So I was reading this article from Beansprout recently.

The article is titled “UOB offers lowest dividend yield amongst local banks. Switch to DBS?”

It explains how UOB pays the lowest dividend yield compared to OCBC and DBS bank.

And the conclusion was that “Against this backdrop, we would still look at the Singapore banks more for their dividend yields rather than expectations for better earnings prospects in 2024…. Hence, DBS may appear to be a better option compared to UOB if we are looking to hold on to the Singapore banks for their dividend payment.”

Wow… a lot to unpack there.

Now the market is usually pretty efficient.

So the fact that you can sell UOB and buy DBS to get a higher dividend yield.

Strikes me as a “free lunch”.

If things were truly so simple – why is anyone still holding UOB stock at this stage?

So I decided to do a deeper dive, to understand why this is the case.

Dividend Yield and valuations of UOB compared vs DBS and OCBC Bank

I’ve summarised the relative valuations of UOB Bank vs DBS and OCBC below.

|

|

UOB |

OCBC |

DBS |

|

Price (as at 26 March 24) |

29.25 |

13.7 |

36.08 |

|

Market Cap ($ billion) |

48 |

61 |

91 |

|

Price/Book |

1.04 |

1.18 |

1.48 |

|

Dividend Yield (annualising latest yields) |

5.8% |

6.2% |

6.6% |

|

Payout Ratio |

50% |

50% |

50% |

|

Return on Equity |

12.7% |

13.3% |

16.9% |

At first glance, the conclusion above appears to be right.

It just looks like the market is pricing UOB wrongly here.

UOB is the smallest of the 3 banks – which means it should technically offer a higher dividend yield to compensate for the risk.

And yet its dividend yield is the lowest of the 3 banks.

Return on equity for UOB is likewise the lowest.

Looking at this table, you’d think that buying OCBC and DBS over UOB is a no brainer.

UOB’s share price has lagged OCBC and DBS Bank since 2020

Including dividends, since Feb 2020 (right before the COVID crash):

- DBS Bank is up 64%

- OCBC Bank is up 47%

- UOB Bank is up 33%

Again, makes you wonder why even bother with UOB – why not just buy DBS / OCBC bank.

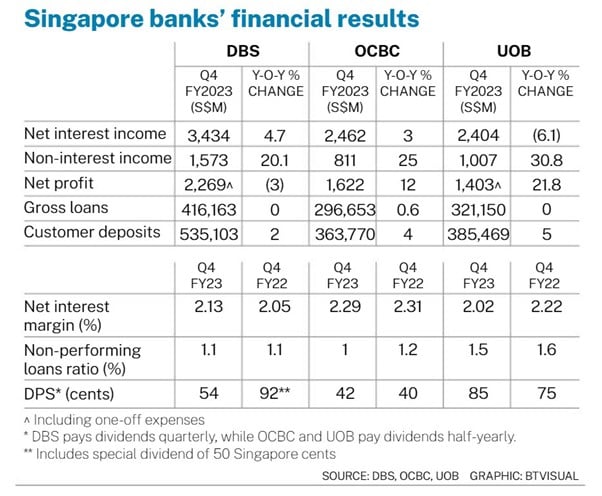

Comparing the latest Financial Results for all 3 Singapore banks

Here’s a great table from the Business Times that compares the latest financial results of DBS vs OCBC vs UOB Bank.

There are 2 areas that stand out – where UOB looks to be performing worse than OCBC and DBS:

- Net interest margin is the worst of the 3 banks

- Non-performing loans is higher

While the 1 area where UOB looks to be better than OCBC and DBS is:

- Non-interest income is growing faster

Let’s discuss each of these 3 points in further detail.

