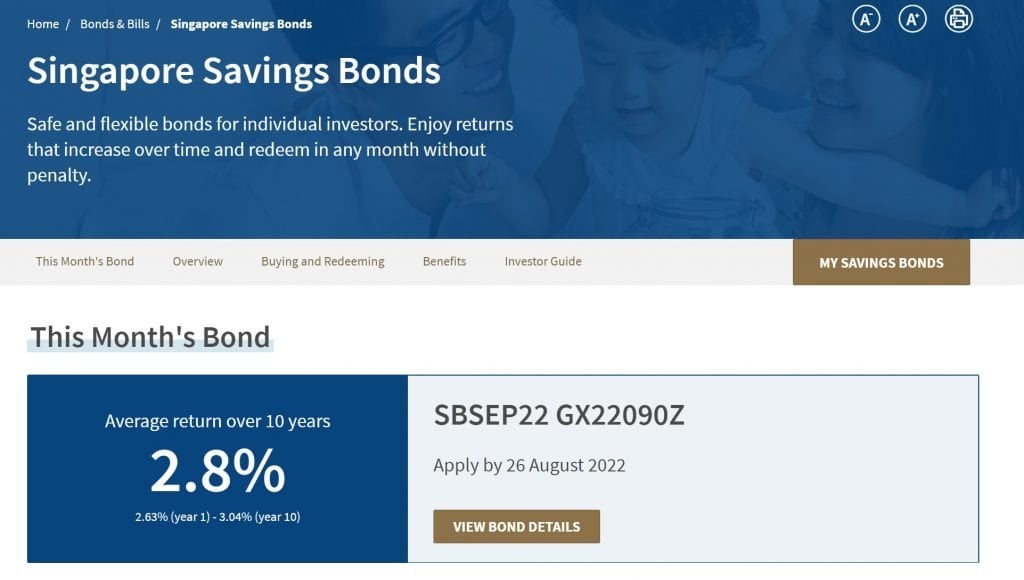

So the latest Singapore Savings Bonds yields are out, and they are really attractive.

I’ve set them out below, and they:

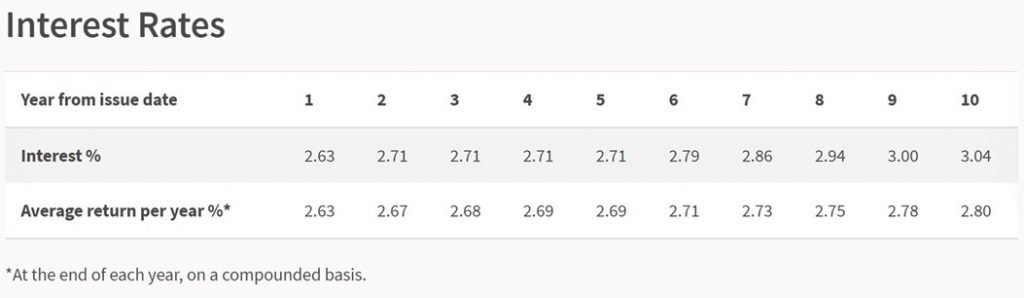

- Start at 2.63% for the 1st year

- Go up to 3.04% for the 10th year

If you are looking for a place to park your cash, this is probably the place to be.

Remember – Singapore Savings Bonds are:

