REITs have been getting a lot of flak recently due to the rising interest rates. A lot of investors out there have been swearing away from REITs in the belief that they will underperform in the coming months.

To me, I’ve always viewed REITs as a long term investment in the underlying real estate. As the price for real estate drops, my appetite for real estate goes up, as long as they are quality assets.

So I was very thrilled when I received this question below on the Financial Horse Forums (minor edits for clarity):

“Hi FH

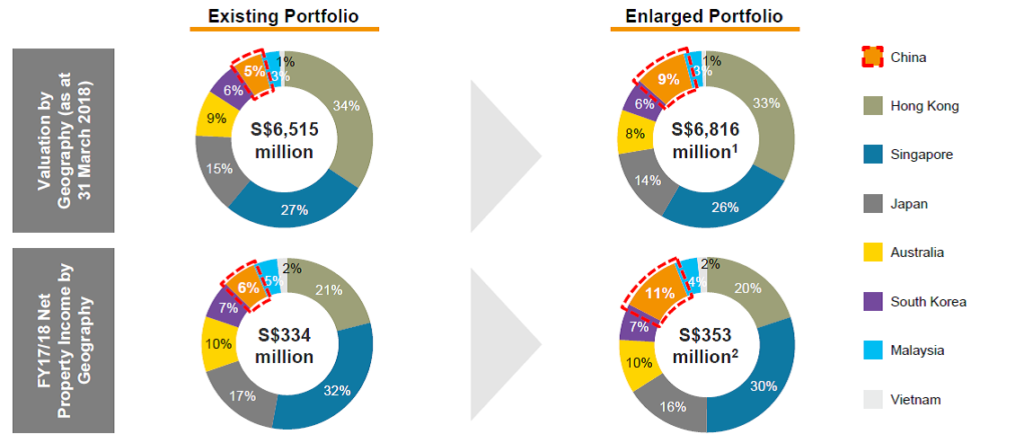

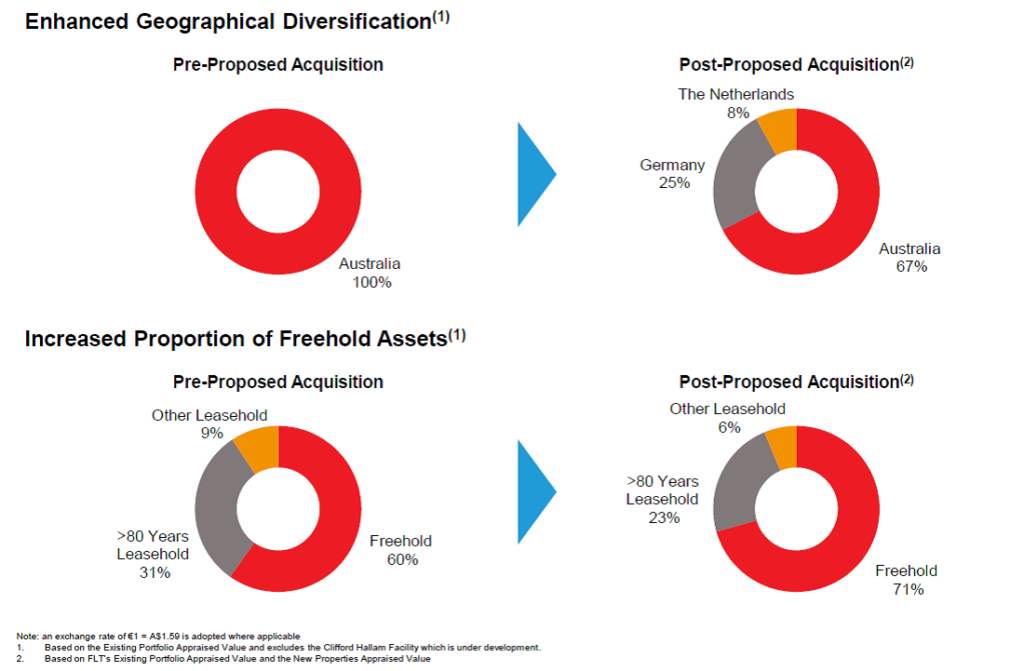

I recently attended the EGM of MLT (Mapletree Logistics Trust) and they mentioned about increasing their exposure to China from the current 9% (after recently acquiring the 11 China properties from their Sponsor) to 25%! During this same period, FLT (Frasers Logistics & Industrial Trust) is doing an equity fund raising to acquire 21 properties in the logistics hub of Europe (Germany and Netherland).

