Ever since SATS announced their acquisition of WFS, their shares have dropped 40%.

A lot of you have asked for an article on SATS, and whether it’s worth buying.

I was a bit tied up over the holiday season, so I finally got around to reading the SATS circular this week.

And I must say, it was one of the more complex transactions I’ve had to analyse in a while.

But who am I kidding.

I loved every second of it – a welcome break from writing about T-Bills and Fixed Deposit.

So here goes!

Basics: SATS Acquisition of WFS for $1.82 billion

Let’s cut to the chase.

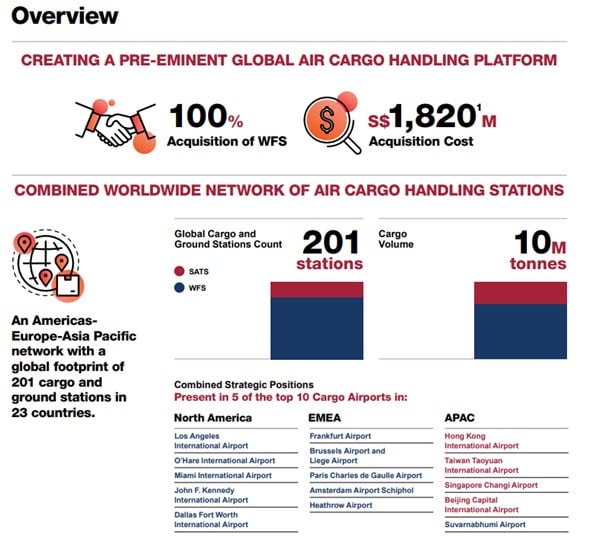

SATS is paying $1.82 billion to buy Worldwide Flight Services (WFS).

WFS is a “global air cargo logistics leader, and the number 1 global operator in cargo handling, with a global network spanning over 164 locations in more than 18 countries on five continents”.

This acquisition will be transformational for SATS

Let me just put it out there that this transaction will be transformational for SATS.

You can see the charts below.

Once completed, SATS will be catapulted from a regional player focussing primarily on Singapore, into a global player spread across Asia, Europe and America.

One of the largest in the world in fact.

A lot of the Temasek companies have been making bids to go global post-COVID (ST Engineering for example), and this looks to be the next in line.

Why does the market not like this acquisition?

But for obvious reasons, the market has its concerns about the acquisition, as you can see from the share price reaction after it was announced:

Let’s discuss the 3 biggest reasons that stand out to me (as a Singapore investor):

- Financing – How will SATS finance a $1.82 billion acquisition?

- Micro – Will SATS be able to successfully integrate WFS and reap operational synergies?

- Macro – How will the next 12 – 24 months look like for Global Air Cargo / Air travel?

Financing – How will SATS finance a $1.82 billion acquisition?

Let’s start with the elephant in the room.

SATS market cap today is about $3.2 billion.

The acquisition of WFS will cost $1.82 billion, which is about 56% of their current market cap.

That’s a lot of money to raise, in a climate where interest rates are creeping up incessantly, and liquidity is tightening.

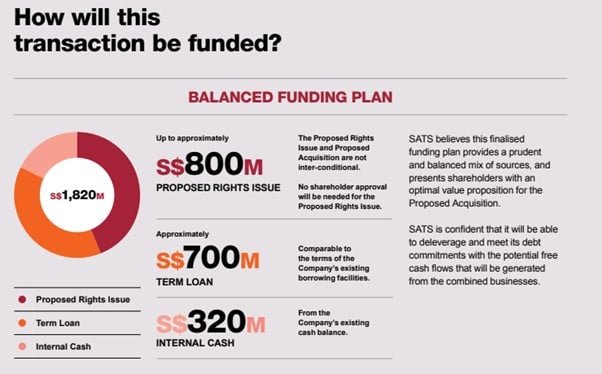

How will SATS finance the $1.82 billion?

When the deal was first announced, no concrete details of the financing was announced.

So the market assumed the possibility of 100% equity fundraising, which would be massively dilutive, and hence the share price reaction.

More details of the financing has come to light, and what we know today is:

- $800m (44%) via a rights issue

- $700m (38%) via a euro term loan

- $320m (17%) via cash on their balance sheet

For (2), approximate cost is 4 – 4.5% interest rate.

Not cheap, but in this climate definitely acceptable.

But (1) and (3) are problematic, and warrant further discussion.

$800 million rights issue is 25% of SATS market cap

For the $800 million rights issue, the exact price of the rights has not been announced.

