Happy National Day everyone!

It’s National day, so I figured what better way to celebrate than to talk about something all Singaporeans love: Property.

COVID19 has been a gamechanger for the entire world. Entire industries, investments and asset classes have been turned upside down.

Will the same happen to Singapore house prices?

It’s the first time we’re doing a property related piece on Financial Horse, so I’m quite keen to see if you like it. Let me know in the comments below! We’ve also started a small Facebook Group – Singapore Property Investments. If you’re interested in Property Investing and want to join the discussion, hop on into the group!

BTW – It’s the one year anniversary of the FH Course, so we’ve launched a big promo with discounted prices and freebies for both the FH Course and REITs MasterClass. Find out more here.

Basics: What drives house pricing?

House prices are driven by supply and demand.

If supply is greater than demand, prices fall. If demand is smaller than supply, prices fall.

To estimate price trends, you therefore need to forecast demand and supply.

Do note that the discussion below is for private residential housing in Singapore. Public housing is slightly different because it’s ultimately controlled by the government, but most of the broad trends here will be applicable as well.

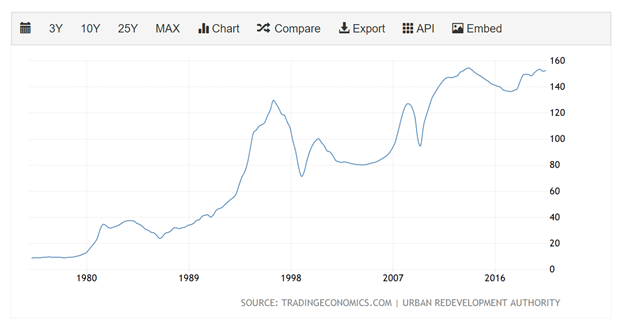

Overview of Singapore house pricing trend

I’ve set out the long term chart of Singapore housing prices above.

As you can see, it’s a very cyclical industry.

It’s separated into short-term cycles (prices go up for a number of years, then go down for a period shorter than the up cycle), and a longer-term cycle (leaving aside the short-term declines, price have been going up steadily since the 1980s).

Couple of big crises along the way that derailed this long-term price trend:

1980s – Pan Electric crisis – Things were bad, but eventually picked up in 1987, and it began a massive 10 year bull run until the Asian Financial Crisis.

1997 – Asian Financial Crisis – Probably the biggest crisis for property prices in Singapore history, you can see the massive decline in property prices from 1997 until 2000. Lots of businesses were wiped out during this period.

2003 – SARS – After the Asian Financial Crisis, there was a short-lived recovery, until 2003 when the SARS epidemic struck.

2008 – Great Financial Crisis – SARS was controlled relatively quickly, so the market bounced back fuelled by easy US liquidity, driving prices parabolic heading into the Great Financial Crisis in 2008.

2012 – Cooling Measures – Drastic measures taken by the Federal Reserve meant that the 2008 GFC was a short one for global asset prices. Interest rates taken down to zero are a powerful tailwind for asset prices, so prices rose drastically. In 2012, the Singapore government stepped in with cooling measures to prevent housing prices from running away. This caused a decline in prices, until around 2017 when the en bloc fever started heating up again.

2020 – COVID19 Crisis – That takes us to 2020, where we have the COVID19 crisis playing out as we speak. How will COVID19 impact house prices in Singapore?

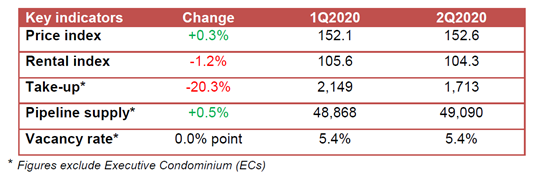

Overview of Price Trends up to 2Q 2020

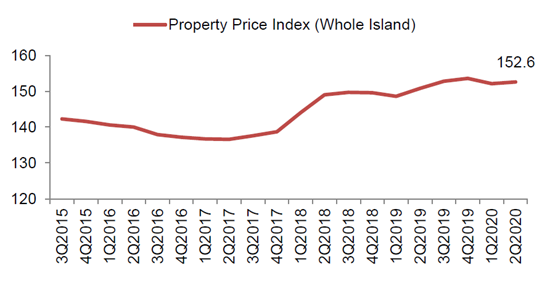

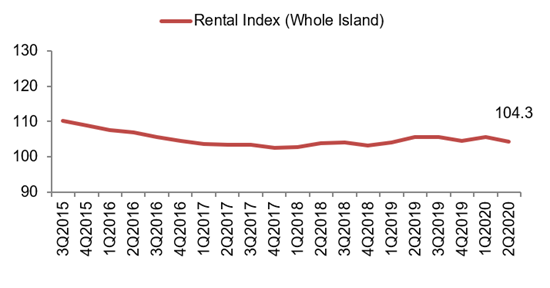

At a high level – sale prices have been very steady, rental prices have been ticking down, and transaction volume is down.