What is your expert view on these 2 trust in terms of their long term prospects. Which is a better logistic reit play if you have to choose one to invest? I noted 93% of the property in FLT’s property above is freehold while the Chinese logistic property all has 50 years lease max although their selling point is that they are positioning for the OBOR play ( china’s one road one belt)

Thank you!”

Challenge, accepted!

Do note that I am going to assume that readers already understand the basics of a REIT and how to evaluate REITs. If you don’t, there is a nice article I wrote a while back that you should read.

Basics: MLT and FLT

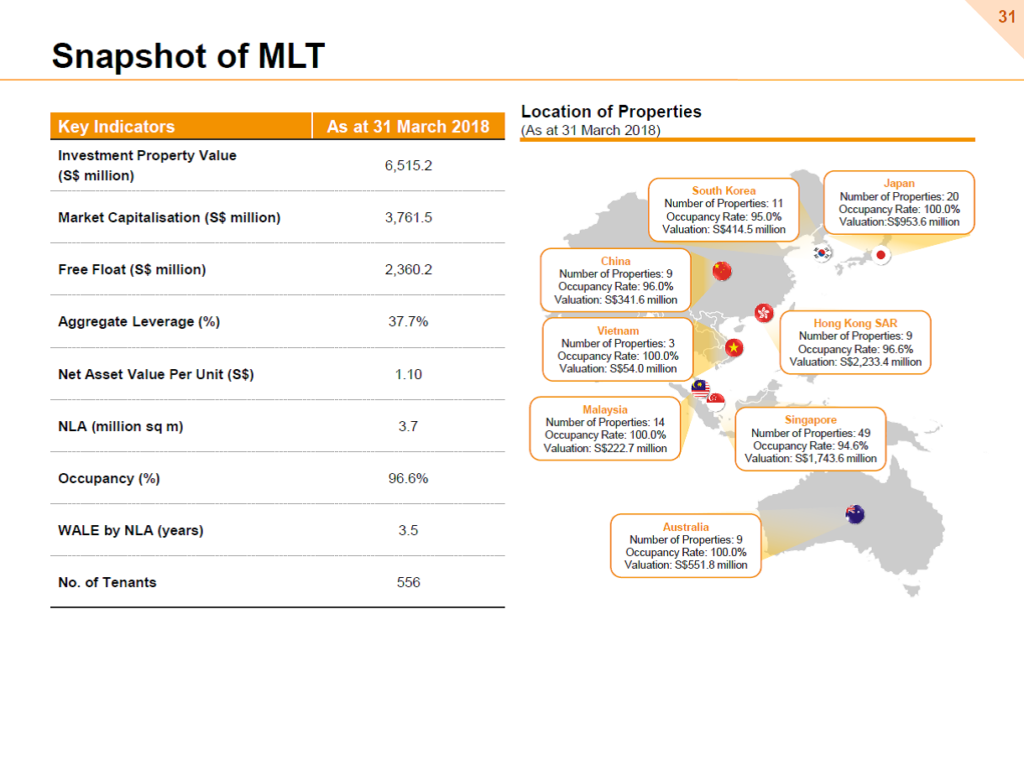

Mapletree Logistics Trust (MLT) and Frasers Logistics & Industrial Trust (FLT) are both logistics REITs (they own warehouses), sponsored by Mapletree and Frasers respectively.

