Happy new year to all FH Readers!

I’ve been getting quite a few questions on why REIT prices have been on a roller coaster ride recently.

After a huge rally since late October, REIT prices have been on a downtrend since the start of the year.

What’s driving this move?

And with rate cuts all but confirmed in 2024 – what are the top REITs I would look to buy this year?

Lots to cover, so let’s dive in.

Why are REIT prices dropping again?

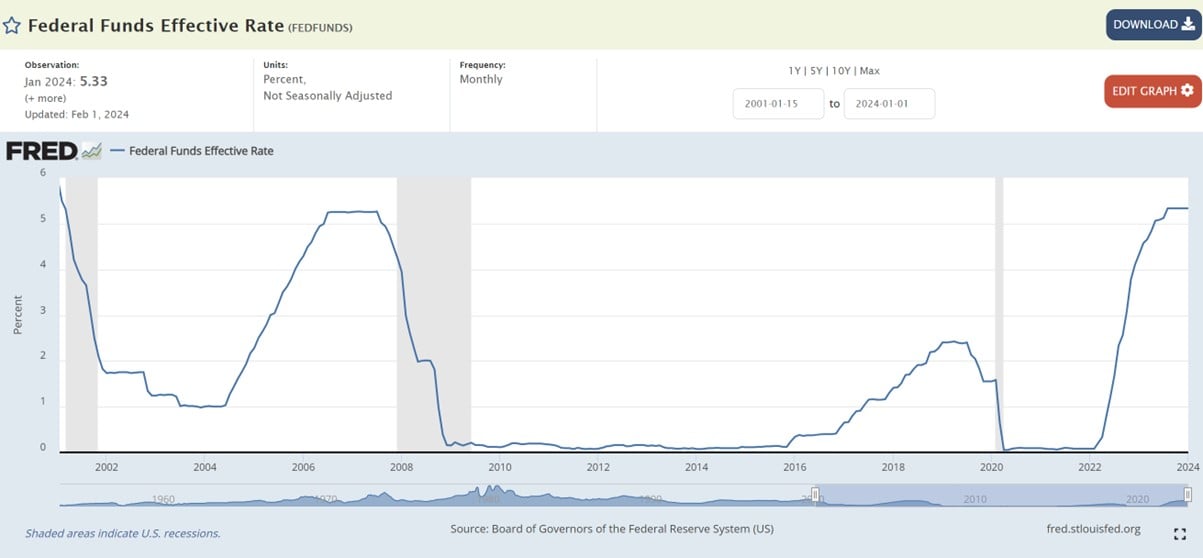

From a macro perspective, I would say the biggest factor is long term interest rates.

Higher Long Term Interest Rates pressuring REIT prices

I’ve plotted the chart of Ascendas REIT against the Singapore 10 year yield (inverted) below.

Yes it doesn’t track perfectly, but by and large the broad trends are there.

REIT prices shot up from Nov 2023 – Jan 2024 because of the sharp drop in 10 year yields.

And since the start of the year, REIT prices have been dropping because of the rise in 10 year yields.

What is driving the move in 10 year yields (and REITs)?

I cover this in greater detail in FH Premium and other articles.

Long and short is that the Fed and Treasury Pivot in late 2023 sparked a huge drop in interest rates.

But of late, the Fed/Treasury have walked back some of that “pivot”, driving interest rates higher.

Singapore being an open market, we take our cue from US markets, and hence S-REITs have responded accordingly.

DPU is dropping – higher rental income offset by higher interest costs

The second point – is that REITs just reported their 2H 2023 results, and the DPU numbers have been less than impressive.

In late 2022 a lot of you guys asked me whether higher rentals for REITs would be able to offset the higher interest expense costs.

My answer was no.

Because if interest rates go from 0% to 5.5% in the span of 18 months.

You would need a massive rental increase to offset that rise in interest rates, which I did not see as likely.

And that’s exactly what we’ve seen.

Are REITs a great play on lower interest rates?

But don’t miss the forest for the trees here.

Jerome Powell has pretty much confirmed that we will see interest rate cuts in 2024.

The only question is how soon, and how quickly they cut once they start.

So much of the headwinds for REITs the past 2 years, may start to reverse going forward.

Where will REIT prices go in 2024?

The tricky part though, is that central banks only control short term interest rates.

If Powell cuts too early, there is a risk inflation comes back, sending long term interest rates higher.

And if you look at previous cycles.

The recession usually hits about 6 – 12 months after the first interest rate cut.

Assuming Powell cuts in mid 2024, this would place the potential “danger” zone in 2025.

Based on what we’re seeing today, and the resilience of the US economy – there’s probably a good chance we avoid a recession.

But sometimes, when markets are the most complacent, that’s when the risk hits.

So what I’m trying to say is this.

Interest rate cuts are coming.

If I had $100 set aside to buy REITs, I’m probably going to buy some here.

But I’m not going to borrow another $300 and all-in REITs, as there are still scenarios that could be terrible for REITs.

Top 3 REITs I may buy in 2024 – 6% dividend yield minimum?

Mapletree Pan Asia Commercial Trust

Current Price: $1.38

Market Cap: $7.24 billion

Annualised Dividend Yield: 6.4%

Price/Book Ratio: 0.80x

It’s sad to see how far Mapletree Pan Asia Commercial Trust has fallen.