Some back of the napkin numbers – $800 million is 25% of SATS current $3.2 billion market cap.

Which means that for every $1000 worth of shares you hold today, you’ll probably be looking at anywhere from $200 – $300 worth of new shares in the rights issue.

That’s not small.

So shareholders will be asked to raise a fair bit of money – and the price of the rights issue will be crucial.

$320 million cash is 46% of SATS cash

As of 30 Sep 2022, SATS had $689 million cash on their balance sheet.

$320 million will go to fund the WFS acquisition, which leaves about $369 million.

In other words, 46% of SATS cash position will be spent to purchase WFS.

This is compounded by the fact that WFS being private equity owned, is highly levered.

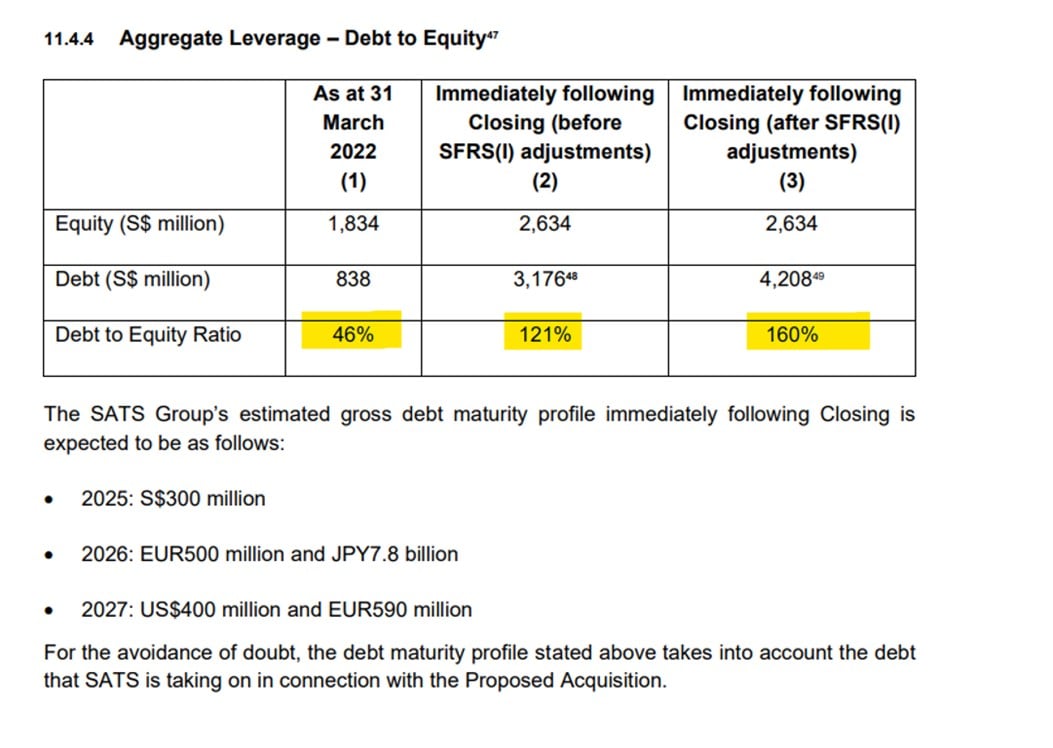

Pre-acquisition, SATS Debt to equity sits at a comfortable 46%.

Post-acquisition, SATS Debt to equity will jump to 121% – 160% (depending on accounting treatment)

I suppose what I’m trying to say, is that cash is a strange thing.

If you follow corporate finance textbooks, cash is a drag on performance.

The theory is that you want to hold as little cash as possible, and operate mostly on debt, to maximise shareholder return (like private equity firms do).

But in my experience – cash gives you optionality.

Cash gives you the runway to make mistakes.

The more cash you have, the more mistakes you can make.

Think about companies like Grab and Sea, and you start to appreciate the value that cash brings.

So… SATS will spend 46% of their current cash pile, and take up a lot of debt, to purchase WFS.

Which means they need to execute well post-acquisition, because the runway for making mistakes would narrow (with less cash on the balance sheet and more debt).

Which brings us to the next point.

Macro – How will the next 12 – 24 months look like for Global Air Cargo / Air travel?

You know the story by now.

Inflation is high, so the Feds are raising interest rates to 5%+ to fight inflation.

If interest rates stay at 5% for long enough, we’ll probably have a recession.

