You guys know the drill by now.

The next T-Bills auction is on 22 June 2023.

Cash applications should go in 1 day before the deadline (21 June), and CPF-OA applications should go in 2 days before (20 June).

I myself have a bunch of cash that came in this week from December’s maturing T-Bills, so I am looking to roll them over.

3 big questions I wanted to discuss today:

- What is the estimated yield on the next T-Bills auction?

- Are T-Bills a good buy vs Money Market Funds, Fixed Deposits and Singapore Savings Bonds?

- What will I be buying – T-Bills vs Money Market Funds vs Fixed Deposits?

What is the estimated yield on the next T-Bills auction on 22 June – BS23113V?

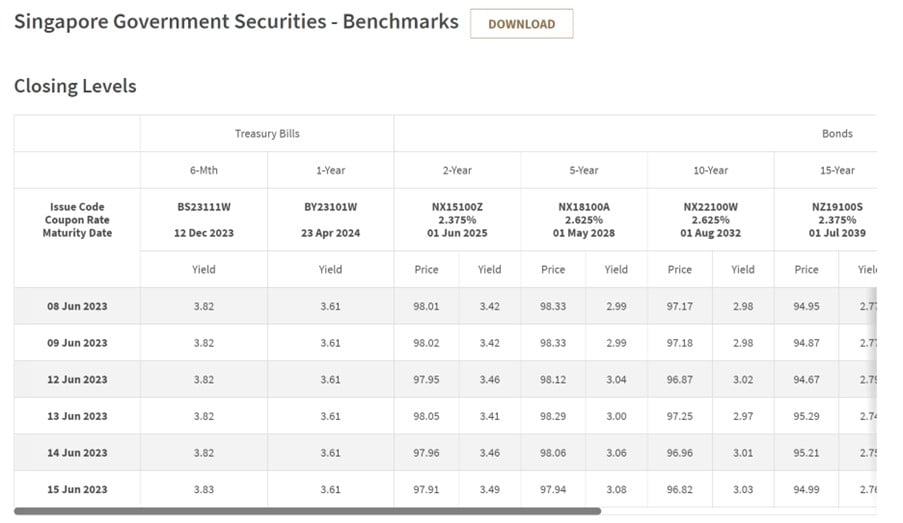

6 month T-Bills trade at 3.83%

First off – the 6 month T-Bills trade at 3.83% on the open market.

