Interest rates on bank savings accounts are horrible these days.

Almost every week, we hear a new bank is cutting interest rates on their flagship account.

I’ve summarized the latest rates below (assuming average spending) – and you can see how hard it is to even hit 1.0%.

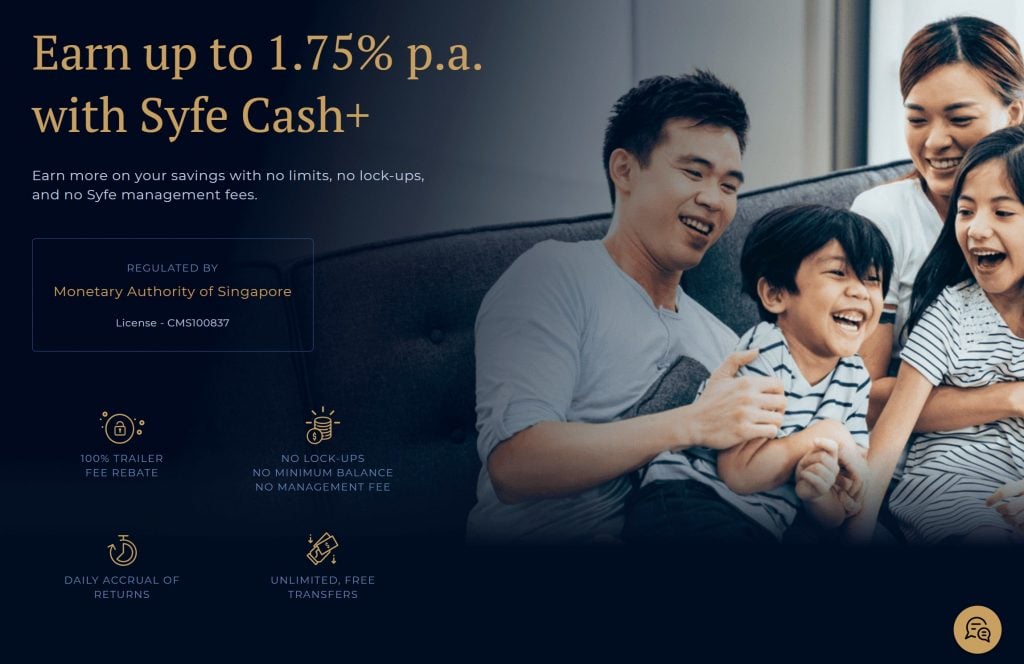

So when Syfe Cash+ launched with a 1.5% yield on cash, it really got me interested.

Basics: What is Syfe Cash+

Long story short, Syfe Cash+ is a money market fund, similar to StashAway Simple and EndowUs Cash Smart.

The key features to note are:

- 1.75% yield per annum (projected)

- Not SDIC insured – NOT risk free

- No lockups (but 2-4 working days to process credit/withdrawal)

- No minimum amount (and no maximum)

- No management fee

1.5% yield per annum (projected)

There used to be a time when Singapore Savings bonds yielded a good return (2%+).

Well, that time is long gone now.

The latest 1-year rates are at 0.32% which is a complete joke.

To earn a good return on your liquid cash today, there are 2 main options:

- Savings Account

- Money Market Funds

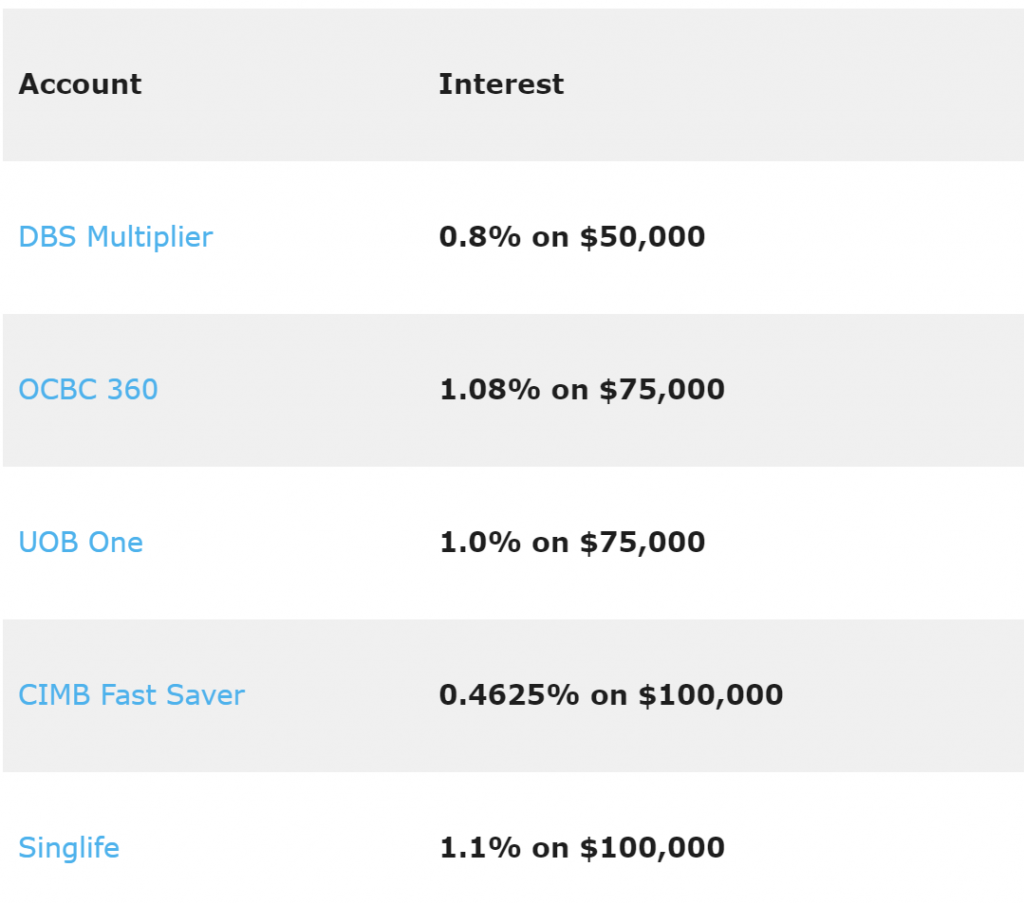

Savings Accounts

Savings Accounts are things like DBS Multiplier and OCBC 360.

The main advantage with Savings Accounts, is that they are SDIC insured.

This means that any amount you put in up to $100,000 is completely risk free. But of course, you get a lower yield for such accounts.

I’ve set out the latest rates below assuming:

- Salary credit

- At least 2 of:

- Credit card spend

- Home loan

- Insurance/investment

| Account | Interest | Remarks |

| 0.8% on $50,000 | ||

| 1.08% on $75,000 | ||

| 1.0% on $75,000 | ||

| 0.4625% on $100,000 | 0.3% after $100,000 | |

| 1.1% on $100,000 | On waitlist now (2% for first $10,000) |

Not super attractive.

The highest you can get is Singlife at 1.1% on $100,000, but they no longer accept new applications (waitlist only).

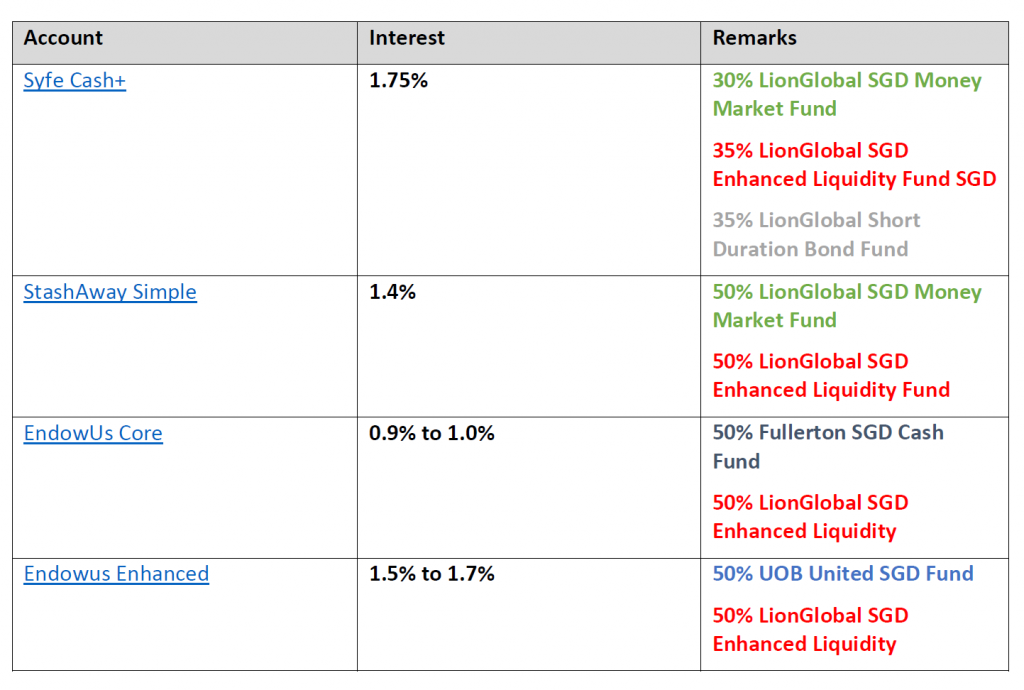

Money Market Funds

Enter the Money Market Funds like Syfe Cash+.

The rates they provide are set out below, which are waaaaaay higher than savings accounts.

| Account | Interest |

| 1.5% | |

| 1.2% | |

| 0.8% to 0.9% | |

| 1.2% to 1.4% |

How stable is the yield of Syfe Cash+?

What you do need to know though, is that this is not like putting your money in a bank.

What Syfe Cash+ does, is to take your money, and invest them in money market funds. If there is a loss in the underlying fund, or if the actual returns deviate from the projected rates, that’s your problem.

Syfe Cash+ (or StashAway or EndowUs) will not guarantee your yield.

So this is not like a bank where they take your money, and they promise to pay you a fixed yield for the next year.

To give an example, StashAway Simple launched in Nov 2019 with a projected 1.9% yield, but in Aug 2020 that yield was revised down to 1.4%.

So these yields are not fixed in stone.

BTW – we share commentary on the COVID crisis every weekend, so please sign up for our mailing list, its absolutely free.

It’s a weekly newsletter that goes out every Sunday, and rounds up the week’s posts so you never miss anything.

Don’t forget also to join our Telegram Channel!

[mailmunch-form id=”928667″]

Not SDIC Insured (NOT Risk free)

The biggest point you need to know about Syfe Cash+, is that it is NOT Risk Free.

