I’ve been talking for months about how I think S-REITs are a good buy.

And to put money where my mouth is – REITs are the only asset class I’ve been consistently buying.

This week, we had massive news out of Mapletree Commercial Trust and Lendlease REIT.

And announcements on further reopening post-COVID.

So I figured this was a great time to relook REITs.

What are the Top 5 REITs to buy in Singapore right now, in 2022?

Flash Promo for the Stocks MasterClass – 1 week only! Find out more here!

Top 5 Singapore REITs to buy right now in 2022 – Selection Criteria

I’m not going to get too cute here.

This list will focus exclusively on:

- REITs that I myself may consider buying

- For my own risk appetite and portfolio (full portfolio on Patreon)

Now this article is not meant to be on timing.

But what the heck, I love macro, so I’ll share some views at the end of the article as well.

Top 5 Singapore REITs to buy now – 2022

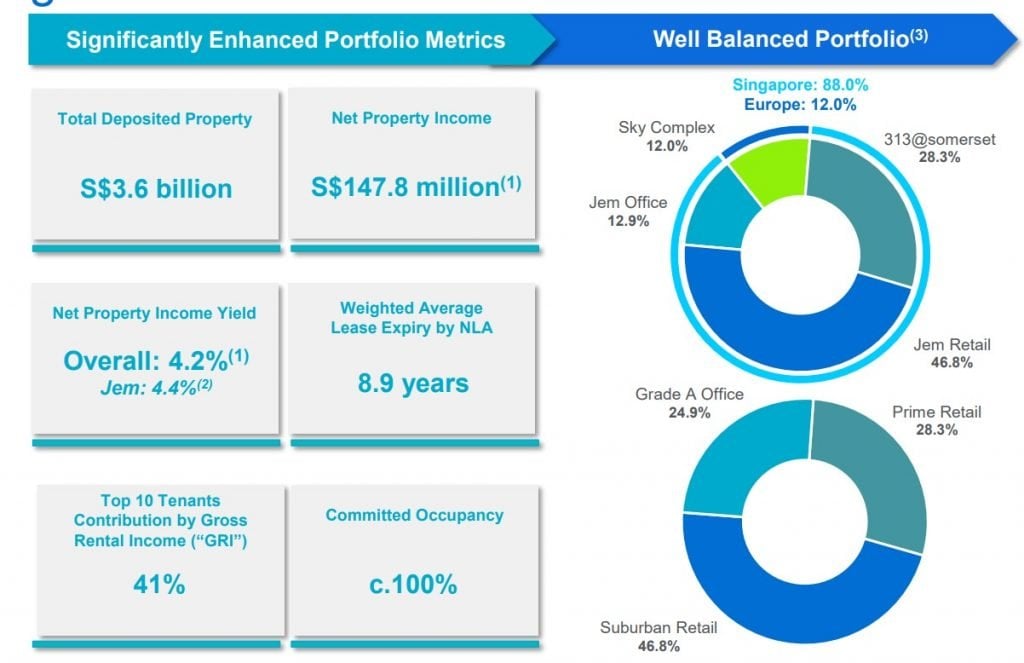

Lendlease Global Commercial REIT

Current Price: $0.80

Market Cap: $983m (before equity fundraise)

Price to Book: 0.82x

Estimated Yield: 5.8%

Lendlease REIT is starting to shape up into a very solid Singapore focussed retail REIT.

After the injection of Jem, almost 75% of the REIT will be comprised of 2 high quality Singapore retail malls – Somerset 313 and Jem.

For the record – Jem and Somerset 313 are probably not best in class malls like Vivocity or Ion Orchard.

But there’s no denying that they’re top tier real estate, in fantastic locations.

And Lendlease as a Sponsor has done a fantastic job in extracting value through strong tenant selection, and both malls have very strong footfall.

Pipeline is rock solid as well with the possibility of future injections of Parkway Parade and Paya Lebar Quarter.

Big and dilutive fundraise to fund Jem

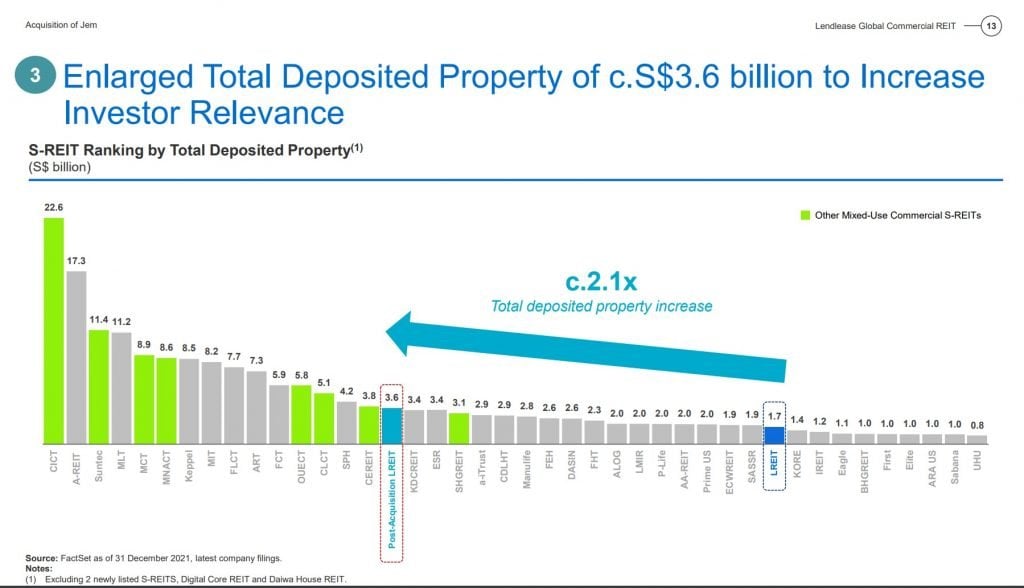

To fund the Jem acquisition, Lendlease REIT did a big equity fundraise this week.

The private placement was priced at $0.725 (9% discount to last done).

While the preferential offering (29 for 100) was priced at $0.72 (9.6% discount to last done).

Now that maximum discount you can price without getting shareholder approval is 10%.

So the fact that Lendlease REIT had to price their placement at a 9% discount, screams to me that liquidity in the institutional space is very, very tight right now.

It’s quite a high quality REIT, buying a strong mall. And they still needed to price in such a big discount to fill their books.

Not a good sign.

What price to buy Lendlease REIT?

With that in mind, it just doesn’t feel good to be buying at $0.80 on the open market now when the institutional players went in at $0.725.

