At its current price of S$0.78, assuming a 4.64 cents yield for FY2019 (from the IPO prospectus), Netlink Trust (CJLU.SI) is trading at a forward yield of 5.95%, which is actually pretty decent.

A lot of investors and pundits have commented that Netlink Trust is a boring counter. As you can see from the post-IPO chart below, its share price has truly gone nowhere. After accounting for the recent FY2018 distribution payout, investors who bought in at IPO are about breakeven after holding for almost a year.

But when it comes to dividend plays, boring is exciting stuff to me.

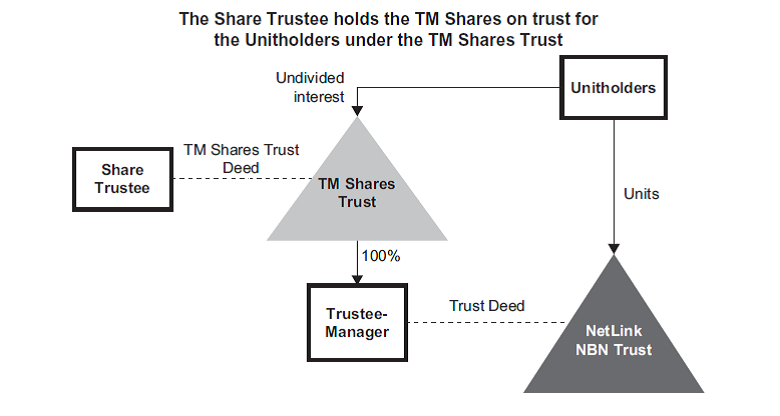

Basics: What is Netlink Trust

It took me quite a while to figure out what exactly Netlink Trust does (its prospectus isn’t exactly bedtime reading).

Simply put, Netlink Trust owns a large majority of the Fibre network in Singapore, that the Internet Service Providers (Singtel, M1, Starhub, MyRepublic, Viewquest) leverage on to provide Fibre broadband to you.

Imagine if you sign up for a S$39.90 a month Fibre broadband connection with M1. If you are a new user, you have to pay a S$200 dollar plus fee for them to set up the Fibre terminal in your house. This fee is payable to Netlink trust, but as it is usually free of charge for new users, M1 will stomach the fee for you. On top of that, you also have to pay a monthly fee of S$13.80 to Netlink trust to “rent” their Fibre network, so that M1 can provide the Fibre broadband to your house. Of course, this S$13.80 fee is baked into the S$39.90 monthly fee, so you don’t actually see it as M1 handles all the backend.

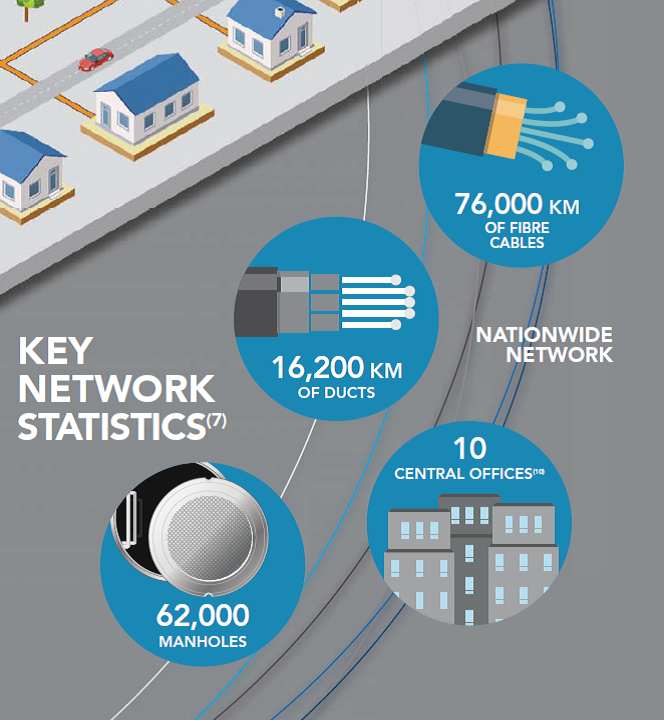

To be more specific, Netlink Trust owns the (1) Fibre cable, (2) tunnels that are used to lay Fibre cables, (3) manholes and (4) central offices where the Fibre cables emerge. They earn a “rental fee” from anyone who taps on their Fibre network, which can include residential homes, corporates and the Internet of Things (things like internet capable traffic lights). They also charge ISPs rental to install switches and routers at their central offices.

