I received a great question from a reader recently:

Dear FH,

I have been following your articles for some years now and would like to thank you for all the awesome content that you write.

I am in a bit of a dilemma now with regards to what to do with a sum of money that me and my husband have saved up over the past 5 years. And wonder if you can help to shed some light on this ????

Not sure if its ok to ask you about this. But don’t really know who else to ask. If we ask a property agent, they will surely try to convince us to buy a property. And friends around us are not savvy enough to give us their opinion.

We have been saving and investing the best that we can for the past 5 years ever since we got married.

We have about 200k cash on hand.

If my husb buys a new 2 bedroom condo for investment. We would have to fork out about 82k cash. The rest by cpf. We intend to sell it at the 3 year mark. Hopefully to make a profit of 100k and above in 3 years time.

My question is whether we should dca the 82k slowly into stocks, reits, etfs in the current bear market? or should we put it into a property?

Which may generate a better return?

My concerns are:

- the rising interest rate environment that we are in right now.

- the new launches are going at crazy prices of $2200 psf for OCR projects. I just wonder what’s our upside if we are buying in at such a high price.

- Should we be forking so much cash when I’m on no pay leave.

For context,

- I have a resale HDB which I bought when I was single (rented out).

- We have about 300k in investments (stocks, reits, bonds, etfs)

- We have 2 young kids and elderly parents to care for.

- We have steady jobs but I’m currently taking no pay leave from work.

- We are in our early 40s.

Hopefully you can share with us your opinion?

Note: Some details have been tweaked to preserve anonymity.

Should you buy a Property or Stocks/REITs in 2022? (as a Singapore Investor)

The more I thought about it, the more I found this quite a complex, nuanced issue.

The answer isn’t as straightforward as buy xx because you will make more money.

So I wanted to share my views in this article.

And hopefully it might come in helpful to others out there who are facing a similar dilemma.

Investment Returns – Which will make you more money?

Let’s start with the pure investment aspect.

The 2 options on the table are:

- Buy a 2 bedroom property – with $82,000 cash, and the rest CPF

- Buy $82,000 worth of Stocks/REITs

Buy a Property

It wasn’t very clear, but it seems the reader is looking to buy a new condo.

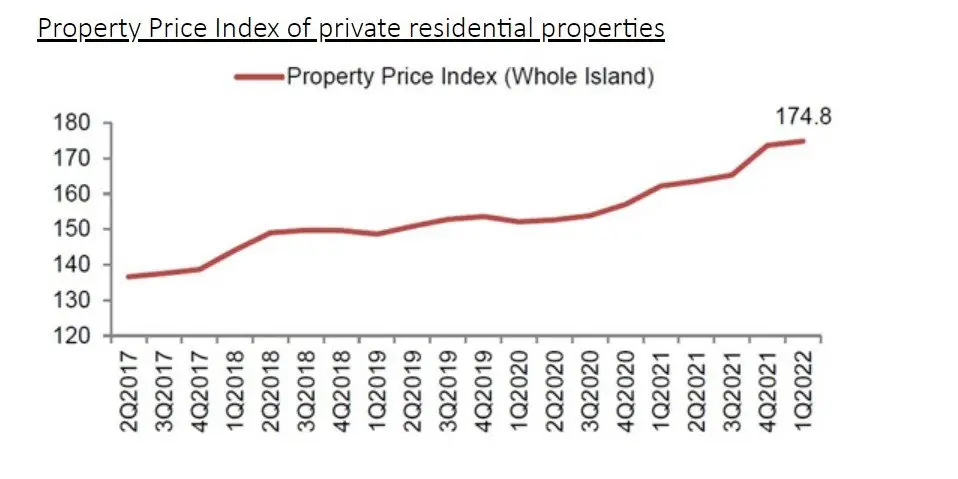

Some of the new 2 bedrooms are about 600-700 sq ft, so at $2200 psf that’s a purchase price of about $1.3 – $1.5 million.

With $82,000 cash, that means $293,000 from CPF.

Which is not unrealistic for a 42 year old who hasn’t touched his CPF-OA.

Is $100,000 profit realistic on a $1.5 million property?

A $100,000 profit on a $1.5 million property over 3 years is a 6.6% return.

This works out to a 2% return a year, give or take.

I suppose that’s not unreasonable.

Are you buying property a high?

Unfortunately – Yes I think so.

