As many of you will know.

UOB One Account was one of the best high interest savings accounts before this.

As long as you credit your salary into UOB One, and spend $500 on UOB credit cards each month.

You could earn up to 5.00% on $100,000.

For cash that you could withdraw any time, and basically risk free given this is UOB and SDIC insured.

It was pretty much a no brainer before this.

Well – all that has changed now.

Because UOB has announced a cut in interest rates across the board for the UOB One account.

And after crunching the numbers, I’ve realised it’s actually a pretty huge nerf to the UOB One account.

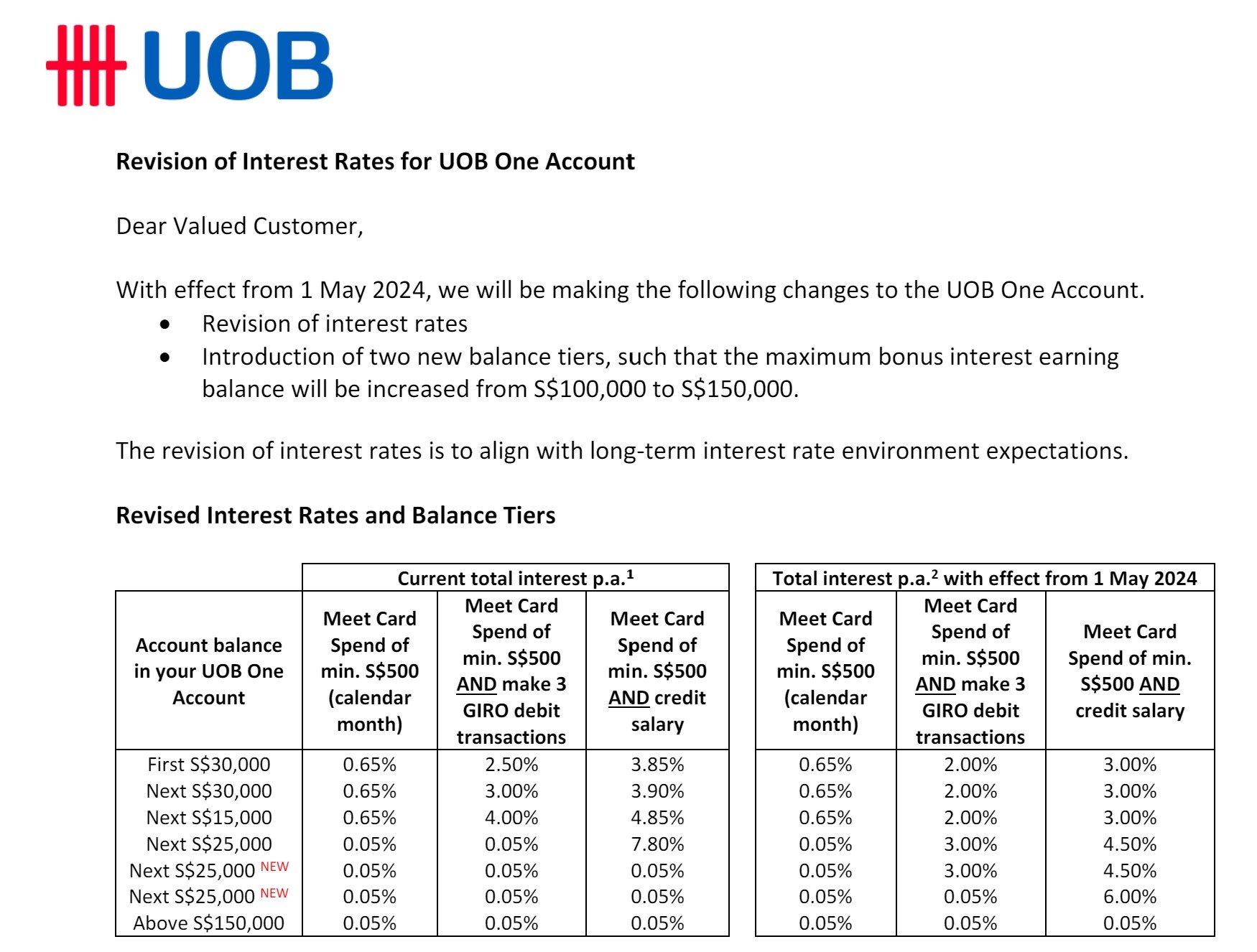

UOB One Account Interest Rates cut across the board

The full changes are extracted below.