This is NOT like a DBS account, where all amounts below $75,000 are SDIC insured, and you will not lose your $75,000 even if DBS goes bankrupt.

There’s no such protection for Syfe Cash+.

If the underlying funds go bankrupt, you will suffer capital loss.

How risky are the underlying funds for Syfe Cash+?

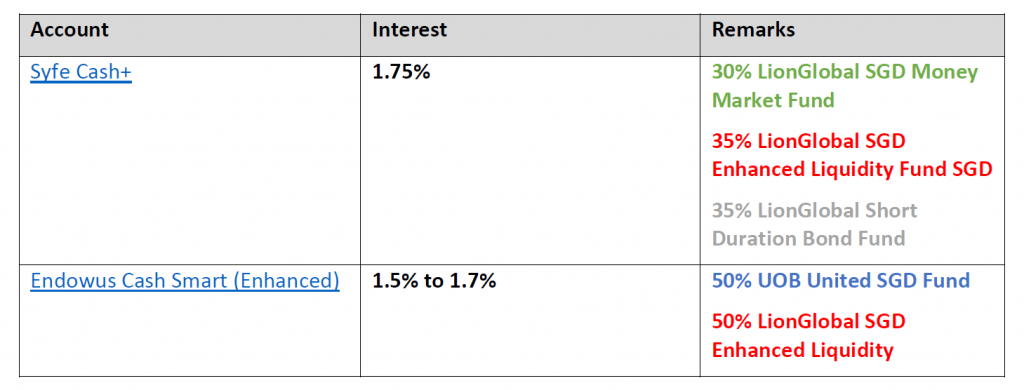

I’ve set out the funds used by Syfe Cash+, compared against StashAway Simple and EndowUs Cash Smart. It’s colour coded for easy viewing (same underlying funds).

Let’s dig into the 3 funds that Syfe Cash+ uses:

- LionGlobal SGD Money Market Fund (30%)

- LionGlobal SGD Enhanced Liquidity Fund SGD (35%)

- LionGlobal Short Duration Bond Fund (35%)