And with the massive 29 for 100 preferential offering coming, there could be a fair bit of headwinds for Lendlease REIT.

At the end of the day, Lendlease REIT is still a very small REIT.

So it doesn’t make sense to pay a premium as well.

That said, I really like this REIT, and if it goes back into the 70s I might finally open a position.

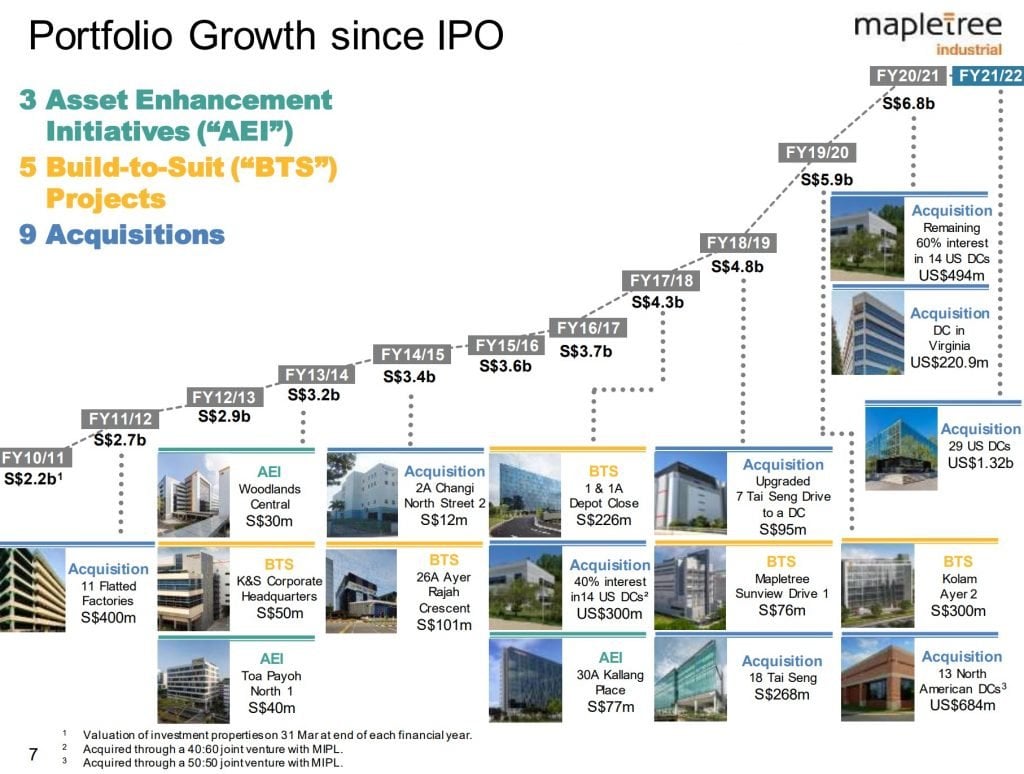

Mapletree Industrial Trust

Current Price: $2.69

Market Cap: $7.2b

Price to Book: 1.4x

Yield: 5.0%

Remember how just 1 or 2 years ago industrial / data centre REITs were the hottest thing since sliced bread?

While retail REITs were “uninvestable”?

But suddenly everybody loves retail for “COVID Recovery” play, and hates industrial/data centres.

Market is funny like that.

Mapletree Industrial Trust is a 50% Singapore industrial REIT, and 50% US Data Centre REIT.

There’s no denying that industrial is not sexy now.

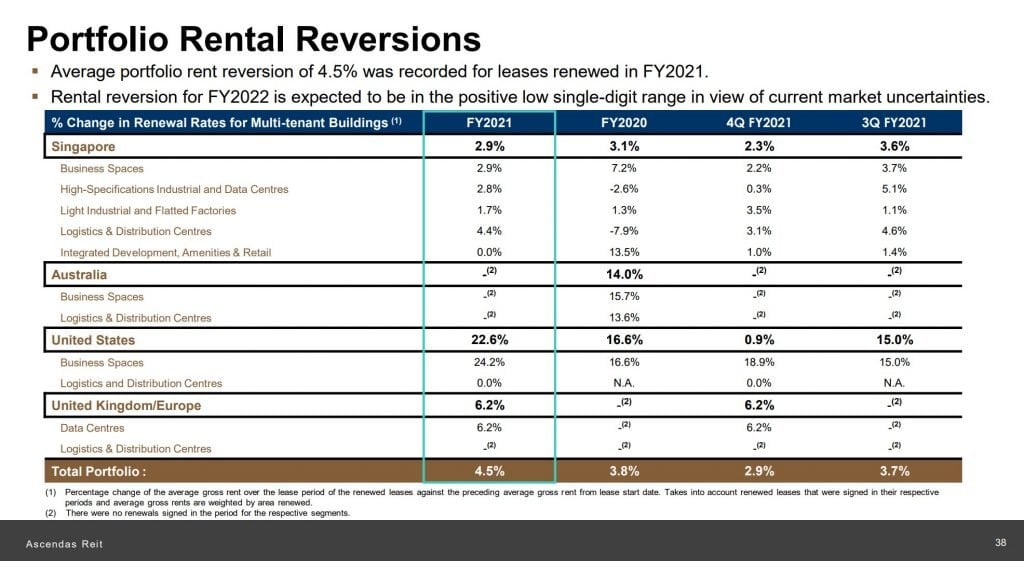

Rental reversions are flat across the board.

With soaring commodity prices and rising interest rates, we’re very likely to be heading into a period of slowing growth and margin compression for companies. That’s not going to be good for industrial companies, and will probably impact industrial rents.

But, as a long term investor, sometimes you want to invest counter cyclically.

Buy high quality retail when nobody wants it (2020 – 2021), buy industrial when nobody wants it (2022 – ?)

For Mapletree Industrial Trust – I like the Sponsor, I like the strategy, and I’m happy to hold long term.

What Price will I buy Mapletree Industrial Trust?

I’ve been generally accumulating MIT at the $2.5+ range.

The bottom for blue chip industrial REITs the previous cycle was 6% yield, which would work out to a $2.2+ for Mapletree Industrial Trust.