One way to see this is as a REIT, only that instead of owning real estate, you are owning Singapore’s Fibre network, and instead of collecting rent, you charge customers a fee to use your Fibre network.

What I like about NetLink Trust

Personally, I hate writing the section about what I like about a stock. I always felt there was a risk of believing your own bullshit. To me, the best way to look at a stock is to look at its key risks, and take a position on whether the risks are manageable. I will keep this section short.

Utility / Bond like nature

NetLink Trust currently trades at a 5.95% forward yield, when using the projected 4.64 cents distribution from their IPO prospectus. Their recent FY2018 DPU outperformed the forecast by 5%, and they even provided a confirmation that:

The Trust Group expects to deliver the distribution forecast as stated in the Prospectus for FY19. The Trust Group expects revenues from key connection services to meet the forecast for FY19, however, overall revenues may be affected by lower installation-related revenues.

With such clear language, I expect them to at the minimum meet the 5.95% forward yield, and likely even surpass it.

A Fibre connection, and internet itself, is in many ways a necessity in Singapore. With the cheapest plans starting at S$29.90 a month these days, there really is no reason for anyone to not be on Fibre. The government has done a great job in rolling out the Fibre connection and keeping prices low, so kudos to them on this. But what this would mean for investors, is that NetLink Trust can be viewed more as a utility stock or as a bond, that is less exposed to economic conditions.

If you lose your job tomorrow, you may sell your car and dine out less often, but would you really call up M1 and ask them to cancel your Fibre connection? For this reason, I view Netlink trust as a good portfolio diversification and a bond or utility proxy, as it may potentially display counter cyclical price action during the next crisis. Yahoo Finance has a great definition for this:

Counter–cyclical or defensive industries are those that do well in economic downturns, since demand for their products and services continue regardless of the economy. It’s a niche industry financial performance negatively correlated to the overall state of the economy.

Not only that, but the prices that Netlink charges are regulated by IMDA. This is both good and bad, as it means that prices will never fall, but the rate of increase is tightly regulated (subject to 5 year reviews). The question that flows naturally from this is then, where does growth come from?

Growth

The way I see it, Netlink trust’s future growth will come from the following avenues:

Population growth / new homes

There’s a fantastic quote from their prospectus that sums up this point:

MPA forecasts residential premises, defined as units (occupied and unoccupied) that are currently available in the market, including HDB units, condominiums and landed houses, to grow at a CAGR of 2.3% between 2016 and 2021. During this period, approximately 170,000 new residential premises are expected to become available in the market. It is further expected that all new units will be Fibre-ready on account of existing regulations governing the deployment of Next Gen NBN in Singapore. The phasing out of older broadband technology types as well as the availability of ready-to-use Fibre connection points, among others, are expected to encourage and facilitate the switch and subscription to Fibre broadband services.

Simply put, with property developers and HDB building new homes at a frantic pace, that translates into a lot of new homes which require a Fibre connection. With more Fibre connections, not only do you earn on the installation fee, you also earn on the monthly recurring fee.

In the long run though, Netlink trust’s growth is going to be pegged to population growth. No matter how many new homes are built, unless Singapore’s population grows, there will not be new households to sign up for a new Fibre connection. There’s some uncertainty over the government’s plans on this, but I remain sanguine, because population growth is the main factor that will propel all asset prices in Singapore. Without this, the property that almost all Singaporeans own will not be seeing decent price appreciation as well.

Corporate users

The penetration of Fibre among corporates is not as prevalent as it is for residential homes. Going forward, there’s a lot more potential for growth here. Netlink Trust isn’t as dominant in the corporate space as it is in the residential space, but as the pie grows, I do expect them to enjoy the growth.