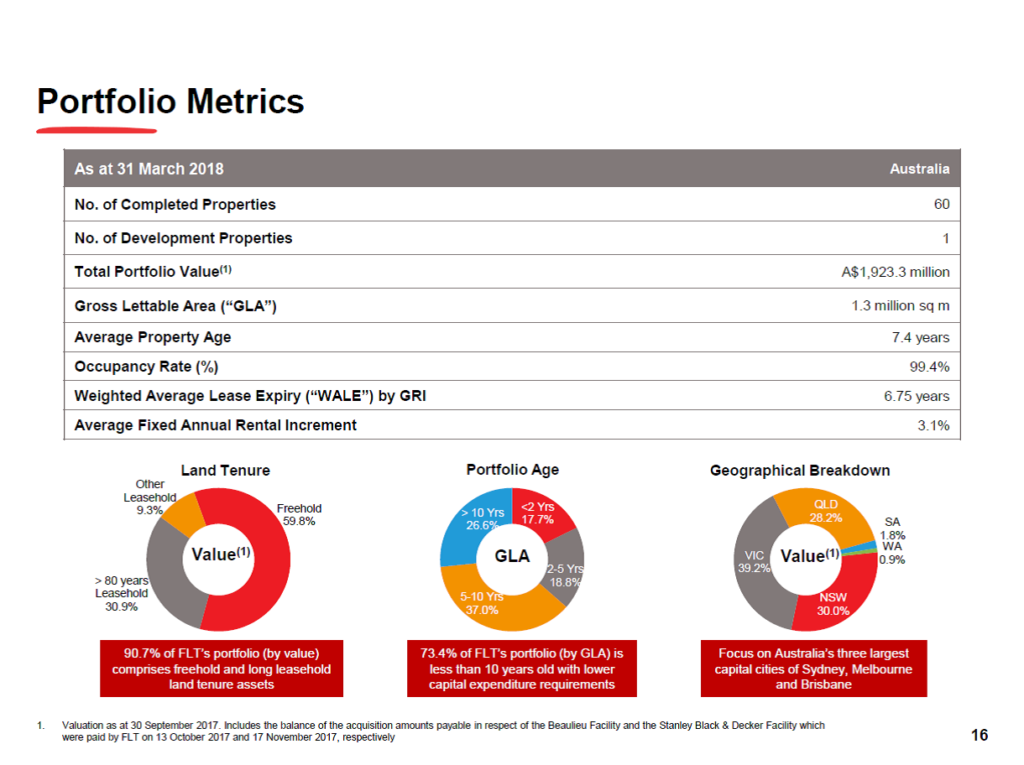

As you can see from the slides below, MLT is an Asia focussed logistics REIT, while FLT (pre-acquisition) is a 100% Australian logistics REIT.

