In my article last week on the Top 5 High Yielding REITs to buy right now, I listed Prime REIT as one of the better high yielding REITs to buy. Having had the chance to go through the prospectus, I kinda still agree with my original assessment.

Let’s take a closer look.

Basics

Prime REIT has been covered quite extensively by some of the other bloggers out there (see here and here), so you can check those articles out for a brief introduction.

Very simply, Prime REIT is a US Office REIT. The closest equivalent REIT in Singapore will be Manulife REIT.

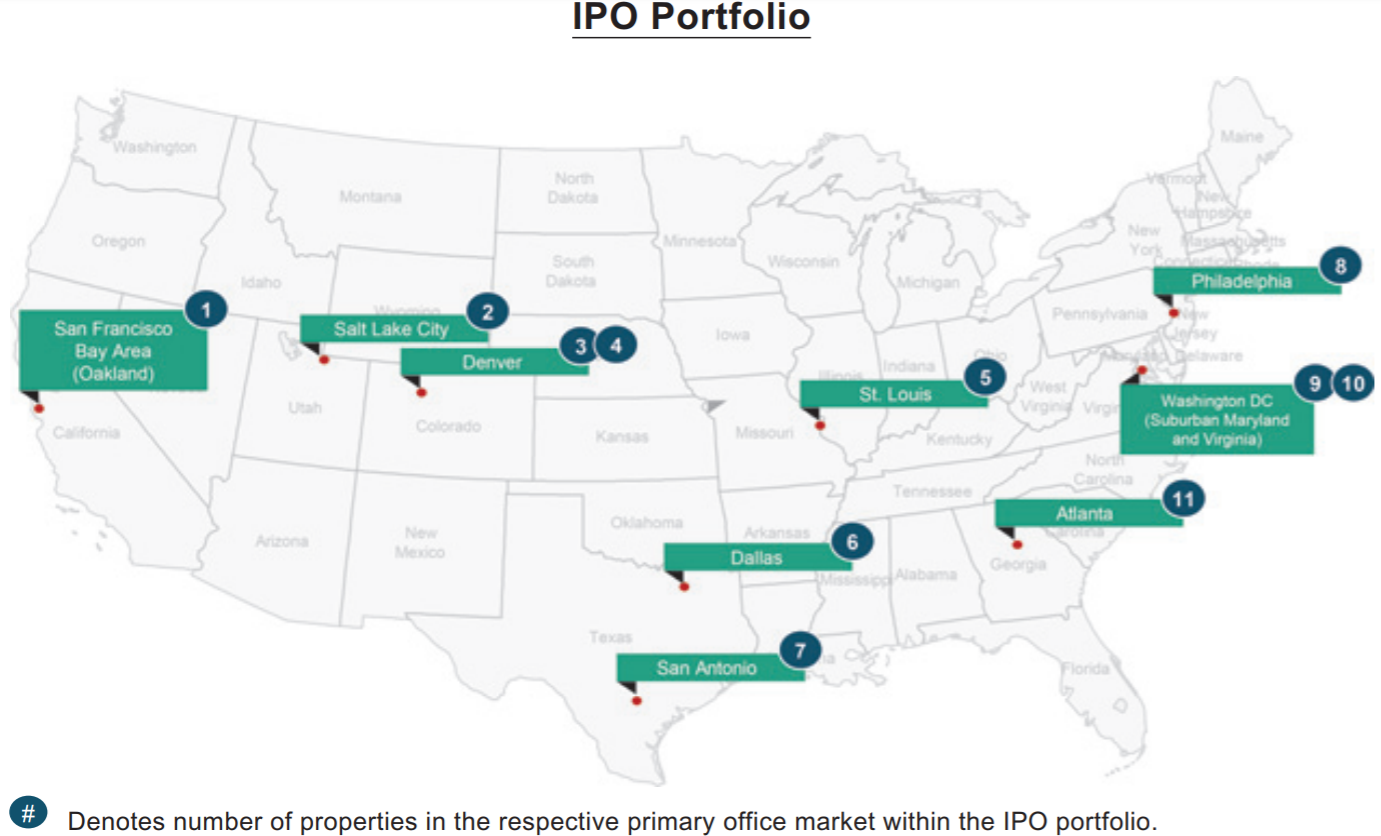

Prime REIT holds 11 assets across US, with a total asset valuation at IPO of 1.2 billion USD. I’ve set out the location of the assets below, and it’s pretty well diversified.