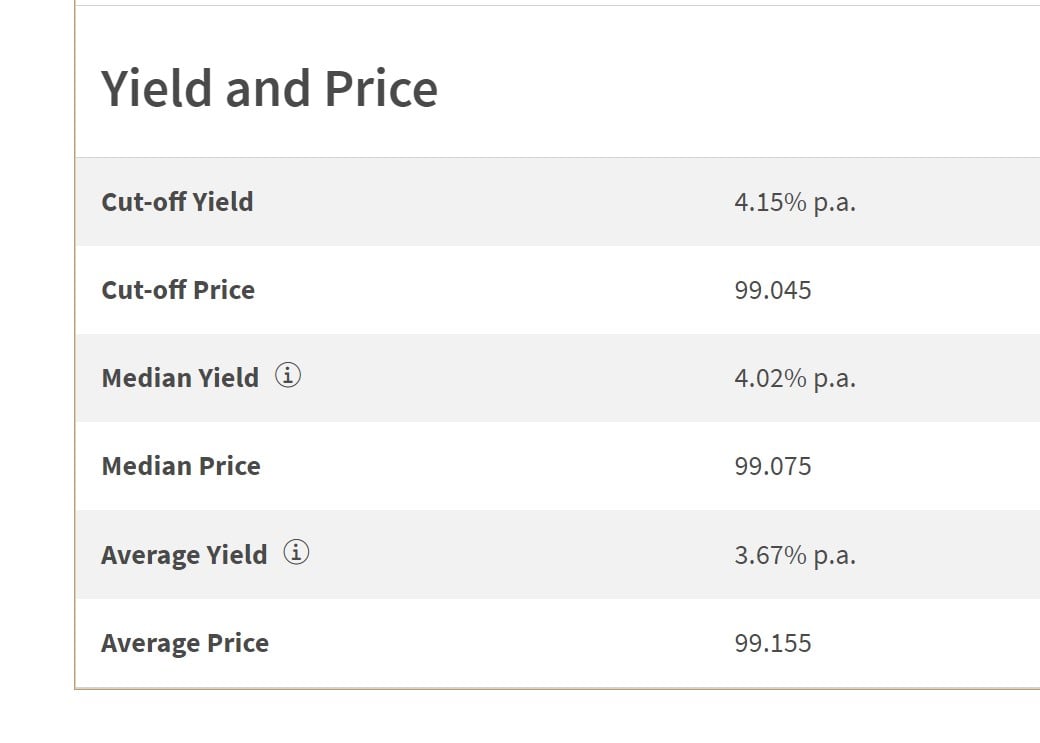

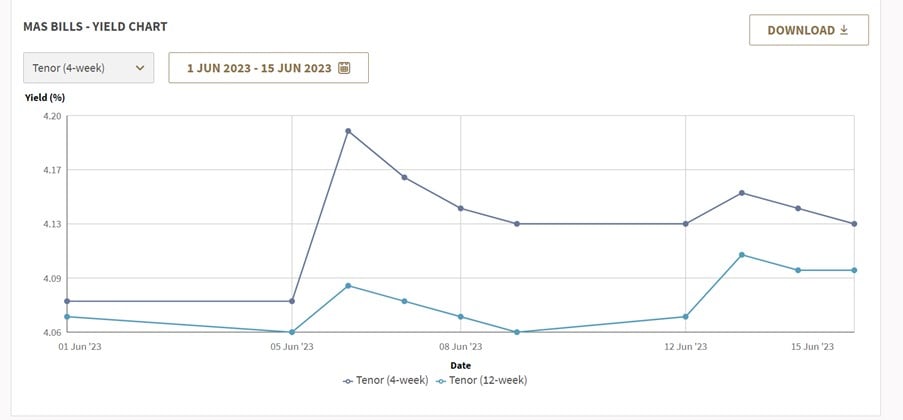

12 Week MAS Bills closed at 4.15% (vs 4.21% for previous auction)

The most recent auction for the 12 week MAS Bills closed at 4.15%.

This is a slight drop from the previous auction (4.21%) – and does indicate a small downtrend in yields.

Here’s the trading price in MAS Bills.

You can see the trend over the past few weeks which is down from early June peak, when market was pricing in the June hike.

12 week bills are trading at 4.10%, which interestingly is below the 4 week bills (4.13%).

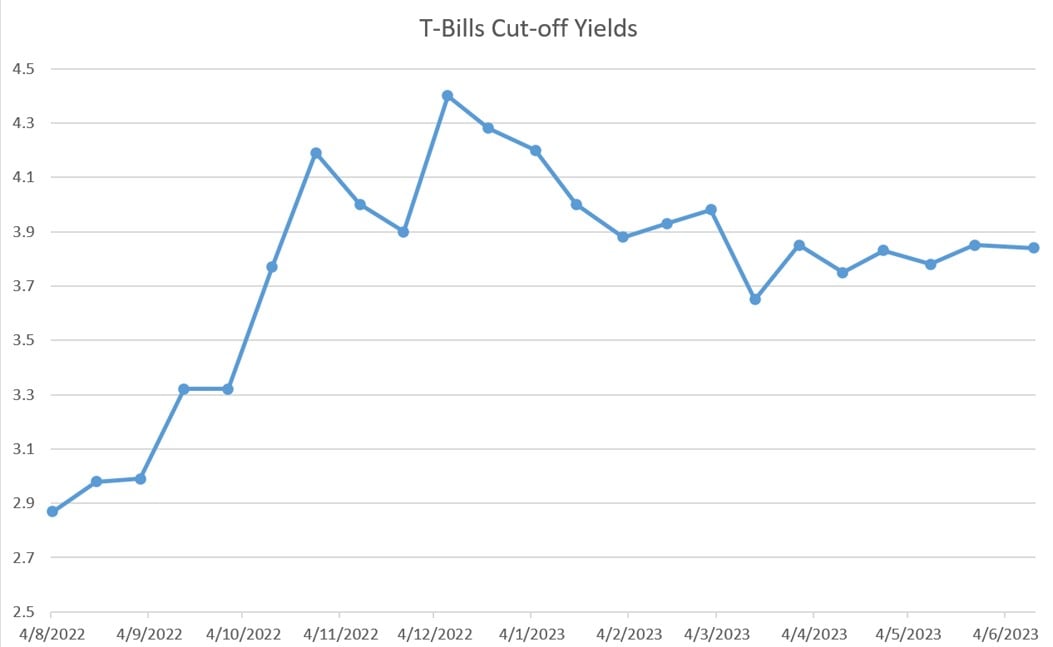

Most Recent T-Bills Auction closed at 3.84% yields

The most recent 6 months T-Bills Auction closed at 3.84%.