Had the merger with Mapletree North Asia Commercial Trust not happened, no doubt this REIT (with Vivocity and Mapletree Business City) would be best in class, heads and shoulders above CICT.

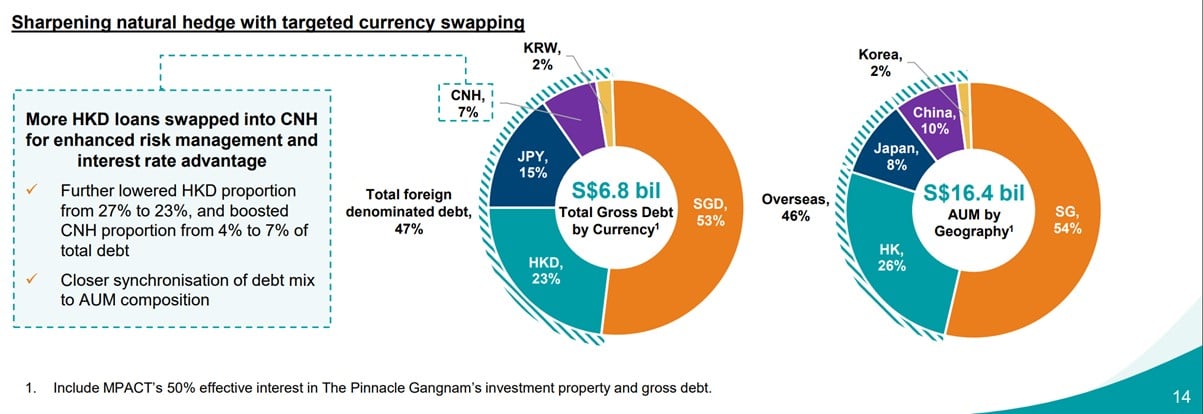

The problem with this REIT today, is the 26% AUM exposure to Hong Kong which is badly dragging the REIT down.

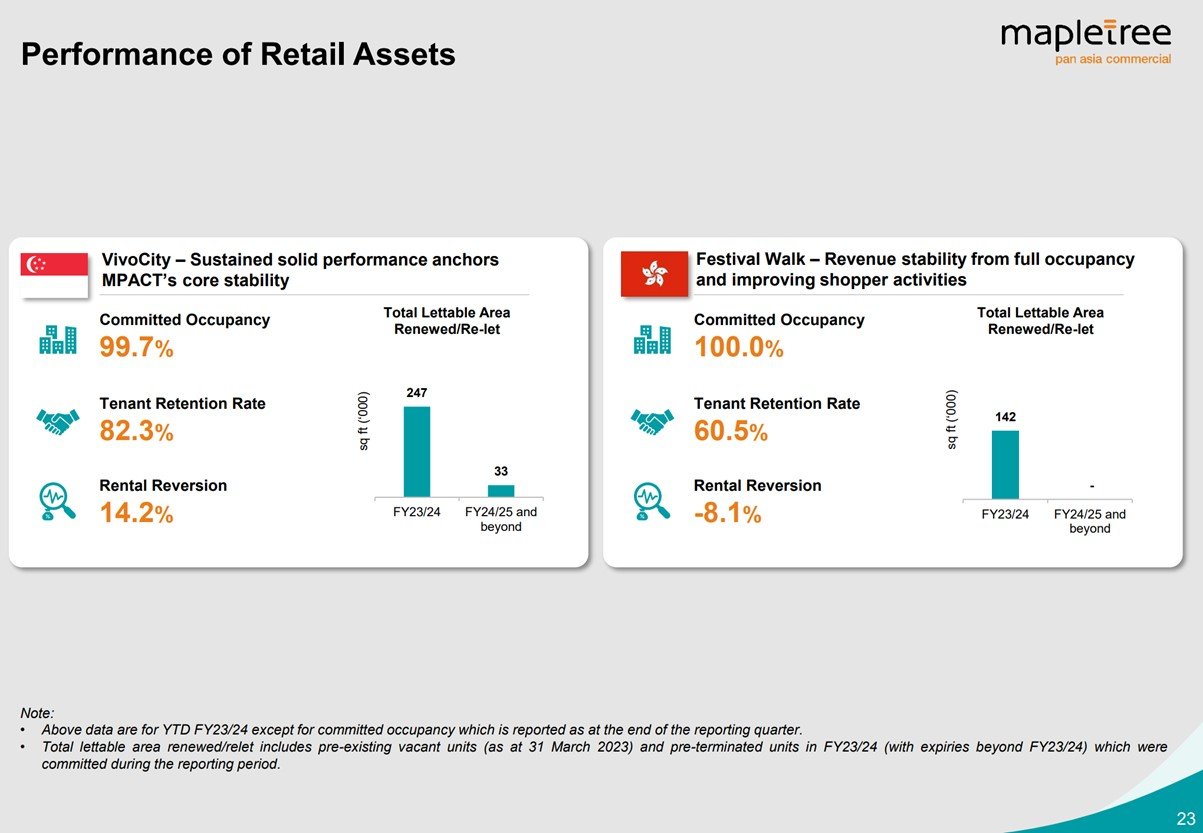

Singapore’s Vivocity is reporting 14.2% rental reversion.