Sponsor

The sponsor of Prime REIT is KBS US, the same guys behind Keppel KBS US REIT.

It’s a small REIT, with around a S$1.1 billion market capitalisation based on the IPO price. With small REITs like this, the only way to drive future growth is by doing equity fund raisings (because the amount of debt they can borrow is limited).

The last time Keppel KBS US REIT did a big equity offering, it absolutely tanked their unit price, so let’s hope the sponsor has learnt their lesson from that one. But the fact remains that because the sponsor is so aggressive about growth, if you buy into this REIT you should probably expect to have to cough up cash down the road for more equity offerings when they do an acquisition.

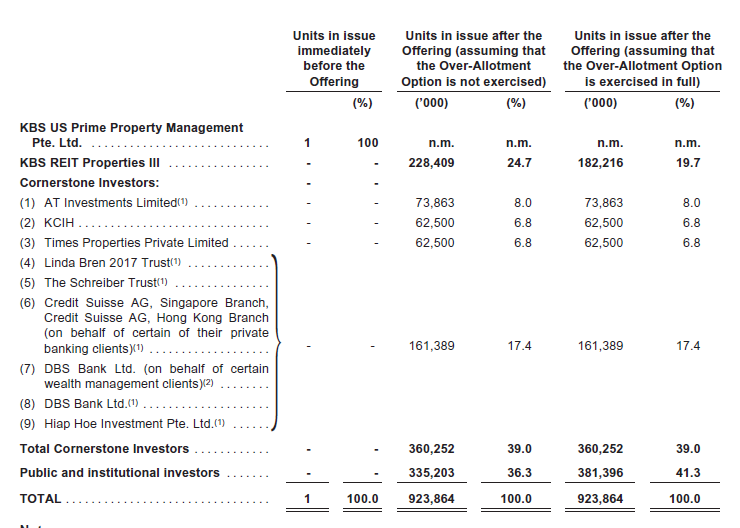

As with most US REITs, no single unitholder can hold more than 10% of the REIT to affect their tax transparency status. KBS US managed to get an exemption on the basis that no more than 5 unitholders hold more than 50% of the REIT, which is why the sponsor is able to hold about 24% of the REIT post listing.

I really like this touch – I always like it when the sponsor is prepared to put money where their mouth is and take up a bigger stake in the REIT.

Asset

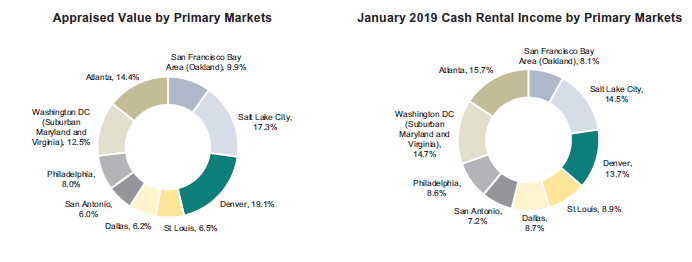

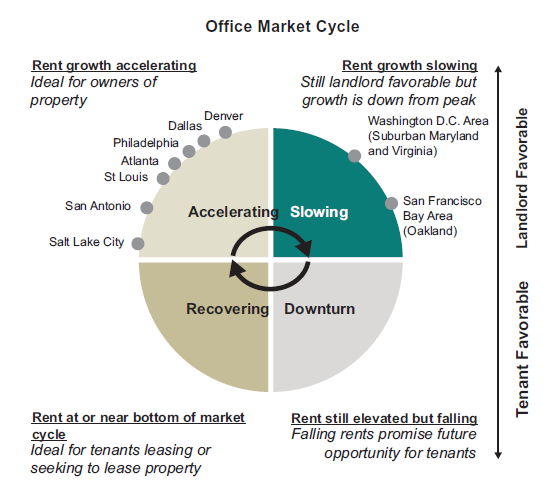

Prime REIT holds US Office assets, and is generally quite well diversified across markets.