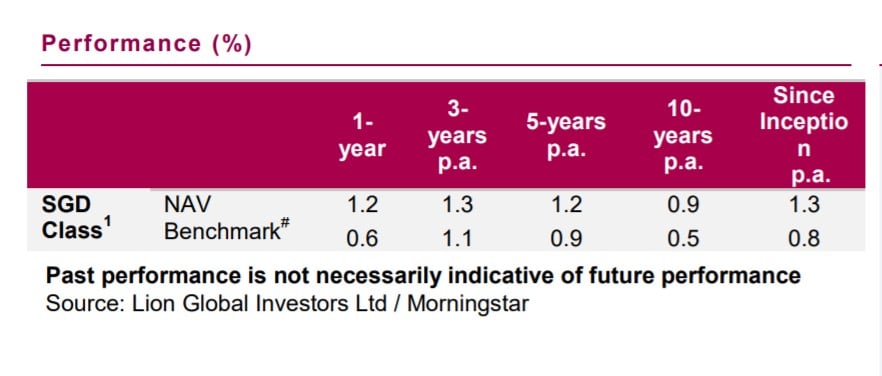

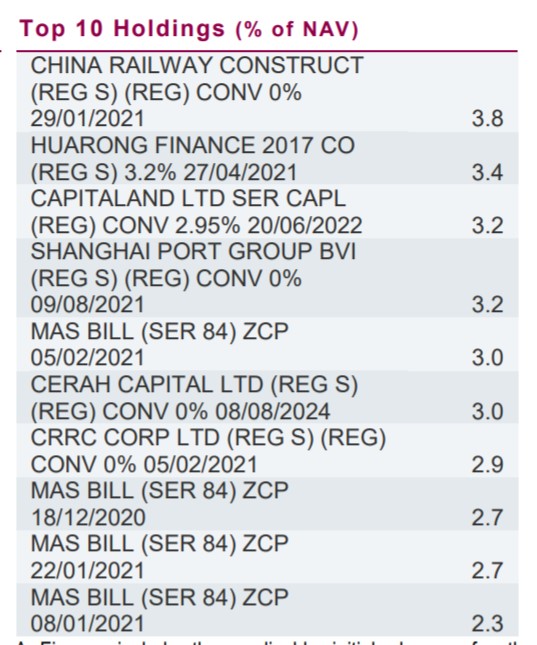

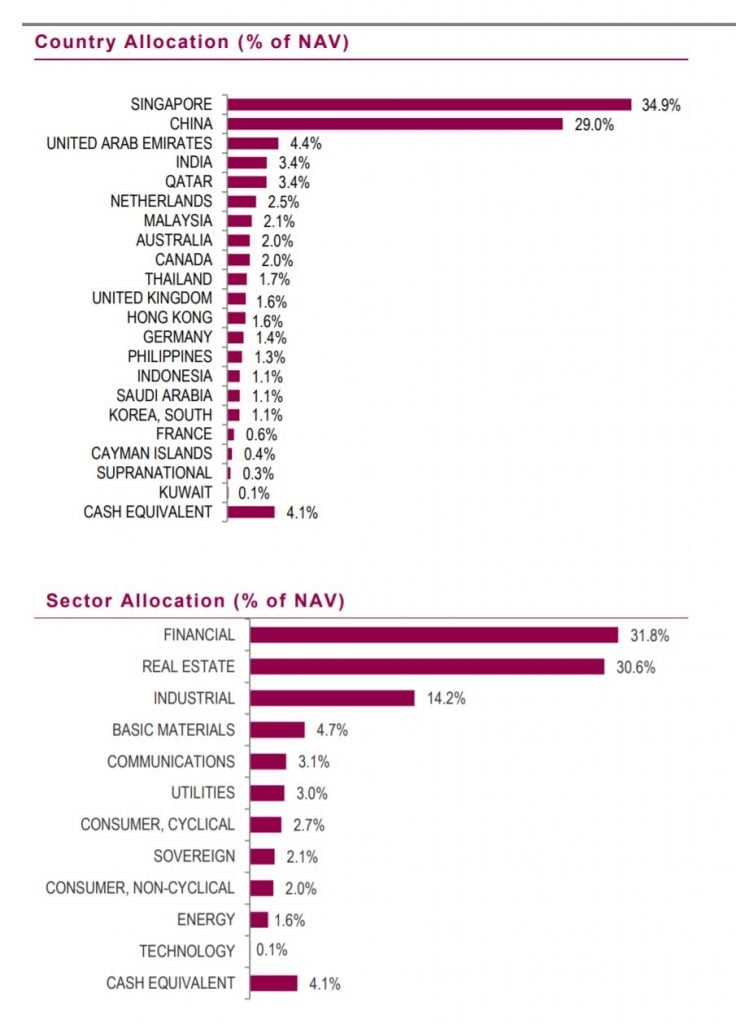

LionGlobal SGD Money Market Fund (30%)

This Fund:

will invest in high quality short-term money market instruments and debt securities. Some of the investments may include government and corporate bonds, commercial bills and deposits with financial institutions.

I’ve set out the relevant tables below below. To sum up:

- Average 5 year performance is 1.2%

- Biggest allocation is Singapore followed by China

- Biggest allocation is Financial, Industrial and Real Estate

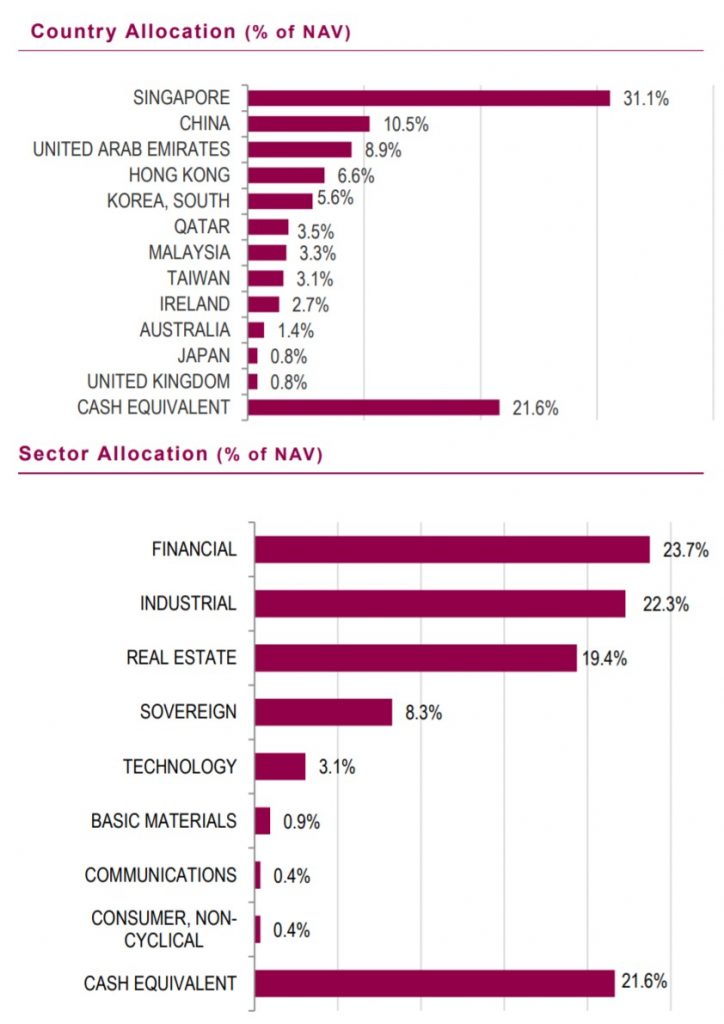

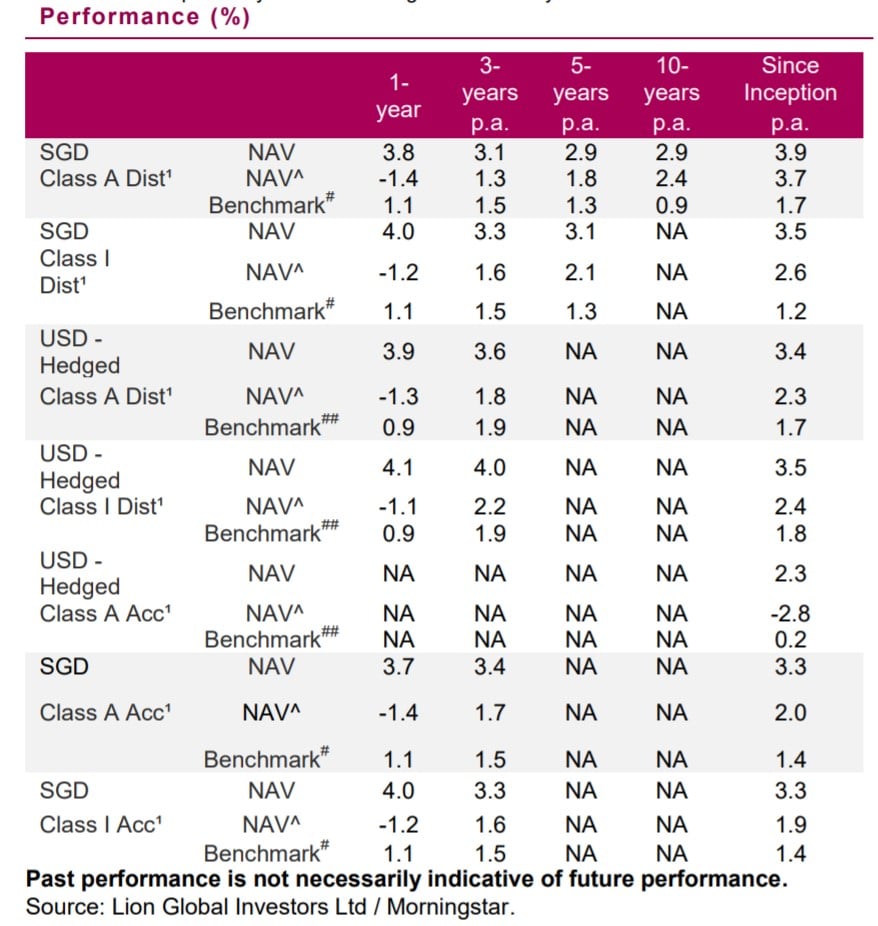

LionGlobal SGD Enhanced Liquidity Fund SGD (35%)

This Fund invests:

in a broadly diversified portfolio of high quality debt instruments. The Fund’s approach to enhancing income while providing liquidity is to invest in a high quality portfolio of debt instruments diversified across varying issuers and tenures while maintaining a weighted average portfolio credit rating of A- and a weighted average duration of around 12 months.

To sum up:

- Average performance since inception is 1.8%

- Largest allocation is Singapore followed by China

- Largest allocations are governments, real estate, industrial and financials

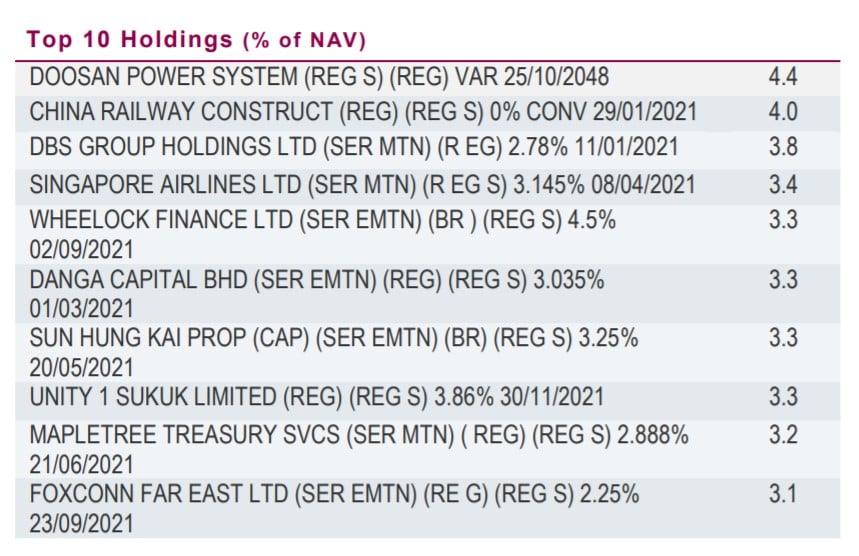

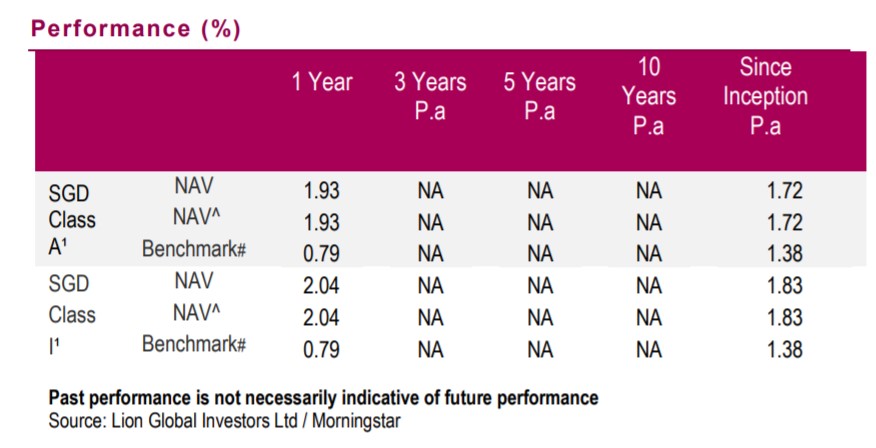

LionGlobal Short Duration Bond Fund (35%)

This fund invests in:

actively managed portfolio of Singapore and international bonds, high quality interest rate securities and other related securities. There is no target industry or sector. For the avoidance of doubt, while we will generally invest in bonds with investment grade quality, we may nonetheless also invest or expose the Fund to sub-investment grade securities.

