Well – what a week.

The big question for 2023/2024 was how the policy makers (Feds and US Treasury) will react to a slowing economy when the time came.

In late October, Janet Yellen (US Treasury) showed us which side she was on by shifting debt issuance from long term debt to short term debt.

And this week, Powell in a stunning reversal from his prior hawkish self.

Effectively said they will prioritise the economy, and that they will cut interest rates even before inflation comes down to 2%.

If I didn’t know better, it would look like the US Treasury and Central Bank are coordinating efforts to juice the economy heading into 2024 Nov elections.

Taken together – this one-two combo is the clearest combination thus far on how policy makers are likely to react in 2024.

And it’s material enough that I started making changes to my portfolio this week, and will likely continue going forward.

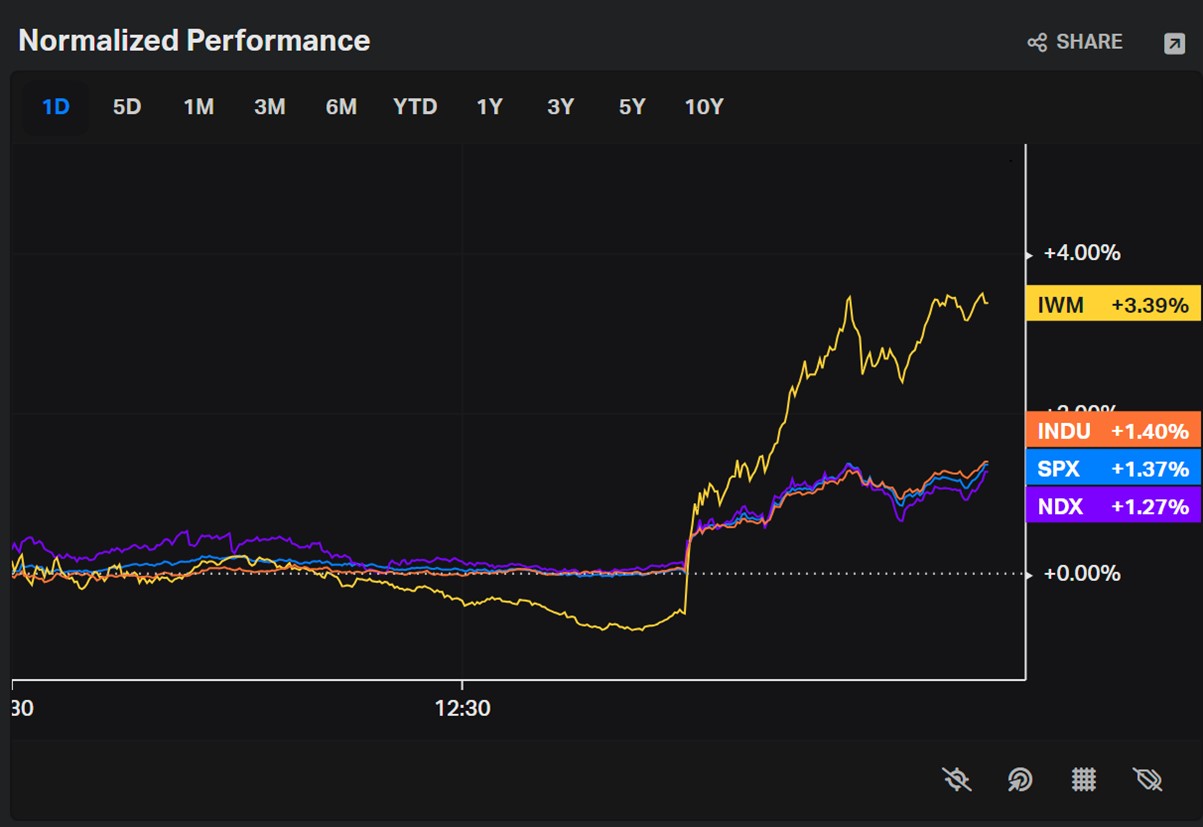

REIT prices jump 10% this week

As many of you would have seen – REIT prices rallied across the board this week.

