I’ve been getting quite a few questions on MariBank – the digital bank by Sea (Shopee).

It pays 2.88% yield, is SDIC insured, and you can withdraw anytime with no minimum deposit.

What’s not to like right?

So I went ahead and opened an account with MariBank, and let me share my experience with you guys.

Basics: What is the MariBank Savings Account?

MariBank is the digital bank by Sea Limited (Shopee).

If you recall, it was the other recipient of the digital banking licence (other was Grab’s GXS)

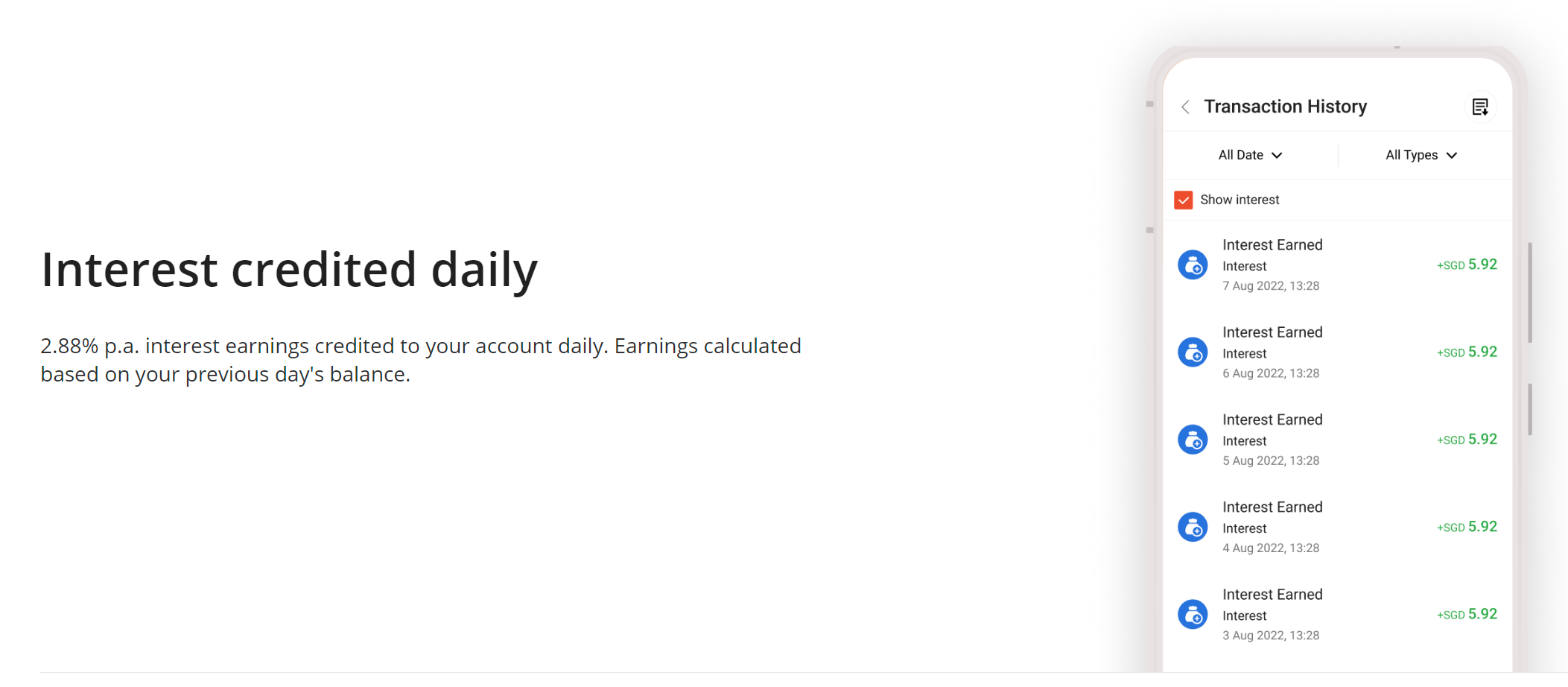

Any amount that you put into MariBank, will earn 2.88% yield.

There is no minimum sum, no annoying hoops to jump through to earn the 2.88%.

And this being a savings account, you can withdraw any time.