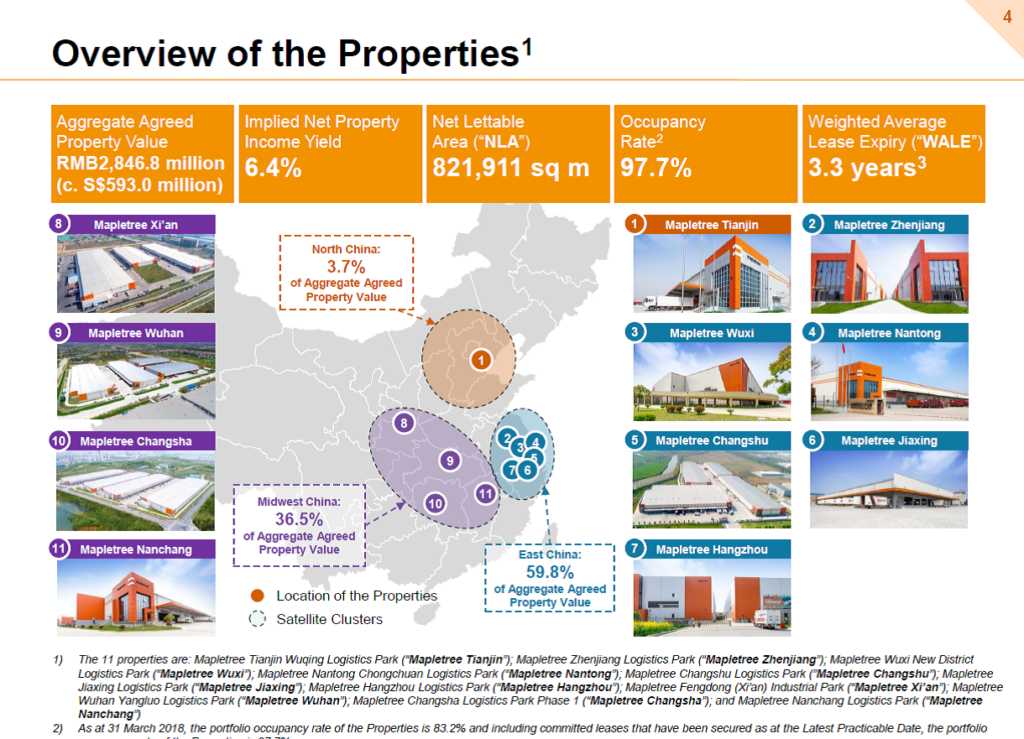

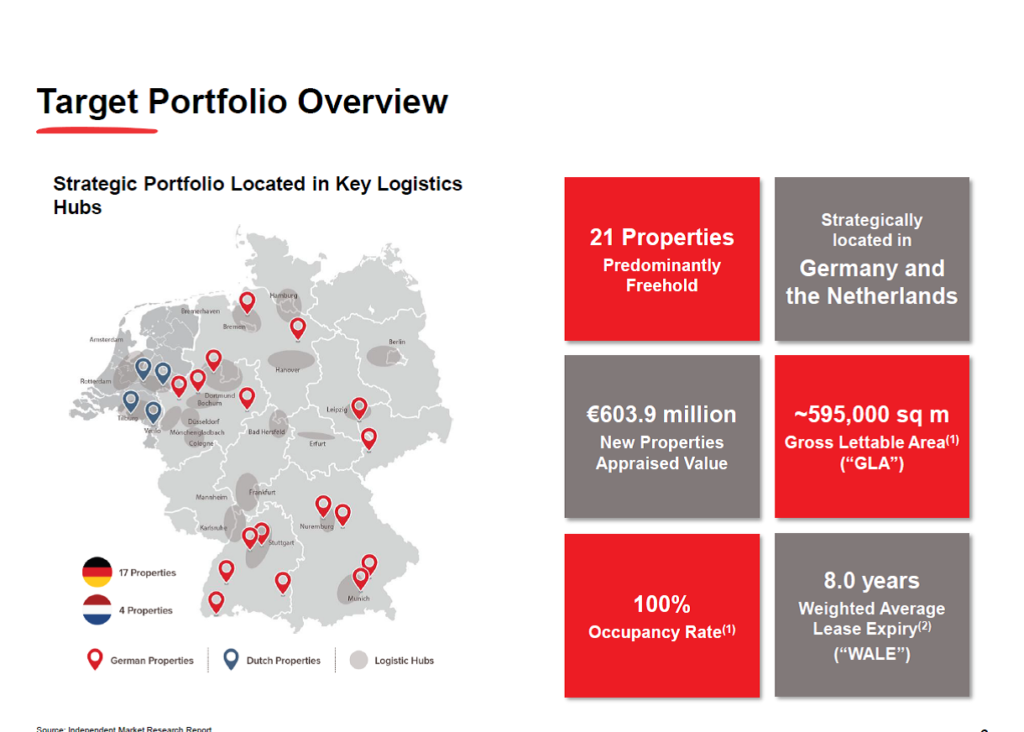

MLT is currently doing a S$600 million acquisition of 11 logistics properties across China, while FLT is doing a S$900 million acquisition of 21 logistics properties in Germany and the Netherlands. Accordingly, both REIT are going down very different paths, with MLT going heavily into China, and FLT going heavily into Europe.