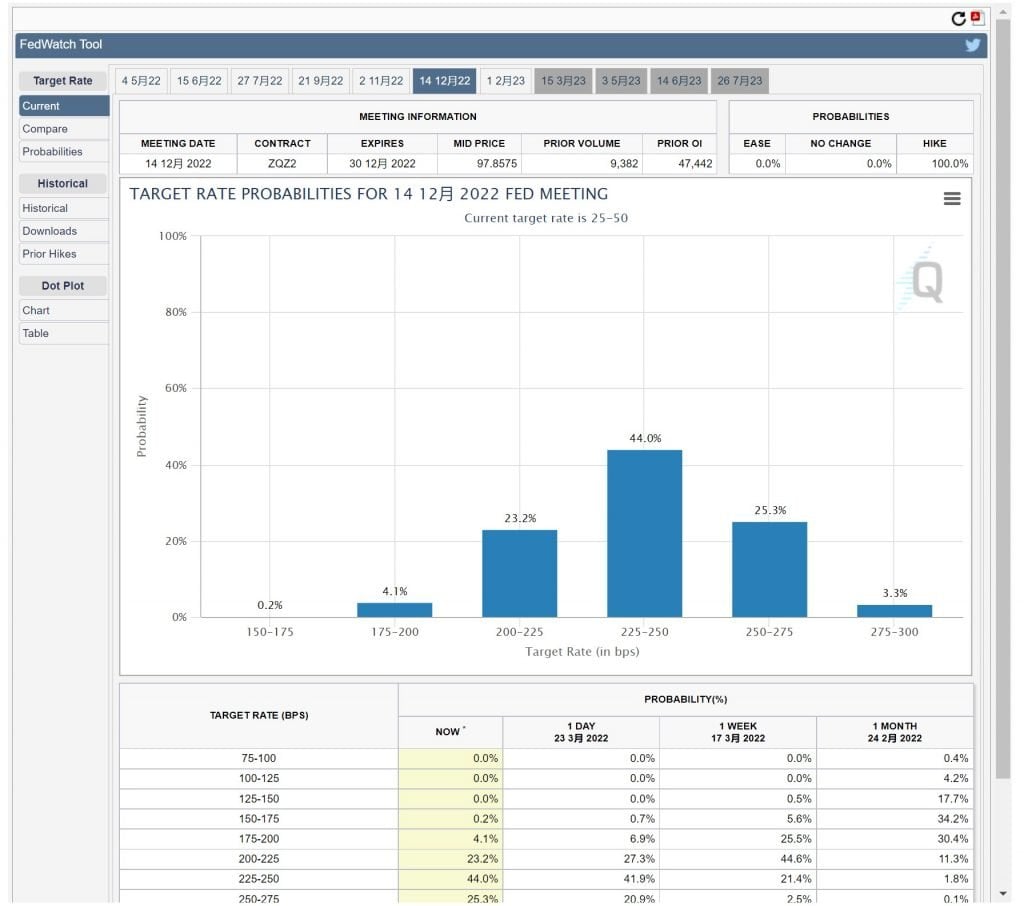

I don’t know if it’ll get there this cycle, but with the market pricing in 8 more rate hikes by Dec 2022, you never know.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Mapletree Commercial Trust

Current Price: $1.9

Market Cap: $6.3b (pre-merger)

Price to Book: 1.0 (post-merger)

Yield: 5.0%

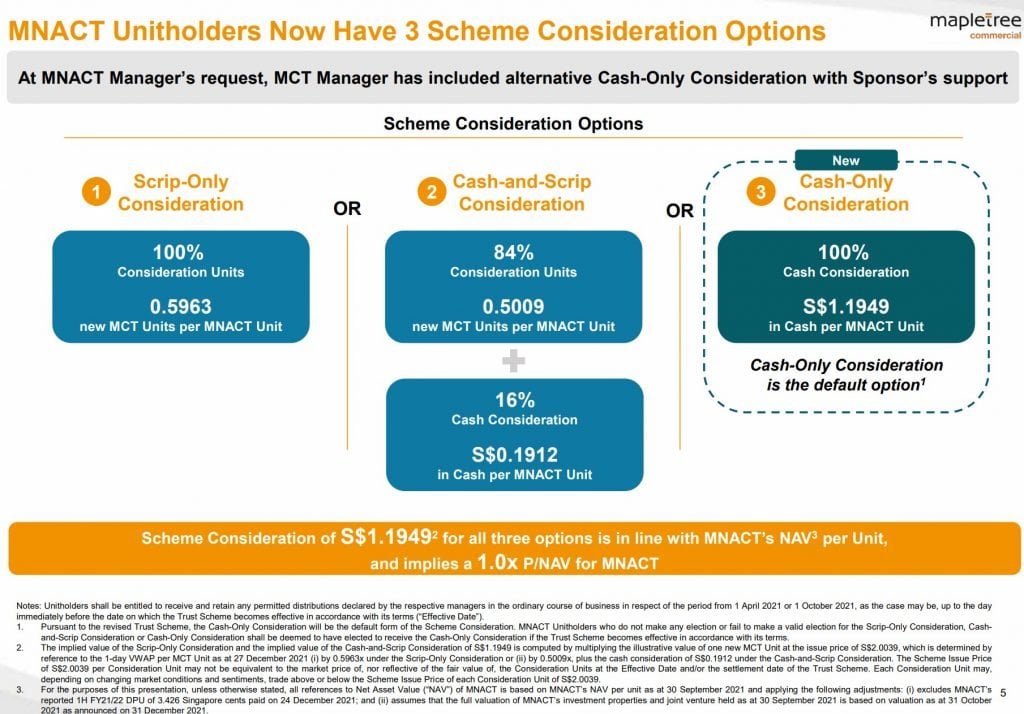

Mapletree Commercial Trust just announced an amended offer for Mapletree North Asia Commercial Trust this week, do check out my article here for full details.

Long story short – after all the hooha, Mapletree finally relented.

MNACT unitholders now have the option to be bought out at $1.1949 in cash (instead of MCT units).

And for MCT unitholders the merger is funded via a preferential offering at $2.00, fully backstopped by Mapletree.

Which means MCT unitholders don’t need to cough up extra capital, and there’s no change to the financial impact.

It’s a change that I really like.

