When interest rates are going up, like they are right now, it is natural for investors to expect that interest rates will go up (and stay up) forever.

But I do want to caution against such thinking.

The way I see it, there is a real risk of economic growth surprising to the downside the next 12 months.

And the way things are set up, I think the next big move in interest rates is more likely to be down than up.

If you’re rolling most of your cash in 6 month T-Bills, there could be a real risk that in the next 1 – 2 years, you’re going to be rolling them over into a very different interest rate climate.

So I think this is a good time to start thinking about how to lock in current interest rates for longer, and Singapore Savings Bonds is one solution.

2 questions I wanted to address in today’s article:

- Are Singapore Savings Bonds a good buy?

- Should you buy Singapore Savings Bonds now or wait for higher yields?

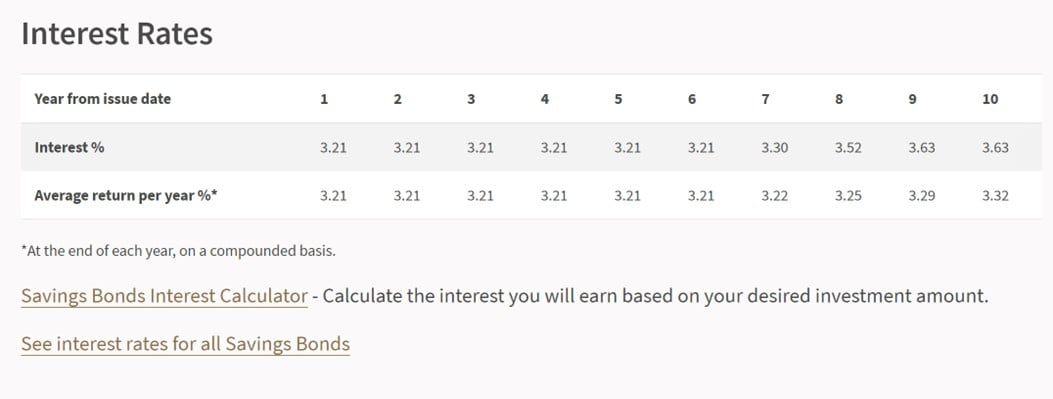

Are Singapore Savings Bonds a good buy? – Singapore Savings Bonds pay up to 3.63% yield

In case you missed it – this month’s Singapore Savings Bonds are actually pretty attractive.

You’re looking at:

- 3.21% for the first 6 years

- Stepping up to as high as 3.63% for the 10th year

And an average yield of 3.32% over 10 years.

What are the alternatives out there – for investors looking for yield?

Let’s sum up the alternatives out there right now:

|

Instrument |

Risk Level |

Yield |

|

6-month T-Bills |

No risk |

3.87% |

|

10 year Singapore Bond |

No risk |

3.41% |

|

REITs (CICT or Ascendas REIT) |

Low – Medium |

6.2% |

|

US 2 year T-Bills |

No risk (USD FX risk) |

5.14% |

|

US 10 year Treasuries |

No risk (USD FX risk) |

4.93% (note withholding tax treatment) |

Now Items 3 – 5 are a bit more complex because they carry risk of capital loss if you don’t know what you’re doing.

So we’ll discuss those in further detail in another article.

The main comparison is vs Items 1 and 2.

Singapore Savings Bonds compared vs T-Bills?

The main risk 6-month T-Bills carry is refinancing risk.

Yes the 3.87% risk is higher than SSBs at 3.21% – but you really don’t know where interest rates will be in 6 – 12 months time.

This is huge, and I think investors are underestimating this.

Singapore Savings Bonds compared vs 10 year SGS Bonds?

The main risk 10 year SGS Bonds carry – is the fact that these bonds only mature 10 years later.

10 years is a very long time.

If you decide you want the money before 10 years, the only way out is to sell the bonds on the open market.

Where the price depends on where interest rates are.

I would say 10 year SGS Bonds are good if you want to make a bet on interest rates going down.