This will take effect on 1 May 2024:

What is the effective interest rate after this?

It’s hard to figure out what exactly are the implications of this change just looking at the table above.

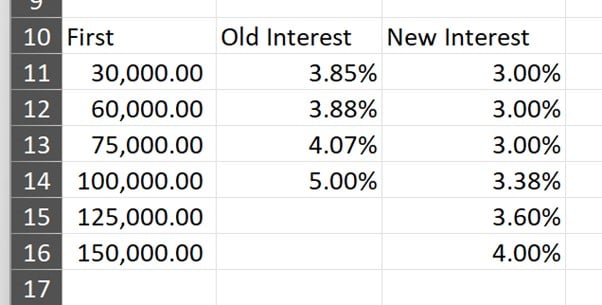

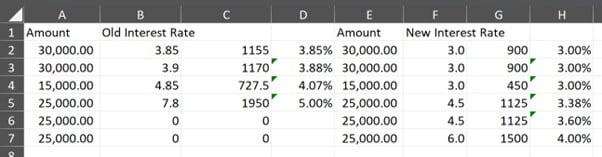

So I crunched the numbers, and these are the effective interest rates before and after.

Oof.

That’s a big drop across the board.

Before this you were getting 5.00% on $100,000.

Now – it’s 3.38% on $100,000.

You do need to top up to $150,000 to enjoy the 4.00% interest rates

And you need to top up to $150,000 to get 4.00% effective interest rates.

Because the next $25,000 after $100,000 earns 4.5%, and the next $25,000 after earns 6.0%.

So if you put less than $150,000, the effective interest rate drops quite drastically.

Is the $150,000 truly liquid? Withdrawing means a lower effective interest rate

So yes, the $150,000 can technically be withdrawn any time.

But if you do withdraw, it does drop the effective interest rate quite a bit, as you can see from the numbers above.

And at $75,000, you’re only getting 3.00% interest rate, when you can get 2.88% on Maribank with zero hoops to jump through.

Not sure UOB One Account makes sense anymore unless you top up to the full $150,000.

I was hoping this would have been an April Fool’s joke by UOB, but sadly that has not been the case.

Will I still use UOB One Account or switch to T-Bills / DBS Multiplier / OCBC 360 account?