Valuation (P/B and Yield)

To me, valuation metrics are like looking at prices on Carousell. For the same product, there will be idiots quoting 20% above market price, and there will be idiots who sell at a huge discount to the retail price. As long as you know what you’re buying, you’re best off buying from sellers who price low.

I’ve set out the valuations for both REITs below (prices as at 14 June 2018). Please note that these are post-acquisition numbers:

| MLT | FLT | |

| Market Capitalisation | S$3.79b | S$2.11b |

| Price | S$1.23 | S$1.06 |

| NAV (Book Value) | 1.11 | 0.90 |

| P/NAV (Price to Book) | 1.11 | 1.18 |

| Yield (Pro Forma) | 6.22% | 6.49% |

| Gearing | 37.5% | 35.4% |

Note: I calculated the yield using the pro forma DPU numbers from the respective acquisition circulars, so there are a number of assumptions behind them (as set out in the MLT circular and FLT circular).

A couple of observations on the valuations:

- MLT’s market cap is significantly higher than FLT (80% higher)

- FLT is trading at a higher P/NAV than MLT, but has a higher yield. This looks like FLT’s properties are quite conservatively valued.

- Gearing metrics are approximately similar.

The price movements of both REITs (Blue is MLT, Red is FLT) are set out below. Both seem to be exhibiting similar patterns, being a huge run-up last year, and a correction in Feb this year in line with global yield products.

On the valuation front, I would say both REITs are very similarly valued, so it’s hard to pick between the two from here.

Sponsor

MLT is sponsored by Mapletree Investments Pte Ltd (Mapletree), while FLT is sponsored by Frasers Property Limited (Frasers). Mapletree is Temasek-owned, while Frasers has Thai owners (Thaibev). You can read into that what you will, but both are highly experienced property players and are behemoths in their own right. I don’t think either of these boys are going to get pushed around any negotiating table.

Mapletree has copious assets and expertise in Asia, and more specifically, China. This means that MLT has a huge ROFR pipeline from China, and as expressed in their recent EGM, that is where future growth will be coming from. The same is true for Frasers in Europe.

MLT is currently doing a S$600 million acquisition of 11 logistics properties across China, while FLT is doing a S$900 million acquisition of 21 logistics properties in Germany and the Netherlands. Both REITs are acquiring the portfolio from the Sponsor. I expect this trend to continue going forward, as their respective Sponsor start to divest mature assets into the listed REIT.

Personally, I’ve always had a soft-spot for Mapletree. They are the latest of the large developers to join the REIT game, and I think they really learnt from the mistakes of their peers. This is reflected in their corporate practices (they don’t do financial engineering), and I like their progressive corporate culture and strong corporate governance.

I really want to give the lead to Mapletree here, but I think that would reflect a personal bias. To be very objective, both are high quality, solid sponsors, and you won’t go wrong with either of them.

Geographical Allocation

The pre and post-acquisition geographical allocations of both REITs are set out below.

To sum it up very simply, MLT is diversified across Singapore, Japan, Australia, Korea, China and Hong Kong. Going forward, expect the China and Hong Kong portfolio to eventually form up to half of the portfolio. FLT is diversified across Australia, Germany, and the Netherlands. Going forward, it is likely that the European portion of the portfolio will increase.

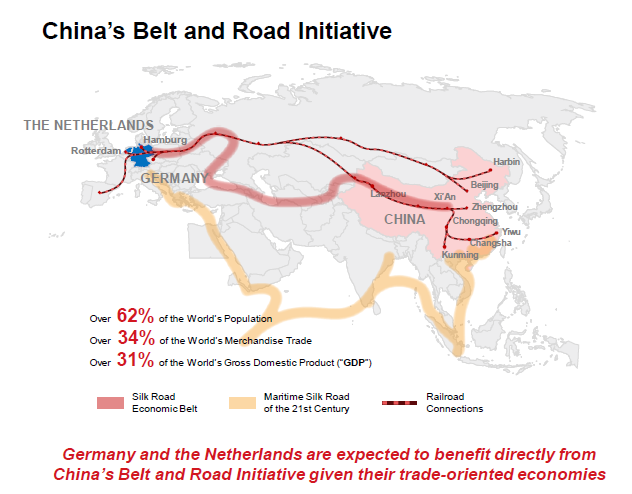

I found it very interesting that both REITs touted their acquisitions as a play on the China One Belt One Road (OBOR) initiative. If you take a look at the maps below, it seems like both are not wrong. MLT will hold assets along the China portion of the OBOR, while FLT will hold assets on the western European part of the OBOR.