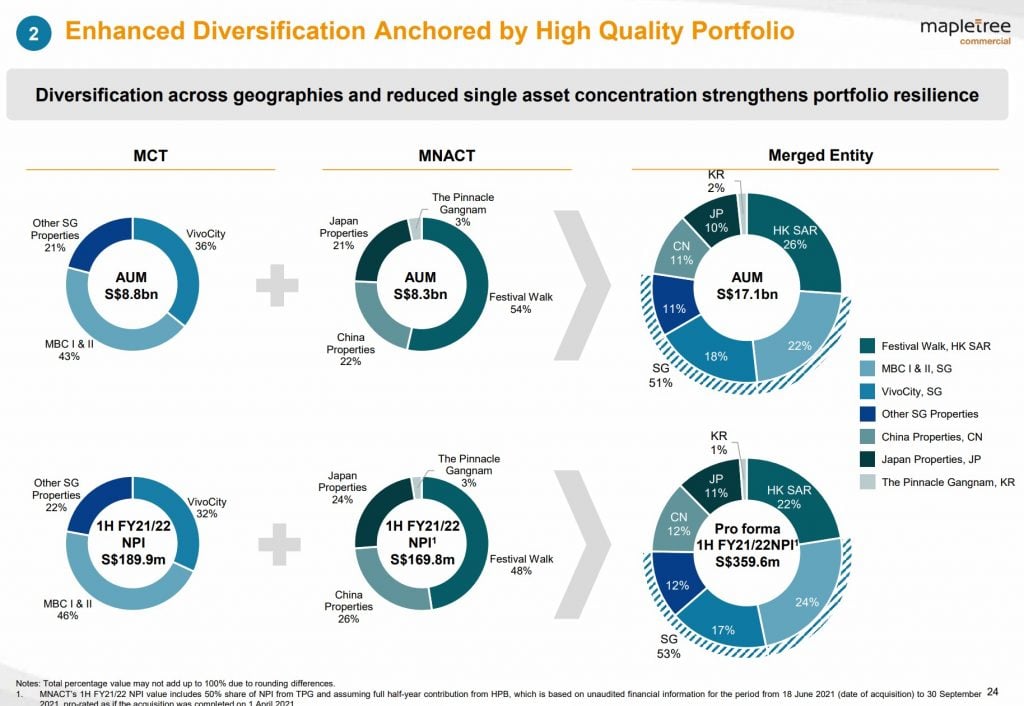

But just to put it out there – I’m not the biggest fan of MNACT’s portfolio.

The flagship property Festival Walk is located in Hong Kong, a city which I’m not particularly keen to invest in long term.

The other offices in China, Korea and Japan while decent, are very far from being best in class real estate.

And the rental reversion across the board for MNACT is horrendous.

That said, I adore Mapletree Commercial Trust’s portfolio.

Vivocity and Mapletree Business City are best in class plays in retail and business park respectively. And the exposure to Greater Southern Waterfront rejuvenation longer term is worth its weight in gold.

This is a 10 – 20 year play for me.

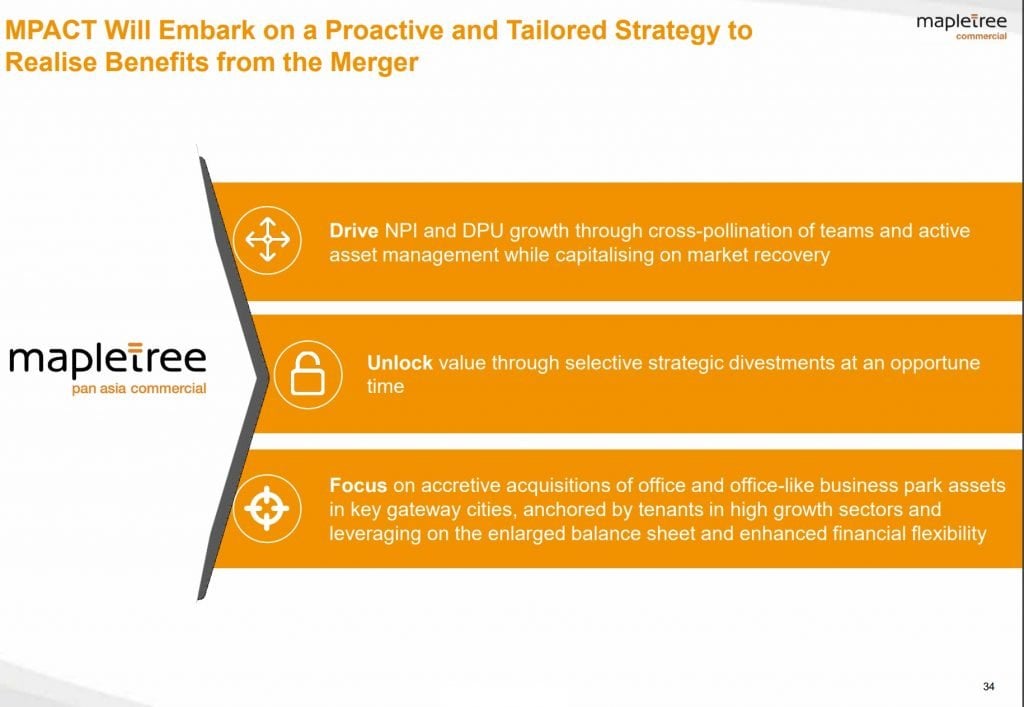

For some reason, Mapletree seems to think that merging the 2 REITs is the best way forward, and they keep talking about their plan for “unlocking value”.

I kind of get it, because MCT and MNACT alone cannot compete with the likes of CICT and Ascendas REIT in AUM anymore, and real estate is a scale game. So this move is crucial for MCT’s long term competitiveness.

At current price, you’re buying in at about a 5%+ yield, and at NAV for the expanded portfolio.

While I would love to get it cheaper, I do have to admit that 1.8+ is probably fair value for Mapletree Commercial Trust after this week.

And at the end of the day, the 50% exposure to Vivocity and Mapletree Business City is probably sufficient to justify investment into this REIT.

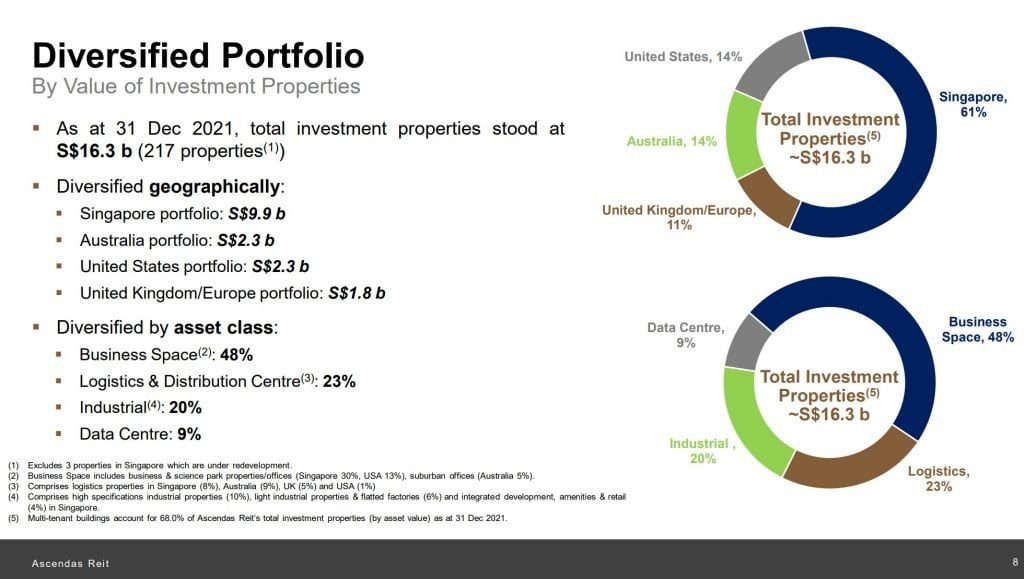

Ascendas REIT

Current Price: $2.92

Market Cap: $12.2

Price to Book: 1.19

Yield: 5.2%

I never understood why some investors want an “exciting” REIT.