I wrote a long post for Patrons recently on the housing issue.

The long and short is that I think rentals/prices can hold up short term because the supply of housing in Singapore is still very tight.

But if you look out into the medium term, say 2 – 3 years, then the picture does look quite different.

Over a longer timeframe – More supply will start to come online.

And the rising interest rates are going to kick in.

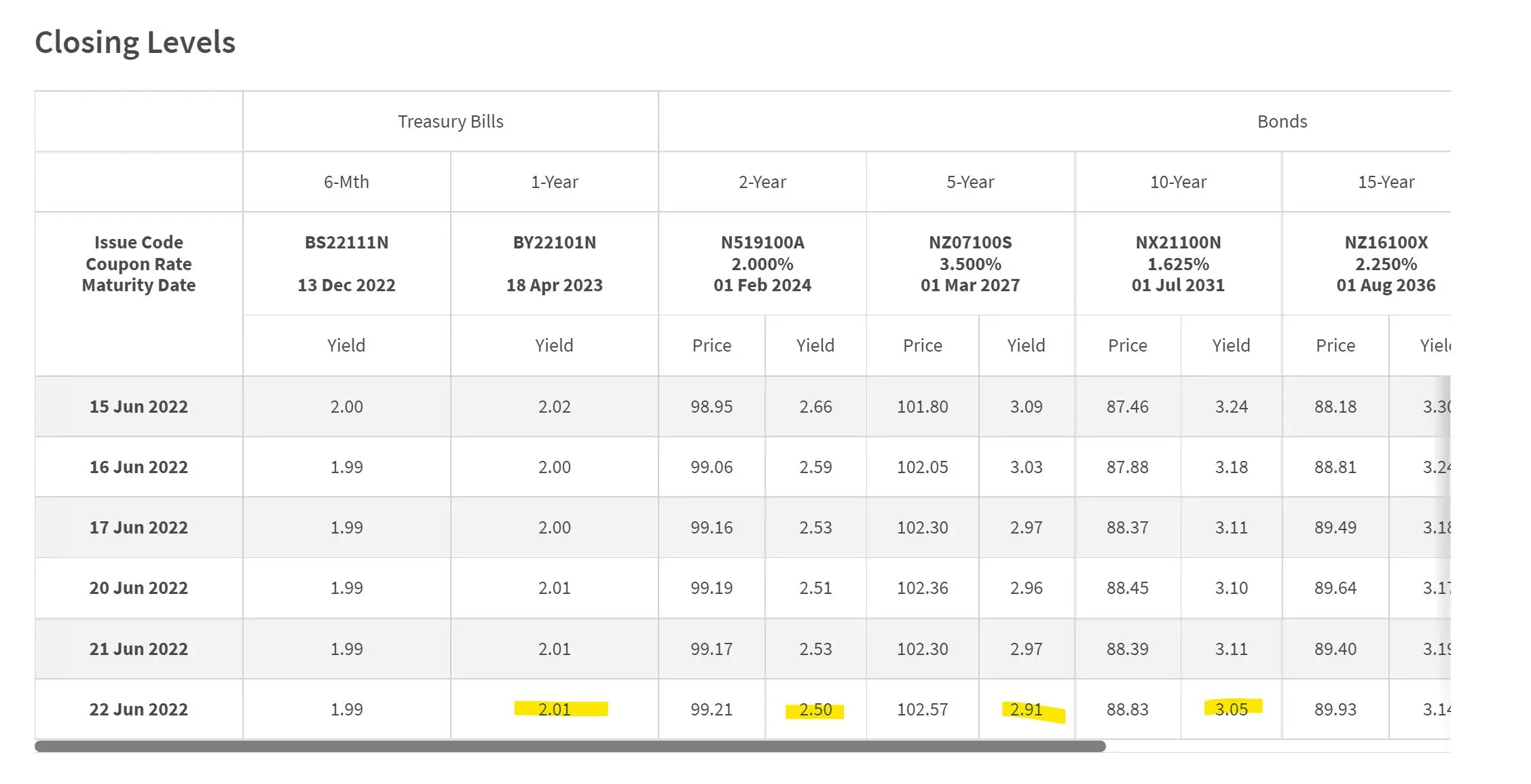

I mean just look at the latest interest rates – 10 year SGS is at 3.05%.

If mortgage rates go anywhere near there, and stay there, I would expect demand for housing to come down significantly.