To sum up:

- They can invest in sub-investment grade securities – this one’s a bit of a red flag for me

- Average 5 year return is 2.9%

- Biggest allocation is Singapore then China

- Biggest allocation is Financial and Real Estate

Hey FH, what does this all mean?

This is quite technical I know, so let me summarise.

Basically, Syfe REIT+ uses 3 funds with increasing levels of risk (arranged from lowest to highest risk):

- LionGlobal SGD Money Market Fund (30%)

- LionGlobal SGD Enhanced Liquidity Fund SGD (35%)

- LionGlobal Short Duration Bond Fund (35%)

The lower risk funds have a lower return, and the higher risk funds have a higher return.

Blend them together, and it gets you a 1.75% projected interest rate going forward.

But as we have seen, these funds invest in all kinds of underlying instruments, including:

- Bonds

- Commercial Paper

- Fixed income securities

- Bank deposits

If one of the underlying investments default, there is real risk here.

How safe is Syfe Cash+?

Which brings us to the million dollar question – how safe is Syfe Cash+?

This is what EndowUs says about their Enhanced product:

We combine the best performing money market fund and short duration fund from the biggest SGD money managers to give your cash a boost in yield. Advised for cash needs >1 month away for extremely rare periods of negative performance.

And I think my personal view here is very similar.

Objectively speaking, these are very low risk investments.

It will take something like Lehman in 2008 or a repeat of March 2020 to put these funds at risk.

In 2008 – the commercial paper market froze because of the subprime crisis, and there was a point where even these ultra-safe money market funds were at risk of going under. Fortunately, the Feds stepped in with their bailouts and unfroze the markets.

Investors in money market funds didn’t suffer any loss, but there was a short period of a few weeks where liquidity stress went nuts, and you couldn’t withdraw your money from these funds without taking a loss.

Lesson here – If 2008 or March 2020 happens again, all bets are off.

But historically speaking, most of the volatility is short term.

So if you can afford to hold on until the volatility passes, usually there is no capital loss.

Think about it this way – with the kind of assets these money market funds hold (government bonds, short term corporate debt from AAA issuers etc), if there is capital loss, it means that very very bad things are happening to the global economy. In such a scenario, your stocks are probably down 30% or more anyway.

So personal view – while they are low risk, these are most definitely NOT ZERO risk. In rare periods of market volatility you may need to leave the money in there for a month or two for volatility to fade. And there is a tail risk of capital loss.

Long story short – If you want zero risk use a savings account but accept the lower yield. If you want a higher yield, you need to decide if you are comfortable with the risk.

There’s no free lunch in this world.

No lockups (but 2-4 working day to process)

There is no lock up period.

You can withdraw your money anytime, which makes this superior to endowment plans or fixed deposits.

Do note that it takes about 2 – 4 working days to process any credit or withdrawal though.

Same story with EndowUs Cash Smart and StashAway Simple, so this isn’t unique to Syfe Cash+. This is because the money is parked with the fund manager, which takes some time to process it.

No minimum amount (or maximum)

Whether you have $1000 or $10 million, Syfe Cash+ still works.

No management fee (trailer fee rebate)

Syfe Cash+ will give you trailer fee rebates.

All this means is that the fund will pay Syfe a “referral fee”, and Syfe will refund this fee to you.

In practice, this means a higher yield, which is great stuff.

Similar to StashAway Simple and EndowUs Cash Smart.

Syfe Cash+ vs EndowUs Cash Smart (Enhanced)

A big question I had was how does Syfe Cash+ stack up against EndowUs Cash Smart (Enhanced).

Both offer very similar yields.

EndowUs uses UOB United SGD Fund

The big difference is that Syfe Cash+ drops UOB United SGD Fund, and uses a mix of LionGlobal SGD Money Market Fund and Liong Global Short Duration Bond Fund.