While Hong Kong’s Festival Walk is reporting negative 8.1% rental reversion.

That pretty much sums up the divergence in fate of the 2 cities at this point.

What are the risks with Mapletree Pan Asia Commercial Trust?

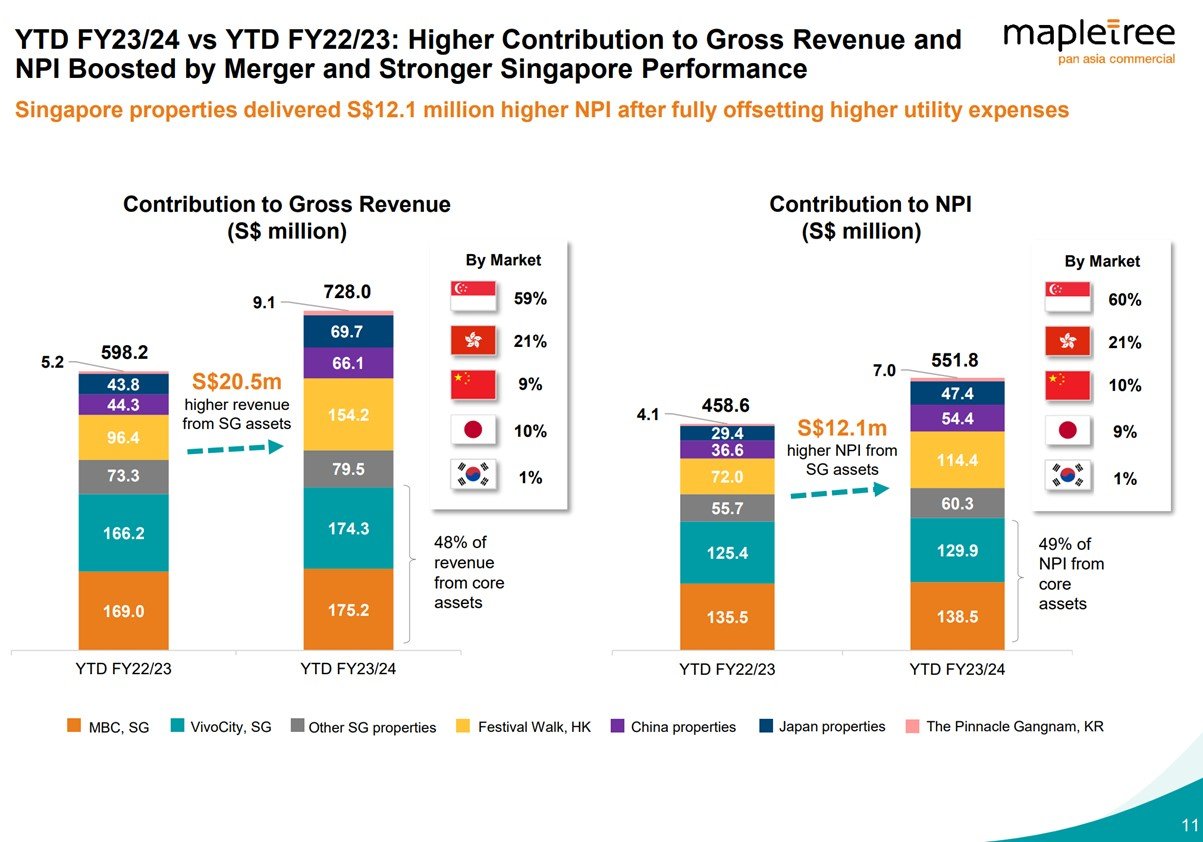

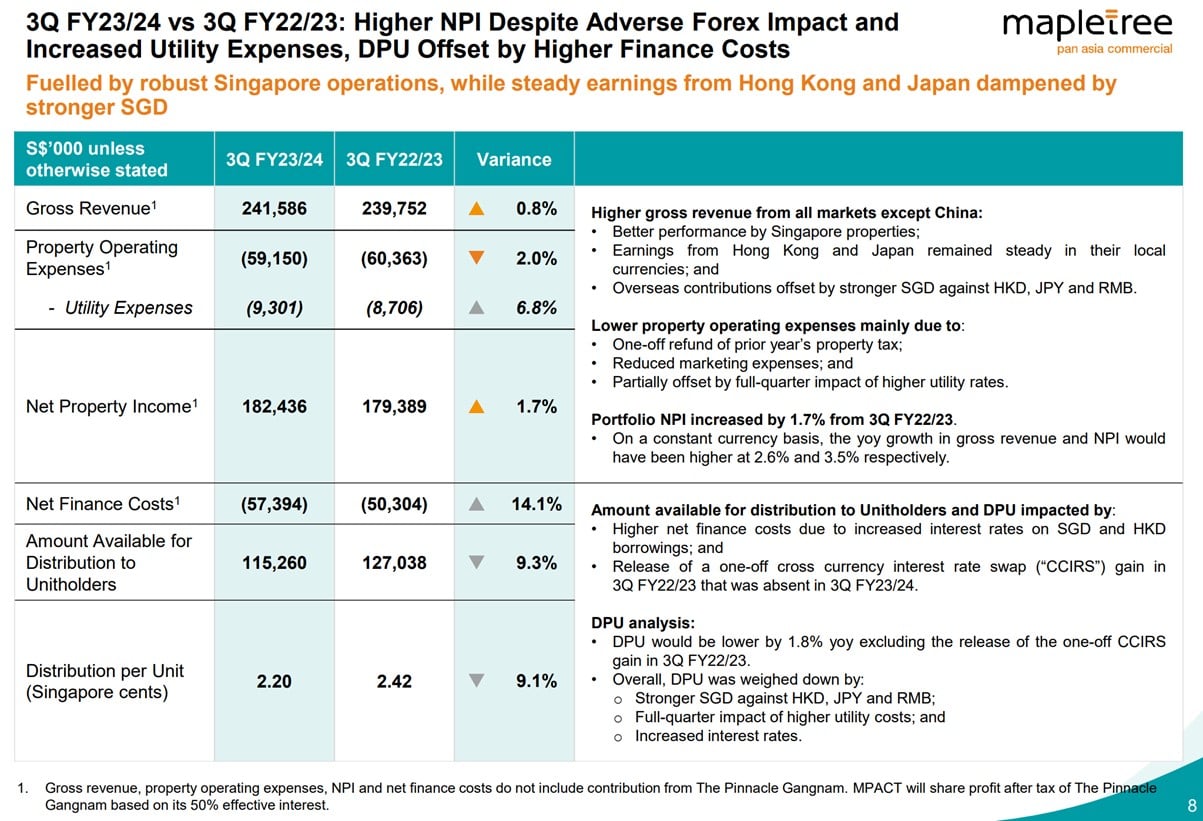

You can look at the latest breakdown of net property income (NPI) below.

Singapore’s 54% AUM contributes 60% of NPI – punching above its weight.

While Hong Kong’s 26% AUM contributes only 21% of NPI – well underperforming.

I used to think that Hong Kong’s issues were temporary and would eventually resolve itself.

Recent events have led me to question that belief.

Hong Kong is now in a position where China troubles will drag them down.

And yet if China succeeds, it is arguable that the mainland cities like Shenzhen, Shanghai, Guangzhou, may benefit more than Hong Kong.

So as an investor, why would I build exposure to Hong Kong real estate here?

If I wanted to make a bet on China, why not just buy Shanghai or Shenzhen real estate instead – given how cheap valuations are now?

Hong Kong at this point looks more downside than it’s worth.

For what it’s worth, the financial results are not pretty.

Net property income is actually up 1.7%, but DPU is down a whopping 9.1% due to higher financing costs.

What price would I consider buying Mapletree Pan Asia Commercial Trust?

That said, 54% of the REIT is Singapore assets.

Best in class Singapore assets at that – Vivocity and Mapletree Business City.

So yes Hong Kong is dragging the REIT down, but as real estate investors, you live by the mantra that “at the right price, anything can be a good buy”.

I don’t think book value is that helpful given most of the REITs valued their real estate in a climate of zero interest rates.