If we take a step back, what this means is that even though both are logistics plays, comparing MLT and FLT is a bit like comparing apples and pears. Both have vastly different geographical focuses.

But that’s not doing anyone any favours. I’m going to set out my personal opinion below, and readers can assess for yourself (feel free to disagree in the comments below).

Personally, I am far more bullish on China real estate than European real estate going forward.

The way I see it, Western Europe is a highly developed market, and a lot of the properties are richly valued. What Europe has going for it though, are the incredibly low interest rates. If you buy a warehouse at a 5% NPI Yield and borrow at 1%, that’s a massive 4% spread you’ve made right there. So you’re earning on the income spread every year, and if property prices gradually appreciate, you also get to earn on the capital gains. It’s a really good deal, and it’s why other REITs like CCT have gone into Europe recently as well. In fact, the only other geography with a similar dynamic is Japan.

The problem with this though, is that the ECB literally just announced their plan to increase interest rates in September, and cut QE starting from next year. Without the ECB backstop in place, I’m not fully certain what will happen to interest rates in Europe. The entire Eurozone is, in my opinion, one political crisis away from a massive rerating of bond prices (just look at Italy).

Not only that, but the long term future for Europe is not clear to me. I’ve always felt that the EU in its current form is not workable, and that there would eventually have to be huge political change.

China on the other hand, has a different dynamic. The onshore interest rates are not cheap (which is why it looks like MLT funded offshore), and property prices can be quite fully valued. However, China is undergoing a massive economic transformation as they transition from an export driven economy to a consumption fuelled economy. If you believe in the China miracle (as I do), I think the next few decades are going to see hundreds of millions of Chinese consumers being lifted into the middle class. A rising tide lifts all boats, and what MLT has going for it is this massive Asian/Chinese tailwind.

It’s the same story for the rest of MLT and FLT’s portfolio. MLT’s current portfolio is Asia centric, while FLT’s current portfolio is wholly Australian. Australia is a highly developed market, so while you get stability, you may not have the same kind of growth that Asia can offer (but of course, this comes with greater risk as well).

Again, it’s going to be a tie here. Both REITs have very different geographical focuses, and the one you pick will likely reflect your world view of the decades to come.

