Unless you’ve been living under a rock, you probably heard about the changes to HDB rules for the new “Prime Location” BTOs.

After last week’s article, I received a lot of questions on the potential impact of these changes:

Good job, FH!

As per your prediction, new HDB rules were indeed announced! ????

Now that MND has given its position on the upcoming Prime BTOs, do you think they will tackle the high property prices (both private and HDB resale) as well?

Now my initial reaction, is that the potential impact should not be underestimated.

If we look back at this moment 10 years from now, we could well see this as the turning point for Singapore property.

But first, let’s look at what exactly has been changed.

*Stocks MasterClass Launch Promo ends on Sunday, 31 October!*

Sign up now and get freebies worth $500:

- 3 Months Subscription to the Highest Tier of Patreon (worth S$200). Get full access to the FH Stock Watch, FH Portfolio, and Premium Exclusive Articles!

- Complete e-Book on How to Invest in REITs (as a Singapore Investor) (worth S$200).

- Complete e-Book on How to Invest in Private Real Estate in Singapore (worth S$100).

Our launch promo is always the best promo – so don’t miss it! Find out more here!

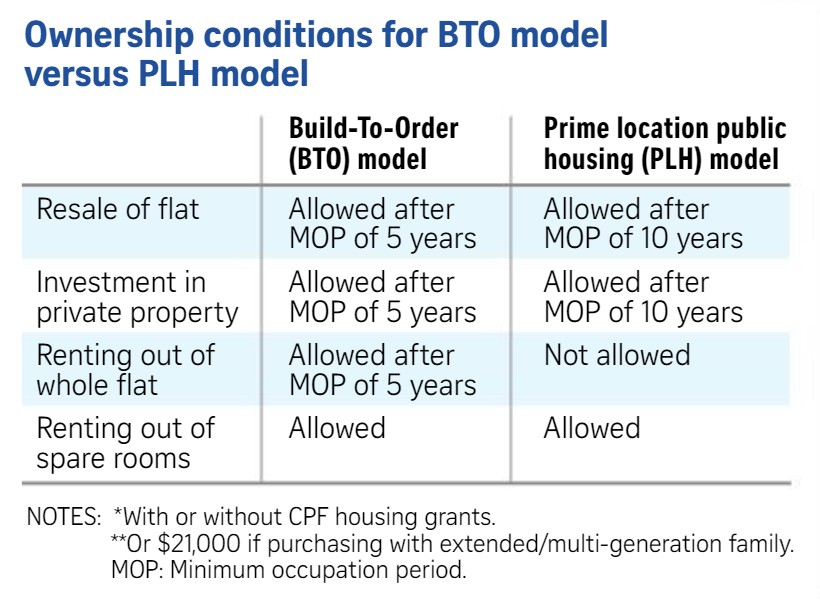

New HDB Rules Explained – Prime Location Public Housing (PLH) Model

The main changes are:

- 10 year Minimum Occupation Period (MOP)

- Not allowed to rent out whole flat at all (even after MOP)

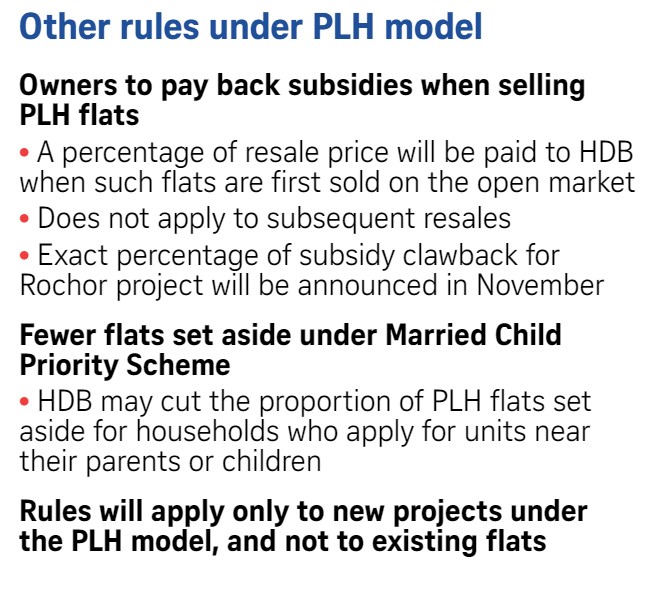

- The first time the BTO is sold, a percentage of the resale price to be paid back to HDB (even if sold after MOP – but only for the first resale)

*Do note that these rules will only apply to new BTOs going forward. If you already own a HDB at a prime location, you will not be affected.