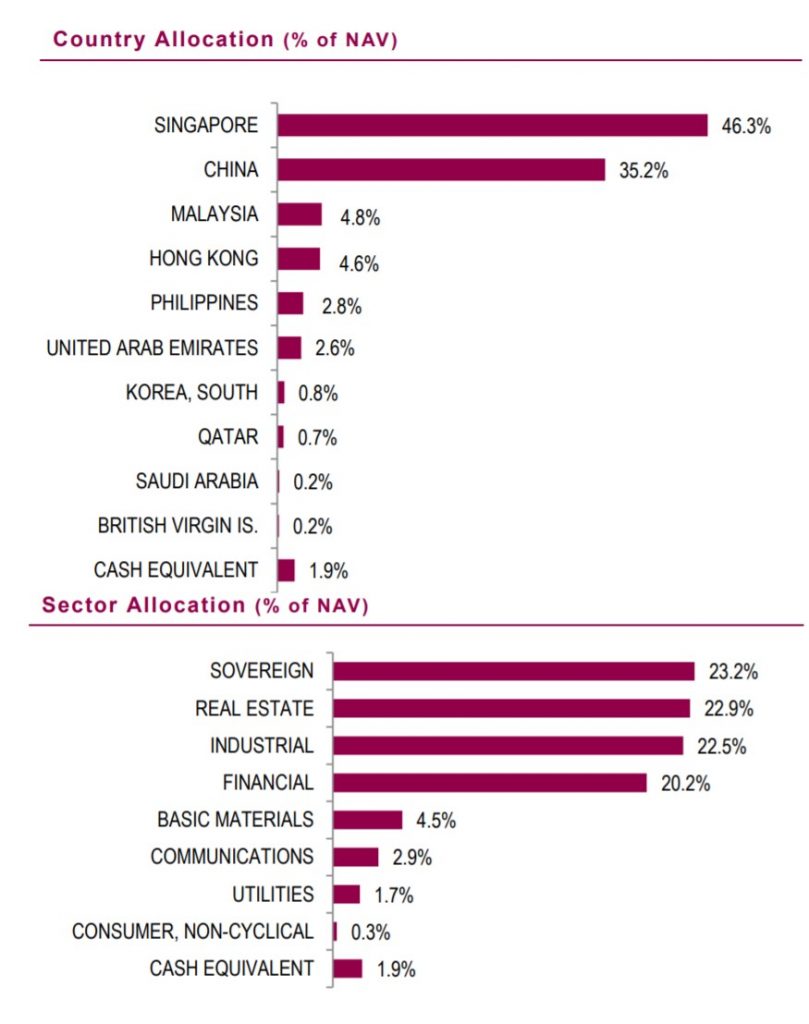

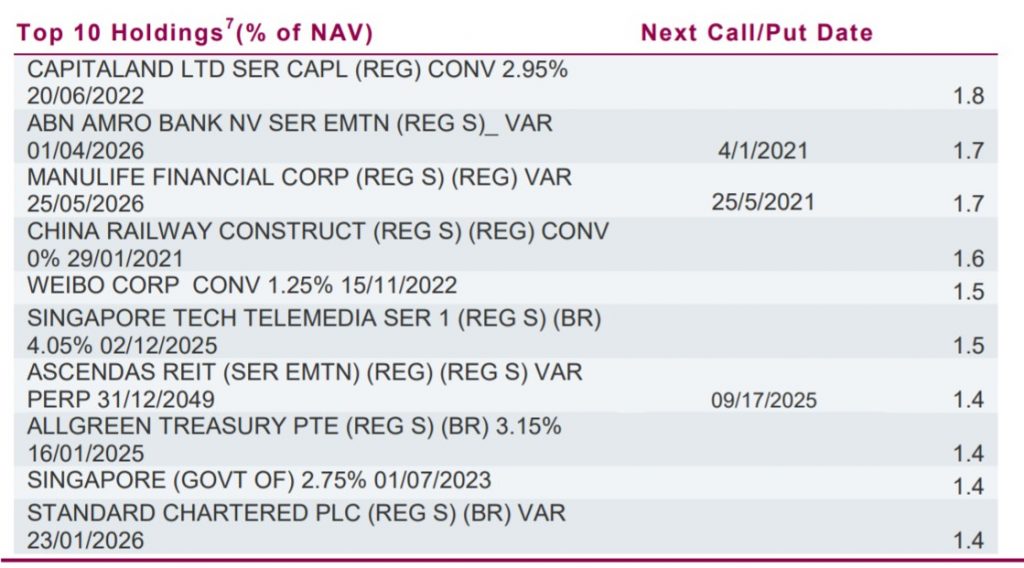

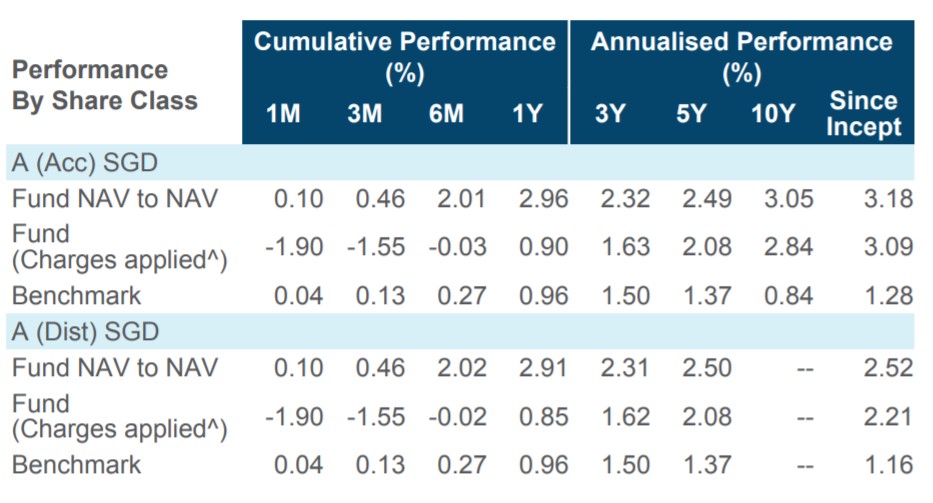

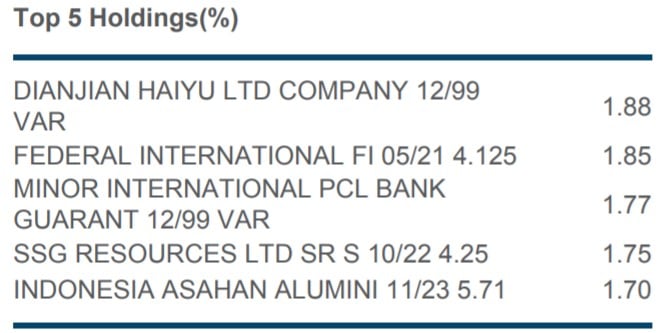

So I took a deeper dive into UOB United SGD Fund:

The investment focus of the Fund is to invest substantially all its assets in money market and short term interest bearing debt instruments and bank deposits with the objective of achieving a yield enhancement over Singapore dollar deposits