So I calculate the “effective cap rate” – I took the net property income, divided it by the price of the real estate (being market capitalisation of the REIT + debt).

This allows me to better understand how much net property income I am getting per dollar put in (stripping out the interest expenses).

This “effective cap rate” for MPACT today, is 5.04%.

This means that if you put $100 in, you get $5.04 back each year in net rental income (the actual dividend yield is higher because of the debt).

For a portfolio that is:

- 54% Singapore

- 26% Hong Kong

- 10% China

- 8% Japan

It’s hard to say that’s a screaming buy, but like I said the Singapore portfolio is best in class, and good enough that I would be keen to build long term exposure.

Annualising the latest DPU gives you a 6.4% dividend yield, which is not too shabby (almost 3.4% spread vs the Singapore 10 year yield).

From a technical perspective, there is support at the current 1.38 level going back to 2017.

Lows for this cycle was 1.3 though, so if the China sell-off continues there could be further downside.

That said, I know not everyone is comfortable with China/HK risk – so I leave for investors to decide what price they are comfortable with, or if they prefer to skip this REIT entirely.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Starhill Global REIT

Current Price: $0.49

Market Cap: $1.12 billion

Annualised Dividend Yield: 7.27%

Price/Book Ratio: 0.70x

Starhill Global is one of those boring REITs that has flown under the radar for much of its existence.

But with REITs – boring is good.

I last picked up a position in Starhill Global in the low 40s during COVID, and sold it all in the 60s post COVID.

Now that it’s back to the 40s again, I picked up a position again.

