In The Psychology of Money, award-winning author Morgan Housel shares 19 short stories exploring the different & interesting ways people think about money.

Here are 6 life-changing lessons from The Psychology of Money.

1. Don’t Judge other people

Everyone has different attitudes about money – so don’t judge.

Understand that everyone comes from different backgrounds, which influences their perspective.

For instance:

- age

- where they are born

- upbringing

- parents’ perspectives on money

- whether they have experienced financial crisis in their lifetime

These factors all influence how we view money, save money and invest money.

For instance, the generation of Singaporeans who have experienced the ’97 financial crisis, or various housing booms/busts, will influence their view points on money – and often times, validly so!

Adding onto this, we shouldn’t underestimate the importance of luck in people’s money journeys.

About half of the differences in income across people worldwide is explained by their country of residence and by the income distribution within that country.

So in a way, dont be too hard on yourself and don’t judge others’ (and your partner) too harshly when it comes to differing money views.

Instead, try to understand the context in which their understanding of money has been shaped, and try to find value in others’ perspective.

2. Money No Enough – Really?

The books points out the phenomenon of people always comparing themselves with others doing better than themselves.

This leads the (often) false belief that they don’t have enough money.

But this is rarely true!

Ask yourself:

Do you really need more money? Do you really need these extra things?

The book cites many examples of already rich people risking everything for more money. E.g. ponzi scams, or hedge fund managers taking on unnecessary risk

The recent Archegos scandal comes to mind.

The book cautions us to think about how much money we really need – and whether taking on excessive risk is worth it.

Also, there’s no point comparing yourself with others.

They may be living on debt and credit cards, or they may have additional family help.

Not only do people want to play down their inherited wealth or money from family “but they actively try to hide it,” Dalton Conley, a professor of sociology at Princeton University said. “We have this ideology of individualism and worshiping of the self-made man or woman.”

There’s fundamentally no point in making yourself bad by comparing yourself with others.

Especially on social media, which is a highlights reel of others’ people lives – and rarely portray the real picture.

See Netflix’s documentary – The Tindler Swindler – where a Tinder con artist catfished women and persuaded them to give him hundreds of thousands of dollars by pretending to be a billionaire’s son.

3. Building Wealth = Savings Rate

The book argues that building wealth has less to do with income, but more to do with your savings rate.

You may not be able to control your income, but you can control your savings rate.

Savings = Income – Ego

The book recommends you to question your spending.

Is it tied with your ego?

Additionally, we all know high-income earners who are deeply unhappy, because they don’t like their job, but they have to suck it up because they have very high expenses.

Remember these interviews with Singapore pilots whose incomes were affected by the pandemic?

A 50-year-old pilot told TODAY that he is cash-strapped, because he used to earn S$23,000 a month compared with S$13,000 these days.

“My monthly expenses add up to over S$19,000 a month and it’s not the right time to give up my stocks and bonds and sell my properties because I’ll get nothing. I’ll get a second job, I’ll sell my clothes if I have to,” he said.

On the other hand, pilot Terence Soon, 30, said that the pay cuts have not really affected him or brought worry upon his family, despite having a five-month-old daughter to care for.

This is because his expenses are very low.

“My mentor has always told me that you’ve got to treat your salary like you’re just taking your basic salary. Don’t ever count your allowances because you never know there would be a day when suddenly there’s no more flights and you have to survive on your basic pay,” he said.

“So, the amount that I spend per month is really rather low and I try to be consciously aware of that, because how many things could I possibly need?”

Indeed, if we manage our expenses, and keep up a high savings rate, we can build wealth.

This means less stress on keeping a high income, and having the option to leave a job that is making us miserable.

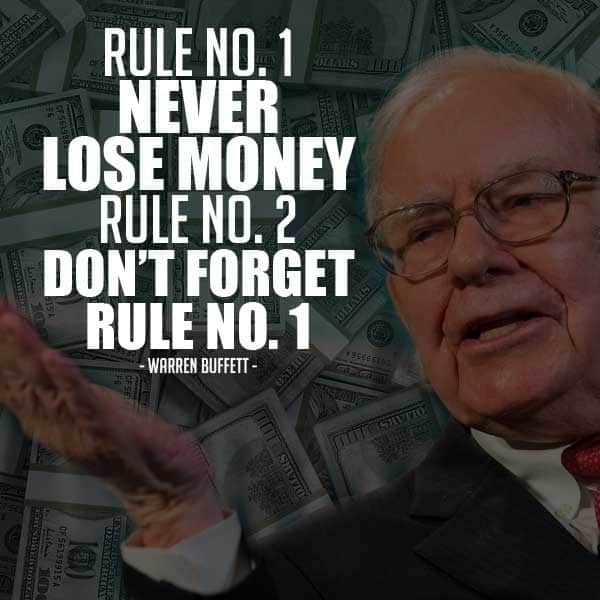

4. Investing is about NOT losing money

Rather than focusing all your energy into making high-risk bets than can generate 10x returns, the author argues that you should focus on not making big mistakes.

Big mistakes cost you big time.

Protect your downside, and you’ll have an upside.

Focus on not losing money consistently, and you’ll benefit from the magic of compound interest.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

5. Getting Wealthy is different from Staying Wealthy

Getting money often involves big risks, but keeping money is often the opposite – to reduce risks.

The book shares stories of how quickly you can lose money.

This is very true.

For instance, Lim Oon Kuin, the founder of collapsed oil trading firm Hin Leong Trading, was slapped with 105 new charges of cheating and forgery in the State Courts last year.

Hin Leong collapsed in 2020 owing US$3.5 billion after the oil price plunge sparked a debt default that exposed years of hidden losses and alleged fraud by the Lim family.

Another example of losing money quickly – Dr Wong Yew Choy, a Singaporean, racked up $44 million in Baccarat debt at an Australian casino in 2017.

This is why it’s important to re-frame once you have acquired a certain level of assets.

It may be time to re-evaluate your asset allocation & risk profile.

This is one reason why Asian investors love buying property.

Buying property is sometimes seen as a means of “forced savings”.

Money is “locked up” – and hence harder to lose (versus more liquid types of investments).

6. Money buys you Freedom

The book emphasizes that the real value of money is that it buys you time and options.

Income has significant diminishing returns after a certain point – research pegs it at about USD 75k/year.

You don’t become happier just because you have a higher income.

Buying expensive stuff rarely brings you happiness, especially if you trying “impress” others.

This article was submitted by a Guest Contributor.