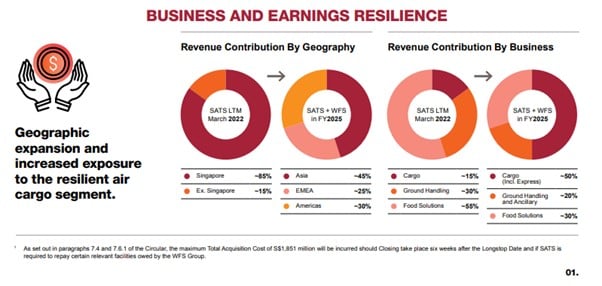

Recession is bad for Global Air Cargo / Air Travel, which is a decent part of SATS (and WFS) business.

Should SATS have waited to do the acquisition?

To give credit where credit is due, I think an opportunity to buy a company like WFS only comes around rarely.

Pass over this chance, and you don’t know when a company like that would be on the market again.

So I get the naysayers that say SATS should have waited for the stormclouds to pass before buying WFS.

But sometimes when you have a golden opportunity like this to become one of the world’s leading air cargo handlers, you don’t pass it up.

You just seize the opportunity, and do your best to navigate what comes.

And I do respect management for making that decision.

It’s bold, and it’s gutsy.

But… looming recession?

That said, this doesn’t change the fact that there’s a good chance that we’re heading into a global recession (or at least a slowdown).

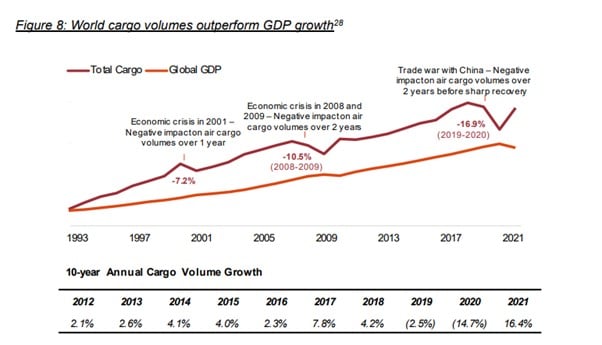

Now the cargo handling business is based on volume.

You get paid a flat fee per volume of cargo handled.

It’s not like airlines or freight forwarders who are directly exposed to freight costs, which can be very volatile.

So I would expect the impact to be less volatile.

But if you look at the long term numbers, you can see that where there is a global slowdown (eg. in 2009 and 2019), air freight volume does go down quite a bit.

So to say SATS or WFS is immune to a global slowdown is probably not true either.

And for what it’s worth – margins might come under pressure too, if inflation stays high.

But to be absolutely fair to them – this is entirely beyond the control of management.

All things considered, I do still think that making the acquisition is the right strategic move.

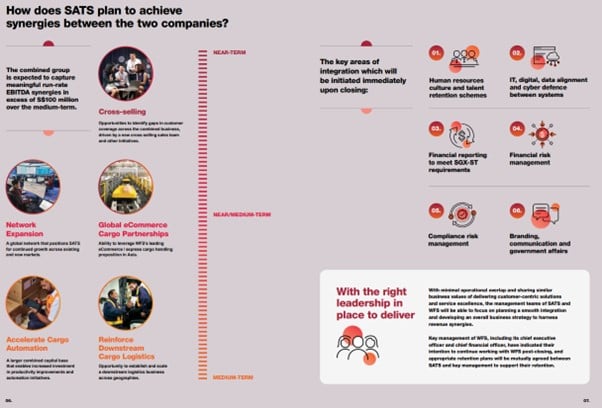

Micro – Will SATS be able to successfully integrate WFS?

And finally, will SATS be able to successfully integrate WFS and achieve “synergies”?

Refinancing the debt could be a big one

Off the top of my head, financing would be the low hanging fruit.

WFS was private equity owned, which means their borrowing costs would be much higher than what SATS can reasonably get as a Temasek owned company.

There could be a lot of cost savings there just from refinancing the debt.

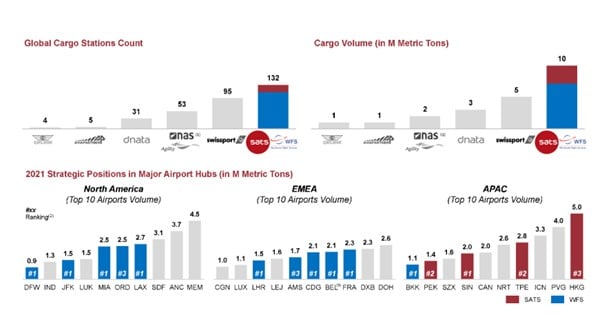

As for the other synergies, you can see the table below.