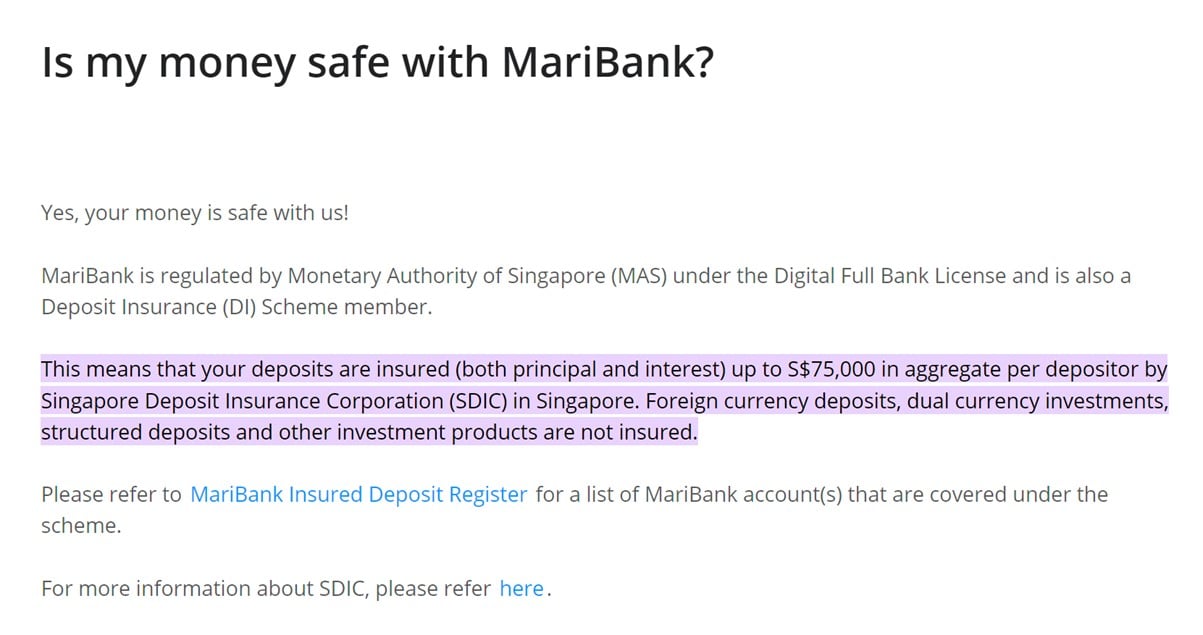

Maribank is SDIC insured (risk free)

Yes – Maribank is a holder of a Digital bank licence.

Anything up to $75,000 is SDIC insured and risk free.

Enough said.

Maribank Promo Code for FH Readers (extra $10 Shopee Voucher, valid till 31 Dec 2023)

After this article, Maribank very kindly reached out to offer an exclusive promo code for FH Readers

Promo code is “MARI28FH“.

Sign up for a Mari Savings Account, and apply the promo code, and get a $10 Shopee voucher with no min spend.

Some important notes:

- Promo ends 31 Dec 2023.

- Users need to link their MariBank account to their Shopee account so that we are able to credit the $10 shopee vouchers.

- Incorrect input of code will not qualify for the reward.

- Voucher will be credited within 3 working days of successful application

- Full T&Cs here

Full disclosure that I don’t get any bonus from you guys using this code, so the benefit is all yours. 😉

Review of the MariBank App?

I played around with the app for a while, and it has all the usual features you would want.

Receive money, transfer money, Paynow, that’s it right?

Anything more fancy than that, you really should just use your DBS/UOB/OCBC account.

Account opening is via Singpass and doesn’t take more than a few minutes.