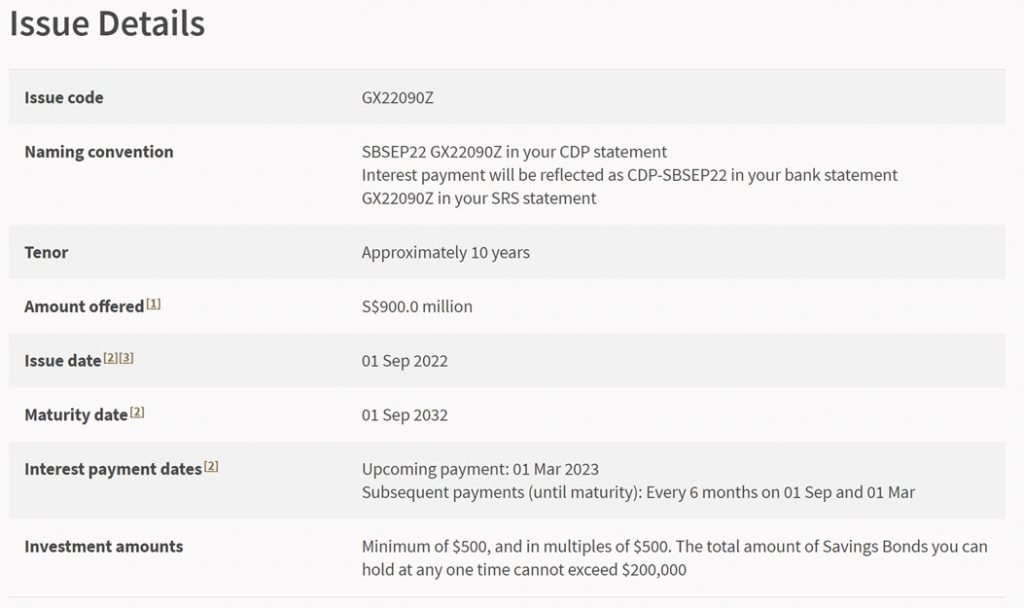

- Risk free – Backed by the Singapore Government

- Can be redeemed any time with accrued interest

- Each person can apply up to $200,000

- Can be held for up to 10 years

How much Allocation of Singapore Savings Bonds are you likely to get?

The problem of course, is that these Singapore Savings Bonds are really attractive.

And everybody knows that.

So everybody in Singapore is desperately applying for them.

Last month’s SSBs were heavily oversubscribed, to the point that each person only got $9,000 allocation.

Which is dismal to say the least.

This month, the offer size is slightly upsized at $900 million (vs last month’s $700 million).

But at the same time, the 1st year yield has jumped significantly from 2.0% (last month) to 2.63% (this month).

So if anything, this month’s Singapore Savings Bonds are going to be even hotter.

In which case you might be looking at an allocation of less than $9,000 per person.

What’s an investor to do in times like that?

Note: This was originally a Patreon article. Making it available given the widespread interest around Singapore Savings Bonds, T-Bills and Singapore Government Securities (SGS). Do support Financial Horse as a Patreon for more exclusive content like this.

SGS or T-Bills as an alternative to Singapore Savings Bonds?

First off – a bit of background.

The Singapore government issues bonds to investors.

Think US Treasuries, but for Singapore.

There are 2 types of bonds: (1) Singapore Government Securities (SGS), and (2) Treasury Bills (T-Bills)

A Singapore Government Bond with maturity of 2 – 30 years will be called an SGS Bond, while a Singapore Government Bond with a maturity of 1 year or less will be called a T-Bill.

There’s a very helpful table from Seedly below that sets out the difference between SGS, T-Bills and Singapore Savings Bonds:

|

|

Singapore Savings Bonds |

SGS Bonds |

Treasury Bills |

|

What is it? |

Safe and flexible bond option for investors |

Tradable government debt securities |

Short-term tradable government debt securities. |

|

How it works? |

Pays interest every 6 months. |

Pays a fixed couple every 6 months. |

Investors buy it at a discount. Upon maturity, investors will then receive the full face value of the bill. |

|

Investment duration |

10 years |

2, 5, 10, 15, 20, 30 years |

6 months or 1 year |

|

Minimum investment |

S$500 |

S$1,000 |

S$1,000 |

|

Maximum limit per investor |

S$200,000 |

No Limit |

No Limit |

|

Fees |

S$2 |

S$2 |

S$2 |

|

Payment of interest |

Once every 6 months |

Once every 6 months |

No interest |

|

How is the price and rate determined? |

The interest rate is fixed and published by Monetary Authority of Singapore (MAS) every month. |

Determined by auction |

Determined by auction |

|

How to apply? |

Apply through DBS/POSB, OCBC and UOB ATMs or internet banking |

Apply through DBS/POSB, OCBC and UOB ATMs or internet banking |

Apply through DBS/POSB, OCBC and UOB ATMs or internet banking |

|

How to redeem? |

Redeem the full principal with accrued interest through Online Bank or ATM. |

Return depends on market conditions when traded in the exchange |

Return depends on market conditions when traded in the exchange |

|

Can we invest using our SRS account? |

Investors can invest through their respective SRS Operator’s internet banking portal. |

Investors can invest through their respective SRS Operator’s internet banking portal. |

Investors can invest through their respective SRS Operator’s internet banking portal. |

|

Can we invest using our CPF? |

No |

CPFIS |

CPFIS |

|

Tax |

There is no capital gains tax in Singapore |

||

What is the advantage of SGS or T-Bills (vs Singapore Savings Bonds)

The main advantage of SGS or T-Bills, is that there is no limit to how much an investor can buy.