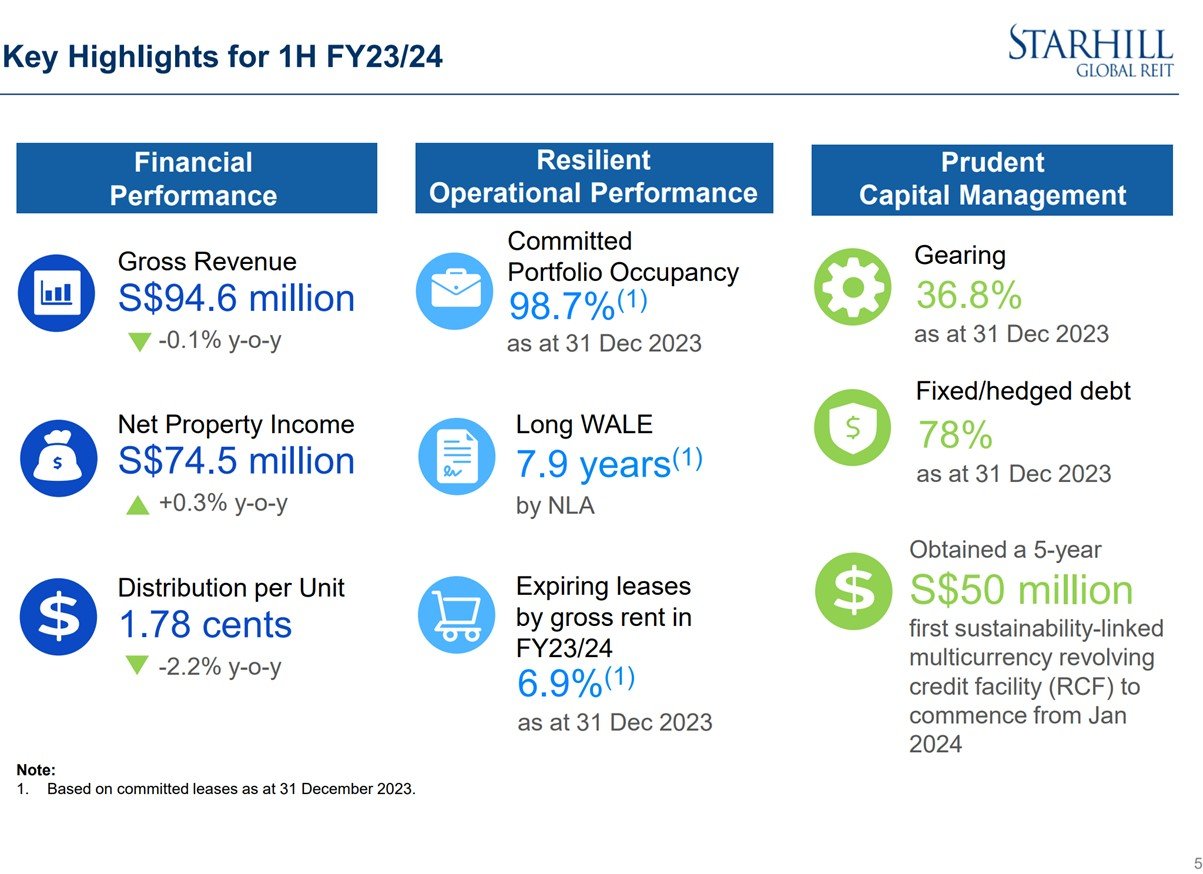

Financial Results are actually not too bad.

DPU is only down 2.2% year on year.

Annualising the DPU gives you a 7.27% dividend yield, almost a 4.3% spread vs the Singapore 10 year yield.

Using the “effective cap rate” concept – you’re buying Starhill Global REIT at a 6.67% cap rate.