You can see this charted below.

Yields are firmly down from the late 2022 highs, but have settled into a 3.8 – 3.9% range since March.

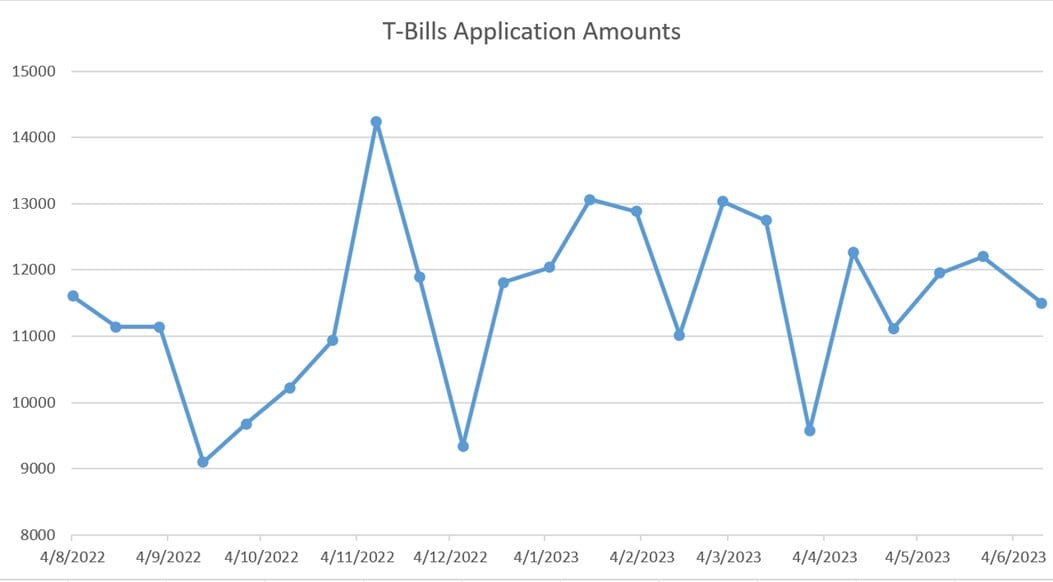

T-Bills application amounts is a wildcard

T-Bills demand usually tends to be a wildcard.

However if you look at the most recent T-Bills auction, application amounts actually fell quite a bit from $12.2 billion to $11.5 billion.

That’s almost a 5% drop and is quite meaningful.

Why exactly T-Bills demand is dropping is unclear, perhaps most investors who already want T-Bills have already gotten their allotment filled.

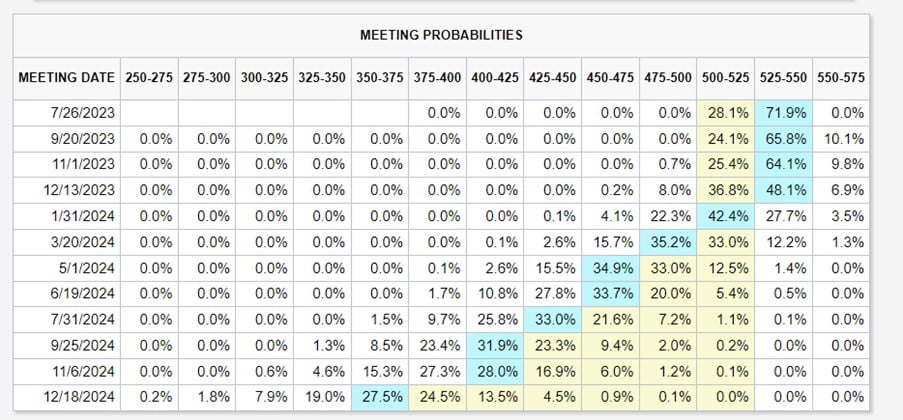

Will T-Bills yields go higher based on the Fed’s call for 2 more rate hikes?