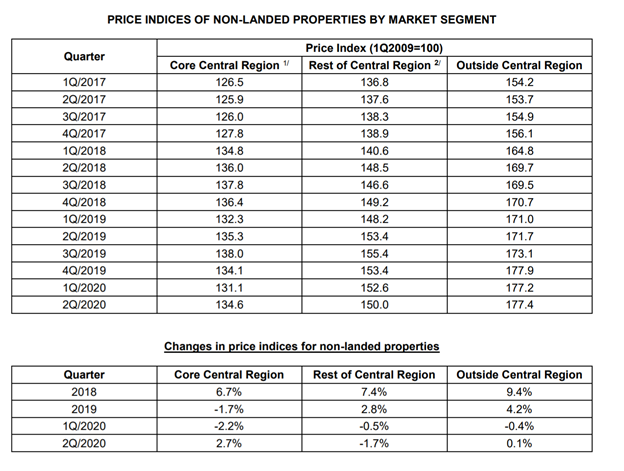

The table above provides a more granular breakdown. Prices in the Core Central Region have been coming down since 2019. The rest of the Central Region is down but isn’t as bad. While outside Central Region has been the most resilient thus far.

Property Sale prices have been generally quite steady, but what’s worrying is that the rental index has been gradually ticking down for a while now.

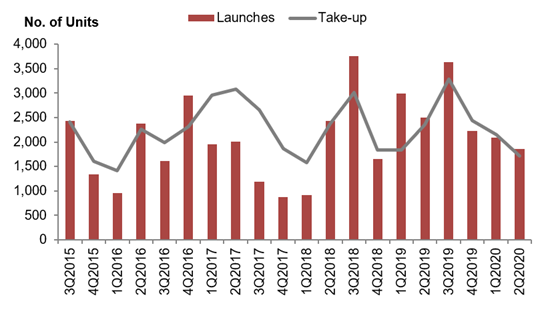

Number of private housing units launched and sold by developers (excluding ECs)\

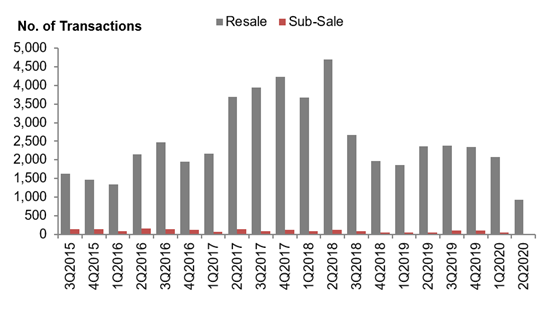

Number of resale and sub-sale transactions for private residential units (excluding ECs)

Transaction volume of new houses has dropped, but this could also be due to the fact that developers are starting to control the supply they release onto the market.

Likewise for resale houses, where transaction volume is down post-COVID.

Interpretation of data

It’s hard to interpret this data because it’s so early on in this COVID19 crisis.

Q2 was the eye of the storm, when we had a 2 month “circuit breaker” and massive government stimulus. This cut transaction volume drastically, preventing true price discovery. At the same time, sellers would be holding out for better prices and adopting a wait and see attitude.

What is clear though, is that up till Q2 2020:

- Sale prices are steady

- Rental prices are on a small downtrend

- Transaction volume has declined massively

Demand

What will demand look like going forward?

There are 3 big factors to think about:

- Additional Buyer’s Stamp Duty (ABSD)

- COVID19’s impact on incomes

- Rental Demand

Additional Buyer’s Stamp Duty (ABSD)

Profile of Buyer |

ABSD Rates on/ after 6 Jul 2018 |

|

Singapore Citizens (SC) buying first residential property1 |

Not applicable |

|

SC buying second residential property1 |

12% |

|

SC buying third and subsequent residential property1 |

15% |

ABSD has been around for a while now, and the rates are set out above.

12% on your second property, and 15% after that.

12% additional stamp duty on a million dollar (or more) purchase is no joke, so it’s definitely had a big impact on demand.

The big question is whether the government will remove ABSD if the situation gets bad.

I don’t profess to know how the government thinks, but my hunch is that they will wait and see how bad price declines get. If we get a bad decline (eg. >20%), they will ease back on the cooling measures. If the decline is mild (<10%), they might leave it untouched.

Which leaves a sweet spot of 10 – 20% declines where it’s not so clear what the government would do.

Big uncertainty here.

COVID19 – Impact on consumer incomes

We’ve said many times on this site that COVID19 has had a very uneven impact on the economy.