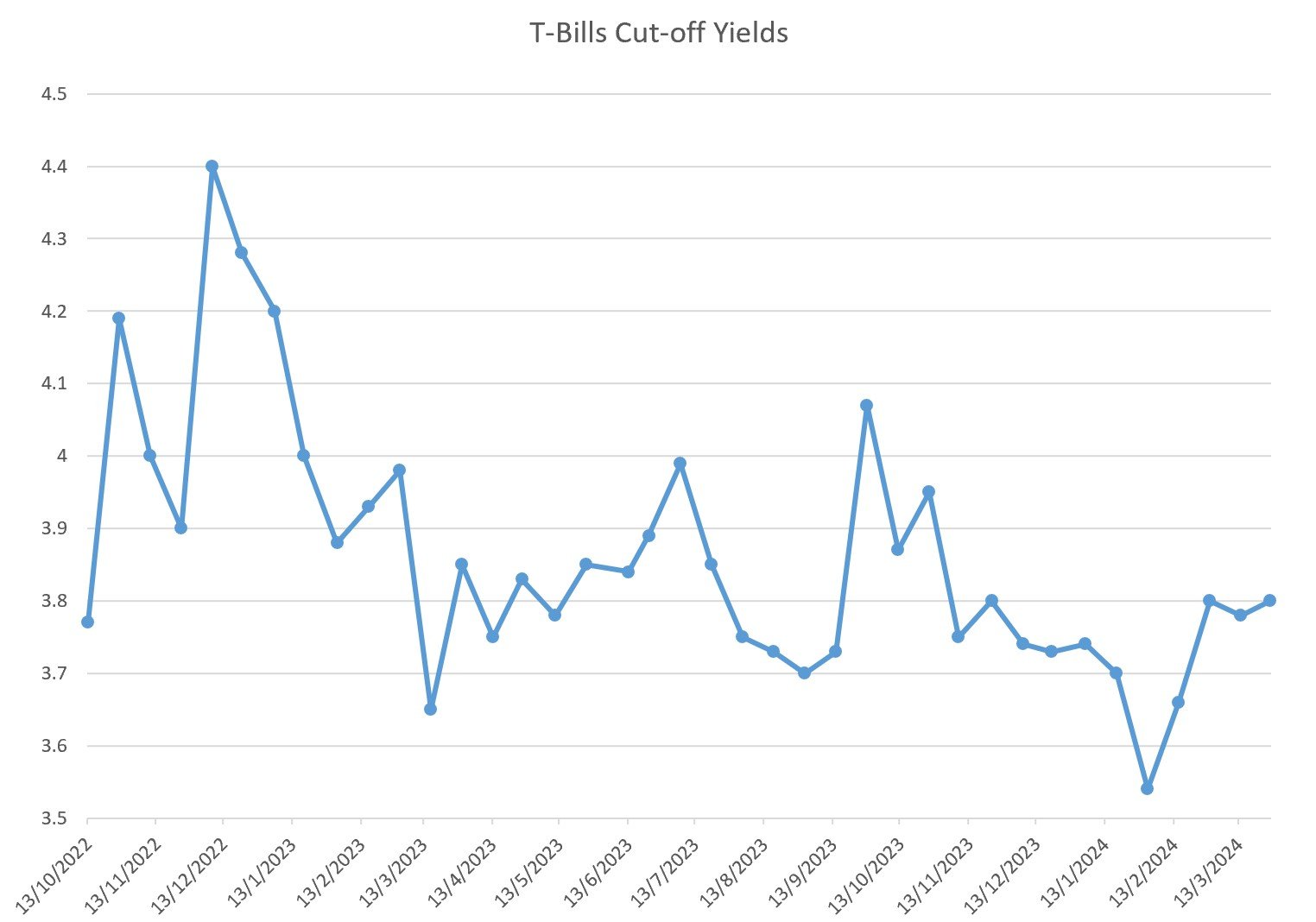

UOB One Account vs T-Bills

Latest 6-month T-Bills are paying 3.80%.

But that’s locked up for 6 months, and at 3.80% it’s still lower than UOB One Account’s 4.00%.

T-Bills will make sense if you don’t want to park the full $150,000 though.

But if you have $150,000 lying around, UOB One Account is probably still better.

DBS Multiplier is not much better than UOB One – many hoops to jump through

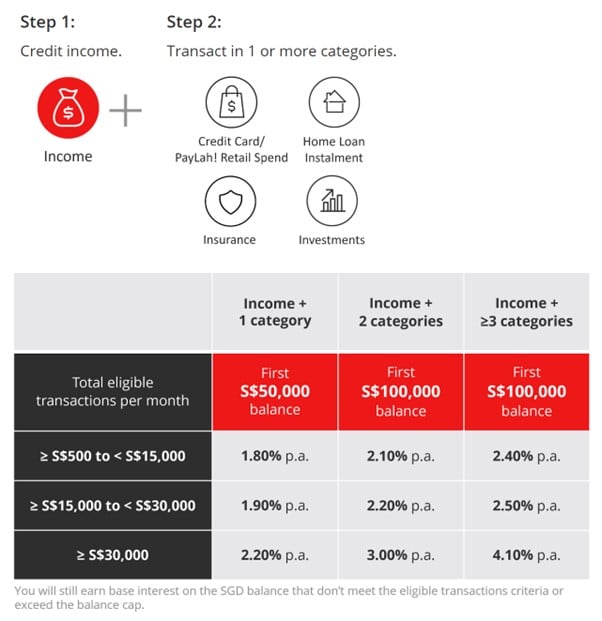

DBS Multiplier can pay up to 4.10% on your first $100,000.