The early signs from other countries are not positive:

Is a 3 year holding period realistic for Singapore Property?

That said – a big gripe I have is that I’m not sure if the 3 year holding period is realistic.

I think we’re at a short term high now, so whether you’ll be able to flip the property for a profit in 3 years, is quite 50-50 in my view.

The longer one is able to hold the property, the higher the certainty of returns.

Otherwise, it will come down to how good you are at picking the property, and what the macro conditions / cooling measures / demand supply situation is like in 3 years.

Which can be quite hard to predict.

I think there is a real risk if you pick poorly, and if macro conditions turn – you could be underwater on your property in 3 years.

How much can you make with $82,000 in Stocks / REITs?

Let’s not mince words.

If you want to make $100,000 on stocks/REITs, with a $82,000 initial capital.

That’s a 120% return over 3 years.

Which means you need to achieve a 35% a year return – for 3 years straight.

I mean it’s not impossible, and if you’re a great investor, with fantastic timing and nerves of steel, you might just pull it off.

But if you do – you should probably switch to fund management full time instead.

With this kind of performance, I’ll give you my own money to invest.

What if you invest more in stocks/REITs?

Let’s say you decide to all-in stocks.

You take the $82,000 cash, throw in $100,000 CPF-OA (the max you can invest assuming a $300,000 CPF-OA).

Maybe you even take a $100,000 margin loan on top of that.

That’s only $282,000, give or take.

A $100,000 return on that is a 35% return over 3 years.

About 10% a year.

Not impossible – but you probably need to take on a fair bit of risk. Which makes it very tricky with the margin loan.

What would I do?

So from a pure mathematical perspective.

If I buy a house, I just need to achieve a 2% a year return to make $100,000 over 3 years.

If I buy stocks/REITs, I need to achieve a 35% a year return (or 10% a year if I’m ultra aggressive) to make $100,000 over 3 years.

Which would I be more confident in achieving?

Probably the former.

But… I think the situation is much more nuanced than that..

Leverage is a double edged sword

If it isn’t already obvious by now – the key differentiating factor above is leverage.

Leverage allows you to juice your $82,000 cash outlay into a $1.5 million property investment.

But of course, leverage works both ways.

Just like how it can juice your returns.

It also means that if you buy the wrong property, or if the property market turns against you, you can lose far more than your initial $82,000 cash outlay.

Differentiating between the short term, and the medium term

The other point I wanted to add though, is that the timeframe is key.

If you’re investing for 1 year, 3 years, or 5 years – your considerations are very different for each.

My simple view is that I think the short term (6 – 12 months) will be bad for financial assets.

Tightening monetary conditions and rapidly rising interest rates are going to crush financial assets, which is a point I’ve been going on and on about since Jan 2022.

But if you look past the next 12 months.

If you look into second half of 2023, or 2024 and beyond.

What does that look like?

I don’t know about you, but it looks very inflationary to me.

Why I think this decade will be inflationary

I just see a confluence of factors coming together to create supply chain disruptions that persist into the middle of the decade.

Underinvestment into commodities. Russian oil getting shut off due to sanctions. Transition to net zero. Deglobalisation.

I see many supply chain disruptions, but very little realistic solutions.

The solution from the Feds is to raise interest rates.

And sure – higher interest rates will crush demand. Demand comes down, and inflation goes away.

But at some point, the pain will be too much to bear.

At some point – whether the S&P500 is down 30%, 40% or 50%, the Feds will relent.

This isn’t China, the Americans and the Europeans don’t have the stomach to do what it takes to truly crush inflation.

When the pain gets too much, they will roll over.

So some time in 2022/2023 when financial assets are crushed, and after the mid term elections, the Feds are going to start easing interest rates, and printing money again.

But the supply situation hasn’t been solved right?

So when demand recovers – prices start going up again, and inflation comes back.

What do the Feds do?

Reducing Inflation Will Come at a Great Cost: Stagflation

Ray Dalio wrote a great piece this week on inflation.

It’s well worth the read, but to sum up:

In summary my main points are that 1) there isn’t anything that the Fed can do to fight inflation without creating economic weakness, 2) with debt assets and liabilities as high as they are and projected to increase due to the government deficit, and the Fed also selling government debt, it is likely that private credit growth will have to contract, weakening the economy, and 3) over the long run the Fed will most likely chart a middle course that will take the form of stagflation.