I really like this chart that shows you which stage the sponsor thinks the property cycle is at for each of the cities that Prime REIT is in. Of course, things like that should be taken with a pinch of salt, because with all the recent PMI data this bad, the key question is going to be whether the Fed’s insurance rate hikes will be sufficient to counteract the slowing economy. If it doesn’t, the most of the property cycle is just going to accelerate into downturn stage until the economy picks up.

Yield

The forecast yield is 7.4% for FY2019, and 7.6% for FY2020.

Another thing that is great about office assets, is that they are always locked in for long term leases. Unlike hospitality REITs where customers basically stay for a couple of nights (creating hugely cyclical revenue streams in a downturn), office REITs usually sign long term 3 to 5 year leases. This gives the REIT a lot of clarity upfront as to the future cashflow from rentals, because the leases are already locked in, and the tenant is bound to such rates unless there is a big downturn resulting in a default or tenants negotiating lower rates.

Long story short, when they forecast a 7.6% yield for FY2020, it’s probably going to be somewhat true, unless the economy gets really bad.

The other good thing about Prime REIT is that their current leases are at below market rents, so there could potentially be some upside when it’s time to renew leases. Of course, whether they can actually lock in the higher rents will depend on how strong the property market is at the time. It’s no different from renting out your own property really, just on a larger scale.

Price/Book

At IPO price of US$.88, that works out to a 1.05 Price/Book ratio. Manulife REIT is trading at a 1.09 P/B, 6.7% yield, so Prime REIT’s 1.05 P/B and 7.4% yield does look comparatively better, especially when you factor in the potential upside in rental reversions.

For reference, Keppel KBS US REIT is at 1.0 P/B, 7.74% yield, but those are more business park style of assets, so it’s fair that they trade at a risk premium to offices.

It’s always hard to comment with this things, but my gut feel is that Prime REIT is actually quite fairly priced.

IPO Tranche size

As you would expect, after the disastrous Eagle Hospitality Trust IPO, they’ve been a lot more careful about Prime REIT.

The size of the public tranche here is S$20.1 million, significantly lower than ARA US Hospitality Trust’s S$50.8 million and Eagle Hospitality Trust’s S$35.0.

ARA US Hospitality Trust |

Eagle Hospitality Trust |

Prime REIT |

|

| Public Tranche | $50.8 million | $35.0 | $20.1 |

| Public Tranche Subscription Rate | 1.1 | 0.4 | ? |

| IPO day price performance | 0% | -6.4% | ? |

| IPO day trading volume | 9.6 million units | 15.3 million units | ? |

| Stabilising Action on IPO Day (bought back by underwriters) | 6.3 million units | 7.99 million units | ? |

| Amount of stabilising action (as % of IPO day trading volume) | 65% | 52% | ? |

Do I like this REIT?

To be honest, I quite like this REIT. I think it’s a very decent REIT. If I had zero exposure to REITs as an asset class right now I probably would buy some.

Unfortunately though, I already have big exposure to REITs. My current stock portfolio (available here) is about 40% weighted to REIT (this has gone up significantly due to the runup in REIT prices). So on that basis, I wouldn’t buy more REITs unless they’re absolutely fantastic buys, because I don’t want to be overweight to REITs at this stage in the cycle.

And Prime REIT at this price, really isn’t a fantastic buy. It’s a decent buy, and a very decent buy at that, but I just don’t see it as a must-buy for me. But of course, that’s unique to my personal situation, so please don’t copy what I’m doing as your personal situation could be different.

Macro Outlook

Given where we are in the market cycle, it’s probably wise to talk a bit about the broader macro outlook. The analogy I like to use is that stock picking is like picking the right boat, while the macro outlook is like the weather. Even if you get the stock pick right (ie. Get the right boat), you’re still going to be in for a rough time when the storm comes (ie. Economic slowdown).

The outlook doesn’t look so great these days. Jerome Powell’s testimony the past week basically cemented the case for a July US rate cut. Because of the good job and inflation numbers, a 0.25% (25 bps) rate cut seems the most likely.

Based on historical precedence, each time the Fed embarks on an insurance rate cut, they typically cut about 75bps, which means 3 rate cuts in total, which coincidentally is exactly what the Fed Funds future market is predicting.