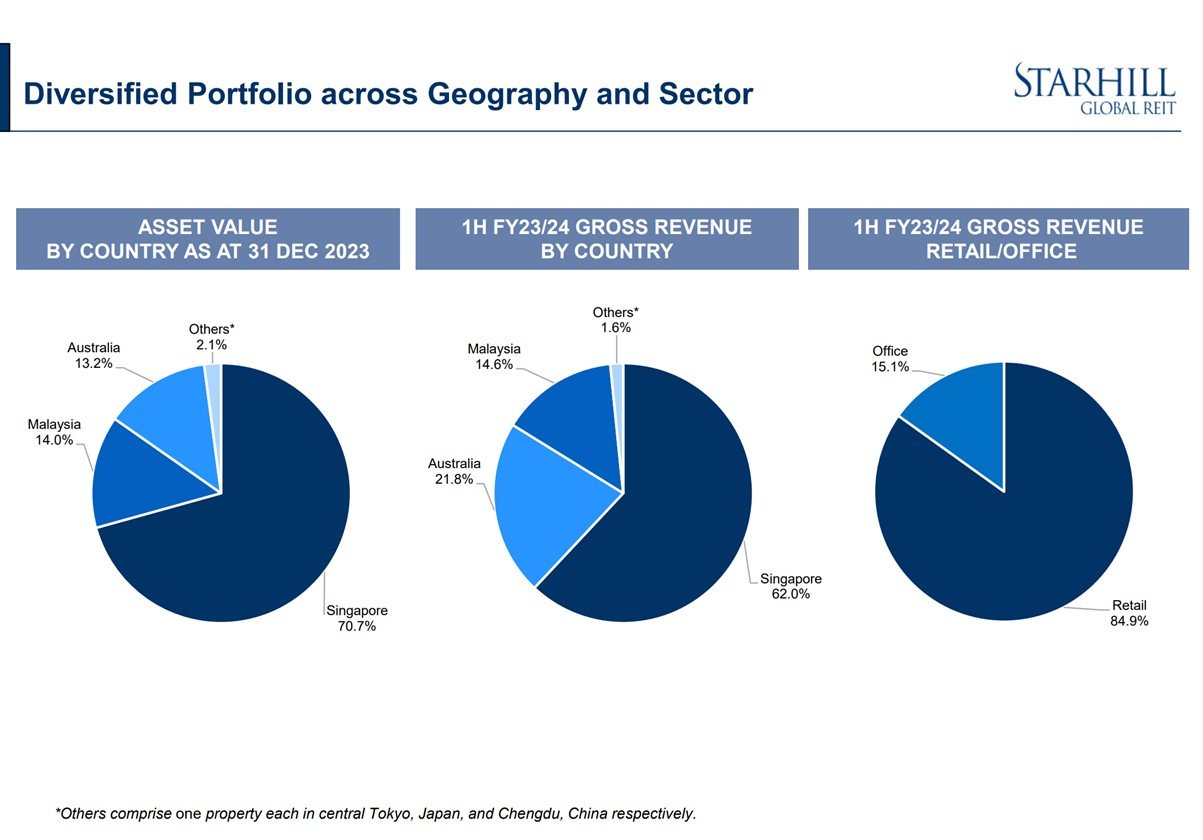

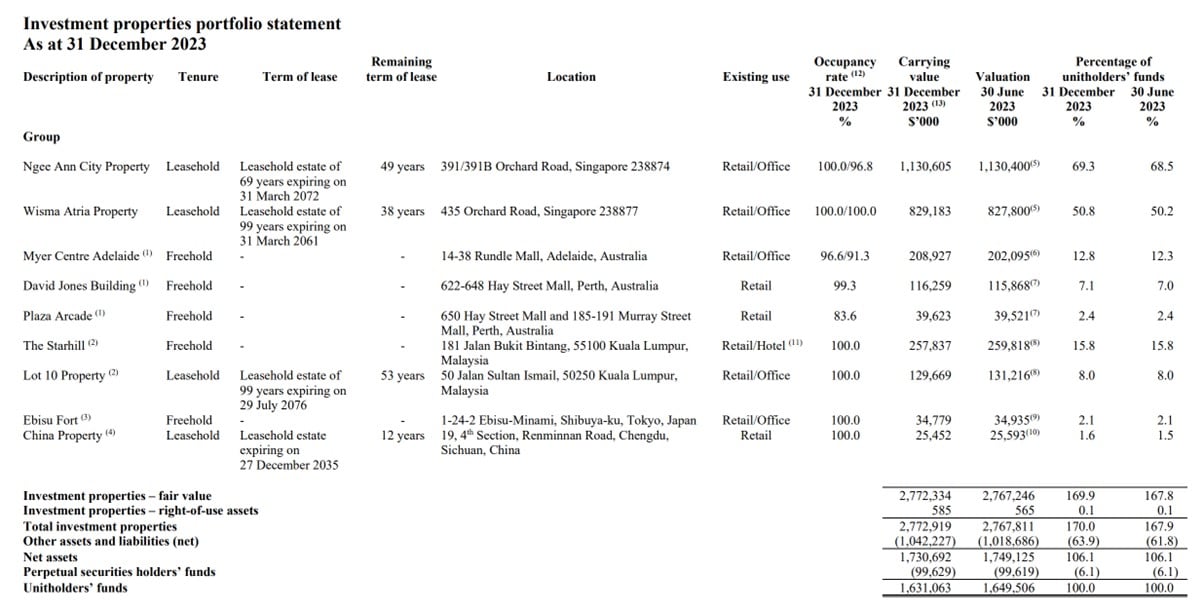

For a property portfolio that is:

- 70% exposure to SG (41% Ngee Ann, 29% Wisma Atria)

- 14% Malaysia (the Starhill and Lot 10 in KL)

- 13% Australia (Myer Centre, David Jones – in Adelaide/Perth respectively)

I could get on board with that actually.