So if you want to buy $10 million worth of SGS or T-Bills, the world is your oyster.

This itself is probably the main advantage of SGS or T-Bills, especially for investors who have more than $200,000 cash.

What is the disadvantage of SGS or T-Bills (vs Singapore Savings Bonds)

But of course, there’s no free lunch in this world.

There are quite a few notable disadvantages:

- No early redemption

- Liquidity

- Potential for Capital Loss if not held to maturity

- Competitive Bidding process

No early redemption

Unlike Singapore Savings Bonds where you can redeem anytime to get back your full principle + accrued interest.

You cannot do the same with SGS or T-Bills.

If you want to exit your investment before maturity, the only way is to sell on the open market.

Which means that:

- You are subject to liquidity constraints on the market

- You are subject to the price on the open market

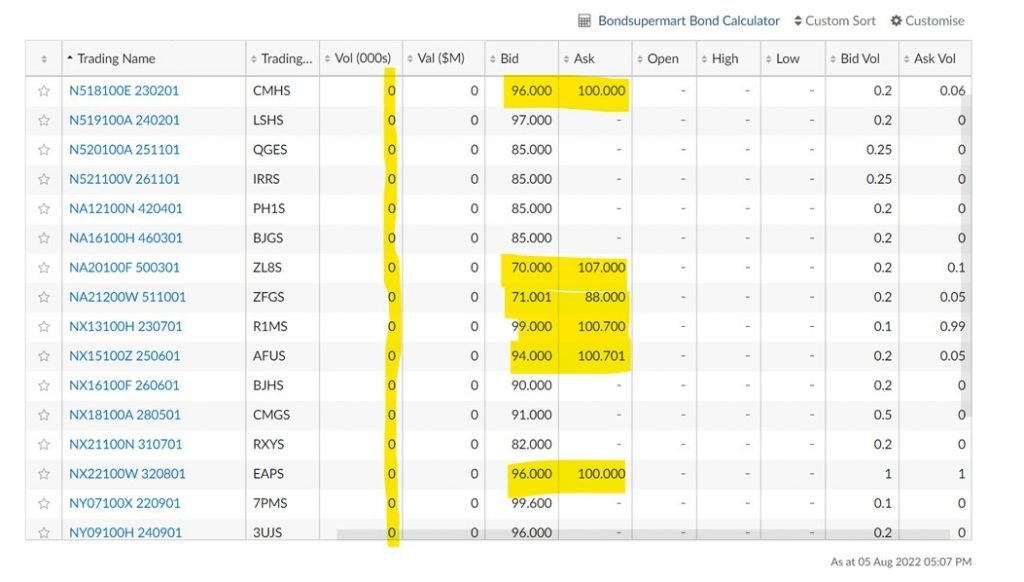

Liquidity

Imagine that you hold $10 million SGS, with 10 year maturity.

You need the cash back, so you try to sell $2 million of it.

But nobody wants to buy it from you on the open market, unless you sell it at a discount.

What are you gonna do?

That’s liquidity.

And it’s a very real problem.

You can take a look at the daily liquidity of SGS Bonds below.

Absolutely dismal.

Only SGS Bonds are Tradeable on the SGX

To further complicate matters, only SGS Bonds are tradeable on the SGX.

T-Bills on the other hand, are not tradeable on the SGX.

T-Bills can only be sold via a dealer bank (which is basically one of the 3 local banks).

This means that if you hold T-Bills, and you want to exit before the 6 month / 1 year maturity, you need to transfer the T-Bills from your CDP to DBS/OCBC/UOB, for them to sell it for you.

And spoiler alert – the liquidity for T-Bills is very poor.

Long story short if you’re buying T-Bills, you’re better off just saving yourself the hassle and holding them to maturity.

Won’t be more than a year anyway.