But if you are just looking to collect the yield it’s not so great.

Singapore Savings Bonds lock in decent yield for 10 years, with no risk of capital loss

Viewed this way, the Singapore Savings Bonds is kind of a cash-bond hybrid.

It allows you to lock in decent interest rates for the next 10 years.

And unlike long duration bonds, there is zero risk of capital loss even if you want to exit before maturity.

If interest rates go up, you can just redeem the SSBs any time and get your full principal back with accrued interest.

For investors who want to lock in yields, and don’t want to bet on interest rate movements, I think they are a good option.

Should you buy Singapore Savings Bonds now or wait for higher yields?

Now the second question – should you buy SSBs now or wait for higher yields?

There’s really 2 parts to this question:

- Will SSB yields go even higher next month(s)?

- Will you get full allotment for SSBs?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Will SSB yields go even higher next month(s)?

Singapore Savings Bonds yields track the average yield 10 year Singapore government security for the previous month.

The average yield on the 10 year SGS this month so far, is about 3.3 – 3.5%.

Put that together, and you might see next month’s Singapore Savings Bonds offer around:

- 3.4% for 10 years

- 3.3% for first 5 years or so

Compared to the latest Singapore Savings Bonds – it’s definitely slightly better.

But it’s only marginally better.

So we’ll want to look at point 2 as well – whether you will get full allotment.

Will you get full allotment for SSBs?

The next point to think about is allotment.