You get the guys who work in hospitality or airtravel who are going through the worst downturn, ever.

Then you get the guys in tech or eCommerce who are going through the biggest growth in market share ever. We’re talking years of growth compressed into 3 months.

So there are people who are doing very well, and people who are doing very poorly.

The key question then – Are there more people who are better off, or are there more people who are worse off? Ie. Is the average consumer now better or worse off compared to pre-COVID?

Given how the Singapore economy is structured, my take is that it the average consumer will be worse off.

The current Singapore economy is heavily tilted towards old world industries – oil, shipbuilding, real estate, airlines, tourism etc. That’s the eye of the storm for COVID19. The tech sector in Singapore will do well, but it simply cannot make up for the impact on those old world industries.

What about government stimulus?

The wildcard here, is government stimulus.

In 2020 so far, the Singapore government has injected close to $100 billion in stimulus into the economy. Some of this came via wage subsidies, some via free cash to everyone.

The point is – This definitely helps.

The economy doesn’t care where money comes from. Regardless of whether money comes from someone spending their savings, or from the government drawing down on reserves, it’s still money, and it’s still spending. So as long as the government can keep spending, it will offset a big chunk of the COVID19 economic impacts.

The question though, is whether the government will keep up the current pace of stimulus.

I’m not so sure about this one.

I think the March wave of stimulus was a unique once off – broad based stimulus to prop up the economy that was going through a lockdown.

But now that the full impact of COVID19 is emerging, to persist with the same type of stimulus would be artificially propping up zombie companies, that will never survive on their own.

It can be done, but it will perpetuate inefficiencies in the economy, and come back to haunt us eventually.

So I suspect that at some point, the stimulus has to become more structural in nature – focusing on shifting the economy towards industries that can continue to survive during and post-COVID.

This is good long term, but short term, is will mean higher bankruptcies and unemployment as the economy shifts gears.

This will hit consumer income short term.

Rental Prices

Rental prices will go down. We’re seeing that in the price trends, and I think that will continue in 2021.

The argument goes like this – the overall stock of houses available for rent is relatively stable short term. If you have 2 investment houses that you rent out, and rental prices go down, are you really going to convert one into a vacation home? No, you’re probably just going to suck it up and accept lower rents.

This means that the supply of rental houses is fixed short term, which means demand will be what drives prices.

And demand will likely go down, because nobody can come into Singapore anymore.

It’s just super hard for anyone to get an employment pass to come into Singapore right now with all the COVID restrictions. And at the same time, a lot of expats based here are gradually being recalled to their home countries as MNCs downsize and cut back on costs.

Rental prices are fixed on the margin, so when less people rent houses, demand drops and prices drop. This affects demand for investment properties, and pricing.

Where is demand coming from?

So where will new demand for houses come from? Probably one of the following:

- First time buyers – New couples or singles who are buying their first home

- Upgraders – Buyers upgrading from a HDB or existing Condo

- Decouplers – Couples who decouple and hold 1 property in each name

- Rich and wealthy – The well-off who are cash rich can simply pay the ABSD charges if they find a good property at a great price

- Foreigners – Foreign money coming into Singapore. Short term, I think this will mainly feature in the higher end, premium market. ABSD is a real deterrent for them though – they’re paying 20% on each property.

Supply

What about supply?

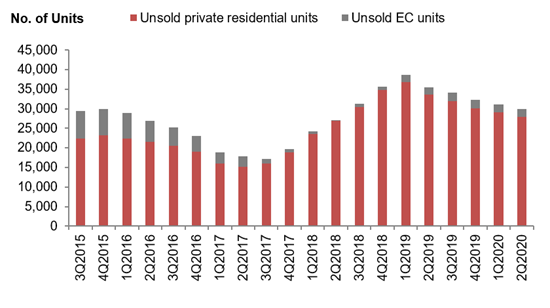

Total number of unsold private residential units in the pipeline

Pipeline supply of private residential units and ECs (with planning approvals) by expected year of completion

To sum the charts above:

- Homes that have been built but are unsold – There’s a fairly big stock of unsold new homes. About 30,000 as at Q2 2020.

- Homes that are still in construction – There are also a large number of new houses launching over the next 3 years. New launches are probably going to be delayed due to the foreign worker situation, so there’s some respite there.

- Private Resale – This can be split into 2 groups: (1) owners who voluntarily sell their house for personal reasons, and (2) owners who are forced to sell due to cash flow issues / foreclosure by bank.

3 in particular is interesting. The government has implemented mortgage deferment due to COVID19, so anyone who is in financial difficulty can defer paying their mortgage up till 31 Dec 2020.

The problem with this, is that while it helps short term cash flow, it doesn’t address the longer term solvency issue. The money that is owed doesn’t go away, it’s still due and owing as at 1 Jan 2021.