Ray Dalio probably puts it more eloquently than me – but the gist is the same.

The Feds will try to fight inflation, which will cause a financial asset sell-off (and possible recession) in the short term.

But mid – longer term, they don’t have the stomach to do what it takes to crush inflation.

And they will return to money printing, which will result in an inflationary decade.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Okay gun to my head – do I buy a $1.5 million property this year, or $82,000 in stocks/REITs?

I’m probably buying the property.

But – and massive caveat here, I just think I’m buying into a short term high in the property market. With rising interest rates.

So I’m going to do a ton of due diligence, and make sure I’m picking the right property.

This isn’t a bull market where a rising tide lifts all boats, and you can get sloppy with your selection. In a weakening market, only the strong properties perform well.

The reason why I picked this way – is really because of the leverage.

In an inflationary decade, you want to take on as much debt as you can, and use it to buy real assets.

The value of your real assets goes up, while the value of your mortgage gets eroded away.

How to finance the loan?

That being said – there’s no doubt that interest rates are going to go up short term.

Do you go with fixed or floating?

I know a lot of you have been writing in for my views on this, and I plan to write a full article for this. But in this market – I think you’re pretty much forced into taking floating rates. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In any case – I came across a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing. It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I set up the reminders for my own properties just this week and it’s pretty neat.

Do give it a try here.

How to service the mortgage? Should you be forking out this much cash?

The reader has $200,000.

After $82,000 spent on the house, that’s $120,000 left in cash.

But this is a new property, so you can’t rent it out.

While mortgage payments will be going up due to rising interest rates.

Should she be forking out this much cash?

That’s ultimately a question only the reader can answer.

Everyone’s risk appetite is different, and I don’t know the income situation of the family.

But the way I see it, $120,000 cash, CPF-OA fully depleted to pay off the house, 1 income in the family, 2 young kids and elderly parents to care for.

I think that might be a little too tight for my liking, from a cash flow perspective.

Sure there is $300,000 in stocks/REITs, but if the market declines further this year, most of that cash cannot be accessed without selling at a big loss.

Caught between a rock and a hard place

But I mean I completely get the dilemma here.

Play it safe and chuck the cash in a bank, and watch it get eroded by inflation.

Take some risk for the chance to make more, but risk losing your hard earned cash.

It sucks that we are in this situation, but a decade of poor central bank policies has us here. And it is the ordinary people who have to pay the price.

It breaks my heart.

Third Options – Hold cash

There is of course a third option here – which is to just do nothing, and hold cash.

The upside, is that if the rising interest rates cause a property market crash, or stock market crash, then at least you escape the losses.

And you can buy into a low.

The downside of course, is that if the property market doesn’t crash – perhaps because supply is tight, or government intervenes, then you’re out of luck.

The other problem with this kind of thinking, is that I know of many investors who patiently build up a warchest to “Buy the Crash”.

Then when the collapse comes, and the Feds pivot, they are too afraid to buy because REITs are down 40% – and they think it can go down another 20%.

So I think you want to think a bit about the kind of investor you are.

If you have nerves of steel, are a seasoned investor – with no problems deploying serious amounts of money into a 2008-style event, I think this third option can be considered.

If you’re prone to panic selling, then maybe you want to think twice.

What would I do if I had no constraints?

Let’s say I didn’t have any of these constraints.

What would I do, if I were in the same situation?

I might actually use the money to buy a resale condo, and rent it out for yield.

But I won’t be in any rush to buy.

If I see a great property at a decent price, Ok I go for it.

If I dont see anything I like, I could just sit on my hands for the next 6 – 12 months, while I watch the global macro play out. And I can then decide whether to buy a property or stocks/REITs, depending on how prices move over the next 12 months.

I went with this approach because I still think the leverage is the key.

The leverage allows you to multiply a $82,000 cash outlay into a $1.5 million investment. Which I think could be very helpful during this decade, which I still think will be an inflationary one.

The same with stocks, only takes you up to $300,000, and with significant risk.

But with this approach – the price, and the property are absolutely key. As is cash flow management in the short term, as interest rates go up.

Pick wrongly and you can lose big money. Which is why I would not be in any rush to buy.

Bide your time, and if no fat pitches come along – you can always change your mind and buy REITs if they drop in price significantly.

With a resale property, valuations also haven’t gone up as much as the new launches. And you *should* still be able to rent out the property, to cover some of your monthly mortgage payments.