Many blue chips like CICT, MPACT, Ascendas REIT jumped 5% on Thursday alone (the day after the Fed “Pivot”).

The fact that the blue chip REITs rallied more than the mid caps indicate that some of this was from institutional / index driven flows, which is indeed bullish.

If you look beneath the surface, you’ll notice that some of the smaller cap REITs jumped as much as 10%+ this week.

Here’s Keppel Pacific Oak REIT, up almost 80% from the November bottom.

This raises an interesting question.

Is this Fed “Pivot” the start of a new bull market for the REITs?

Or a dead cat bounce with heavily shorted REITs rallying?

To really understand this, we need to understand what exactly happened this week.

This was what I wrote for FH Premium subscribers on Thursday after the FOMC press conference.

It’s important enough that I extract the full article below, with minor edits:

FH Premium Article: The Fed “Pivot” is here – What happens next?

As many of you already know by now – Jerome Powell’s last night confirmed, in the clearest terms to date, that interest rate cuts are on the table in 2024.

This was Jerome Powell’s most dovish press conference since the start of the rate hike cycle, and has been interpreted by many as an effective Fed “Pivot”.

The biggest concern that we have been discussing for 2024 is how will the Feds will balance the inflation fight vs preventing a recession.

Hold rates too high too long, and you get a recession.

Cut rates quickly, and you avoid a recession, and the economy comes roaring back (potentially with inflation).

After last night’s meeting, the Feds have for the first time this cycle shifted from worrying about inflation, to worrying about reession.

This was music to the ears of the market, and sparked a huge rally across all asset classes.

A lot of you have asked for my thoughts on the FOMC, so I wanted to share some initial takeaways here.

I will split this article into 3 parts:

- What actually did the Feds say?

- What does this mean?

- What happens next?

What actually did the Feds say?

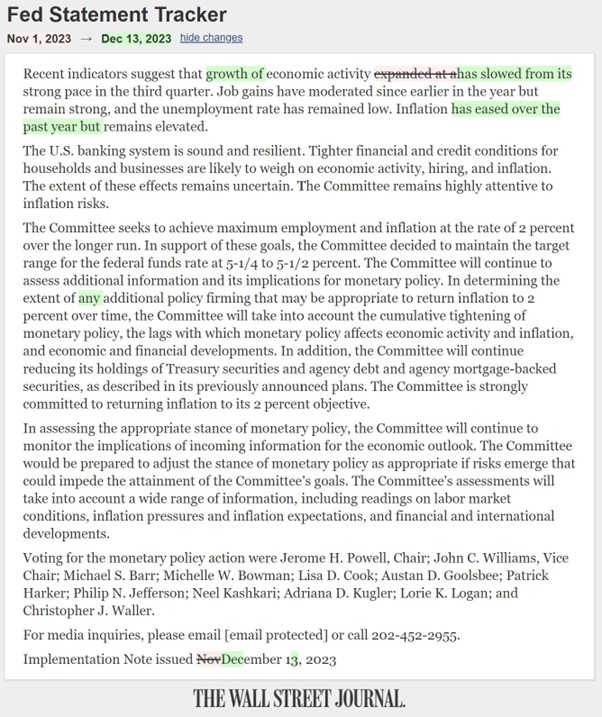

Let’s start out with the changes to the official Fed Statement.

The 3 big changes are:

- Acknowledgement that economic activity has slowed

- Acknowledgement that inflation has eased over the past year

- Addition of the word “any” in front of “additional policy firming” – suggesting that no further rate hikes are on the table

You can see the actual changes to the Fed Statement highlighted below.

But the big one is the press conference

Buy boy… the big changes were from Jerome Powell’s press conference.

I extracted the key answers I felt were material (yellow highlights), and my interpretation of what they mean:

FH Interpretation:

- Feds are done with rate hikes for this cycle

- Feds effectively confirmed 2024 rate cuts – question now is how many and how soon

Reference from Powell:

Q: Thank you. Chris Rugaber at Associated Press.

I wanted to ask, how should we interpret the addition of the word “any” before additional firming in the statement? I mean, does that mean that you’re pretty much done with rate hikes and the committee has shifted away from a tightening bias and toward a more neutral stance? Thank you.