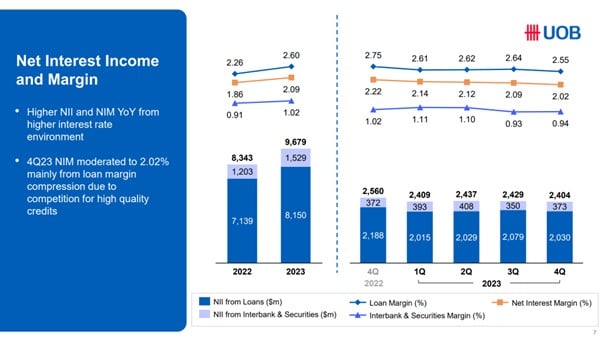

UOB Net interest margin is the worst of the 3 local banks

I’ve summarized the quarter on quarter net interest margin for the 3 banks below.

You can see how OCBC is performing the best (0.88%), while UOB is the worst of the 3 banks (-3.35%).

Absolute numbers tell a similar story.

UOB’s net interest margin of 2.02% is the lowest of the 3 banks.

On a year on year basis, UOB’s net interest margin is down 9%, while DBS or OCBC are reporting flat / improving net interest margins.

Why is UOB’s net interest margin so poor?

Which begs the question why this is the case.

This was what UOB has to say in their financial results:

“4Q23 NIM moderated to 2.02% mainly from loan margin compression due to competition for high quality credits”.

Competition for high quality credits.

In layman terms – let’s put it this way.

There is a pool of very high quality borrowers, that everybody knows will have no problems repaying the loan.

Think names like CapitaLand, Keppel, Singapore mortgages etc.

But because these guys have no problems repaying the loan, all the banks want to lend to them (while nobody wants to lend to the more risky borrowers).

And this pool of high quality borrowers is finite.

So that point that UOB seems to be making, is that DBS and OCBC are both also competing to lend to these borrowers.

To compete, UOB has had to lower interest rates, which means lower margins.

But funnily enough if you look at DBS / OCBC’s results, their net interest margins are holding up much better than UOB.

Does this mean that the best borrowers “prefer” DBS and OCBC, if given the same interest rates?

Or is it because UOB has to pay more to depositors to park money with UOB?

From the financial results alone it’s not very clear to me why UOB’s net interest margin is lower than OCBC / DBS.

If you have any theories I would love to hear it below.

UOB’s Non-performing loan is the highest

So UOB has the lowest net interest margin of the 3 local banks.

Funnily enough – it also has the highest non-performing loans ratio.

At 1.5%, it is much higher than OCBC (1.0%) or DBS (1.1%).

Makes you wonder whether it has something to do with UOB’s choice of who to lend to, and their lending practices.

Why is UOB’s non-performing loans so much higher than OCBC or DBS Bank?

Anyway I dug a bit deeper into the loan book of UOB vs DBS and OCBC.

Broadly speaking, nothing really stands out.

UOB has the highest Singapore exposure to Singapore at 48%.

UOB also has the lowest exposure to China at 17%.

Both are good things, because you would think Singapore loans are “safe”, and China loans are “not-safe”.

What stands out I suppose, is the higher South East Asia Exposure for UOB – 21% vs 8% and 14% for DBS and OCBC respectively.

Maybe the South East Asia loan book is more “risky”?

|

Loan Book |

OCBC |

DBS |

UOB |

|

Singapore |

41% |

46% |

48% |

|

Greater China |

25% |

29% |

17% |

|

South East Asia |

14% |

8% |

21% |

|

Rest of World |

20% |

17% |

14% |

What did UOB themselves say on non-performing loans?

