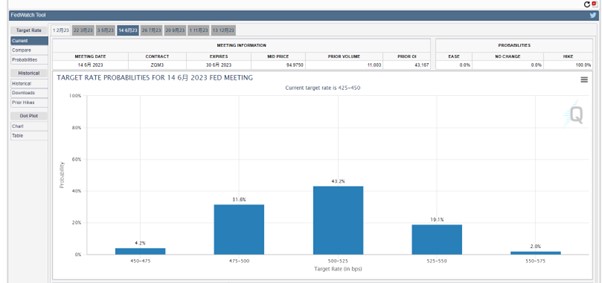

The market right now is pricing in a peak of 5.00 – 5.25% on the Fed Funds Rate.

We are at 4.25% now, which means market is pricing in at least another 3 0.25% rate hikes to go.

With the US 1 year sitting at 4.8-ish, you could probably argue that much of the rate hikes is already baked in.

So I suppose if you ask the market, they will say that we are at or close to peak interest rates.

My Personal View?

If you ask me though, I still think the market may be too optimistic on how quick rates are cut.

Looking at latest job numbers holding up, I think the terminal will be closer to 5.25% – 5.50%.

Which means another 1.00% of rate hikes to go.

Why do I disagree with market pricing?

While I agree inflation has peaked.

I’m not so sure if inflation will go from 8% to 2% in a straight line.

There’s a good chance it just bounces around for a while.

Ie. Inflation, vs inflation volatility, are very different things.

Inflation has peaked, but inflation volatility may take quite some time to come down.

And that could cause big problems for a Fed on a crusade to stamp out inflation.

So I don’t think the Feds cut until the economy weakens significantly.

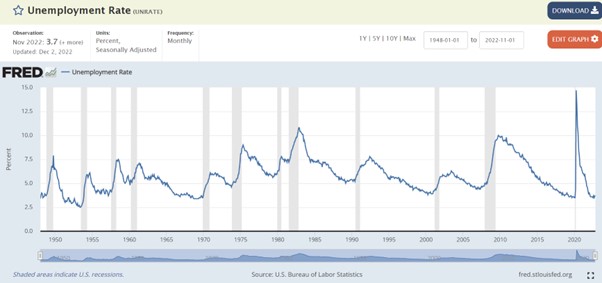

And with US unemployment still at generational lows of 3.7%, I don’t think the rate cuts will come as soon as the market is pricing in.

So if you ask me, I don’t think interest rates have peaked just yet.

BUT – I do not deny the bulk of interest rate hikes are behind us

That being said, I do not for one second deny that the bulk of interest rate hikes are behind us.

Jerome Powell has told you as much.

He’s told you that the bulk of rate hikes are behind us, and they want to go slow on hikes going forward.

I mean when you go from 0% to 4.25% in less than 8 months.

And the biggest debate now is whether the terminal is 5.25% or 5.50%.

Yeah… I would say the bulk of rate hikes are already behind us.

Should you lock in an 18 month Fixed Deposit at 4.2% instead? Or 4.20% T-Bills?

So…

Markets think interest rates have peaked, or are close to peaking.

I think interest rates will peak slightly higher than what market is expecting (by 0.25%).

Remember that saying about a bird in hand being worth two in the bush?

Yeah..

If you ask me, I think locking in an 18 month fixed deposit at 4.2% today (eg. from CIMB), is really not the worst thing in the world.

You see if the market is right and rates are cut, you lock in the 4.2% for 18 months (mid 2024).

If the market is wrong and rates go waaaay higher, you can just break the fixed deposit and roll over at higher rates.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

My general thought process?

I talked about the 80-20 rule as one of my biggest investing mistakes in 2022.

It’s the idea that you want to focus your efforts on the 20% of the decisions that drives 80% of the results.

What is clear, is that the bulk of the interest rate hike cycle is behind us.

Yes, there’s probably 4 or 5 more 0.25% hikes left in the tank.

But we’re no longer hiking 0.75% each FOMC.

The bigger questions now are long we stay at these levels before rate cuts.

And whether we peak at 5.25% or 5.5%.

So I encourage you to focus on the bigger picture here.

Important Caveat on this analysis

Do note that this analysis only applies for the risk free yield instruments like SSBs, T-Bills and Fixed Deposit.

If you’re betting on the timing of rate hikes (eg. buying REITs, tech, bonds etc), you probably want to buy closer to the peak.

The key different is that with the former, you don’t suffer capital losses if interest rates go up. Whereas you most definitely will with the latter.

For those who are keen, my macro analysis is updated weekly on Patreon.

What will I do – Buy Singapore Savings Bonds, T-Bills or Fixed Deposit?

For the record, I’ve been buying everything the past few months – Singapore Savings Bonds, T-Bills, Fixed Deposit.

To me, each has their own pros and cons.

I like Singapore Savings Bonds because they offer liquidity and can be redeemed any time. And I have the option of holding for 10 years if interest rates are cut.

I’ve been buying T-Bills because they offer the highest short term interest rates, at the expense of liquidity.

I’ve been placing money in Fixed Deposit because the yields are decently attractive, and I have the option of breaking early if I want to.

While I will do the same going forward, I’ll probably start looking to adjust duration longer – to lock in the interest rates longer term at these levels.

Will I still be buying the February Singapore Savings Bonds?

I still have one final tranche of Singapore Savings Bonds from 2019.

Even into year 4 – 5, they’re only yielding 2.3%.

If I can get 2.84% for the first 6 years, it’s pretty much a no-brainer to redeem the 2019 bonds, and rotate the cash into the latest bonds.