On 3 – Huttons’ head of research Lee Sze Teck estimates the clawback will be 3% – 5% of the resale price. I have no clue how they arrived at this number though, so take it with a pinch of salt.

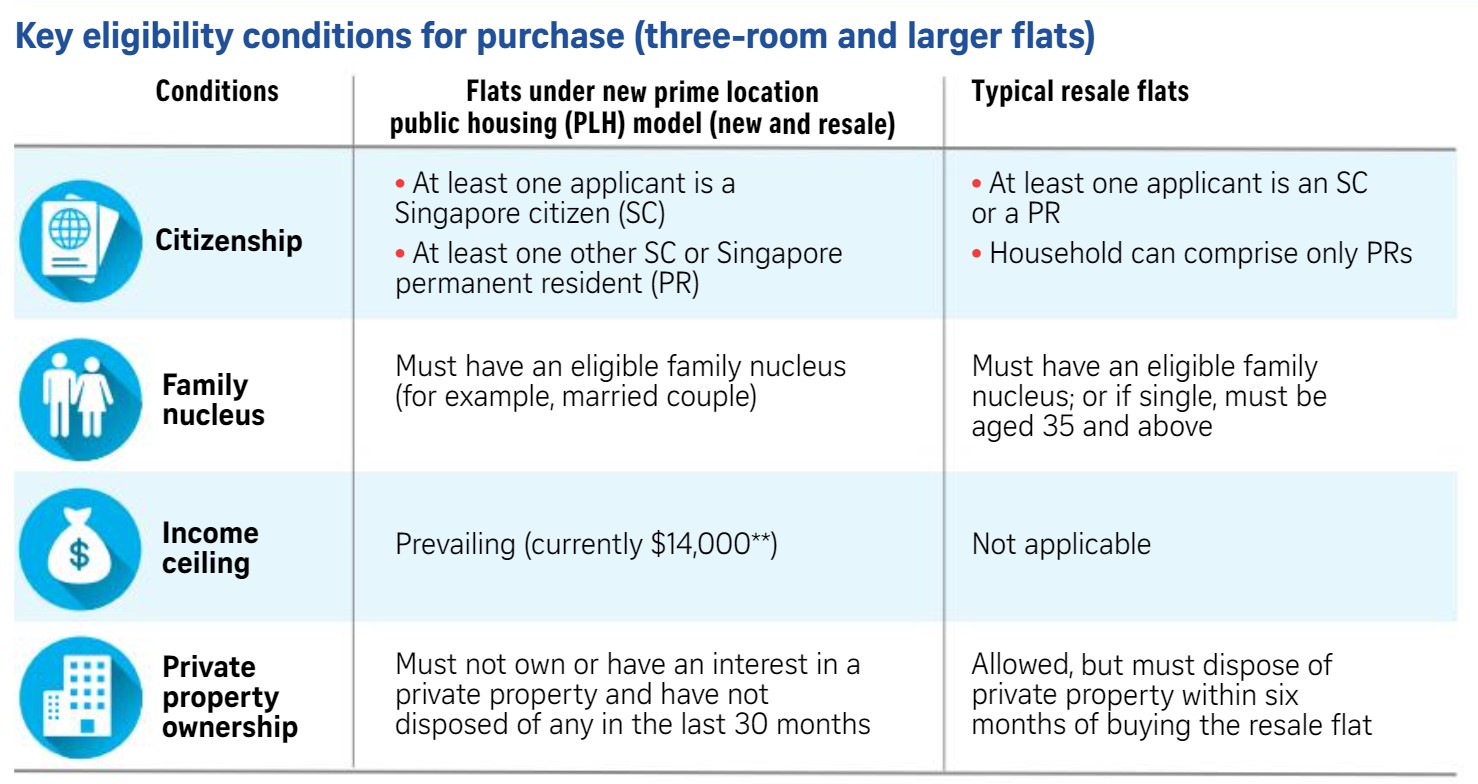

Prime Location Public Housing (PLH) Model – Changes to Eligibility Conditions

There are also new eligibility conditions you must meet before you can buy a Prime Location BTO.

These rules apply even if you are buying on the resale market:

- Must be 1 Singapore Citizen + 1 Singapore Citizen / PR

- Must be family nucleus (eg. married couple)

- $14,000 income ceiling for the household

- Must not own private property or sold within 30 months

Married Child Priority Scheme

Finally, there will be fewer flats set aside for the Married Child Priority Scheme.

Previously, the government set aside about 30% of the BTOs for people whose family members stay in the area.

The problem is that these are prime locations, so if your family owns a property in the area you’re likely to be well off anyway.

So it was felt that rules like these exacerbate inequality.

Fair enough, this was probably the least controversial change they made.