But frankly – there is no free lunch in this world. If you want to generate returns, you do need to take on a certain level of risk.

The question to ask yourself is whether this is a risk you are comfortable with, if things head south.

Update: Be realistic about the return?

I had a couple of great discussions with readers on this.

And it got me thinking – Maybe the real answer here is to be more realistic about the returns.

With property markets at a high, a collapsing stock market, and the most aggressive Feds in 25 years – frankly this is not the kind of macro climate you want to be loading up on risk.

This is the kind of market where as long as you get through the next 12 – 18 months without a significant loss of capital, you’re already happy.

And I can get on board with this.

So maybe the answer here is to just hold cash, and bide your time – and wait for the Feds to pivot before deploying serious cash.

Closing Thoughts: Be realistic with your level of knowledge

The final point I wanted to make – is to be realistic with your level of knowledge.

Picking the right property is absolutely key here. You must realise you’re buying into a property market at a high, with rising interest rates.

And whether the rental market will hold up going forward, nobody really knows.

I have a simple guide on the points to look out for when evaluating property, but you must understand that for every property transaction, there is a seller on the other side.

There is a guy out there, who thinks that he is getting a fantastic deal selling his property to you.

Do you think you are smarter than him?

Because that’s what it’s going to come down to.

Refinancing Tool – Will you save money by refinancing your mortgage?

I know a lot of you have been writing in for my views on fixed vs floating loan mortgages, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating rates. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

Whatever the case, mortgage rates are going to move a lot in the coming months, and if you’re out of your lock in period, it’s probably a good time to refinance.

If so – there’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing. It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I set up the reminders for my own properties just this week and it’s pretty neat.

Do give it a try here.

As always, this article is written on 24 June 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi FH,

I think this is very dangerous advice. Taking on leverage in an environment where one does not know what the peak interest rates will be is highly risky. In the broad spectrum of history, the low interest rates of the last decade are an anomaly caused by the belief after the 2008 financial crisis that printing money excessively has no consequences. Clearly, that view has changed and the era of free money has ended. Looking back at historical interest rates over the last 50 years, one finds that mortgage interest rates of 5% or more are actually very common. A leading Singapore economist was recently quoted in BT saying that he expects Singapore mortgage rates to reach 4% by year end and 4.5% by 2023. In the US, they even went above 10% in highly inflationary environments.

Furthermore, taking the assumption that one can pay off part of the mortgage with rent is also a risky one. In a downturn, one may not be able to find tenants. There will be 30,000 new completions of condos between now and end of 2024. One will be competing with many investors to find rentals.

Finally, there is not enough attention paid to the risks of buying at the peak. Those investors who bought before the 1997 Asian Financial Crisis took more than 10 years to break even. Even those who bought at the most recent previous peak took 6 years. So while gaining 2% per year may seem doable, when the market is at a peak, losing 10-20% of leveraged money is equally doable and in this environment, one could be on the hook for 5% mortgage while struggling to find tenants. If the mortgage is 4-5% while rental yield is 2-3%, the tenant is not paying your mortgage, you are subsidizing his rental!

Hi CMC,

Very valid points – and I agree with what you raised.

Another point I might add is that with an intention to sell in 3 years, there’s no guarantee one would make a profit by then. Property market could easily be underwater with a 3 year horizon.

Taking a step back though, I suppose the bigger question is what is the alternative.

Is it to park the cash in a bank account? Because if the mid term outlook is going to be inflationary, cash has a very real opportunity cost associated with it as well.

Is it to hold cash, and hope for a housing crash in the next 1 – 2 years to deploy? Hard to call also, because of the supply constraints, and possible government intervention.

It was a similar line of thinking that led me to buy another property in mid 2021, as a way to increase my leverage + get exposure to real assets. Whether the move still makes sense today, whether it makes sense for individual investors – that’s ultimately a question for each investor.

Hi FH,

I think the principle to buy when things are low and not when they are high still stands as Fastpace alludes to below.

Reits are fairly low now having corrected somewhat already, especially blue chip ones like Ascendas and MIT offering 5.5% yield. They could go lower for sure, but they will never go bust and will always provide some yield until cycle turns again.

Taking on high leverage now to buy a property when prices are at all time highs may lead one to personally go bust if the market turns against you.