Quality of Assets

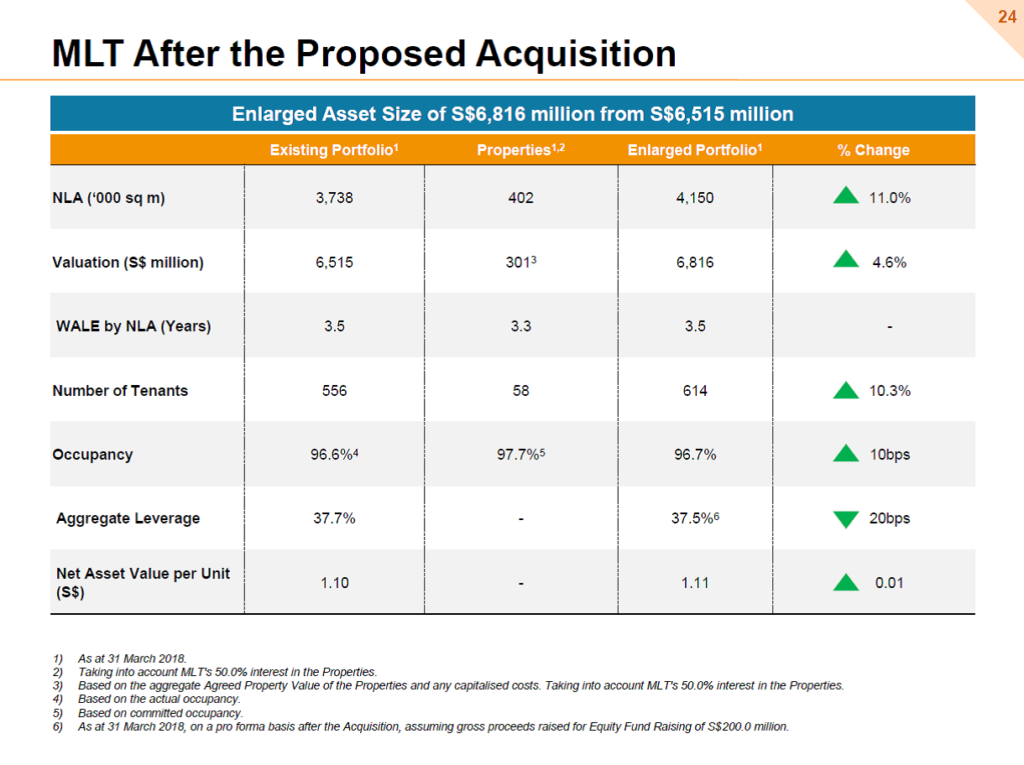

I’ve added some obligatory pictures on the NPI Yield, NLA, Occupancy and WALE numbers below. One notable point that jumped out was that the MLT acquisition portfolio has a WALE of 3.3, while FLT’s is 8.0. This is reflected in the enlarged portfolio as well (3.5 for MLT vs 7.1 for FLT). While this may look bad at first glance, I think it merely reflects the different market practices in their respective markets.

Australia and Europe are developed markets where tenants are more willing to commit to a longer term lease in exchange for lower rent. By contrast, Asian tenants are less willing to lock themselves in to a long term lease. The flipside of this of course, is that if rentals up go, MLT has greater flexibility to enjoy the upside, while the longer term leases with FLT will limit the upsize to a certain extent. It’s a quirk of the home markets, so there’s not much we can do about it, but it’s worth considering when deciding whether to invest.

A point raised in the original question was that FLT is acquiring Freehold land, while China is acquiring Leasehold land. Again, this is a quirk of the home markets. China does not have a concept of Freehold land, and 50 year commercial leases are the norm. What I’ve been told, is that when your lease tenure comes to an end in China, you can approach the local authorities and pay a nominal fee to get the lease renewed. Of course, there’s always a bit of uncertainty over whether the regulations will change in future, but I view these as risks that come with the jurisdiction. If you want to invest in China, these are the risks you will need to assume.

I won’t go into detail on the individual properties, because these are portfolio deals (there may be one or two bad eggs, but will be good ones to offset those). But I will say that both Mapletree and Frasers are highly reputable Sponsors. If they are prepared to divest assets into a REIT, I trust that they will be quality assets.

Again, it’s going to be a tie here, because it really depends on which geographical allocation you prefer.

Closing Thoughts

I think what is clear from the discussion above, is that MLT and FLT are tied on most counts. At the end of the day, both are logistics plays, but MLT has a Asian focus (HK and China), while FLT has an Australian/Europe focus.

Personally I hold a position in MLT, because I like Mapletree as a Sponsor, and I am bullish on the prospects of Asia (and specifically, China). But I get that not everyone will share my enthusiasm, so feel free to disagree.

If you like Australia/Europe, FLT is a good logistics play. If you like Asia, MLT is a good buy. If you really can’t decide, you can just buy both to diversify, and be done with it.