POWELL: So specifically on “any,” we do say that in determining the extent of any additional policy firming that may be appropriate, so any additional policy firming, that sense. So we added the word “any” as an acknowledgement that we believe that we are likely at or near the peak rate for this cycle.

Participants didn’t write down additional hikes that we believe are likely, so that’s we wrote down. But participants also didn’t want to take the possibility of further hikes off the table. So that’s really what we were thinking.

…

POWELL: So the way—the way we’re looking at it is really this. When we—when we started out, right, we said the first question is how fast to move, and we moved very fast. The second question is, you know, really how high to raise the policy rate, and that’s really the question that we’re still on here. We’re very focused on that. As I—as I mentioned, people generally think that we’re at or near that, and think it’s not likely that we will hike, although they don’t take that possibility off the table.

So that’s—when you get to that question—and that’s your answer—there’s a natural—naturally, it begins to be the next question, which is when it will become appropriate to begin dialing back the amount of policy restraint that’s in place. So that’s really the next question. And that’s what people are thinking about and talking about.

FH Interpretation:

- Feds have shifted from inflation fighting to preventing a recession

- For much of this cycle Powell’s Fed was focussed singularly on combatting inflation even at the cost of a recession. The first time this cycle, Feds are now prioritising avoiding a recession.

Reference from Powell:

Q: Mike McKee from Bloomberg Television and Radio. Mr. Chairman, you were by your own admission behind the curve in starting to raise rates to fight inflation, and you said earlier, again, the full effects of our tightening cycle have not yet been felt. How will you decide when to cut rates? And how will you ensure you’re not behind the curve there?

POWELL: So we’re aware of the risk that we would hang on too long. You know, we know that that’s a risk and we’re very focused on not making that mistake. And we do regard the two—you know, we’ve come back into a better balance between the risk of overdoing it and the risk of underdoing it. Not only that, we were able to focus hard on the—on the price stability mandate, and we’re getting back to the point where—which is what you do when you’re very far from one of them, one of the two mandates. You’re getting now back to the point where both mandates are important and they’re more in balance, too. So I think we’ll be—we’ll be very much keeping that in mind as we make policy going forward.

…

And that’s really the question that we’re on. But of course, the other question—the question of when will it become appropriate to begin dialing back the amount of policy restraint in place—that begins to come into view, and is clearly a topic of discussion out in the world and also a discussion for us at our meeting today.

FH Interpretation:

- Feds will cut interest rates even before inflation hits 2%

- They do not want to wait until 2% inflation before cutting rates because that would be too late

Reference from Powell:

Q: Thank you, Chair Powell. Jennifer Schonberger with Yahoo Finance. You said back in July that you needed to start cutting rates before getting to 2 percent inflation. As you mentioned, PCE inflation is now running at three-and-a-half on core. On a six-month annual basis, core PCE is running at 2 ½ percent—though, when you look at supercore and shelter they are, of course, stickier. So in looking in the different components of the data, how much closer do you have to get to 2 percent before you consider cutting rates?

POWELL: I mean, the reason you wouldn’t wait to get to 2 percent to cut rates is that policy would be—it would be too late. I mean, you’d want to be reducing restriction on the economy well before 2 percent because before you—or before you get to 2 percent so you don’t overshoot, if we think—we think of restrictive policy as weighing on economic activity.

You know, it takes—it takes a while for policy to get into the economy, affect economic activity, and affect inflation. So I can’t give you a precise answer. But if you look at what’s in the—in the SEP and—you know, I think you’ll see a reasonable estimate of the time lags and things like that that it would take.

FH Interpretation:

- While rate cuts are on the table, no change to QT is anticipated for now

Reference from Powell:

POWELL: We’re not talking about altering the pace of QT right now, just to get that out of the way.