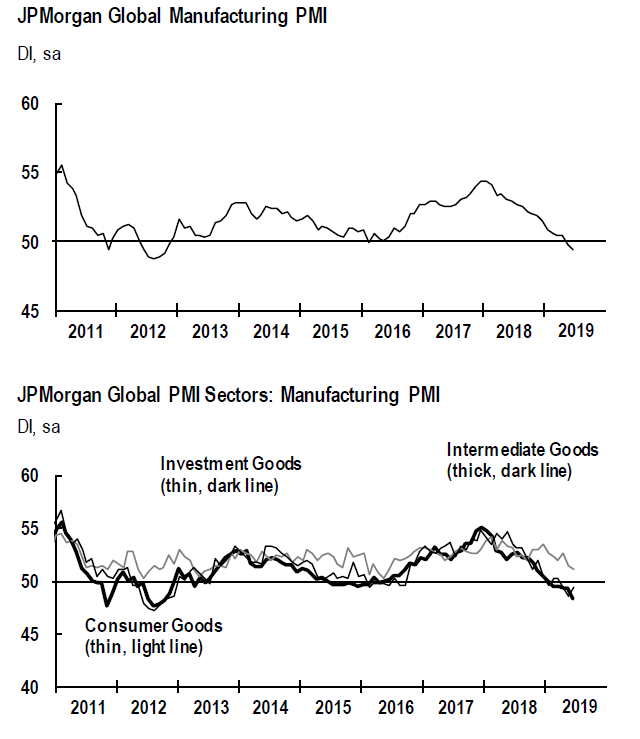

Recent global PMI data has been horrible as well. JP Morgan’s global PMI data (which is a blend of PMIs across 30 nations globally) is at it’s lowest since 2012. From the bank:

At 49.4 in June, the J.P.Morgan Global Manufacturing PMI™ – a composite index produced by J.P.Morgan and IHS Markit in association with ISM and IFPSM – fell to its lowest level for over six-and-a-half years and posted back-to-back sub-50.0 readings for the first time since the second half of 2012.

“The global manufacturing sector downshifted again at the end of the second quarter. The PMI surveys signalled that output stopped growing, as inflows of new business shrank at the fastest pace since September 2012. This impacted hiring and business optimism, with the latter at a series-record low. Conditions will need to stage a marked recovery if manufacturing is to revive later in the year.”

The past week, 2Q GDP data from Singapore also had a horrible print, coming out at a 0.1% growth.

One last interesting point that just popped up today is Anheuser Busch cancelling what was about to be the largest IPO or the year, citing poor investor demand. Moves like that don’t exactly inspire confidence in the global market.

So the key question here, is whether the Fed’s insurance rate hikes are going to be sufficient to offset the global manufacturing slowdown.

My gut feel, and don’t quote me on this, is that the answer will be a yes, but only in the short term.

I think over the next 1 to 2 quarters the rate cuts may be sufficient to support global asset prices.

But in the longer term, anything from 2020 onwards, I think there eventually comes a time when global central banks run out of tools to stimulate the global economy. Because if you do a 75 bps cut now and bring US rates to 1.75%, what happens in the next downturn? You need about 5% cuts on average to bring about the next cycle, but once you cut to 0% you’re basically stuck from a monetary policy angle.

So in a way, these rate cuts are merely delaying the inevitable downturn that will eventually need to come, and that downturn can probably only be addressed by fiscal policy from government (Modern Monetary Policy if you like).

What does this mean for the average investor? I see these movements as being short term bullish, but mid term bearish. In the immediate term, there may not be a recession due to central bank policy. But in the mid term (2020 out), all this does is deplete central bank ammunition for the next recession. There’s a recent piece by Ray Dalio that puts it way better than I can, so do check it out if you’re keen.

Closing Thoughts: How good is this REIT?

Again, I think Prime REIT is a perfectly decent REIT. Of the 3 US REITs (ARA US Hospitality Trust, Eagle Hospitality Trust, Prime REIT), I like Prime REIT the most because of its exposure to the US office sector, and the stability that comes with office assets.