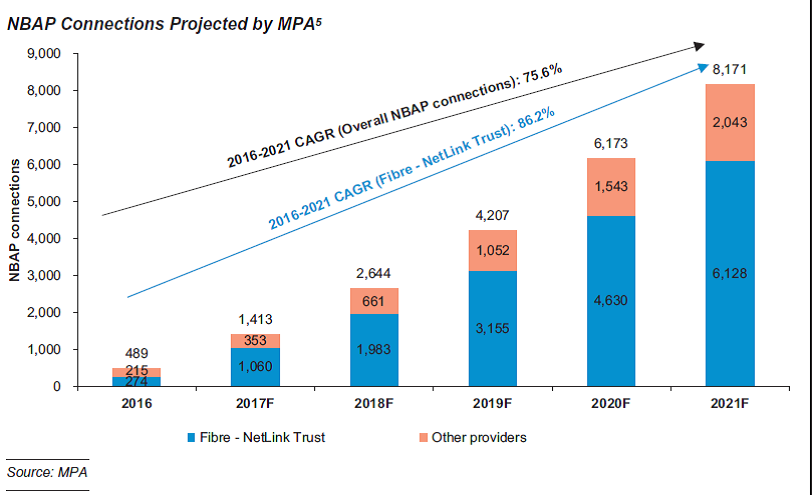

New uses of Fibre – IOT

The prospectus talks a lot about NBAPs, or non-business access points. These are basically locations that do not have a physical address or postal code, but which require a Fibre connection nonetheless. This is mainly the Internet of Things category, such as an internet enable traffic light or camera, and is being touted as a major growth area. I have my doubts on whether this category will grow as fast as projected (do traffic lights really need a 1GBPS Fibre uplink?), but there’s nothing much to lose here. If it goes up, you enjoy the growth, if it doesn’t you still have the main residential and corporate markets.

Price increase will be small, but is still there

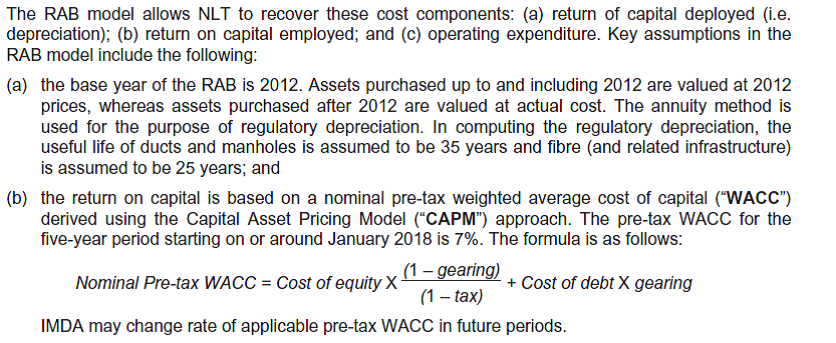

The price that Netlink trust can charge is heavily regulated by IMDA. The assumptions used are disclosed below. The key takeaway is that unlike a REIT, you’re not going to be able to raise rents after every lease expiry.

But in the long term, I do expect a gradual appreciation in prices. The formula is subject to 5 year reviews by IMDA, and given that Netlink trust is now largely held by public shareholders, I expect them to make some concessions.

What I am concerned about

There are 3 key risks that I am concerned about.

Technological change

This is the risk that Fibre becomes obsolete. Before this, broadband was via cable (Starhub) or telephone lines (Singtel). Before that still, it was via dial-up. With the pace of technological change, it is inevitable that Fibre will eventually be replaced by a newer technology. The key question however, is when will that change happen. At a 5.95% dividend, assuming no capital loss, you have already enjoyed a 60% absolute return in 10 years.

Netlink makes some arguments on the resiliency of their network below:

Further, in MPA’s view, wireless broadband connection is complementary and not a substitute for Fibre, as it cannot provide the same reliability and average speeds of a wired broadband service provided via Fibre. Wireless broadband services such as the current 4G and potentially future 5G networks may suffer from network congestion as well as signal degradation caused by physical obstructions to the cellular signals, such as buildings and walls, especially in a heavily built-up environment in Singapore. As such, MPA believes that wired connections will continue to be the most common type of connection and potentially future 5G networks, which will require a relatively large number of base stations for optimal performance, will require Fibre network infrastructure backhaul.