In my books, the more boring the REIT, the better.

Just pay me my yield, some small capital gains, and I’m happy.

Ascendas REIT is another boring as rocks REIT.

That said, it’s backed by CapitaLand (Temasek majority owned), is one of the largest REITs in Asia, and holds a very high quality industrial / data center portfolio that spans Singapore, Australia, US and UK.

At a 5.2% yield.

What more do you want?

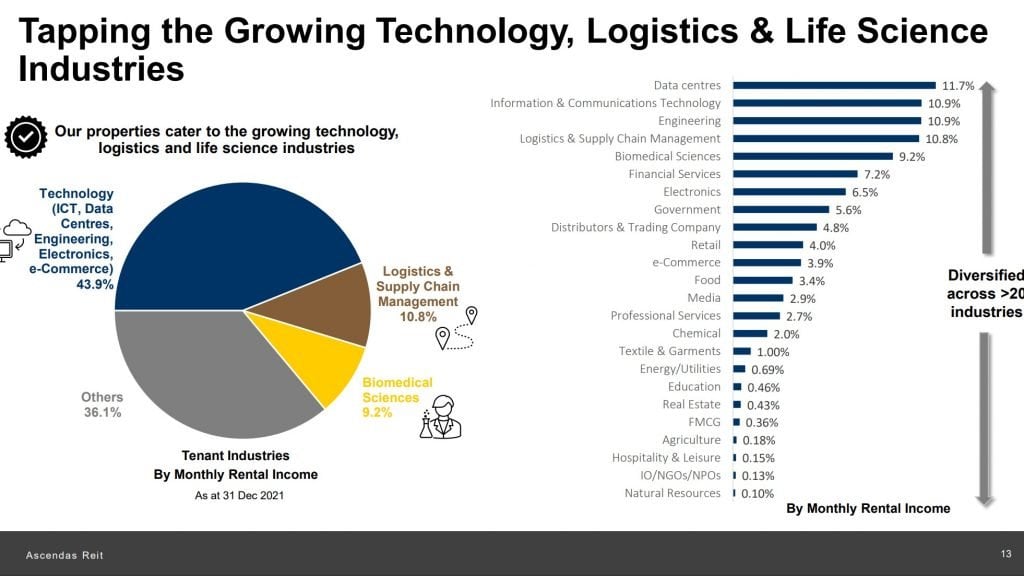

For what it’s worth, Ascendas REIT does come with fairly big exposure (43.9%) to the Technology tenants.

But don’t kid yourself that you’re investing in Tech.

This is plain old vanilla real estate.

Ascendas REIT owns buildings and they lease it out. To whoever can afford to pay the highest.

Today that is technology, tomorrow it may be someone else.

Just like with Mapletree Industrial Trust, rental reversions are not good. Low single digits for Singapore.

What Price would I buy Ascendas REIT?

I last bought Ascendas REIT a few weeks back at $2.7+ when news of the Ukraine war broke.

The bottom for Ascendas REIT in 2018 was a 6% yield.

Working backwards, that would be about $2.5+ this cycle.

Again – I have no idea if it gets there, but if it does that’s probably my cue to buy in size.