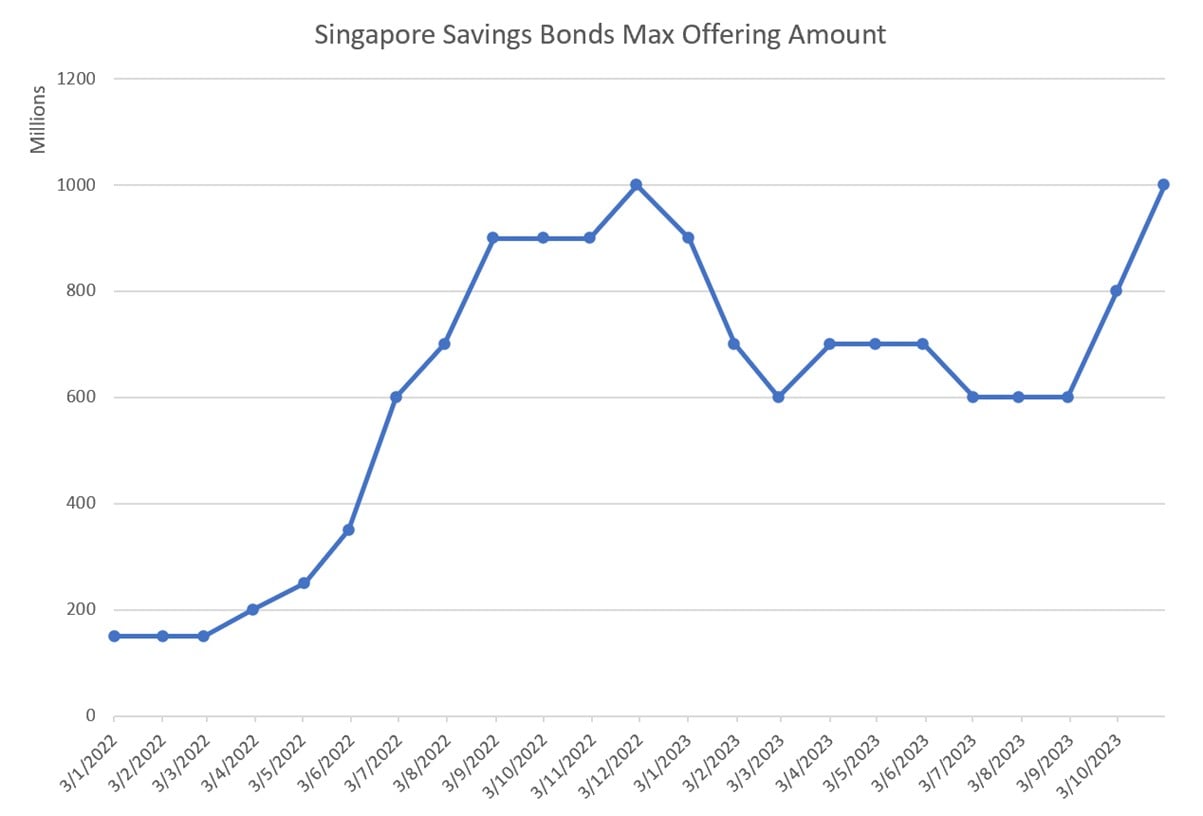

I’ve charted out the SSBs allotment limit since Jan 2022 below.

You can see how in 2H 2022, demand for SSBs was very hot, to the point where you were looking at only $10,000 – $15,000 allotment each month.

If this repeats, it could take a long time for you to get a meaningful allotment.

How likely is this?

Will Singapore Savings Bonds Allotment Limit stay at $200,000 the next few auctions?

Looking at the numbers.

The amount of SSBs available each month has gone up significantly, standing at $1 billion this auction (vs $600 million just 2 months ago).

That’s a huge increase in supply of Singapore Savings Bonds:

At the same time, demand has definitely gone up since the middle of the year.

But in the grander scheme of things – demand for SSBs is still well below 2022 highs.

In 2022 we saw as high as $2.4 billion demand, while for the most recent auctions we’re only in the $600 million range.

Note that institutional investors cannot apply for Singapore Savings Bonds – so this demand is purely retail investors.

Here’s Singapore Savings Bonds application amount less the max offering amount.

It has gone negative for much of 2023, which shows demand is less than the offered amount (hence full allotments for every month).

So… full allotment for Singapore Savings Bonds again?

Based on the above, I *think* you’ll see full allotment of SSBs for the next one or two auctions again.

So if you wanted to subscribe the full $200,000 at one go, you *probably* still can do it.

So given that yields on Singapore Savings Bonds will probably go up next month, and given that you can probably still get full allotment the next one or two auction.

I think if you really want to maximise it you could probably wait a month or two first before applying.

But do note liquidity issues for Singapore Savings Bonds

But do note that the cash is deducted from your account when you apply for Singapore Savings Bonds.

So if you are redeeming existing SSBs to buy new one, you must have the cash in your account to buy the new SSBs (as the cash from the existing SSBs won’t be in until the next month).

This could be a factor to think about – that favours staggering the purchases over a few months instead of all at one go.

What will I do – Apply for Singapore Savings Bonds or skip?

I have a bunch of Singapore Savings Bonds yielding 2.9ish% in the first year that I’ll probably look to refresh to the higher yields.

I’ll probably look to redeem about half of them this month to subscribe for the latest Singapore Savings Bonds.

And perhaps refresh the rest of them the following month(s).

But again, that’s just me, and there’s no right or wrong here.

Singapore Savings Bonds Application Timeline (26 Oct 2023)

If you’re interested to apply for the Singapore Savings Bonds.

Application deadline is 9pm on 26 October 2023.

Same timing for both applications and redemptions of Singapore Savings Bonds.

– Get up to USD 2000 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 2000 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Hi FH,

“If interest rates go up, you can just redeem the SSBs any time and get your full principal back with no accrued interest.” -> i think accrued interest will be payable? Source: https://www.mas.gov.sg/bonds-and-bills/investing-in-singapore-savings-bonds/how-to-redeem

Also, suggest to use srs to buy ssb to lock in decent interest rates (almost 1% higher than cpf oa already) for 10 years as a low risk way to build that nest egg + reduce taxable income.

Thanks!

My bad! Meant to say with accrued interest, have corrected it.

Interesting tip on SRS. I actually use srs to buy stocks / reits since they are locked up long term, so I might as well take the chance to go for higher capital gains.