They also go on to elaborate on the Fibre vs Wireless internet/5G debate, the argument being that Fibre will still remain relevant before Wireless broadband has (1) limited speeds, (2) lack of unlimited data plans, (3) network latency and (4) network coverage and reliability.

I am a lawyer by training, so perhaps I am not the best placed to comment on this. But as a millennial, I am inclined to agree with them. Wireless broadband has far too much lag and unreliability in terms of speed and connection to be a true replacement for a wired connection. And with the blazing fast speeds that a Fibre network can sustain, I personally think that it may be quite a while before the Fibre network becomes obsolete. It is very possible that future technological advancement may address all the issues described above, but in the interim, I am happy to collect my 5.95% yield.

Replacement cost

Like real estate (or MRT tracks), Fibre assets require constant upkeep. But when your assets are buried underground all over Singapore, and with 76,000 kilometers of it, replacement costs can be very real.

Here’s what Netlink trust has to say:

While the typical accounting lives of Fibre cables are 25 years, in practice, these physical assets last much longer, especially in the case of the Trust Group, as large components of the Fibre network infrastructure are buried underground in Singapore and therefore less exposed to weather and other elements that cause wear and tear, according to MPA. Hence, the Trustee-Manager believes that the durability and longevity of the Trust Group’s Fibre cables means that its existing network will continue to operate for many years to come without the need for any material upgrade or replacement of Fibre cables.

Again, I’m not the best place to confirm the veracity of this statement. But 25 years is a long time. If the Fibre cables can last the full 25 accounting lifespan without requiring major replacement and going obsolete, at approximately 6% returns a year I am already a rich man and enjoying retirement.

How much of a monopoly is Netlink?

Netlink says that:

In MPA’s view, building another nationwide Fibre network infrastructure to achieve the same extent of coverage to that of the Trust Group would be both logistically and financially challenging. As such, the Trustee-Manager believes that there are high barriers to entry in the creation of similar or competitor networks.

I definitely agree with this. Given the size of Singapore, it doesn’t make sense for another player to build a nationwide Fibre network to rival Netlink. It would entail billions of dollars in investment, without much to show for it.

Netlink trust is the main player in residential Fibre connections (about 76% in 2017). However in the non-residential (corporate space), it controls only about 32% of the market share. It turns out the competitors, Starhub and Singtel, have large Fibre connections in the CDB area that translates into heavy competition for Netlink.

In particular, the Trust Group faces competition with respect to CBD buildings and certain large business parks where many of the Trust Group’s non-residential competitors have established and continue to build on their own Fibre networks. Many such networks were built prior to the establishment of the Trust Group. … The Trust Group’s principal competitors include Singtel and StarHub. The Trustee-Manager believes one of the Trust Group’s competitive advantages in its non-residential business is its extensive nationwide network coverage, as compared to the networks of its competitors, which are concentrated in the CBD and large business parks. This also allows the Trust Group to access non-residential end-users across Singapore, in particular SMEs located outside the CBD, in a timely and cost efficient way. Further, as an independent network provider, the Trustee-Manager believes that the Trust Group offers an attractive neutral option for Retail Service Providers who do not have an established network as compared to competitor networks affiliated with certain Retail Service Providers.

But to be fair, I do believe Netlink’s argument that once you go beyond the CBD and business parks, no other player has the same extensive infrastructure to rival Netlink, so Netlink may be able to grow market share in this aspect. Following its divestment from Singtel, Netlink is also now perceived to be an independent player, so if you are a new player (TPG Telco for instance), you are more likely to rely on Netlink for your Fibre than to go to a rival such as Singtel or Starhub.

It’s not 100% a monopoly like Google, but its enough of a monopoly for me. Don’t forget these are real world assets where barriers of entry and economic moats are real, despite what Elon Musk may say.