That said, after this round, I would be maxxed out on my $200,000 quota, and I don’t see myself applying for Singapore Savings Bonds going forward (unless the interest rates pick up).

Will Singapore Savings Bonds go back up above 3.5%?

One final question that quite a few of you have asked.

I don’t know why 3.5% is the magical number, but it’s what you asked for so I will roll with it.

Now Singapore Savings Bonds track the average interest rates for the previous month.

So for SSB interest rates to go back up above 3.5%, we need to see 10 year SGS yields average above 3.5% for one month.

Now short term interest rates like 6 month T-Bills are very volatile, and respond very strongly to Fed rate hikes.

Whereas 10 year SGS yields are a lot more stable, and respond more to market expectations over long term economic growth and inflation rather than rate hikes.

It’s why you see short term rates move so sharply, while long term rates remain much more stable.

So… will 10 year Singapore Government Securities average more than 3.5% for a whole month?

Gun to my head?

I think there is a possibility.

The10 year SGS is at 2.98% now, so a move like that would be a massive 50 bps increase.

That would cause devastation for S-REITs.

But as 2023 drags on, I wouldn’t rule it out, especially as liquidity continues to tighten.

Focus on the bigger picture for interest rates…

But that said, for those of you thinking of whether to lock in interest rates for fixed deposit / Singapore Savings Bonds / T-Bills at these levels.

I do encourage you to look at the bigger picture.

A year ago if I told you you could get a 18 month fixed deposit at 4.2% (or Singapore Savings Bond at 2.97%), you would have jumped out of your seat.

Now that interest rates are actually here, people are fretting over whether they are locking in too low.

So yeah… look at the bigger picture guys.

Worst case you can always break your fixed deposit early, or redeem your Singapore Savings Bonds early.

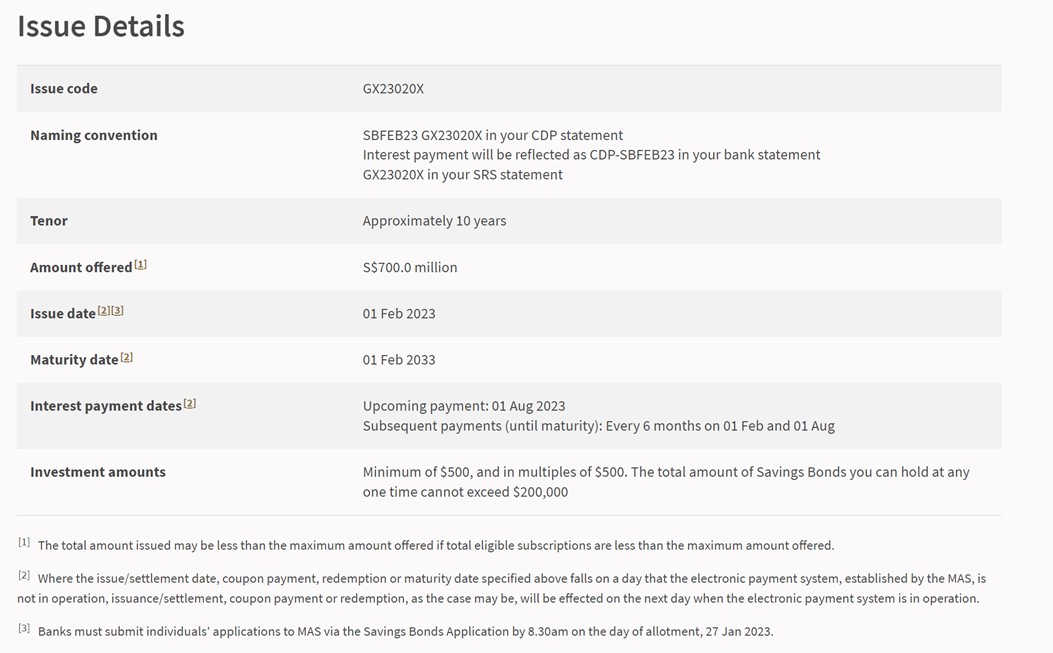

Singapore Savings Bonds Application Timeline

For those who are keen, don’t forget to get your Singapore Savings Bonds applications in by 26 Jan.

If you want to redeem older Singapore Savings Bonds, deadline is 26 Jan as well!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi

As a primarily equity investor, I couldn’t agree more with that last reminder to look at the bigger picture.

I prize liquidity (how do I convert the SSB/FD/TBILL into cash) above all considerations, because when the market presents an opportunity, I need cash to take advantage of it.

There is nothing wrong with optimizing the cash equivalent part of the portfolio, it’s free money after all. However this should always be viewed from the perspective of your overall portfolio strategy.

Absolutely agreed! Investors should approach cash management holistically in the context of their entire portfolio.

Don’t just be seduced by yield – liquidity, when you need it, is far more important.

How to strike the right balance between yield and liquidity, by using all the range of instruments available (T-Bills, SSB, Fixed Deposit), is the question investors should be asking.

I made a bid @ 4.0% using CPF OA. May I know when the tbill will be allocated?

10 Jan – you can check from the calendar here: https://www.mas.gov.sg/bonds-and-bills/auctions-and-issuance-calendar/auction-and-issuance-calendar-2022

Curious because you seem to have SSB to redeem every month? why didn’t you redeemed all in the first instance you could e.g. why wouldn’t have you redeemed all last month or the month before?

Because the SSB allotment amounts were very low the past few months.

If I had redeemed all at one go I would have been sitting on a bunch of cash earning 0%.

Only when it was clear that allotment amounts would go up a lot (eg. last month), did I start redeeming in size.