New Prime Location BTO Flats not attractive?

There are 3 big issues I see with these changes:

- What is the definition of “Prime Location”?

- How much can you sell this HDB for… 10 years later?

- What if you need to upgrade before 10 years?

What is the definition of “Prime Location”?

Okay, I get that Rochor and Greater Southern Waterfront (Pasir Panjang) are Prime Locations.

What about Bishan though?

Or Toa Payoh?

Or Queenstown?

Resale BTOs there are going for a million these days, so a good argument can be made that those are “Prime Locations” too.

Channel News Asia interviewed some analysts, and this was what they said:

In the meantime, he suggested putting in place a proper criteria and clear definition of prime areas to avoid “any contest of the new rules” in future.

“One thing is the definition of prime area and what qualifies it to be – for example, the closeness to the MRT station?”

I suspect that it’s too hard to define properly though.

The whole point of this policy is that it requires some flexibility to determine what are Prime Locations. It allows you to gauge public reaction to the new BTOs, and decide whether they should be expanded (or reduced) over time.

So it’s Rochor and Greater Southern Waterfront today, but the key question is whether this will eventually expand to other locations.

If so, this could suck out liquidity from the market, as:

- More buyers with a 10 year MOP will mean more people locked into their property for a longer time, and

- Less demand to upgrade to private property in the short term (from HDB upgraders)

How much can you sell this HDB for… 10 years later?

There was a great interview in the Straits Times (emphasis mine):

Among those who plan to apply for a unit in the upcoming Rochor build-to-order (BTO) project, the first site to come under the PLH model, is logistics manager Jacob Phua, 40.

He is more deterred by the pricing and waiting time for the flat than the various restrictions under the new model.

“The restrictions are not an issue to us because we plan to stay for the long term if we get a unit. Whether it’s five years or 10 years’ MOP, we’re unlikely to sell once we get used to the convenience of the location,” said Mr Phua, who has lived in Yishun all his life and hopes to move to a more central location with his wife.

“But looking at prices in previous BTO launches, I believe the Rochor prices may be more than $500,000, in which case, I may have to reconsider. There’s also the completion date to consider; I’m not that young to wait for more than five years for a flat,” he added.

The problem with these Prime Location BTOs, is that if you apply for one now, you only get it 5 or 6 years later.

If you’re a 30 year old couple, that means you get it at 35, and you can only sell it at 45!

That’s crazy.

And don’t forget that when you sell, you need to find a buyer who can meet the full set of requirements, and is fine to be bound by the 10 year MOP. And even after you find that buyer, you still need to pay a percentage back to HDB.

So chances are you’re not going to make much from the property.

This suggests to me that the ideal buyer is someone much younger. A 24 or 25 year old couple, who can get their house at 30, and upgrade at 40.

And who doesn’t plan on upgrading to a larger place or condo before 40.

What if you need to upgrade before 10 years?

What if you need to upgrade before 10 years – for legitimate reasons such as kids?

Fortunately, there seems to be a special exemption for these:

But experts also noted that this could cause inconvenience for buyers whose circumstances change over time, such as families who have children and decide they need more space. National Development Minister Desmond Lee said that appeals by those who genuinely face extenuating circumstances will be reviewed on a case-by-case basis.

Impact on Singapore property market – My Reactions

What is the broader impact on the Singapore property market?

3 big issues that jump out at me:

- Price of “normal” flats in the area will go up

- This doesn’t solve the short term structural demand supply imbalance for housing

- Are resale HDBs / Condos next?

Price of “normal” flats in the area will go up

Channel News Asia interviewed a bunch of analysts:

…they added that the tighter rules could have the unintended impact of driving demand for flats in nearby areas, which do not face the same rules.

“These kinds of older flats or previous launches are not affected by this – owners can still sell them in five years, sublet it out. Definitely for those looking for future rental returns or capital appreciation gains, they will probably look for these homes,” said Dr Lee Nai Jia, Deputy Director of the Institute of Real Estate and Urban Studies (IREUS) at the National University of Singapore.

“They will also know that in future, there will not be any such products in the market, especially in the city centre area. So I think definitely demand and pricing will see some spike,” said Dr Lee.

…

While ERA Realty’s head of research and consultancy, Nicholas Mak, agreed that demand would spill over to surrounding areas, he said prices are unlikely to go up significantly.

“The overall stock of HDB flats in that location will increase with the completion of the PLH flats. Based on economic theory, an increase in supply can moderate the rise in prices.

“Hence, any increase in the resale prices of the non-PLH flats will still depend on other major factors, such as the state of the economy, household income, market conditions and government intervention,” said Mr Mak.