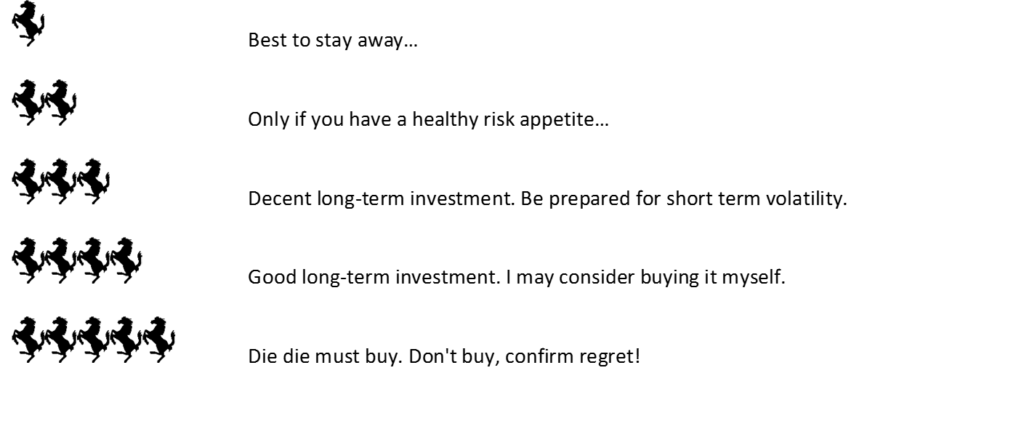

Holistically though, I do like both MLT and FLT as a long term investment, and I will give both a 3 Financial Horse Rating. However, as these are yield plays, please expect some volatility going forward as the capital markets reprice yield products. If you are a long term investor such as myself, it really doesn’t matter, because I am happy to take a long term position in the underlying estate, and collect my semi-annual distributions over a multi-decade period.

Note: Full Disclosure, I have an existing position in MLT, but I have no plans on adding to my position in the next 3 trading days. Read into that what you will!

Financial Horse Rating – MLT/FLT

Financial Horse Rating Scale

Long Weekend Giveaway

Financial Horse is doing a giveaway for the Hari Raya Long Weekend! I have 3 tickets to Seedly’s Exclusive Meetup: Coffee Meets Investing to giveaway (normal price is S$30 per ticket).

The rules are simple:

- Like the Financial Horse Facebook Page or join the Facebook Group

- Comment on the Facebook post on 1 stock, ETF or investment platform that you want Financial Horse to review (Hint: I will write an article on the winning stock).

Note: There is 1 thread on the Facebook Page and another on the Facebook Group, so feel free to use either.

The comments that receive the most likes (or that I like the most) will win the tickets. The winners will get to choose between either a pair or a single ticket. Competition closes on Monday, 18th June!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Another well written article, thank you.

No worries, glad you enjoyed it. 🙂

Thanks for the great article! As you say, both have strong and reputable sponsors with strong pipelines. So which to buy will probably depend on our view on which market has a stronger long term outlook. ie a bet on china overall growth and impact on their pan asia portfolio and their inner tier cities, e commerce( looking at their heavy presence in the latest 11ppty) and success of the china govt led obor initiative vs EU’s…. ( I am trying to think what is the big growth story they have…)

Hi FH, Thanks for the great article! Agree both are well managed and have strong sponsors with strong pipeline. so the choice could be boil down to comparing the long term outlook of the 2 regions that they seek to expand into. on one side, china growth and impact on their pan Asian ppty and the inner tier cities where these 11ppty are mainly located + the Chinese e commercial growth story and their expansion into asia+ china led obor initiative. vs the EU’s… (trying to think what is their big megatrend story..)

Hi Jon!

Yes, absolutely right. I think it’s very hard to pick between the two based on things like Sponsor, valuations etc.

I think the key is to decide whether you prefer to invest in Australia/EU, or Asia/HK/China. EU’s growth story won’t be as compelling as China, but what they have are low interest rates, and a relatively stable economy. China has blistering fast growth, but whether this growth can be sustained is not fully clear as well.

Personally I like Asia, and I like Mapletree, which is why I own MLT. But if you are really undecided, you can just buy both and be done with it.

Cheers!

A very incisive review. Both are good quality REITs with strong sponsors. Thank you for sharing.

Thanks, I am glad you enjoyed this article. Welcome to Financial Horse 🙂