Lots of cross-selling opportunities I can imagine.

Can SATS achieve “corporate synergies”?

Now years of investing in public markets has left me jaded.

I’ve seen one too many mega M&A where this horse was promised huge synergies, only to get a much more mundane outcome.

Can SATS achieve these corporate synergies?

Frankly I have no clue.

The optimist in me wants to believe.

But the realist in me says the proof is in the pudding.

I will believe it when I see it.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

WFS is bigger than SATS?

Just another interesting nugget of information.

WFS pulls in about $2.5 billion revenue (ending March 22).

Whereas SATS does about $1.6 billion revenue (ending Sep 22).

So revenue wise WFS is bigger than SATS, which will only add to the integration difficulty.

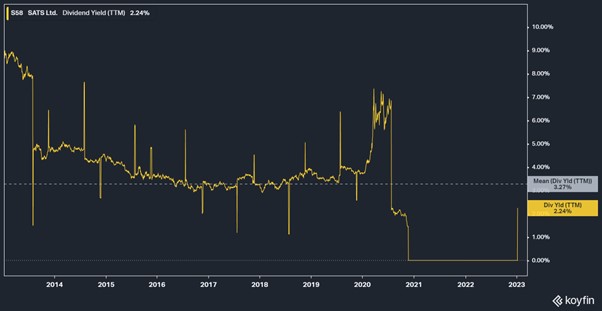

Dividend of SATS?

Pre-COVID, SATS was a stable dividend stock, averaging about 3%+ dividend.

Since COVID though, that dividend has been cut to 0, where it remains till today.

Management did address this in their FAQ, with the following reply (emphasis mine):

In light of the ongoing post-pandemic recovery, the Board of Directors believes it would be prudent to not pay a dividend until SATS restores profitability without government reliefs. This will enable the Company to continue investing in building capabilities and leveraging opportunities for profitable and sustainable growth.

I suppose at some point the dividend will be reinstated, but when, and how much, is frankly anyone’s guess.

Which raises further questions.

SATS today, is this going to be a dividend play, or a capital growth play?

Tricky.

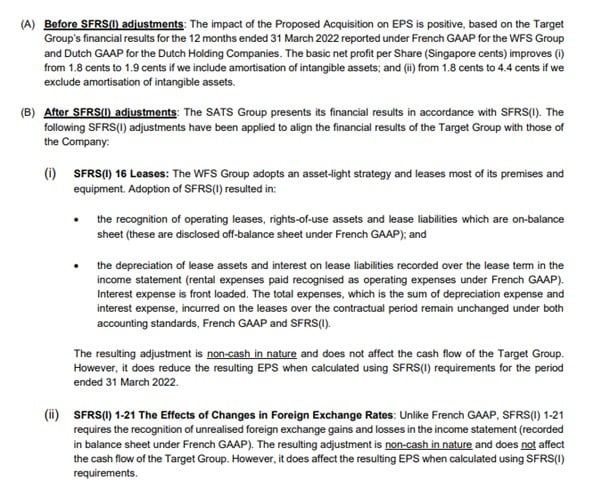

Fundamental analysis of SATS

I also tried running some simple fundamental analysis for SATS.

But long story short – the numbers are not meaningful because (1) SATS in FY22 was still loss making (2) there is a lot of accounting treatment required to translate WFS’ numbers over to SATS and (3) we don’t know the rights issue price.

If you really wanted a number, the pro forma in the circular, using a more generous accounting treatment, and assuming rights issue price of about $2.21, gives about 4.4 cents EPS.

At latest price of $2.84 that is 64x P/E.

But like I said, fundamental analysis is not meaningful.

You can take a look at all the assumptions required below just to transform the earnings into SATS.

Rights Issue price for SATS not out – this is a key piece of the puzzle

And finally, the rights issue price is not out yet.

The circular assumes a $2.21 rights issue price (which would be about 20% discount to latest market price), but that’s illustrative and I wouldn’t put too much weight on it.

Based on the timeline we should have the details some time in the first quarter of 2023, after the transaction is approved at the EGM.

Without knowing the rights issue price, any fundamental analysis on the stock is not meaningful, because the numbers will be distorted once the new shares from the rights issue comes into play.

So if you buy into SATS stock now, this is a big wildcard you must be aware of.

Will I buy SATS stock?

Full disclosure that I do not hold any positions in SATS currently.

What I like about SATS stock?

For the record – I like the vision behind this WFS acquisition.

