As shared over the weekend, I’ve been doing a lot of thinking about inflation recently.

And I came across 2 fantastic pieces of material on this.

One from Credit Suisse’s Zoltan Pozsar, and another from Blackrock.

I’ve attached both reports to this article, both very high quality reads.

If you have some time this week, I do recommend reading in full (especially Zoltan’s piece).

You may not necessarily agree with them, but it does provide important colour in this climate.

Summary of Zoltan and Blackrock’s views on the causes of inflation

In any case, let me summarise the views from Zoltan and Blackrock on the causes of inflation.

Zoltan

The way Zoltan sees it, low inflation over the past decade was built on 3 fundamental pillars:

- Cheap immigrant labour

- Cheap goods from China

- Cheap Russian gas powering EU

(1) has changed because of tighter immigration policies after Trump and COVID globally, and distortions from COVID (eg. Early retirements, shift in type of workers required).

(2) has reversed because of the US-China trade war that started with Trump, and continued under Biden. China’s zero-COVID policy is not helping too.

(3) is no longer true because of Western sanctions on Russia after the Ukraine war.

All of which has been exacerbated by geopolitical risk, due to the developing conflict between China and US.

And as the cost of living goes up, the bargaining power of labour goes up. So we see increasing cases of workers unionizing and going on strikes globally to demand for higher wages.

A classic case of inflation getting entrenched, and eventually building into a wage-price spiral.

Blackrock

Blackrock identifies many of the same concerns as Zoltan.

They narrow it down specifically to 2 big points:

- Spending patterns have shifted post-COVID

- Shift from services to goods

- Shift in travel patterns

- Shift in living patterns

- Hiring difficulties

- People have left the workforce after COVID

- Immigration policies are tight

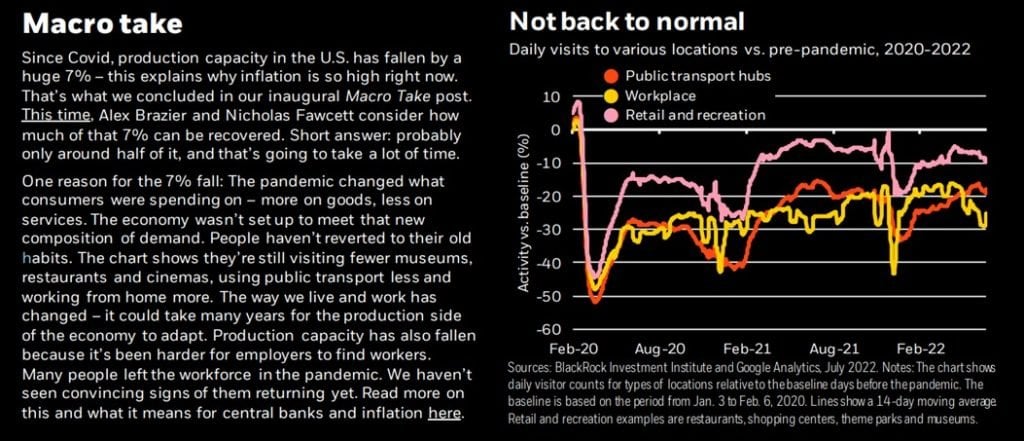

For (1) – COVID has brought about a structural shift in spending patterns.

Consumptions has shifted away from services to goods, travel has fallen across the board due to work from home trends, while working from home has led to shifts in where and how people live.

While it was originally thought many of these trends would be transitory, it’s become quite clear that a lot of these trends are structural.

COVID has changed the world and how we live, for better or worse.

At the same time, our existing supply chains are geared up for the pre-COVID world.

As the world changed rapidly post-COVID, production and supply could not keep up with the changes in demand patterns.

This is particularly pronounced in the labour market, where almost every country in the world is facing labour undersupply at the moment.

Why exactly this is the case is not very clear, but ask any employer out there and you will realise this is a very real problem.

Blackrock pins it down a combination of skill-gap, and workers leaving the workforce / retiring early after COVID.

How to solve the problem?

If you accept that the issues identified above are generally true, then there are only 2 possible solutions to the problem.