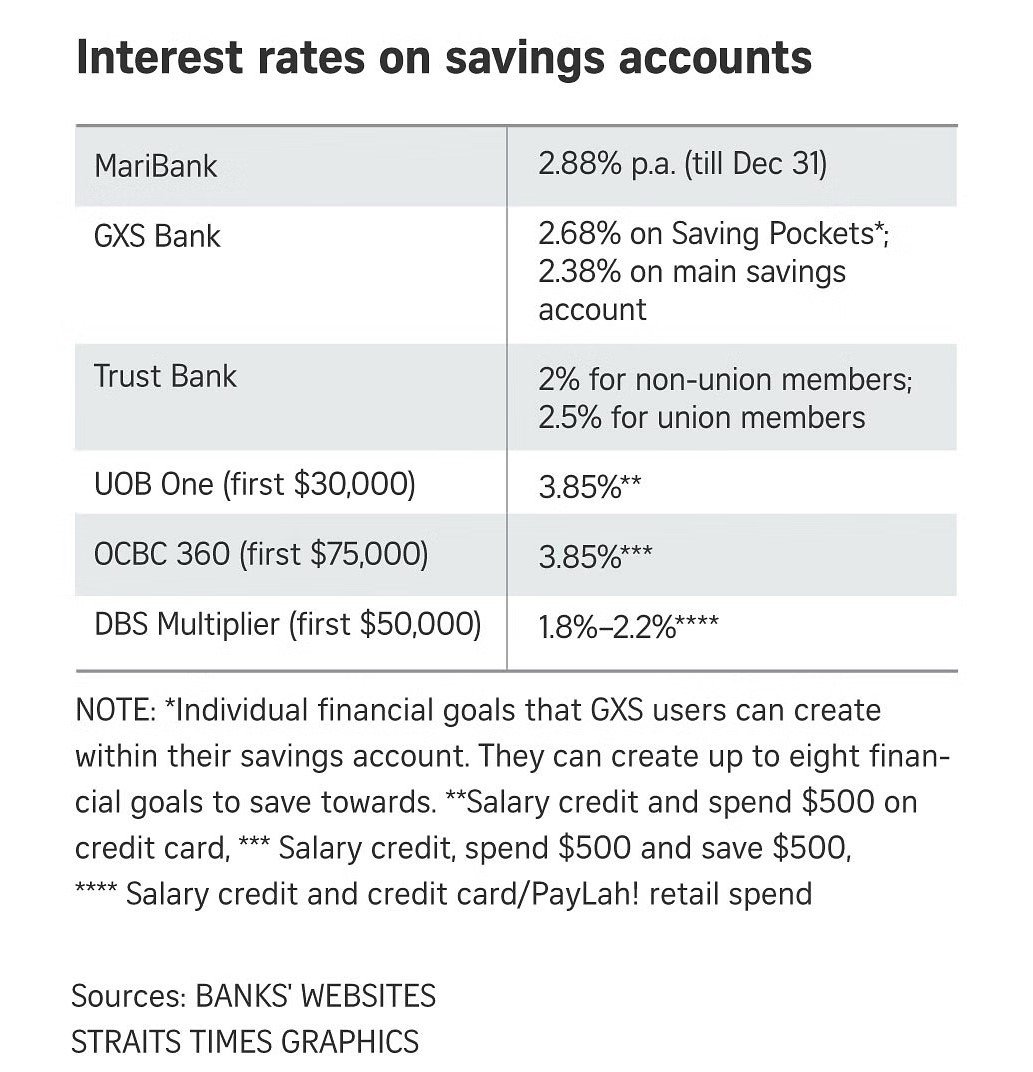

Is MariBank’s 2.88% yield competitive vs other savings accounts?

The Straits Times had a nice table comparing the various interest rates in the markets.

If you just want a savings account to park some cash, and not jump through any hoops to earn the extra interest.

MariBank is the best option out there right now.

The alternatives are GXS (2.68%) or Trust Bank (1.5%), but all are lower than MariBank’s 2.88%.

Of course if you don’t mind doing a salary credit and minimum $500 spend on credit cards, then the best would be UOB One which pays 5.00% on $100,000.

My Personal View on MariBank’s 2.88% yield?

The 2.88% cannot be compared to options where the cash is locked up.

Thos include T-Bills at 3.73%, or fixed deposits at 3.6%.

But the main advantage of MariBank is that the money can be withdrawn any time.

Even if you park it in Singapore Savings Bonds, you’re only getting a slightly higher 3.05% yield (first year), and the money isn’t as liquid as you only get it back the start of the next month.

So I would say for money that can be withdrawn any time, 2.88% is actually a pretty decent deal.

2.88% offer extended to 31 March 2024

MariBank’s 2.88% interest has now been extended to 31 March 2024, after which the base rate is 2.50%.

But I think at this point, all of us are pretty used to moving our money around at the click of a button to chase the highest yielding option.

A month or two ago that was GXS.

Today it is MariBank.

Whatever option may come along the road

It really doesn’t take more than a few minutes to transfer all the money out, given that there are no withdrawal restrictions.

One big advantage of MariBank vs GXS Bank – You can add recipients!

One huge limitation of GXS Bank is that there is no way to save a transfer recipient.

So even if you want to transfer money out of GXS Bank to yourself, you need to manually add the details for each transfer, you cannot save it for future use.

In this day and age, that is unforgivable – and in my view a huge drawback with GXS Bank.