Upside at this stage is limited but downside can be disastrous so the risk reward ratio is not great. A mortgage is a 20-30 yr commitment which one is stuck with if interest rates soar.

So at this point, rather than aiming for high gains like your reader is doing, risk management is probably the more prudent approach to take. For vast majority of people, the Reits path is probably better right now.

That’s a good point.

Maybe the answer here is to be more realistic about the returns.

This is not the macro climate where you want to be loading up on risk, and gunning for 100k returns in 3 years. This is the kind of market where as long as you get through the next 12 – 18 months without a significant loss of capital, you’re already happy.

I can get on board with this. Just hold cash, bide your time – and wait for the Feds to pivot before deploying serious cash.

In any case, I wanted to thank you for your great comments CMC. I’ve updated the article to incorporate some of these points that you mentioned. I do agree that if the reader is ready to accept lower returns, the much safer play might be to just do nothing… for now.

And let the next 6 – 12 months play out before making further decisions.

A few issue has been highlighted, ultimately is still the person to make his decision. There is no hard n fast rules on which one to chose and it is not easy to invest big sum of money now, understanding your own risk profile is importance here n how far you can go, should situation turn south fast n hard. IMO no point joining the herd to rush to get into property now, when we are at all time high now n interest rate is not going to be kind to you. Buy or invest base on counter cyclical, when market hates it, that the time to move in n pick what you like, All the best to them.

Yes exactly this.

I absolutely agree that it is not easy to invest big money now. This is one of the trickiest markets in a long time, and anybody telling you they know how the next 3 years is going to play out is just lying.

There’s a good chance we get deflation and an asset bust, and also a good chance we get stagflation / inflation. Druckenmiller had a great interview recently where he said there’s no historical precedence for our current situation, in his 45 years of investing. I see macro investors drawing historical parallels with post-WWII era, which goes to show how unique our current situation is.

As investors – it pays to be humble in times like this.

Recognise the risks, protect the downside. But at some point, one needs to make a decision on how to allocate wealth. And that’s ultimately a question only each investor can decide for themselves.

It seems they have more experience with stocks & reits than properties. Trying to get OJT property experience when property prices are high & mortgage rates are going up seems kinda risky. Reminds me of mom & pop investors getting interested in stocks after the market has gone up 100% in the last 2 years. 😉

Personally I’d enjoy the 1 year no pay leave without having any financial stress overhang. Her salary in years 2 & 3 will likely be over $200K. Save half of it & you have the $100K at end of year 3. 😛

In the meantime, if there’s any capitulation event in stock markets over the next 6-12 mths, they can put some of their $200K to work.

That’s a good point. The 300k in stocks/REITs does indicate a decent level of familiarity and comfort with stock/REITs.

Which may tip the scales strongly in favour of capital markets. Especially given the possibility of a tail risk event the next 6 – 12 months.

Also agree that this is not a good market to be buying property (or learning about property). I last bought one in mid 2021, and market was already not a fun one back then for a buyer. Looking at the latest prices and liquidity, it has only gotten worse.

Hahaha – love the point about the no pay leave. True indeed! 😉

Hi FH,

I would advise differently, based on the principles of longetivity (for your reader and her husband to be able to stay the course in their wealth building journey), flexibility (to cope with unexpected circumstances), and realistic risk-return expectations.

Your reader presents two binary choices between 1) put 82k + wipe out CPF + borrow to invest in property and 2) invest in stocks / bonds with her 82k in cash (with approx 120k remaining). Return target of 100k in three years.

I would first say that 100k in 3 years is certainly not a realistic expectation. Sure one can leverage with property, but given the headwinds you have highlighted, I do not find the risk-reward to be attractive.

In fact I would advise against BOTH options at this juncture. With 300k invested in stocks / bonds / etfs, I think they are already in quite a good financial position. The four room HDB generating rental Yield is also a huge plus. The 200k in cash helps give them peace of mind and flexibility, especially as they have two kids + two old parents, so they would have to buffer beyond the traditionally advised 6m of emergency savings.

Should they have the appetite, i think they can slowly DCA into their existing stock / bond / etf portfolio. But I would definitely advise against deploying the full 82k at one go.

If they still wish to buy a second property, I think it would be prudent to WAIT. Interest rates have adjusted higher, but property prices have yet to adjust lower. So in my view, I think they can time it better and wait for the market to turn down before going in. I appreciate the demand-supply mismatches are ever present, but what we are seeing the same in most developed markets but yet prices have started to decline as mortgage rates rise, even though home supply remains constrained.