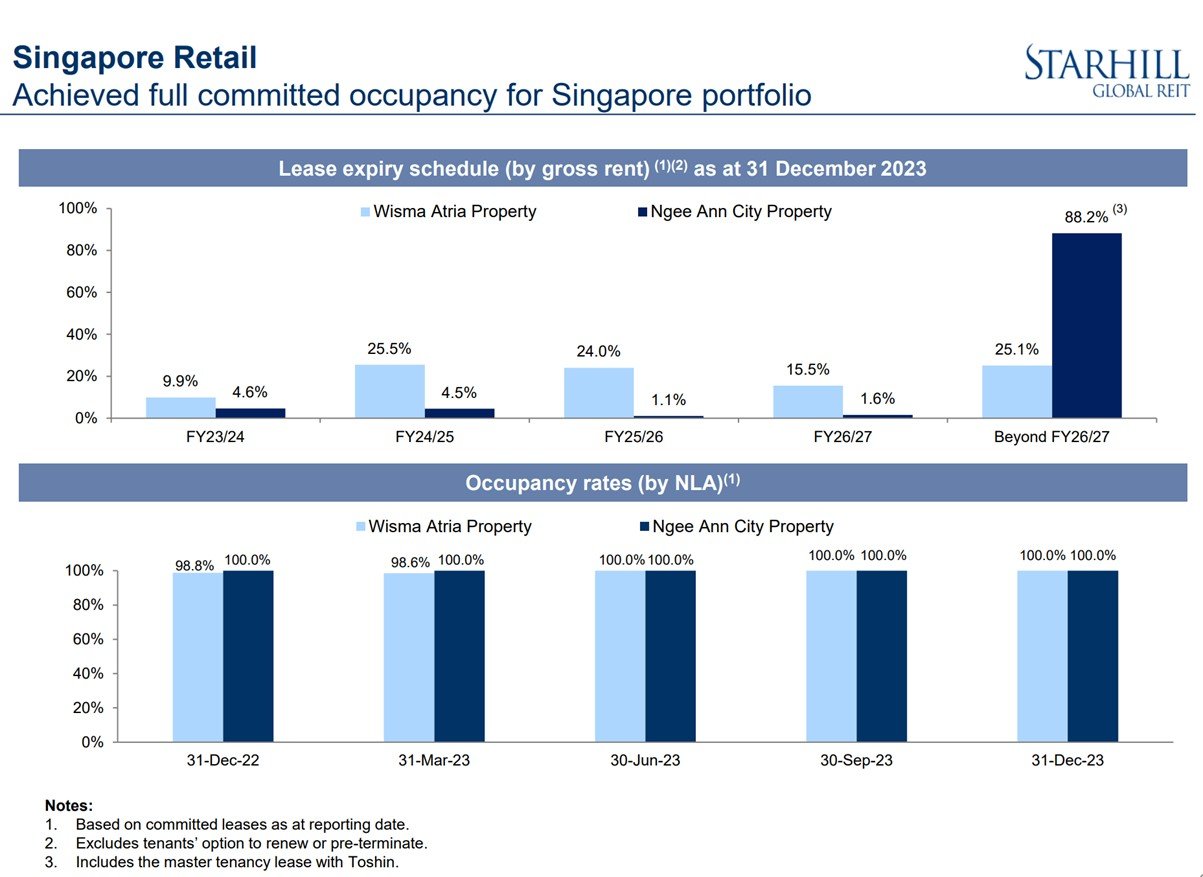

Risks with Starhill Global REIT?

My concern with Starhill Global has always been centred on Wisma Atria (29% of the AUM).

While Ngee Ann City is a strong asset.

Wisma Atria runs the risk of being a pass-through mall – you know the one where people only walk through the basement to get from Taka to Ion, but never actually visit the mall?

In my latest visit to Wisma Atria though, I thought the tenant mix was decently attractive, and footfall was decent.

NPI is up 1.0%/3.9% for Wisma Atria, and you’re looking at 100% occupancy.

What price would I consider buying Starhill Global REIT?

If price goes back to the low 40s, I might just back up the truck.

If it stays in the high 40s?

Probably fair value for me – but again I leave investors to reach their own conclusions.

Keppel REIT

Current Price: $0.89

Market Cap: $3.46 billion

Annualised Dividend Yield: 6.5%

Price/Book Ratio: 0.69x book value

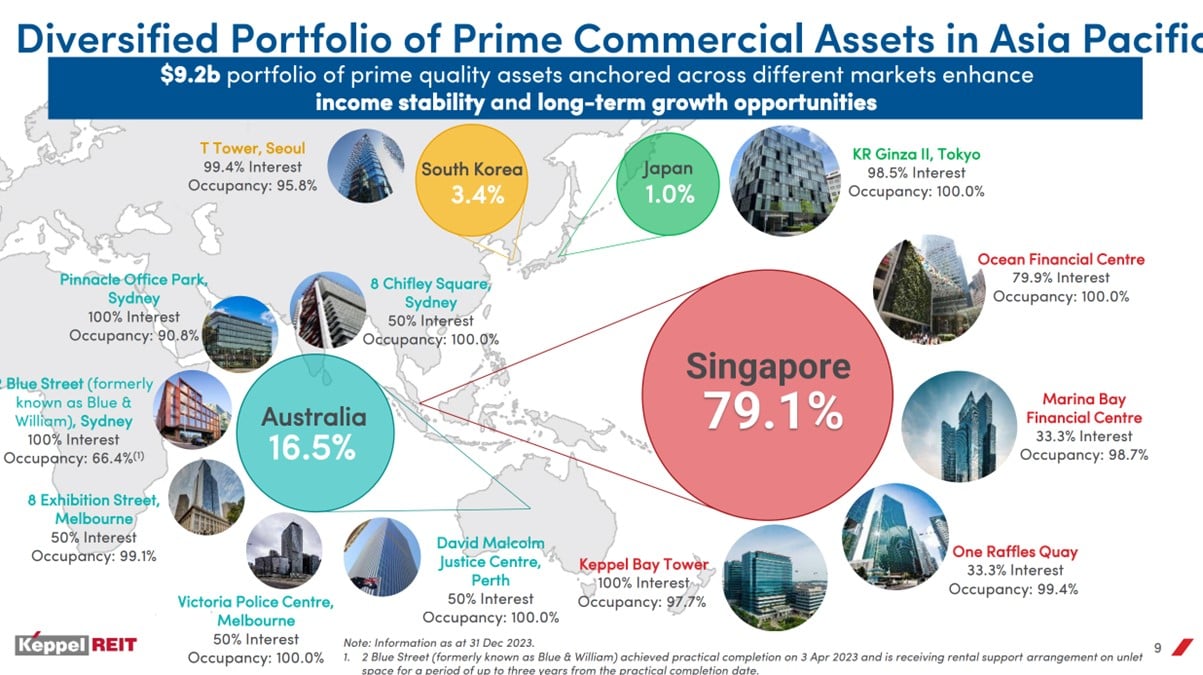

Post-COVID there was a lot of fear over Keppel REIT.