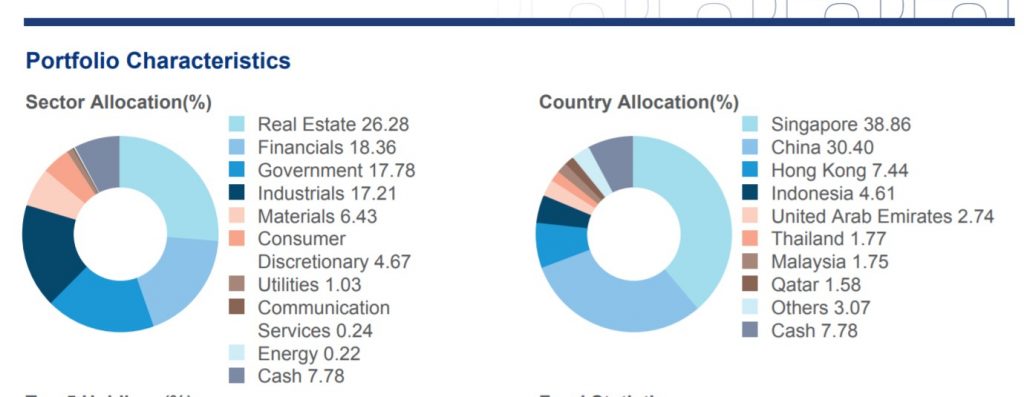

- 5 year return is 2.49%

- Country allocation is Singapore then China

- Sector allocation is real estate then financial

The main difference is that:

- The fund has been around longer

- The market cap is significantly bigger at $2 billion (vs $300 to $600m for the others)

- Fees are higher

Really, really tough to say which one is better, especially since the fund Syfe Cash+ uses has a shorter track record.

Gun to my head, I may just favour UOB United SGD Fund for the fund size – but I think it’s really close. You could just split your funds among both and be done with it.

No free lunch in this world

I think the biggest takeaway is that there is no free lunch in this world.

Fed Funds rate are at 0%, so the value of money has dropped all around the world.

If you want zero risk, go with the savings account, and accept the 1% yield.

If you want a higher yield, options like Syfe Cash+ are worth considering, but you do need to accept that there is risk here.

Would I invest?

Yes I probably will.

I have a bunch of cash stuck in CIMB Fastsaver now. After the rate cuts, it only yields about 0.4625%, which just seems silly to me.

I’ll probably transfer a portion of that out into either Syfe Cash+ or EndowUs Cash Smart Enhanced.

I might just put it in both to test out both platforms (and update this review).

But again – these things are NOT RISK FREE. There is a small chance things can go really bad, which results in capital loss. That’s a risk you need to be comfortable with, as do I.

I may think of these funds as having a 1 – 2 month lockup, for the periods of rare volatility.

For those who are keen, we have referral codes for Syfe Cash+, Endowus Cash Smart, and StashAway Simple below:

Syfe Cash+ Promo Code / Referral Link

Use code “FINANCIALHORSE” to enjoy Syfe Wealth: Zero management fees for 3 months; Syfe Trade: Additional S$10 bonus on top of existing promotions when users make their first trade

There are no Syfe management fees for Cash+, but this will apply if you decide to test out their other portfolios – so you might as well use it.

Endowus Promo Code / Referral Link

When you create your account from this promo code / referral link, you will get S$10,000 managed free for 6 months ($20 equivalent).

Referral Link: https://endowus.com/r?code=FH_XOKU9GZMTJ

StashAway Promo Code / Referral Link

Sign up with this promo code / referral link, and you will get 50% fees for the first SGD 50,000 invested for 6 months (you’re paying $187.5 on $50,000 for 6 months, so the 50% waiver works out to $93.75).

Referral Link: https://www.stashaway.sg/ref/financial-horse-BwENAQUNCQ8IBAYEBAcNCw

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

CIMB Fast Saver is cutting their rate in Jan 15, so effective rate for a deposit of $100k will be 0.3%

Thanks for raising this! 🙂

I notice that Syfe cash after rebates charges a mere 0.05%. Endowus cash products are higher, from 0.2+ to 0.3+. I am just wondering why the bigger difference here and since Endowus promotes alot on their 100% rebates?

That’s a good question. I will see if I can check with Endowus on this point. 🙂

I checked – the access fees at 0.05% for Endowus. The 0.2% to 0.3% fees are fund level fees, so no way around that. Those fees are alrerady net of the rebates.

Hi, Please kindly confirm if the Principal remains “unaffected” ? Is it only the “interest” that may not be 1.75% as advertised ?

The principal will be affected if the underlying funds suffer a loss. It’s a low risk event, but not impossible.

Sad to say, Endowus Enhanced returns have been lowered to 1.4-1.6% instead.

Oh dear. Thanks for raising this though.

This is correct but still doesn’t match up. If you take a look here https://www.syfe.com/cash-plus-portfolio-details, the fine level fee is at a 0.35% but the rebates (100% trailer rebate) is rather striking at 0.3, bringing the overall fees at a mere 0.05% compared to Endowus 0.2-0.3%, a 4-6X difference though it’s a small% . Just curious why is it that Syfe is able to generate a higher rebate!

I believe the funds that Syfe uses charge lower fees. As I recall – the fees for the UOB fund that Endowus uses is about 0.6%.