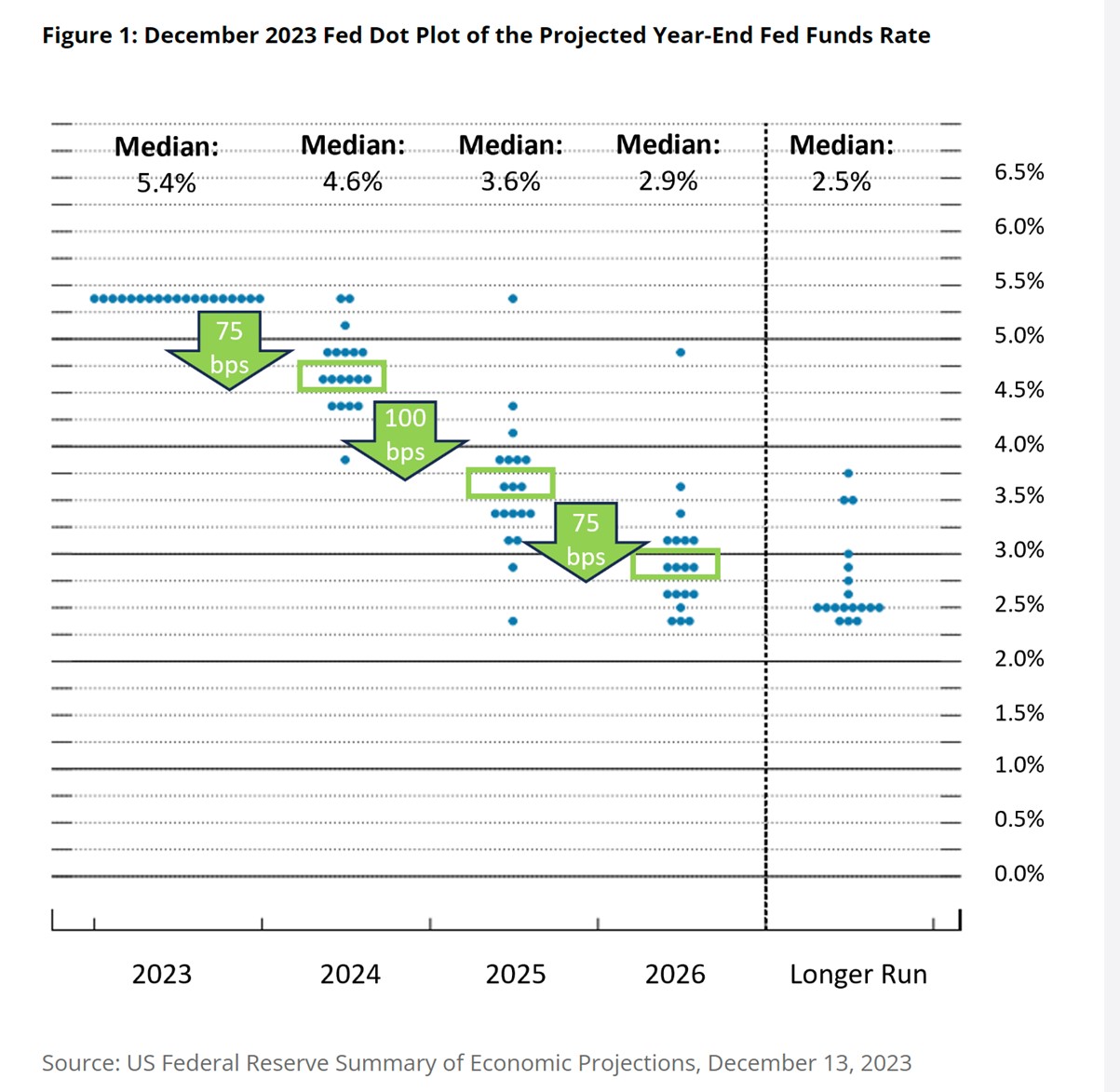

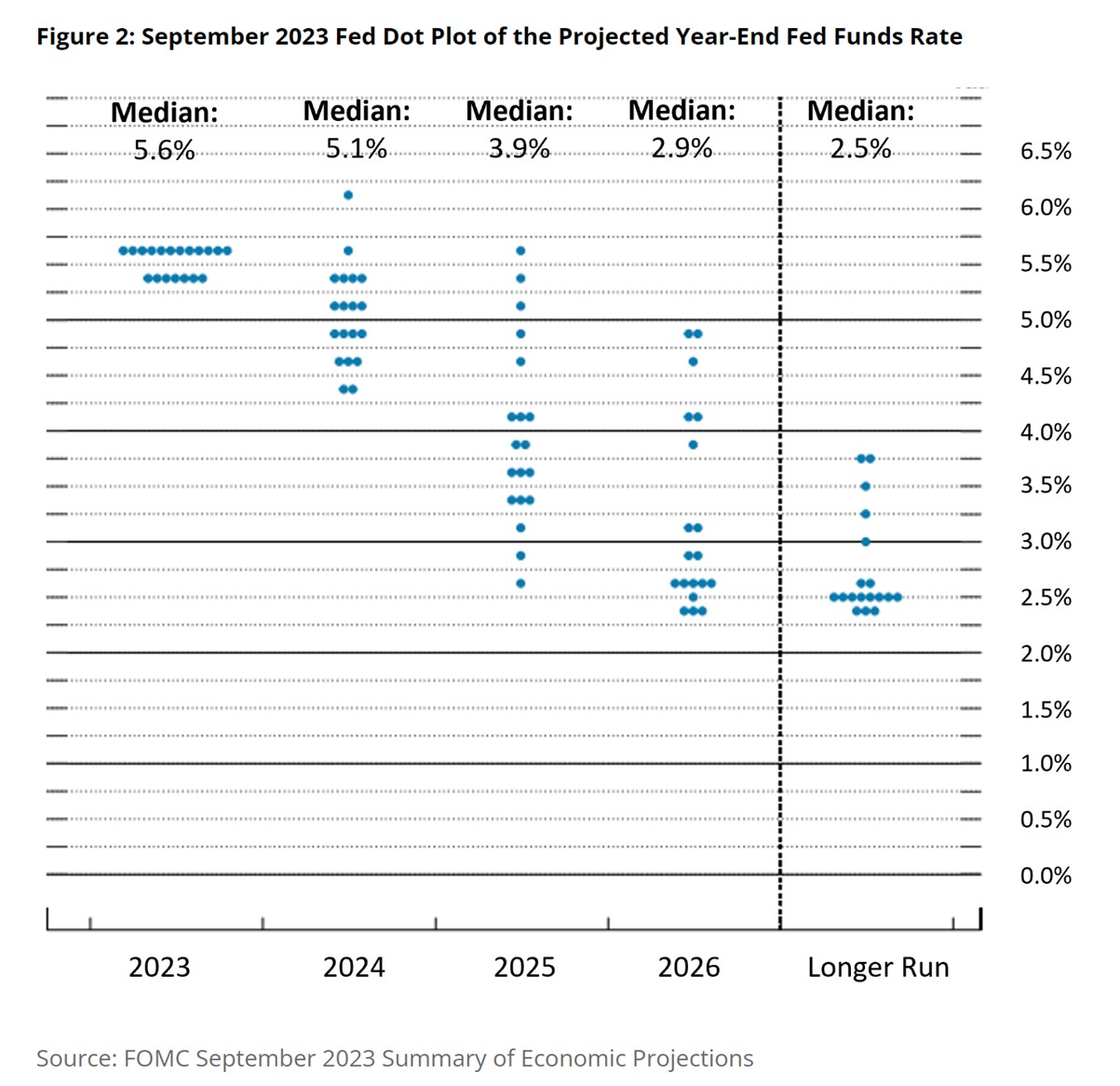

Changes to Dot Plot

The Fed’s Dot Plot indicates where the Feds see interest rates at the end of 2024 and 2025.

Here’s the latest dot plot – indicating an average of 3 rate cuts in 2024, and 4 rate cuts in 2025.