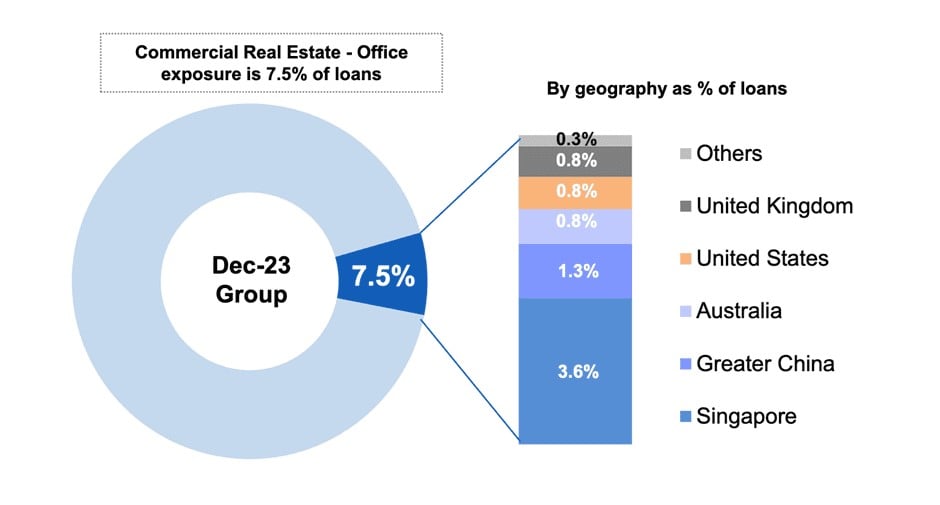

What UOB shared in their latest quarterly update though, is that of their commercial real estate loan portfolio, office exposure is only about 7.5% of its total loan book.

Of this loan book, half is Singapore exposure.

While the overseas exposure is backed by strong sponsors and largely secured by class-A office properties.

I suppose what UOB is trying to say is that their loan book remains strong, and to not be too worried about their overseas real estate exposure as it is a tiny fraction of the portfolio.

My take on the non-performing loans for UOB?

For what it’s worth – this is incredibly tough to evaluate as we don’t know exactly what kind of exposure UOB is holding on their books.

Big picture, the exposure doesn’t look fundamentally different from OCBC / DBS, which suggests it could be anything from:

- Bad luck – they just made that one big loan to that borrower who ran into difficulties

- Systemic – different loan approval practices may expose UOB to different kinds of risk

- Internal practice – or maybe they are just more “kiasu” in booking non-performing loans

Again, no easy answers here.

Outlook for UOB in 2024

For what it’s worth, this is UOB’s outlook for 2024.

UOB’s management expects low single-digit loan growth along with double-digit fee income growth.

This is expected to be further supported by the integration of Citigroup Thailand which is on track to complete by the second quarter of this year.

CEO Wee Ee Cheong remains upbeat on Southeast Asia despite a weak global economic outlook.

He believes that domestic demand, coupled with a tourism recovery and strong investment flows, should benefit the region and help the bank to grow its franchise further.

Nothing really unusual there, we see DBS and OCBC saying the exact same things about low single digit loan growth, and being “cautiously optimistic” on the economy.

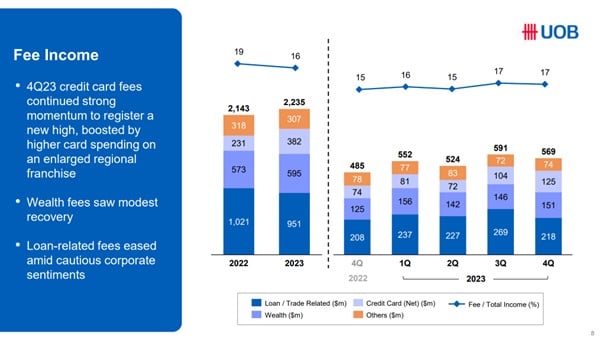

Non-Interest Income growing – driven by credit card fee income

The saving grace though, is that UOB’s non-interest income is growing well.

At 30.8% year on year growth, that’s higher than both DBS (20.1%) and OCBC (25.0%).

This is good.

But if you dive deeper into the numbers, you’ll find that a big chunk of that growth came from higher credit card fee income – up 69% year on year.

And this large growth was itself due to the acquisition of Citibank’s credit card business in South East Asia.

So it looks like a lot of this growth is inorganic from M&A, and not necessarily from the strength of UOB’s business.

But… it’s still the lending business that is the key

At the end of the day though, the core lending business makes up 70% of the income for all 3 local banks.

So it’s still the core lending business that moves the needle, and there UOB does seem to be underperforming.

UOB is just not as good as OCBC or DBS Bank?

Looking at all of the above would suggest that for some reason, execution wise, UOB just isn’t as good as OCBC or DBS Bank.