I’ve been getting some questions on whether T-Bills yields will go higher because the Feds have called for 2 more rate hikes in 2023.

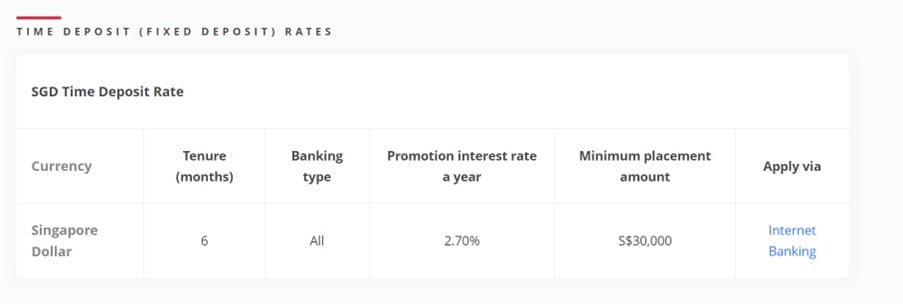

Well, you know where the banks stand on this – because OCBC just slashed their 6 month fixed deposit rates down from 3.0% to 2.7%:

This is what is priced into the US futures curve today.

71% chance of 1 more rate hike.

But the market sees only a 10% chance of a second rate hike from here.

But the market has finally agreed with what I’ve been saying all year – no rate cuts in 2023.

Personal view though – if you look at the SGD yields and MAS bills they barely even reacted post FOMC.

So I doubt you’ll see the T-Bills yields change materially from this.

Next T-Bills Auction – Estimated yields of 3.80% – 3.90%?

In any case, putting everything together.

I think we’ll probably see an estimated range of 3.80% – 3.90% for the next 6 month T-Bills auction.

As always, I encourage investors to submit a competitive bid to avoid any freak results in case yields plunge.

For those doing competitive bidding though, you generally want to make the bid as close to the cut off date as possible.

This gives you time to watch how the market and interest rates play out, which allows you to adjust your bid accordingly.

Better Buy – Fixed Deposits vs T-Bills?

Bank fixed deposit rates are pretty dismal these days.

OCBC has just slashed it further from 3.0% down to 2.70%.

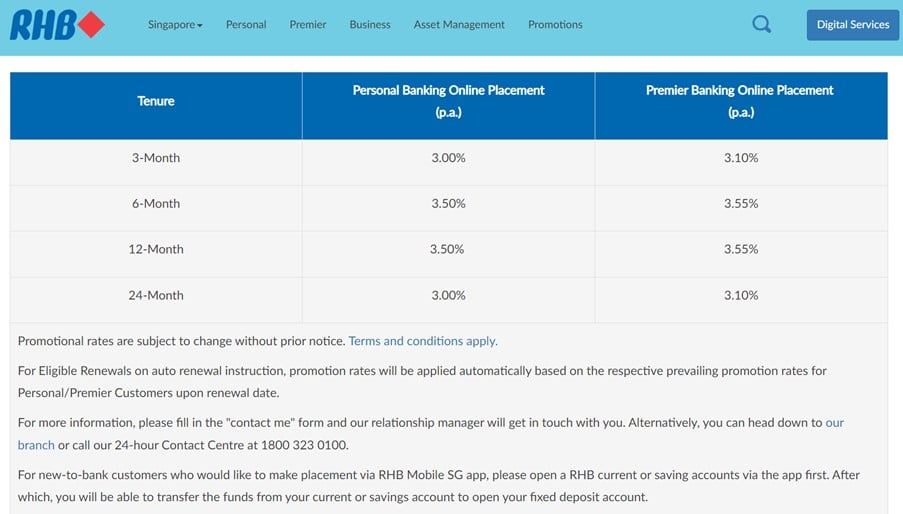

The best fixed deposit I could find was RHB Bank.

Offering 3.50% for a 6 or 12 month Fixed Deposit, going up to 3.55% if you’re premier banking.

Given where I expect T-Bills yields to come in for the next auction, I don’t think it’s much of a competition really.