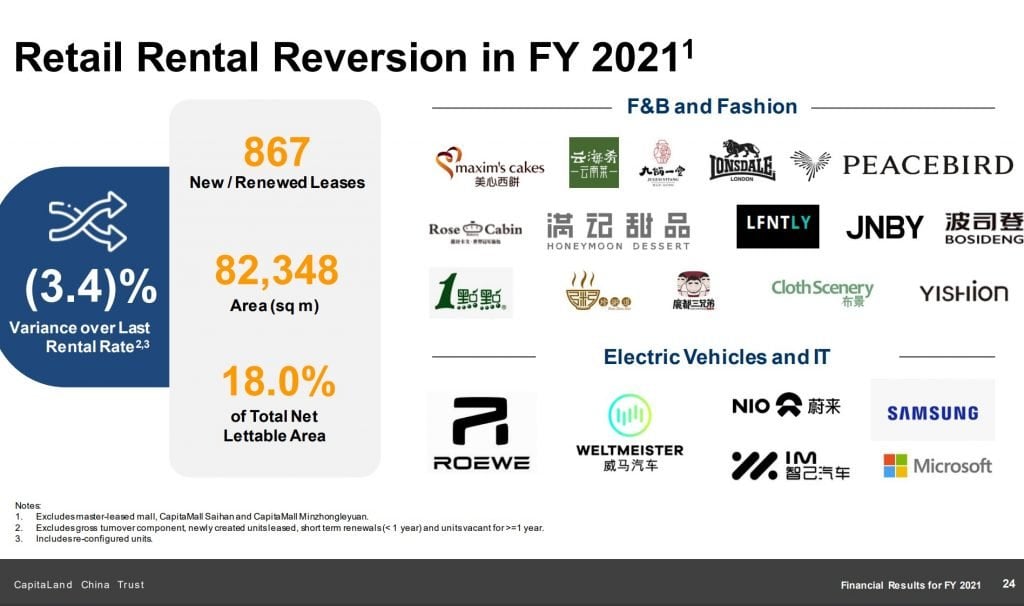

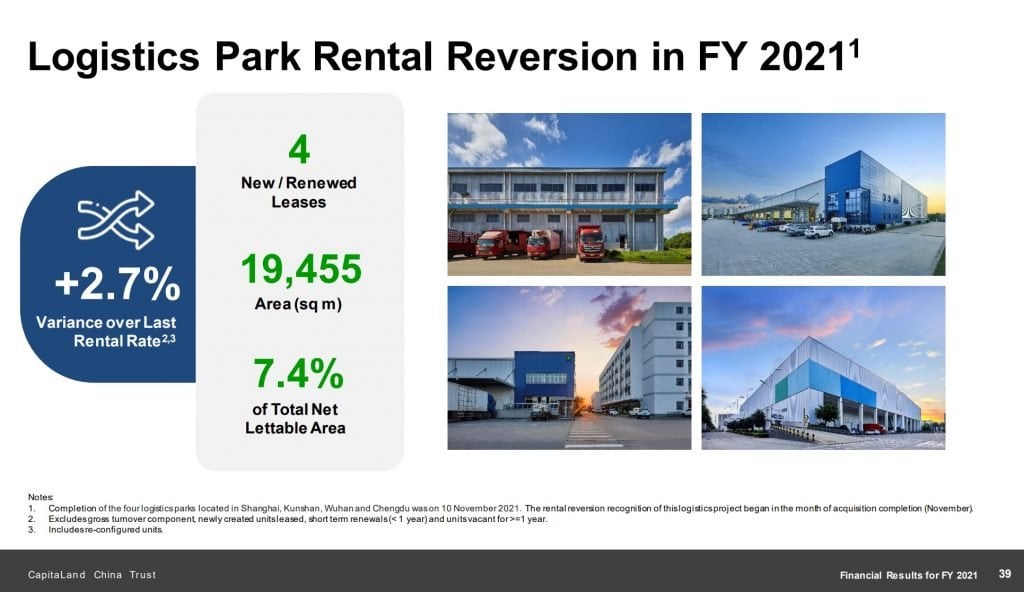

CapitaLand China Trust

Current Price: $1.2

Market Cap: $2.01b

Price to Book: 0.74x

Yield: 7.3%

Okay, so the first 4 are fairly standard REIT names.

With the last one, I wanted to take some measured risk, for a higher yield.

And CapitaLand China Trust was my REIT of choice.

I know not all of you are comfortable with China risk, and if so just skip this REIT and move on to the honourable mentions.

For me – I’m a long term bull on China, and at the right price, I’m happy to take measured risks.

For China real estate, the key right now is the refinancing risk.

You don’t want to touch any of the pure onshore players, because you don’t know if they can refinance their debt when it comes due.

You want to stick with either the (1) SOEs, or (2) offshore players with access to offshore financing.

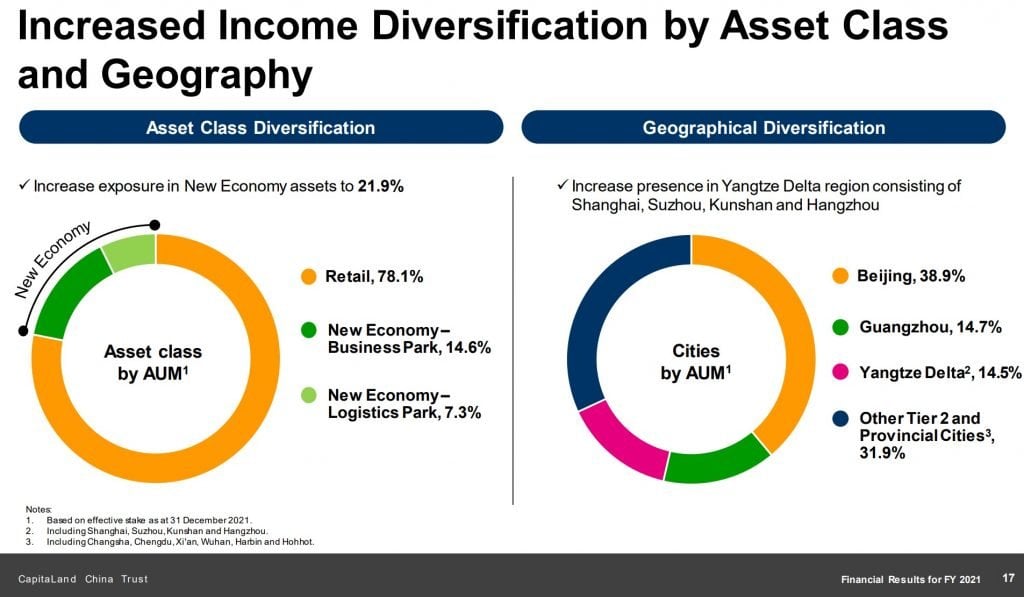

CapitaLand China Trust is one of the few pure China S-REITs, that is backed by a reputable Temasek backed developer, with access to offshore financing.

The portfolio is predominantly retail though, and about 50-50 split between Tier 1 and Tier 2 cities.

As you would expect, rental reversions for the retail portfolio are not good, down low single digits.

Logistics is doing much better – up low single digits.

I’ve been to most of CapitaLand China Trust’s malls before, and it’s something I’m comfortable to hold long term through cycles.

One problem with CapitaLand China Trust, is that in a world of mega-cap REITs, $2 billion is a bit too small to survive in the long term.

There are only 3 ways out:

- Privatise

- Bought out by another REIT

- Do a massive equity fund raise to buy China real estate from CapitaLand

I don’t think 1 is likely, which leaves 2 or 3.

I suppose CICT could buy out CLCT, they already own an 8% stake.

3 is an option too – CapitaLand has a ton of best in class China real estate held in their private funds. Once the fund life is up, divesting into the REIT could be a viable option.

Whatever the case, for those prepared to take the risk, you do get a 7.3% yield, at a 25% discount to book.

Honourable Mention – Other great Singapore REITs to buy in 2022

Just because a REIT didn’t make the list, doesn’t necessarily mean it’s a bad buy.

Here are a few others worth looking at.

CapitaLand Integrated Commercial Trust – 4.6% yield

I love CICT.

It’s one of my largest REIT positions (full portfolio on Patreon).

The problem with CICT is mainly pricing.

At current prices you’re only getting it at a 4.6% yield.

That’s okay, but with so many other REITs trading at attractive prices now, I would rather wait for a better price for CICT.