What I am less concerned about

Rising interest rates

The current gearing is low, with net debt-to-equity ratio at about 20%. In additional the only bank loan that Netlink trust has is fully hedged via a floating to fixed rate swap:

The Trust Group currently has a S$510 million bank loan outstanding and has entered into a series of pay-fixed-receive-floating interest rate swaps to convert the variable interest rates on its bank loan into fixed interest rates, for a total notional principal amount of S$510 million over the period of the bank loan. Accordingly, 100% of the interest in respect of the outstanding amounts under the Trust Group’s existing bank loan has been hedged. The all-in blended fixed interest rate is 2.91% per annum.

Even if interest rates go up, the cost of borrowing for the trust will not go up. Of course, rising interest rates may result in a rerating in share price as investors demand a greater yield, but that’s always something that’s beyond our control.

Conflict of interest

Netlink Trust is structured such that its trustee-manager is basically owned by unitholders. By contrast, under a REIT structure, the manager is typically 100% owned by its Sponsor, which in this case would be Singtel.

This means that while Singtel owns 24.99% of Netlink Trust, they technically do not have 100% control of the trustee-manager. Personally though, I’m not too fussed either way. Singtel is a major regional telco player, so I trust that they will do what is in the interest of shareholders. A 24.99% stake is not to be trifled with, and I see Singtel’s economic interest being aligned with unitholders.

Closing Thoughts

I took advantage of the recent dip in prices ex-dividend to open a position in Netlink Trust. It’s been a counter that I’ve wanted to buy ever since its IPO days, but have always been waiting for a better entry point. It’s definitely possible that prices may drop further, but at current prices, it’s already a 5.95% forward yield which is good enough for me.

Netlink Trust operates in a highly regulated industry, with high barriers of entry in what is a natural monopoly, providing a service that is a necessity. It also operates in Singapore, one of the best run countries in the world where political and regulatory risk is somewhat limited. This gives it unique bond like qualities, and can be great diversification for any portfolio. In a financial crisis, REITs may face negative rental reversions, but given the highly regulated nature of Netlink trust’s cash flow, I expect them to remain resilient.

However, don’t buy into this counter expecting to see double digit capital gains or growth. It’s probably going to be a boring stock to many, but to me, boring dividend stocks are the most exciting. As long as the share price doesn’t drop, I’m already ahead by 5.95% a year.

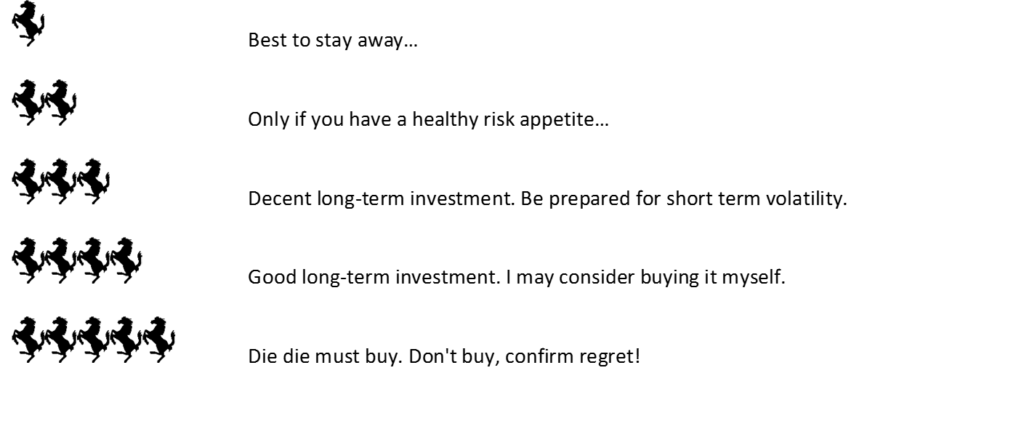

I really like this one, as evidenced by my own purchase. I will give it a 4 Financial Horse rating.

Netlink Trust – Financial Horse Rating

Rating Scale

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Thanks for this article, this one looks very safe. Like a utility company, but with less debt and almost a monopoly.

Cheers, I am glad you found this useful. The cash flow looks very stable, but the price action may still be volatile given the market perception over yield stocks. I view dips as an opportunity to add to my position.