Note this is a big shift down from the last dot plot, which indicated much higher interest rates for longer:

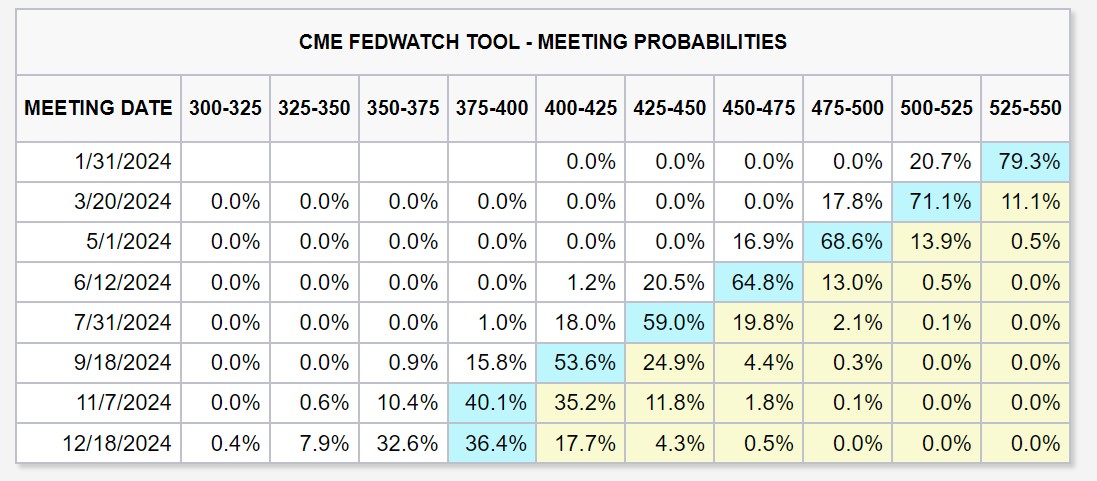

For what it’s worth, the market is even more bullish.

Market is pricing in a total of 6 interest rate cuts (1.5%), starting as soon as March 2024:

Timeline wise the Feds usually cut around 6 – 12 months after the last rate hike.

Given that July 23 was the last rate hike, it does point towards rate cuts in 1H 2024.

What does this mean?

Many people are talking about last night as the Fed “Pivot”.

For what it’s worth, I am inclined to agree.

Powell has been talking tough on inflation all cycle, about prioritising combating inflation even if it means a recession.

Last night was almost a 180 change in that messaging.

In the most dovish language all cycle, he effectively said that:

- No more rate hikes this cycle (July was the last)

- Interest rate cuts in 2024 (but the timing and speed to be decided)

- Feds will cut even before inflation comes down to 2%

- Feds are conscious about the possibility of a recession and wants to cut rates to reduce the risk of a recession

We’ve been talking about how a big question mark in 2024 is whether policy makers favour combatting inflation or preventing a recession.

And last night – Powell indicated a shift from fighting inflation to preventing a recession.

What happens next?

I suppose the next big question – will Powell be successful in preventing the economic slowdown?

The past 40 years has provided a clear template for how this normally works if there is a recession:

- Feds cut interest rates to prevent a recession

- Markets cheer the interest rate cuts which come as economic growth remains strong – and stocks rally into the first 2 – 3 interest rate cuts

- Economic growth continues to weaken despite the interest rate cuts

- Stocks begin sell-off due to fears over economic recession

- Feds forced into rapid emergency rate cuts in the face of recession (and potential financial instability)

There have been 6 interest rate cutting cycles over the past 40 years.

Of these – 4 have ended in recession (circled in red)

The only 2 that didn’t were 1985 and 1995, but those were cases where the Feds were ahead of the curve and hiked proactively to prevent inflation (vs this cycle where Feds were way behind the curve and hiked reactively).

So that seems to suggest hard landing, but the unprecedented nature of this COVID/deglobalisation cycle may distort things.

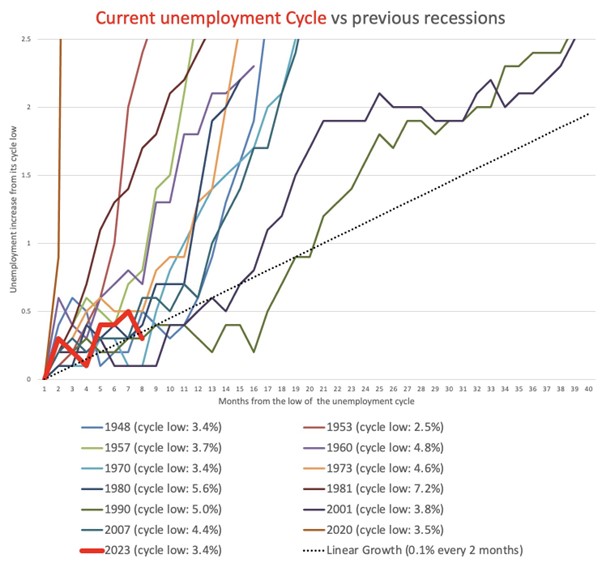

There’s an interesting chart below plotting the current unemployment cycle vs previous recessions.