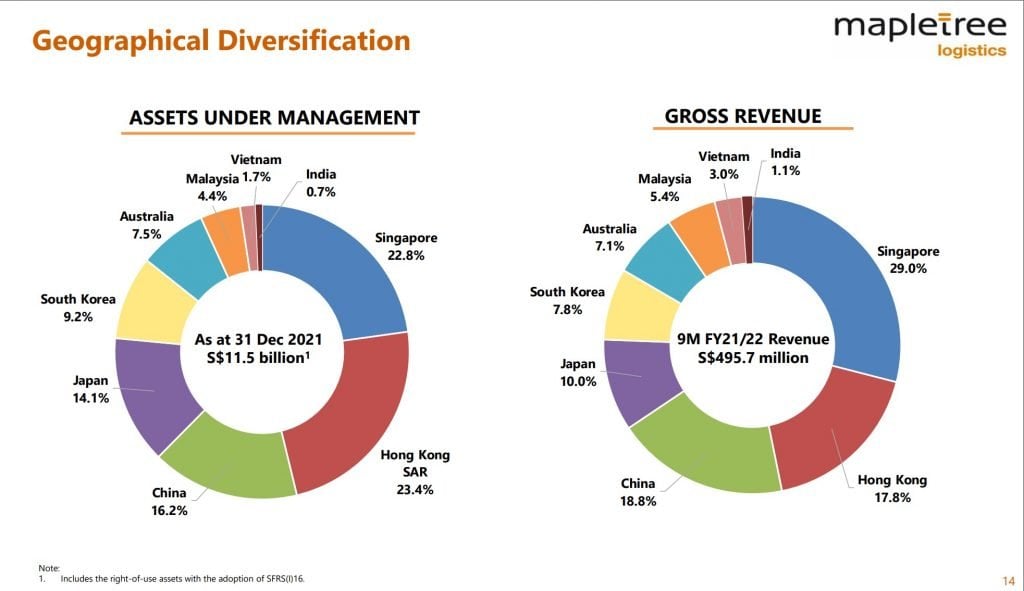

Mapletree Logistics Trust – 4.7% yield

I know a lot of you love Mapletree Logistics Trust.

I have a position too, but I don’t find it a compelling add at this price.

The problem with logistic properties is that longer term the moat isn’t that strong.

Location isn’t as critical as say retail or office properties. With logistics – as long as you’re near enough to the major transportation hubs, you’re good.

So they’re very hot now, but that could change in the future once new supply comes online.

And there’s big exposure to Hong Kong and China (almost 40% of AUM) as well that doesn’t justify the premium valuation to me.

That said, I know some of you love MLT, and if so don’t let me stop you from adding.

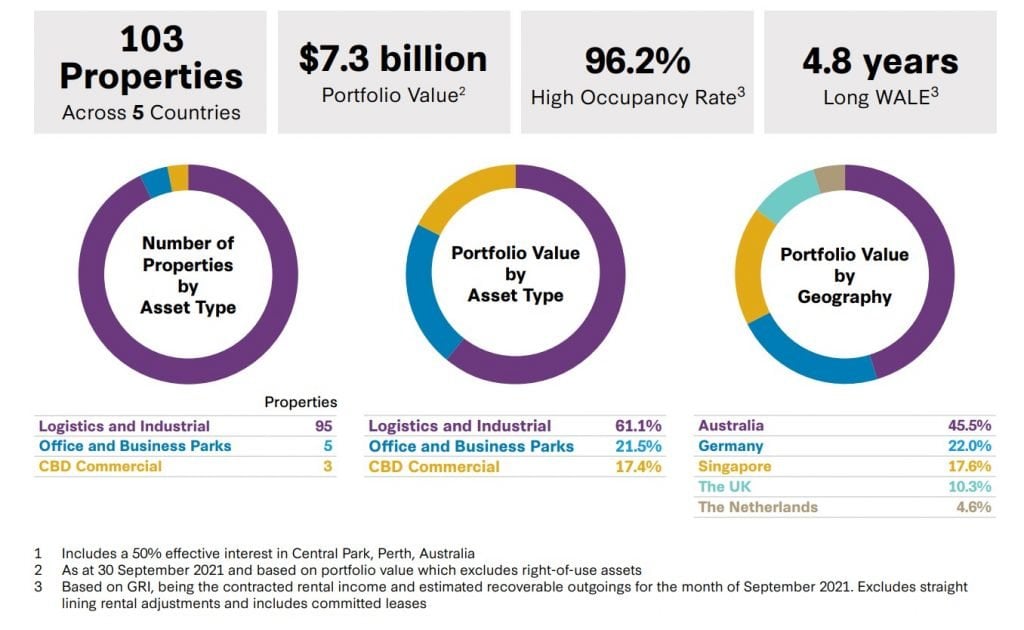

Frasers Logistics and Commercial Trust – 5% yield

Frasers Logistics & Commercial Trust is another fan favourite.

Many of you have written in to ask for my views on this REIT, and to share your love for it.

What I would say is that real estate is a local business. For a REIT with 45% exposure to Australia, you need to be comfortable with Australian exposure.

And the Australian economy is very commodities focussed, so a REIT like that gives you indirect exposure to commodities.

Again, it’s probably a decent buy, but not one for me. Don’t know enough about Aussie real estate to be confident in taking a position.

When to buy Singapore REITs in 2022?

Now, on to timing.

The market has priced an out of this world 8 rate hikes by Dec 2022.

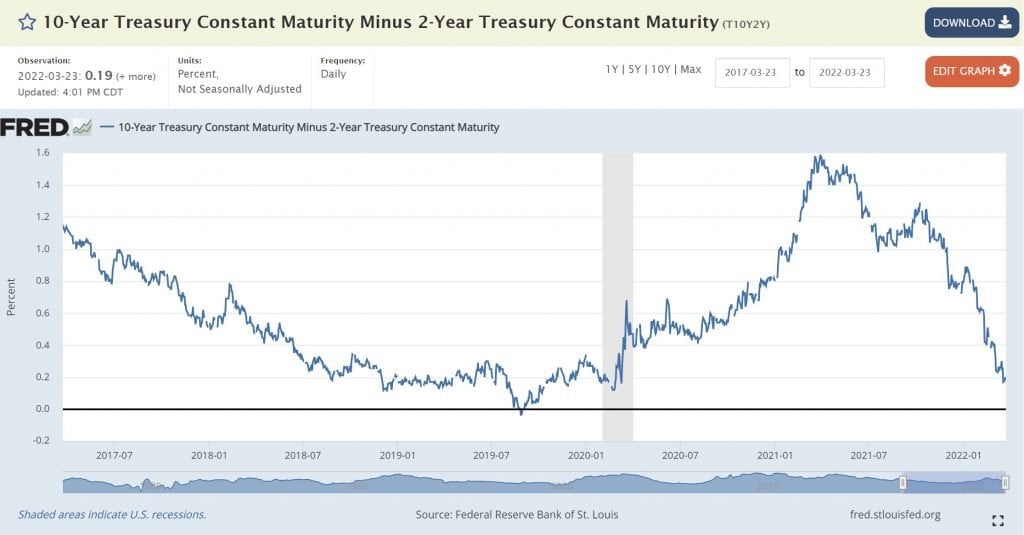

And the 2s10s yield curve is a whisker away from inversion.

Now I get that REIT valuations are reasonable at this price, for long term investors.