Potential for Capital Loss if not held to maturity

And of course, if you want to sell SGS on the open market – you’re at the mercy of market prices.

Which means that if interest rates go up, and your SGS Bonds are trading at a discount, you may not be able to exit them without taking capital loss.

So this inability to redeem directly from the government, and only being to sell on the open market, is a very key difference vs Singapore Savings Bonds.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Competitive Bidding process

And finally – SGS and T-Bills are bought via a competitive bidding process.

This means that at auction stage, you don’t actually know the exact yield you will get.

You’ll only know once the results are out.

You can estimate the yield based roughly on the latest market yields, but you won’t know the exact yield until the results are out.

Sidenote that when you apply you also have a choice between competitive and non-competitive bidding.

Competitive bidding allows you to fix a price you want to buy at, while non-competitive bidding basically buys at the market price it settles at.

In stock terms – think limit order vs market order.

Is it worth buying SGS or T-Bills?

It is clear from the above that SGS and T-Bills are very different from Singapore Savings Bonds.

Sure, they are risk free, but their inability to redeem early make them a very different instrument from Singapore Savings Bonds.

These are more sophisticated instruments, that are actually designed more for institutional investors or more sophisticated retail investors.

My simple view on the T-Bills is that if you buy them, you must be prepared to hold them to maturity. There is no easy way to exit T-Bills before the maturity.

As for SGS Bonds – if you plan to exit before maturity, do understand that you are subject to market liquidity and prices. If interest rates go down you could make capital gains, but if interest rates go up you could make capital losses as well.

This is important to note.

But if you are aware of the risks and prepared to hold to maturity– then both the SGS or T-Bills have no application limit, and could be pretty attractive.

You can buy as much as you want, without ridiculous $9,000 limits on the Singapore Savings Bonds.

What am I doing?

For me personally, I really want the liquidity.

I think the liquidity is king in this market.

So while I will be applying for Singapore Savings Bonds every month going forward, I don’t see myself applying for SGS or T-Bills for now.

Could change in the future though – let’s see!

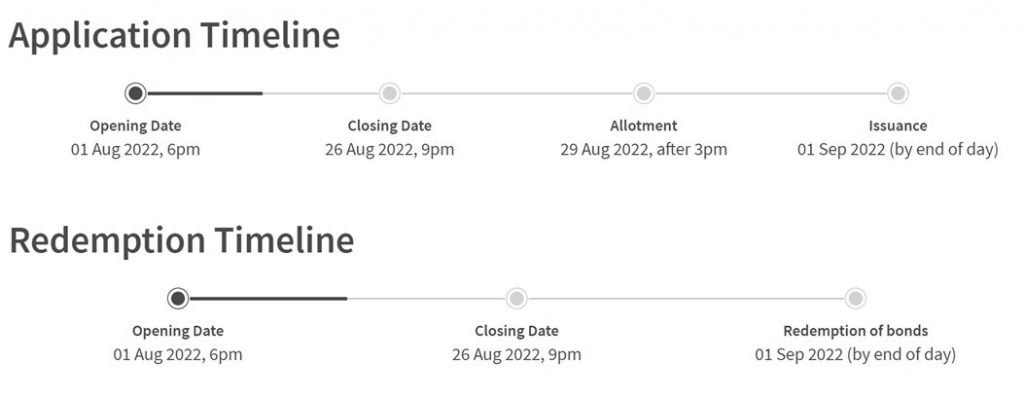

Singapore Savings Bond Timelines

Whatever the case, timelines for the Singapore Savings Bonds below.

If you’re keen, don’t forget to apply before 9pm on 26 August 2022!

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try .

With central banks raising interest rates across the globe are we likely to see a 3% (year 1) SSB? Are there chances that we may see an average of a 5% SSB?

That’s a surprisingly tough question to answer because the SSB curve is smoothed out – the short end cannot be higher than the long end. So one needs to know both the short and long term interest rates to answer this question, which is no easy ask.

Personal view (and I could be wrong) – yes we may see 3% 1 year by end of the year or early next year. But no we will not see 5% SSB this cycle.

Dear Financial Horse,

Great article as alsways.

Like to bring a small pointer to your attention. I think the minimum age our Singapore Children need to be before we can buy Singapore Saving bond in their name is after they reach 18years old.

Thanks for the heads up! 🙂