So I went back all the way to Jan 2008 to pull up the price charts.

If you had bought DBS, OCBC and UOB Bank on Jan 2008.

And held all the way till today, including dividends.

You would be up:

- 375% if you bought DBS

- 251% if you bought OCBC

- 177% if you bought UOB

That’s a crazy disparity in the performance between the 3 local banks.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

UOB Bank doesn’t even hold up well on the downside

Perhaps if UOB is “cheaper” on a Price to Book basis.

Perhaps it will drop less in a crisis?

I pulled up the charts from 2020.

If you bought in Jan 2020, and adjusting for dividends, by Oct 2020 you would have lost

- 19.4% if you bought OCBC

- 20.4% if you bought DBS

- 23.2% if you bought UOB

Again, the worst performer.

Putting it altogether – skip UOB, buy DBS / OCBC Bank?

So UOB pays a lower dividend than OCBC / DBS.

It has a lower return on equity, lower net profit margins, and higher non-performing loans.

It’s share price has underperformed OCBC / DBS since 2008.

And in a market crash like 2008, it actually goes down more than OCBC / DBS.

Boy… when you look at it this way, makes you wonder why you would even bother buying UOB.

When you can just pick up DBS / OCBC bank instead and get a higher dividend yield.

|

|

UOB |

OCBC |

DBS |

|

Price (as at 26 March 24) |

29.25 |

13.7 |

36.08 |

|

Market Cap ($ billion) |

48 |

61 |

91 |

|

Price/Book |

1.04 |

1.18 |

1.48 |

|

Dividend Yield (annualising latest yields) |

5.8% |

6.2% |

6.6% |

|

Payout Ratio |

50% |

50% |

50% |

|

Return on Equity |

12.7% |

13.3% |

16.9% |

Is it true that banks are only for dividend yield?

The final point I wanted to discuss, was this liner in the original article:

Against this backdrop, we would still look at the Singapore banks more for their dividend yields rather than expectations for better earnings prospects in 2024….

Is it true that Singapore banks today are more for their dividend yields than for capital gains?

Here’s the Price/Book chart for UOB going back to the 2000s.

Let’s say we get a cyclical upturn from Fed interest rate cuts.

And UOB goes back up to 1.3x book value, which was the 2022-2023 peak.

That implies a share price of $33.84, or a 14% return from here.

So there is some upside if things play out perfectly.

But… how likely is this?

But I suppose the point is how likely is this to happen.

Conventional logic being that with interest rate cuts and muted loan growth, the banks are unlikely to see a lot of upside, and base case is just the dividend yield.

It’s funny because I’m old enough to remember when investors thought of REITs as a “safe and boring” dividend play – not a lot of upside, but you can get that juicy dividend.

And we all know what happened after that.

The fact that everyone today thinks of banks as the “safe and boring” dividend play, with not a lot of upside but a juicy dividend yield.

Just makes me a bit worried.

Because in financial markets whenever something becomes consensus, you bet that it is priced in already.

And the money is to be made betting that the consensus view is wrong.

My views on the Singapore banks?

I can see 2 potential scenarios how the consensus view can be wrong.

First is if the Feds cut interest rates in 2H2024 into a resilient US economy. And whoever wins the US elections in November (Biden/Trump) spends a lot of money. This creates a new cyclical boom in 2025, and we see double digit loan growth for the banks, sending them to all time highs.

Second is if the economy weakens and unemployment starts to go up. The Feds cut interest rates faster than what is priced in. This impacts bank net interest margins and the banks sell-off.

For what it’s worth, I don’t have a strong view on which we are going to see.

I’m just saying that it’s helpful to question the consensus view.

As shared previously, I don’t have a big position in the Singapore banks today.

I think that if Scenario 1 above plays out, I probably make more money on crypto, US Tech, and commodities.

In Scenario 2, I make more money on REITs due to rapid interest rate cuts.

Which is why I don’t run big exposure to the Singapore banks today – but I run big exposure to REITs, crypto, US tech and commodities.

You can see my full personal portfolio on FH Premium.

This article was written on 28 March 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.