Not a gd buy as ROE is 1 to 2percent due to huge goodwill on BS

Well, I guess only time will tell which of us is right. My only hope is that this does not turn into the next HPH Trust 😀

This is a business trust though and does not need to distribute a fixed percentage of earnings as dividends. Any comments?

Interesting question. Netlink Trust’s distribution policy is:

“NLT’s distribution policy is to distribute at least 90% of its Distributable Income to the Trust.

The Trust’s distribution policy is to distribute 100% of its CAFD.”

Given that Singtel is such a large unitholder, I am inclined to believe them. As you pointed out though, technically there is no requirement for them to distribute a fixed percentage of earnings. However, the same can be said for any company or REIT, since it is always open to the board/manager to vary the dividend/distribution policy.

Thank you for the analysis. I also think it is a safe stock. However, when I look at its PE ratio, it is 43. Why is it so high? it makes the counter look so expensive. Do you have any comments on this PE ratio?

PE Ratios are useless for REITs and BTs. A better metric would be the free cash flow. You can take a look at the articles here for more info:

https://www.fool.com/investing/general/2015/06/18/why-pe-ratios-are-useless-when-evaluating-a-reit.aspx

https://www.investopedia.com/investing/how-to-assess-real-estate-investment-trust-reit/

Hey, I looked up the dividend that they paid out its 3.24 cents. That translates to 4% at the IPO price of 0.81. Does that mean that they did not lived up to the projected yield of 5.95%?

The first distribution was for an 8 or 9 month period, because they IPOed in the middle of the financial year. If you take that DPU and annualise it, it will work out to very close to their projected yield.

Hi,

Tho this seems like a safe stock, but there’s not much growth so far. How would u view this business trust for Long term holdings for 10 years ++. What I’m afraid is if it turns to be another Hyflux.

What are the precautions you would to prevent such a loss in events of such case repeating itself?

Hence, I am only considering holding for short positions for the dividends(until there’s enough days & track record), say buying weeks before distribution dates and exiting afterwards. What would ur thoughts on this approach?

Hi!

Honestly, I think that’s going to be an incredible amount of effort, and you’re unlikely to outperform the market this way because most participants are already aware of this trick.

Personally I don’t think this is a next Hyflux for now, because the underlying business generates tons of cash flow (and is cash flow positive), at least for now.

Growth wise, once everything in Singapore is on fibre connections, it will be tied to Singapore’s population growth, which I believe will trend upwards in the longer term.

So yeah.. I’m actually pretty bullish on Netlink, and it’s one of my core holdings.

Hope this helps! 🙂

Hey thanks for ur insights. What do you think about the growth @current price & target price in the future? I may be buying some & hold for the long term.

I think the price is on the high side for now, I like it a lot more at low 80s. But if you look at the alternative investments like MCT/CMT, they’re all at sub 5% yields, which by contrast make these things look good.

I still think they’re a good long term investment though. But short term, this macro yield environment is incredibly hard to predict.

Hey, I was looking at Netlink’s financials for FY 2019, especially free cash flow and the distributions paid. Looks like the distributions for FY19 include a bank loan of 45 million! Is it normal that Netlink is borrowing cash to pay distributions?

The last I checked I remember the bank loan was used to fund capex. Perhaps I’ll try to do an update post on Netlink since it’s been a year.

Hey, any thoughts on why Netlink Trust borrowed 45 million in FY2019 to pay the distributions? This looks a bit shady to me as the distributions are not solely coming from free cashflow. I may be missing something here

I recall reading somewhere the borrowings was for capex incurred. The top line is growing really nicely though, well ahead of IPO projections.

Hi I’m looking to find a good brokerage firm. I’m a small time investor that doesn’t trade frequently. Will Standard Chartered be a good choice?

I actually think Saxo is the best choice because the minimum transaction fees are a lot lower, and the forex spreads are better for foreign stocks.

If you’re buying local stocks, go with DBS Vickers Cash Upfront for the CDP service.

Hi is netlink a good buy now for long term investment

Sure, it could be. Key is the price. 😉