Buyers may also possibly turn their attention to mature estates which are not in prime areas, said experts. But even then, any such impact may not be seen immediately.

…

I agree with this.

Because the new BTOs have so many restrictions, if you own a normal BTO with a 5 year MOP (or a condo), your property has suddenly become a lot more attractive overnight.

That said, I don’t think the impact will be significant in the short term.

We need to look at the bigger picture.

This doesn’t solve the short term structural demand supply imbalance for housing

And the bigger problem here – is that these changes do absolutely nothing to solve the short-term structural demand supply imbalance.

So you change the rules for a BTO that will complete 5 years from now.

But the just married couple with a kid on the way needs a house next year, not 5 years later.

Are resale HDBs / Condos next?

The natural conclusion here – which was suggested by the reader.

Are there more rule changes coming?

For resale HDBs and Condos?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

En Bloc Market starting to heat up

Just this week, a UOL Singland JV won the Watten Estate Enbloc at S$550.8 million, a 10.2% premium to the S$500 million minimum price.

In other words – the En Bloc market is starting to heat up again.

En Blocs are an important indicator to watch, because the en bloc market almost always starts the timer running on eventual cooling measures.

The fact that the deal was done at a 10% premium to the minimum price suggests that the en bloc market is going to heat up further.

Are more cooling measures coming?

Long story short, I agree that more measures may be coming.

These Prime Location HDB rule changes don’t solve structural demand supply imbalances. If anything, they may even drive up prices short term.

Which means that prices are going to trend up in 2022.

Which makes housing even more unaffordable.

Which disrupts the government’s goal of ensuring affordable housing for every Singaporean who needs one.

So I see these rule changes as just Phase 1.

It could be 6 months, or 12 months, but I do expect that at some point we will see new rules implemented.

What kind of cooling measures are possible?

The problem is that it is very tough to predict the timing, and the exact changes to be implemented.

But that’s the wrong question in my view.

Recognise the Narrative Switch

I talked about this last week, and the key to me is to recognise the narrative switch.

If you only take away one thing from this article, let it be this.

The prevailing narrative is now – Houses for living, not for speculation.

All the housing measures going forward, will be guided by this narrative.

So I don’t know exactly what measures will be implemented and when, but what I do know, is that:

- The government doesn’t want prices to go up too high, such that homebuyers are priced out of the market.

- At the same time, the government doesn’t want prices to crash, because a majority of our household wealth is in real estate, and a crash would destabilise the economy.

And really – that would be my base case going forward.

Low single digit per annum returns on property going forward. But all the 3% price rise a quarter needs to stop.

Will the property market crash?

That said, I wouldn’t necessarily expect a property crash as well.

The reason why property crashed in the past was because of excessive leverage in the system. People borrowed up 90% of the house value and bought 4 properties. When a recession came around, they lost their jobs, couldn’t rent out the houses, and had to fire sale.

Ever since ABSD came into play in 2011, leverage has been very tightly controlled.

At the same time, liquidity is abundant, and the rental market is very hot.

Few homeowners have the need to sell their house urgently.

They can just hold on, collect the rental, and ride out to the new cycle.

So if prices moderate, I suspect homeowners will just rent out the property instead. Hard to see a crash.

What about new homebuyers?

I know a lot of you are looking to buy a property in this market, and have written in with concerns about the price.

It’s a very tricky market to navigate, and I plan to share more views on this going forward.

I’ll be launching the How to buy a Property in Singapore series next week (hopefully on Thursday, Deepavali) – completely free of charge, and hopefully this would help u guys. My way of giving back to the community.

Stay tuned!

Closing Thoughts: Singapore Property worth Investing in?

After last week’s article debating whether Singapore property is still a good investment, a lot of you reached out to share your views.

Some of you think property is a poor investment, some think that prices can only go up.

I’m a bit more sanguine.

I absolutely agree that Singapore property today won’t see the same returns earlier generations saw.

The past 50 years was Singapore rising from backwater town to first world financial center. Remember when Singapore was known as an Asian Tiger?

No way that real estate prices will replicate that kind of returns going forward.

But I think that for those who can afford it, property still has a role in the average Singaporean’s portfolio.

With leverage, you can turn a 3% nominal return into a 6-7% return on capital. And Singapore real estate gives you important diversification benefits, instead of having 80% of your net worth in the stock market.

But I would love to hear what you think! Are more cooling measures coming? Is property still a good investment?

*Stocks MasterClass Launch Promo ends on Sunday, 31 October!*

Sign up now and get freebies worth $500:

- 3 Months Subscription to the Highest Tier of Patreon (worth S$200). Get full access to the FH Stock Watch, FH Portfolio, and Premium Exclusive Articles!