Best case home prices are mild up to flat. No one expects home prices to go gangbusters here. Do you? Worst case home prices fall 10-20%. I find there to be little opportunity cost in waiting here. Since interest rates are rising and fixed rates are unattractive, there is no hurry to lock in mortgage rates here. Why not wait and see how the market will respond to higher interest rates + higher supply a few years out?

So what I would do if I were the couple is put my cash in Singapore savings bonds. I think as a couple they will still have room to deploy; given 300k portfolio and 200k per pax SSB limit. This enables them to wait for a better entry point, protect capital, and collect yield. If SSBs are maxed out, fixed deposits might be an option. In a rising rate environment, short term cash like instruments actually give good yield.

While it is true that cash is being eroded by inflation. It still beats being down 20-30% in stocks and bonds. So while I empathize with the cash is trash view, I do also want to point out that cash performs decently during periods of elevated inflation and when central banks are hiking aggressively. Added optionality is also a big plus here.

I also think we should not overplay the Hong Kong exodus = higher rent story. Bloomberg reports that it has been “a trickle” rather than “a rush”, because the government has also tightened EP approvals. So yes Hong Kong talent is very much welcome, but now the government is more stringent in allowing a “certain type” (either super rich or with rare skills that locals don’t yet possess).

So to summarize my advice to your reader. Be cautious. now is not the time to be super aggressive with risk. Economic uncertainty is elevated, and she is also in a life stage where she is less able to work and has more dependents to look out for. Bide her time, park the cash in SSBs to collect some yield while waiting, and look to buy a property when a better price entry point presents itself and/or when we get more clarity on the outlook.

Hi Moomoo,

Fantastic, well thought out comment.

Better solution might really be to do nothing for now. This is not the kind of macro climate to be taking risk. Just play defensive, lie low, and watch how things play out the next 6 – 12 months.

If all is clear, invest then. If not, one would be glad they waited!

Appreciate your sharing. 🙂

The discussion in the comments section is great. FH you should definitely direct your reader to read the comments section as well! Has a good “for and against”, and serves as a good counterbalance to your article 🙂

I was gonna write the same thing, due to risk profile and current market conditions, if one wants to survive- play it safe, put it in ssb. It also does sound like the majority of their war chest is in cpf oa which is also earning interest. Also, continue with their existing plan which helped them to accumulate 300k in stocks/bonds (still no small feat as a sandwich class)

I remember hearing a financial coconut podcast on property stating that the majority of property returns are on the purchase price. So if one reads all the comments, smells like we’re close to property cycle top.

As usual, stay humble and survive

Am inclined to agree with this.

Having read all this comments and reflected a bit more – I do agree better move might be to just wait and see.

If I were forced to find a way to make 100k in 3 years, the house might be the easier option. But like all of you have pointed out, the problem here might be that the goal is not realistic, given the circumstances. Might be more realistic to just manage expectations, given that their financial conditions are not that bad to begin with.

Yes! The reader has gone through the comments section, and I am sure she will find it as useful as I have! Kudos to all of you I must say.

Btw fh, super good article in terms of getting brain juices flowing and thinking of scenarios. I’m sure there will be more than one reader who is going through this.

Kudos on the topic of choice!

No – big kudos to all the readers (and yourself) who stepped up to share their comments!

Absolutely fantastic discussion, I think you guys helped to flesh out the answer to a far more complete one than I could have done. 🙂

We shall see what Biden can achieve when he visits Saudi. The next 6 months will get interesting as Europe approaches winter again.

Indeed – the next 6 months will be crucial. Will give us much clearer information on how inflation is going to play out.

Dear FH,

Just a small comment. Maybe you can advise your reader to put aside say 6 months worth of their monthly household expense in safe & highly liquid things like Singapore saving bond to give them a peace of mind (Rainy day fund) especially they have small kiddo & elder parent to provide for. (Just in case the $200K that they mentioned to you are indeed all the cash they have now).

Agree with most of your other readers who comment that entering property market now may not be the best thing to do. “Buy high & sell high” is already bad enough, let alone in their current situation which is more or less, “buy high and dunno whether can or cannot sell higher in 3 years time/ find tenant who is willing to pay high rent”. Oh ya, still need to factor some $$$ to do at least some basic renovation + furnishing before they condo is in more presentable shape to fetch better rent.