However the conditions are not easy to satisfy.

You will need to credit your salary (or dividend income).

And hit 3 of the following categories:

- Credit card spend

- Mortgage payment with DBS

- Insurance

- Investment

AND – the total transaction across salary and the 3 categories above needs to be above $30,000.

That’s a lot of work just for a 4.1% yield – I might as well just park in T-Bills instead.

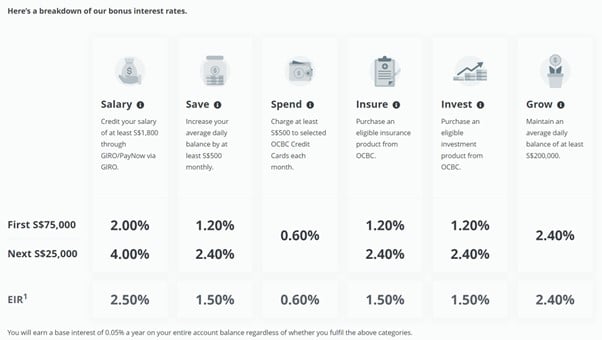

OCBC 360 account may be better than UOB One Account if you can fulfil the conditions

OCBC 360 account may be better than UOB One after this though.

If you credit your salary, spend $500 on OCBC credit cards, and increase your account balance by $500 each month – you’re getting 4.65% on your first $100,000.

But to increase your account balance by $500 each month is pretty annoying though, because you have to remember to do it each month, and that extra $500 after $100,000 is only earning 0.05% interest.

That said if you do all of the above, and you insure / invest with OCBC, you can get up to 6.15% with OCBC.

If you both insure and invest with OCBC, that goes up to 7.65%.

So if you do all your banking with OCBC and can hit all these conditions, this is probably better than UOB One.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Will I continue using UOB One Account or switch to T-Bills / DBS Multiplier / OCBC 360 account?

I’m a sucker for convenience.

My banking is set up such that all my banking and credit card spend is via UOB today.

Shifting all that to OCBC, is just too much hassle for this horse.

Probably doesn’t make sense when the incremental increase in interest rates is not that big

This is how banks preserve their net interest margin (and dividend)?

I suppose this is what the banks are counting on – that it’s too much hassle for us to switch.

It’s funny because as investors you can’t have your cake and eat it.

Everybody loves bank stocks these days for the 6% dividend yield.

How is that dividend yield going to be sustained in a climate when lending interest rates are going down?

Well we see exactly how here.

Banks will have to cut the interest rates they “borrow” at from depositors – to preserve their net interest margins.

What will I do? Continue using UOB One Account?

Having to top up another $50,000 just to get a lower 4.00% is pretty annoying.

But parking in T-Bills and sacrificing the liquidity for a lower 3.80% interest rate doesn’t make sense too.

So I’ll probably continue using UOB One Account for now.

But I think you do have to recognise that the path for interest rates going forward is down.

UOB One Account is cutting interest rates today, and you really cannot rule out another cut down the road.

Which is why I’ve been moving cash into REITs and tech stocks / crypto.

This is a big change from 2022 when the Feds are hiking 0.75% per meeting.

You can see my full portfolio and what stocks / REITs I’m buying on FH Premium.

This article was written on 2 April 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Thanks for this article! This information is not on UOB website yet, though its reported in the Straits Times which I missed. I was considering to transfer from OCBC to UOB, attracted by the formal higher interest! No wonder UOB side doing promotion now!

No worries, hope it helps! Yes with the drop in rates I don’t think UOB is much better than OCBC any more, may not be worth the hassle to switch. 🙂