Just like with any disease, you can either (1) treat the underlying problem, or (2) treat the symptoms.

Or more specifically:

- Treat the underlying problem by:

- Increasing supply

- Changing demand patterns back to pre-COVID

- Treat the symptoms

- Reduce demand

- Raise prices

Treat the underlying problem

If the underlying problem is caused by supply side issues, and changes in demand patterns, it stands to reason that the solutions are:

- Increase supply

- Change demand patterns back to pre-COVID trends

It’s quite clear that (2) is not going to happen.

The world, for better or worse, has changed post-COVID.

Some trends like work from home, video-conferencing, increased consumption of goods vs services, they’re just here to stay.

Which leaves (1).

I agree that if there is meaningful effort to increase supply and solve supply side issues, this will solve the problem of inflation.

However, most of these supply side issues cannot be solved easily and quickly.

Increased investment into commodities capex, increasing labour supply, solving geopolitical disruptions between China/Russia and US/Europe – none of these lend themselves to easy and quick solutions.

And to date, we see very little emphasis on actually solving the underlying problems.

Treat the symptoms

The other solution of course, is to treat the symptom.

Again there are 2 ways of doing it:

- Reduce demand

- Raise prices

(1) is what the world, and the Feds, are trying to do right now.

By raising interest rates, you hit the interest rate sensitive parts of the economy, reducing demand.

If demand can drop back down to meet the current level of supply, you bring down inflation in the short term.

The problem though, is that this is easier said than done.

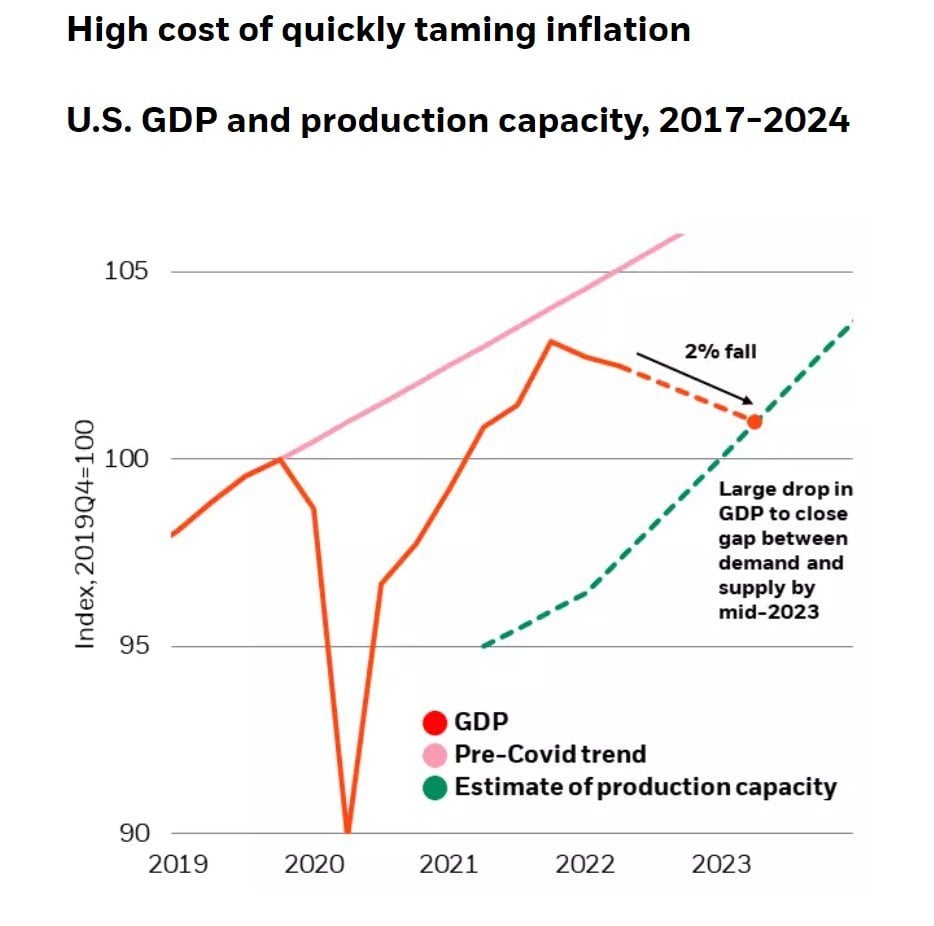

From the Blackrock report:

If they go for the first, that would mean crushing demand and pushing up unemployment. In fact, since it takes time for rate raises to take effect, if the Fed wanted to get inflation back to 2% within two years, that would require rate rises that cause GDP to fall by a little over 2% in total (as the High cost of quickly taming inflation chart shows). That’s 1.5% on top of the estimated 0.6% fall already seen in the first half of this year. That could push the unemployment rate past 5% – meaning up to 3 million additional people out of work.

Simply put, the cost of taming inflation by crushing demand, is going to be very high.

So high that it is not clear if the Feds (or Biden) have what it takes to follow through.

Which of course leaves another solution – live with inflation.

If you accept that 9.1% headline inflation is too high.

What about 5% inflation?

Would 5% inflation, with a 1-2% growth in nominal GDP, be acceptable?

My views on inflation?

For the record, I don’t think my summaries of Zoltan/Blackrock do them justice.

If you have some time this week, I do encourage you to read both in full.

I think whatever the case, one needs to recognize that the world economy is unbelievably complex.

And trying to predict how such a complex system with evolve going forward with limited information, is always going to be educated guesses at best.

Mid Term (3 – 5 years)

In the mid term, I think the Feds will choose to live with inflation.

It’s just the outcome that makes the most sense to me here.

The only sustainable solution in the mid term is to increase supply.

Yet supply cannot be easily increased for the re asons we discussed above.

It will take time, years even, and it will require bipartisan support in the US, and a global coordinated effort to invest more into production capacity.

We’re not seeing any of that just yet. Even if we do, they will take years to bear fruit.

New oil rigs and factories do not spring up overnight.

So as we go down this path of crushing demand via higher interest rates, at some point in time, the pain will be too much to bear, and the Feds will probably choose to live with inflation.

So for mid term investors, it would pay to start thinking of how to invest in a more inflationary world.

Some brief guidelines for me are:

- Elevated cash positions (higher short term interest rates + optionality)

- Focus on dividend plays (income + more stable mature businesses with pricing power)

- Focus on real assets that are not so sensitive to interest rate movements (commodities, high quality real estate, potentially gold/crypto)

Short Term

The short term is where it gets tricky.

Blackrock’s view – is that the Feds will continue to hike this year, with a Fed pivot early next year, after which we just live with higher inflation.

Zoltan’s view – is that the Feds are serious about inflation. And they may go as high as 5-6% on the terminal this cycle, before they start cutting.

Latest US Jobs report

The latest US Jobs report is not pretty.

To summarise:

- Nonfarm payrolls up by 528,000 in July, larger than the average monthly gain over the prior 4 months (+388,000)

- Month on month hourly earnings up by 0.5%

What this shows, is that despite all the doom and gloom, the US economy, and the US labour market specifically, is still very strong.

It’s why I’ve been saying for a while that all the talk about a US recession is too early.

Until month on month earnings start going down, it is not likely for the US to enter a meaningful recession.

Month on month hourly earnings is a key metric the Feds will be focusing on when deciding whether to pivot, and for now at least, the number shows no signs of rolling over.

My Personal View on the short term?

Gun to my head – I think the markets are overly optimistic on how quickly the Feds are going to pivot.

The market thinks we are going to 3.5-3.75% on the fed rate, and then we go down early next year.

I think we go to 3.5%-3.75% on the fed rate, and then we (a) stay there, or (b) go higher.

But again like I said, the short term call is not an easy on to make, and I could well be wrong on this.

If I am wrong, I will just start buying when the Feds make clear that they are pivoting, and I buy then.

But for investors who are not keen to market time, I think it would make sense to at least account for the possibility that this decade might be one that is more inflationary in nature.

And it may make sense to think about how one’s portfolio would fare if we do get a 3- 5 year period where inflation stays at the 3-5% range, while interest rates stay elevated.

As always – love to hear what you think!