If this is going to be a hard landing (recession), we would start to see an exponential rise in unemployment in the coming few months.

Whereas if it stays on a linear path (dotted line), it would suggest soft landing (no recession):

So for now, it is not immediately clear whether the recession or no recession path will play out.

But the fact that Jerome Powell’s Fed pivoted quite significantly last night, is a big factor that may tilt matters towards the latter.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

It doesn’t matter if you’re right or wrong, it matters how much you make when you are right…

Whatever the case, there’s no need to overthink sometimes.

The immediate beneficiaries of lower interest rates, that we have been talking about the past few months are:

- REITs

- Bonds (esp long dated US Treasuries)

- Tech (including crypto)

I have been accumulating (1) and (2) the past few months.

And both have done very well since the late October Yellen pivot, and again after the Powell pivot last night.

Many big cap REITs are up 5% today alone.

CICT for eg. is up about 18% from the low:

The impact is even more stark if you are using US Treasuries (as presumably this is a play that involves leverage via options or otherwise).

The 10 year yield has dropped from 5.0% to 3.96%:

Interestingly Tech has rallied a bit, but not to the same extent as real estate or bonds.

So that could be another play, if interest rate expectations continue to come down.

Crypto has been rallying for quite a while now – which is interesting because crypto seems to have smelt out this policy shift even before traditional asset classes.

What other investments could benefit from the Fed Pivot?

If you believe that the Feds will pivot successfully and avoid a hard landing.

Another big beneficiary here might actually be commodities.

Oil has dropped a lot of late due to fears over higher supply and weaker demand in 2024.

But if the Feds are successful in their pivot, this would mean a cyclical rebound in 2024, together with a weaker USD – both of which are bullish commodities.

Given that many commodities like oil and copper have sold off recently – this could be another potential play on the Fed pivot.

The problem with commodities is that they will do quite poorly in a recession, so it’s unlike bonds or REITs where after the sell-off, you’re getting a pretty juicy yield just to hold those positions (limiting downside where you are wrong).

I made quite a few changes to my portfolio this week

In any case, I thought that Jerome Powell’s “Pivot” (when viewed together with Yellen’s pivot in late Oct) was material enough that I made quite a few changes to my portfolio this week.

I’m still thinking through the full implications, but I will share further views with FH Premium subscribers on the moves that I made, and how I think this week’s events impacted the macro.

I will also update the FH Stock Watch this weekend on the list of Stocks / REITs I am keen to buy.

Do sign up for FH Premium if you are keen!

This article was written on 14 Dec 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

– Get up to USD 5000 worth of shares (Best promo of 2023 – Now Extended)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Seems like it’s not full bull market yet though

What do you mean by full bull market?

In terms of where we are in the euphoria and fear cycle, still very far from euphoria

Hi FH,

My question is not really limited to this post. For past few years, I never encounter any stock spilts in Singapore blue chips, unlike US (Amazon, Google, Tesla etc). Any idea how come Singapore companies do not go for stock spilts to attract more retail investors (eg local banks, Reits etc)? If not wrong, only OCBC had one in 2005

SG market is quite different from US. US stock splits are done for 2 big reasons: (1) make stocks cheaper for retail investors to buy one, (2) reduce price for options (as each option is 100 shares).

On (1) – SGX already did this with the reduction in lot size from 1000 to 100.

On (2) – SGX options trading is nowhere as extensive as US. And given the low price of each share on the SGX, not really a problem.

I know many bloggers regard CapitaLand Integrated Commercial Trust (CICT) as a reliable and resilient Singapore REIT

https://www.smallcapasia.com/3-singapore-reits-i-will-buy-if-i-had-s20000/