I would be buying T-Bills over Fixed Deposit here unless something changes materially.

What about Money Market Funds? Fullerton SGD Cash Fund pays a 3.88% yield on cash – Better buy than T-Bills or Fixed Deposit?

A lot of you have been asking about Money Market Funds vs T-Bills.

I wrote a full article on that yesterday, so do check it out for the full details.

Long story short though – as of today, I still prefer T-Bills over money market funds.

With yields of 3.84%, T-Bills have very competitive yields vs money market funds.

Given how things are playing out, I do think there is a risk that bank fixed deposit rates may be cut further in the months ahead (affecting money market fund yields).

So I like the ability to lock in 3.84% for a 6 months period.

T-Bills are also risk free.

No doubt the risk on money market funds like Fullerton SGD Cash Fund is very low, but when I can get risk free at 3.84% why do I need to bother with low risk?

I don’t deny the lack of liquidity (from T-Bills) is a problem.

Because of that I do need to maintain some cash in high yield savings accounts and Singapore Savings Bonds for me – to provide a healthy pool of cash I can draw on if I need urgent funds.

But for the right kind of investor, I think money market funds like Fullerton SGD Cash Fund can have a real place in your portfolio.

The risk is low, and you’re getting very competitive yields with fixed deposits, and you have T+1 liquidity.

Will I buy Fullerton SGD Cash Fund vs T-Bills or Fixed Deposits?

That being said I do have some funds parked in money market funds like Fullerton SGD Cash Fund.

But this is primarily spare cash that I hold in Moomoo or Tiger Brokers or Webull, that I have not invested in markets yet.

I see this as the primary use of money market funds like Fullerton SGD Cash Fund – as a place to park short term cash, until they can be deployed for other purposes.

The bulk of my cash is still held via a mix of:

- High yield savings accounts – like UOB One or UOB Stash Account

- T-Bills

- Singapore Savings Bonds

- Fixed Deposit

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Money Market Funds can be used to achieve a higher yield if you are comfortable with more risk

There are a whole bunch of other options like EndowUs Cash Smart which mixes and matches money market funds to achieve higher yields (by taking on a longer duration and higher risk).

Generally speaking though, the analysis above holds true.

There’s really no free lunch in this world.

It is up to each investor to decide the right balance between yield, risk, duration and liquidity.

Money Market Funds do offer much better liquidity, but that can come at the cost of yield and risk.

Better Buy – Singapore Savings Bonds vs T-Bills

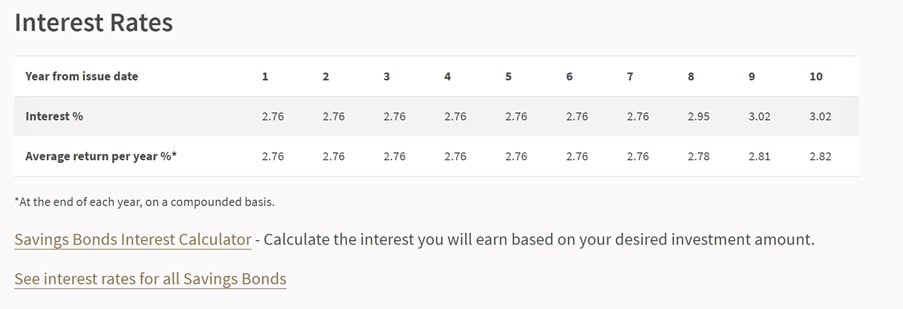

Latest Singapore Savings Bonds interest rates are below.

You’re looking at 2.76% for the first year, stepping up to 2.82% over 10 years.

Like I said, not super attractive, unless you want to lock in interest rates for up to 10 years.

For short term interest rates, T-Bills are probably your best bet for now.

I am putting money where my mouth is – I am buying the T-Bills

As shared above, I do have a bunch of cash that came in this week from maturing T-Bills.

And I am putting money where my mouth is.

I will be applying for the 22 June 2023 Auction 6 month T-Bills.

I think in today’s market, T-Bills are the most attractive place to park cash, as long as you don’t need the immediate liquidity.

If you do need the liquidity though, then you can consider either the money market funds or Fixed Deposits.

This article was written on 16 June 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 500 worth of fractional shares (expires 30 June)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund $100 SGD

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.