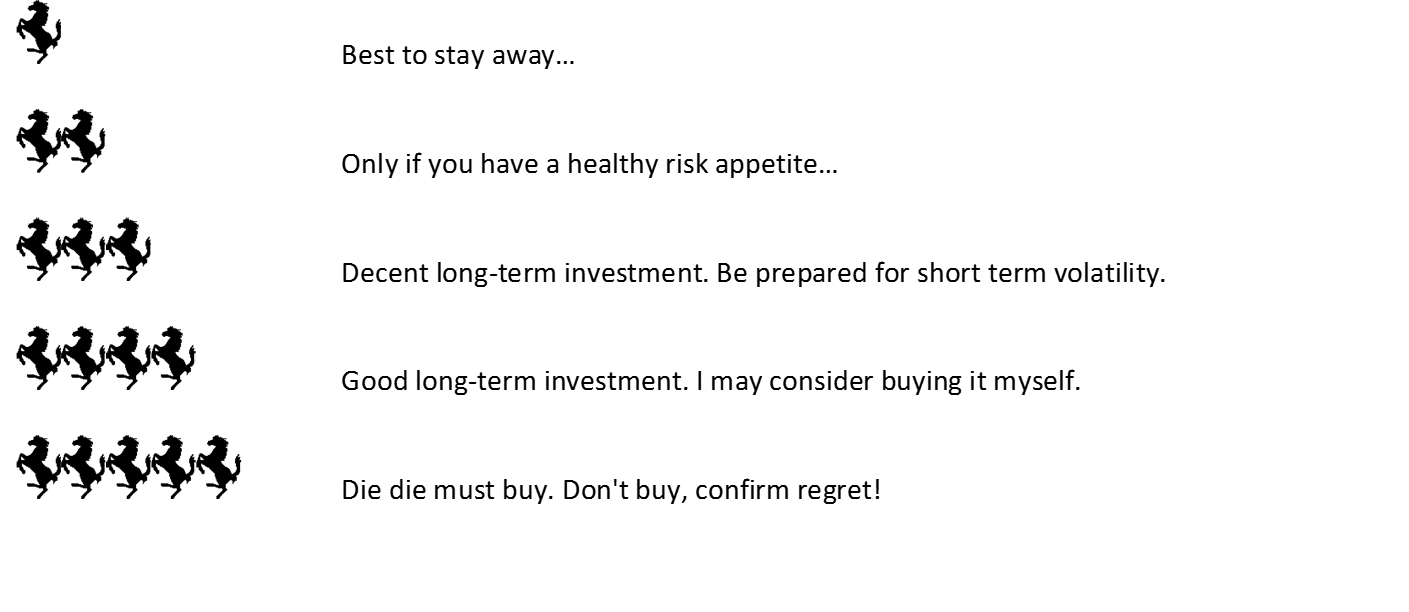

I also like the well diversified portfolio, the above market yields (compared to Manulife), and the potential for positive rental reversions. So I’m giving this a 3 Financial Horse rating.

Am I subscribing for this IPO? Probably not.

I personally don’t think this will flop as hard as Eagle Hospitality Trust because the public tranche is significantly smaller, these are office assets, and there is also the “Keppel” name behind this REIT.

But again, I don’t see the need to take a punt on this at IPO stage. REIT IPOs almost never “pop” on day one, so if I subscribe at IPO stage I’m taking the albeit small risk that it drops, without any real likelihood of price going up. That’s a pretty asymmetric risk to me. I would much rather wait to see the post-IPO price performance before deciding whether to buy. Of course, this strategy only works for small time retail investors, because if you’re a big boy the open market may not give you the liquidity you need to open a big position without moving the price.

So while I’m skipping this IPO, I’m probably also skipping this REIT unless price comes down post-IPO, because of where we are in the market cycle, and because I already have an outsized allocation to REITs.

But don’t get me wrong, these are mostly personal reasons. Objectively speaking, this is still a very decent REIT, and I would fully understand why investors out there subscribe for it. Which is why it gets a 3 Horse rating.

Are you subscribing for this IPO? Share your thoughts in the comments section below! I respond personally to all comments!

Prime REIT – Financial Horse Rating

Rating Scale

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

Hi FH,

U mentioned about US reit, unitholders are not suppose to hold more than 9.8% due to some tax issue.

Just curious, does this applies to custodians? I believe a bank who is a custodian might ends up holding more than 9.8%.

Would love to hear from you soon.

Yes, that is correct based on my understanding of the rule. 🙂

Hi FH,

Thanks for the analysis! Wondering if you have any thoughts on the exchange rate risk, since this is an issue unique to USD-priced equities. A small slip in the USD would completely wipe out any gains…

Cheers,

Jon Wai