- Complete e-Book on How to Invest in REITs (as a Singapore Investor) (worth S$200).

- Complete e-Book on How to Invest in Private Real Estate in Singapore (worth S$100).

Our launch promo is always the best promo – so don’t miss it! Find out more here!

Government needs to get tough on HDB speculators. Impose a 50% capital gain tax. If they want more people to get married and have children to strengthen the Singaporean core instead of keep importing FT to increase the population. Thanks for non stop talks on HDB as an investment asset kind of stuff. When we bought resale, the price was already more than doubled after just the 5Y MOP. Then it’s up by another 75% now. Madness…to me. It makes no mathematical sense that the older a leasehold flat gets, the higher the price go. The young ones will suffer. Affordability needs to be properly manage. If we let market forces determine, then game over, especially for a small country. Maybe stay in Pulau Tekong or Sister Island for future generations. Lol.

Don’t worry, HDB market will not crash even if they impose tough measures. It may drop for short term only. Everyone needs a roof over their heads, a basic roof like a HDB flat.

Just my random thoughts, looking at the big picture, you don’t have to agree or publish it if you deem it unsuitable.

No problem at all, appreciate the sharing. I agree that housing affordability is becoming a real issue. From a big picture perspective, it looks like prices will continue to march higher short term, and at some point the government will have to step in for Resale/Condos.

This policy is designed to address the lottery effect of prime HDB flats like the Pinnacles and to ensure Singaporeans from all walks of life can afford a HDB flat at a prime location. That is a good policy as long as buyers are sure they are buying it strictly to live in it. This policy should not be confused with issues like addressing the current shortage of supply to meet demand or with wealth distribution.

Agree with this. I just cant help but look at the bigger picture and feel that more moves will be required.

It’s like watching the Feds taper QE – bond market has already priced in rate hikes next year and a rate cut after that. Looks the same to me here. Govt is not doing enough to ensure housing affordability, which means they will need to overintervene down the road, which will cause prices to overcorrect.

Agree. The style is reactive instead of proactive. If it has “overcorrect” later, let it be. I don’t even know how much my HDB is worth until agents ask want to sell? Lol. I think the majority of Singaporeans are using the HDB for own stay. Those who want to speculate should be kept out of the public housing market. The invented complicated rebate and grants can solve the affordability issue later when the bubble cannot sustain anymore? Lol.

This is a good way of thinking about it:

https://youtu.be/Uwl3-jBNEd4

By this measure buying in Singapore is a worse decision than renting.

Interesting, thanks for the share!

Do you foresee increased demand and ironically higher prices for existing prime HDBs like Pinnacle @ Duxton since it’s really the only viable alternative now for people looking to live in a HDB in a prime area?

Yes personally I would. Which is why I would expect some further measures down the road to ensure resale prices dont get too unaffordable.

Just hours ago, STimes reported that a Bishan 5-room went for a record $1.36mil.. just 72hours after it was put up on sale.

I also read elsewhere that there were already 159 million-dollar HDB resale flat transactions in just 9 months this year (another record).

With such eyebrow-raising reports, one can’t help but wonder whatever happened to the tenet of HDB flats being affordable forms of public housing?

While there may be some eventual positive outcomes of the newly-announced PLH BTO rules, young couples today may not have the luxury of time to wait till then.

To them, such announcements (while well-intended) are of scant consolation if the reality for them today is still the choice between getting lucky with BTO chances (with potentially stiffer competition increasingly) or just go with the flow and succumb to the high asking prices of resale flats.

It is a vicious cycle: More people gets priced out of resale market -> more turn to BTO balloting -> further increases the already-oversubscribed BTO competition -> more people fail in their BTO ballots -> opportunistic existing flat owners continue to demand high prices.

It is disheartening for young couples to be put through such unpalatable choices through no fault of their own when all they want is a place to set up their home and not be confronted with high COV/high mortgage burden.

Granted, it is also not easy for the authorities to crash property prices overnight as this may lead to even more backlash from existing HDB owners. But there may potentially also be political ramifications for helpless young couples if the current housing situation is left unchecked as it is.

Before the situation gets further out of hand, let’s all hope that some sensible and socially equitable announcements may come sooner rather than later. The narrative switch as you described certainly brings about some positive hope.

PS: Do feel free to not publish this comment if this comes across as too much of a rant and you deem it unsuitable.

Not at all, appreciate the sharing.

I agree with you on this, and personally I would expect to see some kind of measures coming in down the road to tackle high housing prices. The narrative switch always happens first, then policy, then finally price.