I think it’s a bold and transformational deal, that will catapult SATS from a regional player into a global player.

I also completely understand why the deal was done at this point in time, because sometimes when you run a company you cannot pass up an opportunity like this, and you cannot wait for all the stars to align before making your move.

You just have to roll with it.

What I like less about SATS stock?

That being said, from a potential shareholder point of view, I do get why the market reacted this way.

SATS will be taking up a lot of debt, raising 25% of their market cap in equity, and blowing 46% of their cash position to finance the acquisition.

Right as we head into a global economic slowdown.

And normally with a dividend stock you at least get paid to wait, but here you don’t know when the dividend is coming back.

What will make or break this acquisition will be management’s ability to integrate WFS into SATS, and reap the synergies.

Whether this can be done – I leave it for you to decide.

Will I buy SATS stock?

For now at least – I’m not making any moves on SATS.

I would at the very least want to see the rights issue price be revealed before I make any further decisions.

Otherwise this is a massive overhang that will hang over the stock short term.

And given the global macro backdrop – When I can get 4.2% risk free on a T-Bill, I see little need to risk capital at all.

Unless of course it’s an irresistible buy.

So the hurdle rate for any new investment has gone up massively, and for now at least, I would like to see the rights issue price before making any decisions.

If you’re keen, you can check out my full stock and REIT watchlist (and personal portfolio) on Patreon.

As always – love to hear what you think!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Thank you for the article on SATS’ proposed WFS acquisition. I hope you can follow up with another article on the rights issue.

From: Ang See Perk ([email protected])

No worries, hope it’s helpful. Been getting quite a few queries on SATS.

Ok – will see if I can do an update after the rights are announced.

Its not a good acquistion. It is expected in the updated circular for financials SATS EPS will only increase 0.1 cents with the WFS purchase (mentioned BRT in valuebuddies forum), this mean the acquistion will generate about 11 million including acquistion synergy. To finance 1.8 billion purchase for 11 million+ profits yields a 163 PE

EPS is not so meaningful because SATS was loss making in FY22, and the pro forma does a lot of accounting treatment to translate WFS’s numbers into SFRS for SATS reporting.

But that being said, I do get where you’re coming from.

And I’m inclined to agree.

Short term bad, long term could be good depending on how well they execute.

Another component to add is the debt from WFS that SATS will be taking on. The actual total cost of WFS is north of $3B.

$1.8B directly funded by SATS and add on the $1.5B or so debt current in WFS books

This is highly risky for a firm who have no experience in operating a high debt environment. Existing Cashflow cycles need to revamped to cater for the higher yield.

Fair point.

Hihi,

SATS has done a number of acquisitions in the past. How did these turn out? Might give a clue into what their m&a track record is like, especially as it relates to their ability to integrate and execute.

Should we be expecting some kind of temasek backstop? Say if demand for the rights issue is very poor or if temasek could take up some of the debt issuance or via some kinda partial guarantee in the debt.

Dont believe they have done a deal of this size and scale before. So not sure how helpful track record will be.

A lot of things changed post-COVID too.

My understanding from the circular is that Temasek will be taking up their pro-rata stake for the rights. And the rest will be underwritten by the banks.

If you’re asking if there is an implicit Temasek guarantee if things head south though, then that’s a more delicate question. Looking at the track record for the other TLCs the past few years, I would say probably yes, but whether it is done in a way that preserves shareholder value for the minority is probably the better question.

SATS is the company will definitely keep the shares price up by 2 years time. Not so worry about all the saga which is happening now. The company is targeting to gain revenue and profit within 3 to 7years time. Just stay tuned.

Interesting, appreciate the sharing. Could well be true if they execute well on the integration.

To be honest, the acquisition of WFS is considered a baptism of fire for the new CEO, Mr Kerry Mok, whose tenure started only in December 2021. The first acquisition led by the new CEO was actually the acquisition of additional shares in the capital of Asia Airfreight Terminal Co. Ltd (“AAT”). That deal was completed in March 2022 but was for a considerably smaller cost of $58.5 million. WFS is another ball game altogether as the mega deal costs more than a whopping billion dollar.

Regards,

Gerald

https://sgwealthbuilder.com

Thanks, appreciate the sharing of the background!

Curious to hear your views Gerald – are you a buyer of SATS at current price?

Dear Financial Horse

Can I check what is the day of the SGX announcement that shows the post acquisition debt to equity will go to 160% for SATS ?

Many Thanks

Martin

Hi Martin it is in the circular that SATS issued to approve the transaction (for the EGM). 🙂

Thanks !