But if we do see 8 more hikes by end of the year, I can’t imagine what that would do to the global economy and real estate valuations across the board.

Historiy is worrying – Almost every rate hike cycle in the past resulted in a recession.

The only one that didn’t was 1994 – and there rising interest rates crushed US real estate valuations by almost 20%.

Closing Thoughts: Damned if you do, damned if you don’t

Investors are trapped between a rock and a hard place here.

Do you go to cash and have purchasing power eroded away by rampant inflation?

Or do you go into (or stay in) the markets in a year with 8 rate hikes and quantitative tightening?

Now everybody’s risk appetite is different.

What works for me, may not work for you.

Personally for me, I’m still holding onto all my long term positions. But my cash position is definitely on the high(er) side now that we’re in the more advanced stages of this business cycle.

There’s no denying that there are pockets of value here and there among individual names, including for S-REITs. For those, I’m happy to add as and when I see them (and you can see the names I’m keen to buy and my portfolio on Patreon).

But will I go all-in into the market right now?

Probably not.

Just like I don’t want to fight the feds during QE, I don’t want to be fighting them when they’re doing the opposite.

The only tail risk I see here – is if the markets think the Feds will not be able to contain inflation. If that happens, all hell is going to break loose, and we may see markets melt-up, but at the expense of fiat currency (value of paper money drops).

That’s going to be a 1970s style scenario, which let’s hope we don’t see.

As always – love to hear what you think!

Flash Promo for the Stocks MasterClass – 1 week only! Find out more here!

As always, this article is written on 25 March 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hey FH, really enjoy ur articles. Bought netlink years back after reading ur post about it and also loved their business. Currently it gives me the best returns on my portfolio although the position is on tiny side. Regarding MNCT, have u sold ur holding? For me, I have both MCT and MNCT and considering what to do next. Thanks.

Thanks Kid! Always great to hear from a long time follower.

I took profit in my Netlink last year and have been waiting forever to buy it back with rising interest rates. Haven’t had the opportunity so far though, but let’s hope we get one by the end of this rate hike cycle.

For MNACT, have not sold it. With the 1.1949 buyout and 3 cents dividend plus another 3 cents from now till Aug that works out to about 1.25 that is “relatively” risk free. So it’s about a 3 cent arbitrage to hold till Aug and take the cash vs selling on the open market now (1.22). Only risk is that the deal doesn’t close, but with the amended offer I think the odds are low.

So personally – will hold MNACT until deal closes and take the cash. But sometime this year I will add to my MCT position, to replace the MNACT position.

Hope this helps as a reference for your decision making. 🙂

What do you make of recent move higher in both SREITs and US equities? Seems counter intuitive to me especially post the hawkish tilt by Powell earlier this week.

Dead cat bounce or have we already bottomed out?

Yeah great question.

If you look at bond markets they’re definitely not buying this equities recovery. Move in rates this week was quite crazy.

I see 2 ways of seeing this:

1) Bond markets are right, this is a dead cat bounce – pretty self explanatory

2) Markets are worried Powell cannot contain inflation (calling his bluff) – If you think that Powell cannot contain inflation, what asset class do you go into now? Stocks – because that’s one of the few asset classes to inflation hedge. If you look at the 1970s stocks rallied very strongly throughout the decade, mainly because the value of paper money was falling, and stocks were one of the few things to hold their value (despite negative real returns).

I think (1) is more likely, but cannot rule out (2) as well. Which is why I still have all my long term positions in the market.

Dear FH

Lovely write up. I exited MNACT in phases between 1.11-1.21, am not comfortable with their portfolio plus the future with a lot of extraneous pressures. My entry price was under 1$ and got a cycle of dividends as a bonus. Happy to be out. I had bought a sizeable chunk of MCT in the 1.84 average range after the merger news drop. I feel it is fairly valued under 1.90 and I will add under 1.80. Opening up and Sentosa tourism boost to Vivocity is expected plus their office rents will show positive reversion. SG folks prefer SG asset focussed reits and this favours both MCT as well as CICT.

However, I am convinced that the best time to start adding would be H2 2022/eARLY 2023, courtesy FED triggered slowdown/recession.

This is the time to buy at 6-7 percent prospective yield. Currently the 10-year SG bond rate is nearing 2. We need a clear 4 percent more to take on equity risk. As regards Lendlease, it will be available under 70 after placements and equity dilution just like what happened with most REITS.

Frequent calls for money make REITS very dicey and unreliable

Garudadri

Great comment Garudadri, pleasure to read your thoughts as always.

I agree MCT looks fairly valued at 1.8+. I will probably add to replace my MNACT position in the low 1.8s if it goes back there.

Timing wise, I agree on your views as well. Fed hiking cycle looks very real, and the next few months should see very significant moves in yields that may flow over into REITs. If we do go back to the 6%+ range that would be a nice cue to add.

Lendlease REIT – if it goes under 70 I will likely be adding. In fact low 70s and I will probably open a position. 🙂

Hi FH. I have difficulty understanding 2) as that was not the narrative which drove the hawkish Fed / inflation dear equity sell off in the first place! Why does failure to contain inflation favor stocks? It’s only the commodity-focussed / hard real estate plays that will benefit in an inflationary environment. All things equal growth stocks suffer if the Fed has to keep hiking. Unless the equity market is thinking Powell chickens out and does not hike as much as he said he would?

Oh sorry I was referring to stocks more generally, not growth stocks. The narrative I shared would not benefit growth stocks.

Yeah if you want to explain why growth stocks are going up it will have to be what you said – the belief that Powell will not hike. But I think it’s fairly clear that Powell is indeed going to hike until something breaks, which makes this narrative not very plausible.

More likely than not we had a very oversold market that had a brief respite (due to a combination of technical factors like falling volatility etc), and when things moved to the upside it flowed over into the growth stocks. Hard to see this having legs for a sustained rally up without liquidity easing from the Feds. Could trade rangebound for a while though, as the liquidity factors will take some time to flow into equity markets. The move is very obvious in credit though.

Hi FH,

Would you know what the DPU for Lendlease Reit would be like after the injection of Jem into the reit and the equity fundraising? Thanks!

The pro forma they used was assuming EFR at 0.8+, so with their EFR at 0.7+ the pro forma numbers are all wrong.

I did some simple back of the napkin numbers and at $0.77 it will work out to about 5.8% yield, give or take.

Hi, total newbie to S-Reits. Do you think it’s still a good time to dip my toes into this in this rising rate environment?

Well, it really depends on your risk appetite. But I think for those with holding power, and who can average into the decline, it could be a good opportunity to build long term positions.

As always – stick to good sponsors and good real estate, and hold long term.