Having to manually verify the account details before each transfer is a huge annoyance, and increases the risk of making a mistake.

With MariBank you don’t have any such limitation.

You can save recipients for future transfer.

That’s a big win for MariBank vs GXS in my books.

But… Singpass Face verification required for transfers

If there is one limitation with MariBank though, it is that Singpass Face verification is required for money transfers.

So when you transfer money out of MariBank, not only do you need to (a) key in your Pin, you also have to (b) pass the Singpass Face verification.

I suppose you could argue this is a good thing because it reduces the risk of fraud.

But the first time I tried this (while lying in bed), it took me a couple of tries to pass the verification.

So for those of you who have issues with face verification, or who like to do your banking in bed / in the dark (I’m not judging), this is a point to note.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Maximum deposit limit of $75,000 for MariBank Savings Account

Do also note that the maximum deposit limit of the MariBank Savings Account is $75,000 (similar to GXS Bank).

I don’t really see this as a limitation, given that I wouldn’t want to top up the account beyond the SDIC insured limit in any case.

But worth noting.

$100 account opening bonus for MariBank Savings Account

Note that if you open a new MariBank account, you can also get $100 worth of Shopee vouchers.

You just need to connect your MariBank account to Shopee, and deposit at least $1,000.

The Shopee vouchers are a discount on spend though (eg. $50 off for $500 spend), so it’s not really cash.

But still, not too bad if you buy on Shopee frequently.

My personal views on MariBank Savings Account?

For what it’s worth – I opened an account on MariBank this week, played around with it, and promptly transferred half of my funds on GXS (and some spare cash in DBS) into MariBank.

It’s nothing much to shout about really, it’s everything you would expect from a digital bank.

But it’s 2.88% yield, SDIC insured (risk free), with no hoops to jump through, for any cash in the account.

That’s a pretty decent deal for cash that is just lying around idle.

I hate that I cannot save transfer recipients on GXS Bank, and that problem is solved with MariBank.

With a higher interest rate too.

I’ll probably use MariBank as the main place to park spare cash that’s not going into T-Bills.

At least until the next better option comes along.

Love to hear what you think though!

Will you put your money into MariBank?

Maribank Promo Code for FH Readers (extra $10 Shopee Voucher, valid till 31 Dec 2023)

After this article, Maribank very kindly reached out to offer an exclusive promo code for FH Readers

Promo code is “MARI28FH“.

Sign up for a Mari Savings Account, and apply the promo code, and get a $10 Shopee voucher with no min spend.

Some important notes:

- Promo ends 31 Dec 2023.

- Users need to link their MariBank account to their Shopee account so that we are able to credit the $10 shopee vouchers.

- Incorrect input of code will not qualify for the reward.

- Voucher will be credited within 3 working days of successful application

- Full T&Cs here

Full disclosure that I don’t get any bonus from you guys using this code, so the benefit is all yours. 😉

This article was written on 22 Sep 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

– Get up to USD 800 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 800 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

I took the dive into Maribank when I saw the promo banner on Shopee 9.9 when they dangled 300 SGD of Shopee vouchers. I clicked and after a 10min research I took the plunge. It was 2.5% interest then. A week after my first tranche went in, being satisfied with helpful and prompt customer support and liking the app plus its features (barebones but acceptable), I went in with a second tranche. When the 2.88% promo dropped, I put in a third tranche. Clearly this strategy was conceived by clever rational buggers working at SEA who knows that there’s no good reason to say no to this if you have spare liquid capital lying around waiting for good yields. Good things don’t always last is a good maxim to live by so I await the day when their T&C and interest rate retreats. After all they are smart buggers and smart buggers hate losing money. Cheers

Haha very interesting. Thank you and appreciate the sharing!

UOB stash account gives higher interest rate of 3% of Upto 100K in deposits. No lock in and you can move your funds around.

Also MariBank is only for Citizens and PR. While GXS is for Citizens, PR and Expats as well. That’s a huge win for GXS even though the rate is only 0.20% lesser.

UOB Stash you need to maintain 100k for the full 3%. And if you drop the balance vs previous month you lose all the interest. I used it for a while but found this to be a big limitation.

Good point on GXS – thanks for raising this.

Anyone noticed you have to spend $920 in order to utilise the $100 voucher fully? Slightly misleading for those who don’t read the fine print.

Yes that is right. I didnt think it was misleading though, it was fairly clear in the promotional picture.