Cheers

That’s a good point – thanks for raising this.

I suppose the mid term dilemma is that if indeed we are going into an inflationary decade, the money needs to be deployed at some point. Agree that now might not be the right time, but one needs to be careful not to play too defensive and hold too much cash for too long as well.

Like you said though – it’s really about striking the right balance, and things like having 6 months expenses set aside really help peace of mind. I might even go as far as to say 12 months expenses in cash/cash equivalents.

I think since the couple already have a HDB flat, buying another property will attract ABSD of 17 % or more if it is the 3rd property. If you factor in the ABSD the property option will definitely be much more risky.

The HDB flat is in the wife’s name (she bought when she was single) – which means for the husband it is his first property, and no ABSD. 🙂

Hi FH. Thanks again for another interesting article. I would just point out another small factor that doesn’t seem to be taken into account. If you withdraw $293,000 from CPF OA to finance a property purchase you are giving up $7,325 a year in guaranteed interest — even more if you could transfer that to SA — so there is an opportunity cost there.

I personally find the aim of $100,000 profit on a $200,000 investment in 3 years is extremely unrealistic in this environment. Just keeping capital intact may be a decent outcome!

That’s a good point, thanks for raising this!

I do agree on the $100k profit point. If one is able to revise expectations, there are much safer options in play.

If one does insist on hitting that target, then well, a certain level of risk must be taken.

Hi Horse,

Agree with Chan Mali Chan here. You usually give pretty good advice over the years but this recent post is very dangerous indeed. You should consider pulling it down or at least amending the post.

Hi Shohei,

Thanks, I understand where you’re coming from.

I’ve updated the article to better emphasise the risks of a real estate investment at this point in the cycle. And the reader in question has gone through the comments section, and is well aware of all the risks highlighted by the great community feedback!

Beyond financial considerations, one point that’s not been mentioned by the reader is the current situation with their residence.

Are they living with family and crave more privacy?

Are they living in a small place and crave more room?

That may be a powerful driver for considering to buy a second home.

True. Although for this particular reader it seems the objective is primarily investment driven.

Suspect they may be living with parents/inlaws given the kids situation, but I could be wrong here.

Thanks for raising this.

For many of us, the high stamp duties levied in Singapore on investment properties completely kill the idea (which is presumably what the government wants to achieve, in order to keep home prices affordable for young families). The thing is, having a pool of rental properties is also important because there are always going to be some transients in a dynamic economy like Singapore. I’m wondering if the government won’t be forced to rethink how they regulate the market so they can better balance the interests of home buyers and investors. Right now, it looks like they’ve put too many barriers in place for it to be attractive to many of us.

The only thing that still makes property investing attractive in Singapore today, is that it’s the only investment vehicle that provides access to a serious amount of leverage via a mortgage on the property. Margin loans to buy shares are a much riskier prospect, and not so many people are up for that.

Well for most couples with the option to, they can decouple and buy 1 property in each name, which means 2 properties per household. If they are willing to use their children’s name – potentially more.

That said, I agree with you that property offers good access to leverage. It’s one of the cheapest loans you can get out there, and without risk of margin call because property prices are not marked to market (unlike shares)! With very strong government intervention, it’s also unlikely the property market will plunge massively, but like you said, it also means that upside will be limited.

So yes – am inclined to agree that the main advantage of property, really is the leverage!

Timing is key…if the reader bough a new property last year…then the $100k paper gain may not be unrealistics (I myself did that). As one of the bro mentioned, withdrawing CPF will inccur opportunity cost…the property loan also incurred interest…3 years interest for a 1m property can be as high as 6 figures liao….moreover property is not liquid asset and there are selling cost and agent fees to consider…..at the end even if the overall market risen…the profits may be cut by all these nitties gritties. On the other hand, buying a blue chips at 4% to 5% div will be my preference, if the overall market is good, highly there will be capital gain….besides buying and selling stocks is more clear cut and relatively fast….the profits and div is tax free too and more importantly if market tank and the financial situation of the reader changed….cuting lost on stocks is easier than cutting lost on property :p

I think the key difference is that with the stocks you wont be able to access the same amount of leverage. Which I suppose, is both a good and a bad thing.

Margin or CFD account….but higher interest rate of course :p

Risk is very different though – you can’t get margin called on a mortgage, because property prices are not marked to market on a daily bais!