Overseas Investors saw the work from home trends in the US, extrapolated the same to Asia, and sold off office REITs.

They’ve gradually awoken to the fact that the work from home trend in Asia is much less pronounced.

For the simple reason that if you ask Asians to come back to the office, they will come back (unlike in the US).

So office buildings in Asia don’t face the same headwinds that US offices do.

Financial Results are pretty decent as well, DPU is only down 1.7% year on year.

Annualising this DPU gives you a 6.5% dividend yield, a 3.5% spread vs the 10 year yield.

One thing to note about Keppel REIT is that the dividend is artificially boosted by the “Anniversary Distribution”:

“To reward the unwavering support of Keppel REIT’s Unitholders, an additional $100 million from accumulated capital gains will be distributed over the next five years leading up to its 20th anniversary in 2026”

Strip out the special Anniversary distribution, and the dividend will drop to 5.9%.

So this is important to note – the “natural” yield for the REIT is actually lower than the headline number.

“Effective cap rate” is 4.6% for this reason.

But for a REIT with 79% exposure to Singapore office space, I think that’s fair value from a fundamental perspective.

What price would I consider buying Keppel REIT?

Cycle low was 80s, and I sadly missed the opportunity to add at that price.

If it goes back there I might just back up the truck.

Otherwise, the REIT seems too have found a base around the mid to high 80s, which I suppose is fair value-ish looking at the cap rate numbers above.

Honourable Mention – Other REITs I may buy in 2024?

For obvious reasons, I was only able to cover 3 REITs in this list (full disclosure that I hold positions in all 3 REITs above, so read into that what you will).

And depending on how price trades the next few months, there are many other REITs I am keen to purchase.

The full list of REITs I am keen to buy with price targets is shared on FH Premium.

But I just wanted to discuss a few honourable mentions here.

Keppel DC REIT

Keppel DC REIT is a name I am looking to build exposure to.

I just did an write-up on FH Premium last week with updated price targets.

The China exposure (and tenant bankruptcy) is no doubt a worry that will hang over the REIT in the short term, pressuring unit price.

But take a longer term view, and this is likely to be a temporary overhang.

Which opens up an attractive opportunity for long term investors to build exposure to a prized asset class – Singapore data centres.

Keppel Infrastructure Trust

Boy… what is an infrastructure trust doing buying BUS company?!

I had a long rant on FH Premium when I saw the news on Monday.

Is this Comfort Delgro or Keppel Infrastructure Trust that I bought?

The Business Trust is going to hold an EGM and equity fundraising to fund their purchase of the bus company.

This is going to pressure the share price in the short term.

But I’ve been impressed by how KIT has performed the past 1 – 2 years, performing very well even in the face of higher interest rates.

Given there is likely to be some weakness due to the equity fundraise, I may add to my KIT position going forward.

Updated views / price targets will be shared on FH Premium as it plays out.

This article was written on 8 Feb 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

– Get up to USD 3000 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 3000 free shares.

You just need to:

- Fund SGD2000

- Maintain until 31 March

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Hahaha. I thought the press printed ComfortDelGro’s name wrongly too. Does KIT or Keppel Group know how to manage a taxi company? I don’t really like KIT given her shxxxx record when it was called City Spring Trust. It was $1 donkey years ago at IPO when i was a shareholder. Tend to do some stupid stuff once in a while that surprise investors. I dunno why. This may be it again.

Hahaha similar views. I was not a big fan of this BT back in the City Spring days. Real destruction of shareholder value there.

The turnaround since then has led me to change my mind, to the point where I opened a position in KIT last year.

Their recent acquisitions don’t inspire confidence though – going into European windfarms, Saudi pipelines, and now Australian bus companies. Not very sure how KIT management has any competitive advantage in those areas, nor the bandwith to add value.

Buying a foreign bus company from a family that is cashing out is a recipe for disaster if not properly managed.

Would have been much happier if they had stayed to their core competency in SG. But I get that these days all the REITs/BT need to go overseas for growth. Netlink seems to be the odd one out thugh.

Rather than individual reits, what are your thoughts on reit etfs? Would these be a better move moving forward since they’d be more “self-correcting”?

I think they’re fine. Don’t think of a REIT ETF the same way as the S&P500 though – the US is a much more efficient and deep capital market.

Because of that I think with S-REITs it is much easier to outperform with individual REITs, as compared to the S&P500.

But I get that not everyone wants to stock pick individual names, and if the choice is between buying a REIT ETF or buying none, then it’s probably a simple answer.