All it does is give the homeowner time to find an alternative source of cash flow. Given how COVID19 is shaping up to be a marathon rather than a sprint, I’m not so optimistic about the recovery here.

If someone is in deep financial difficulty now, it’s hard to see that miraculously changing by Jan 2021.

Long story short, there’s still a big amount of supply from new homes coming into the market. Resale is tricky, but my guess is that it will trend up as well as this crisis continues to play out and mortgage deferment runs out.

Why I think property prices will go down

To sum up – short term, demand will go down, while supply will continue at its current pace of increase.

Accordingly, I think that property prices will go down.

It’s hard to assign a number, but gun to my head, I would say maybe 10% to 15% decline in the index by the time COVID19 is all over.

The high end, and core central region properties probably suffer more. While the cheaper, suburban properties probably suffer less.

It probably wouldn’t be as bad as the Asian Financial Crisis or 2008 because this time around, we never had that massive runup in property prices heading into the crisis. The cooling measures worked very well to prevent rampant speculation in the market. And without the bubble, blow off top, you wouldn’t get a big collapse as well.

But of course, forecasting things like this never works out well.

There are 3 big wildcards here:

- COVID19 situation – My base case assumes a vaccine in early 2021, and mass production by second half of 2021. If this timeline is accelerated, or COVID19 comes under control far earlier than expected, then all bets are off.

- Government Stimulus – If the government keeps up broad based stimulus to prop up the entire economy, then consumer incomes may not be impacted that badly. This will help stabilize prices.

- Government adjusting cooling measures – If government removes or dials back on ABSD, that could unleash a lot of pent up demand from cash rich Singaporeans.

So I’ll be watching these 3 factors very closely going forward, for signs of change.

That said, all this is the immediate, short term.

Mid to longer term, I’m still pretty bullish on Singapore residential property.

Don’t expect the 7% growth back when Singapore was an Asian tiger, but I think 2 to 3% long term growth should still be sustainable. We’re still a political and financial oasis in the region, and mid to longer term, we’ll continue to remain attractive to foreign investors. That’s bullish for house prices.

Closing Thoughts: Impossible to time the bottom

Most of us are all stock investors here, so I’m sure you get what I mean when I say – It’s impossible to time the bottom.

I suspect the same thing will happen here.

Even if I am right and property prices go on a downtrend into 2021, it’s going to be impossible to time the bottom perfectly.

And if it’s impossible for stocks that you can buy at the press of a buttom, it’s going to be even harder for property where you need to find one you like (via physical viewings!), sign a S&P, arrange a mortgage, get lawyers to handle the deal, and wait for a 10 week completion.

So like how it works with stock investing – don’t get too greedy.

If you find something you like, and it’s at a fair price, just get it. Sure prices may continue going down after, but nobody times the bottom perfectly anyway. And just like stocks – as long as you bought something you’re comfortable holding long term, then just keep on holding, and have faith in your original thesis.

I would really love to hear what you guys think though.

Please, please share your thoughts below, whether you agree or disagree. Where do you think Singapore house prices are headed in 2021?

Happy National Day everyone! Enjoy the long weekend!

BTW – It’s the one year anniversary of the FH Course, so we’ve launched a big promo with discounted prices and freebies for both the FH Course and REITs MasterClass. Find out more here.

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Homes that have been built but are unsold – There’s a fairly big stock of unsold new homes. About 30,000 as at Q2 2020.

Maybe a slight mistake?

this 30k number of units are under construction and not units that had finished building and are vacant now.

Thanks for pointing this out! 🙂

Hello Finance horse,

Great article as alsways. I agree with you that property price should trend downward.

Just like to add that recently National Wage Council are going to meet again soon to discuss and issue guidelines. Coffee shop speculation is that they might propose CPF rate cut to help employer save cost which hopefully will lead to lesser retrenchment. If this coffeeshop speculation is correct, then it will affect a lot of SG ppl who are using their CPF to service their housing loan. This should lead to lesser demand and likely lower house price.

Another point is that we expect more bankruptcy in 2H 2020/ 1H2021. When folks go bankrupt, their property might be force into a force sales situation too.

Last but not least, interest rate is likely to stay low for a few years, guess this might be the only positive thing for house buyer and also folks that are still servicing their housing loan.

Cheers

Hi aaa,

That is really interesting information, thanks for raising this. If that is true, it could have pretty big knock on consequences on consumer income, and have real impact on the economy. Definitely worth watching closely.

I’m expecting bankruptcies to trend up too. But it really goes back to government measures. If they do nothing, we’ll have a repeat of the AFC style situation. But I dont’t see them doing nothing. And the difference between them doing a little vs doing a lot is going to be the difference between night and day as COVID19 plays out.

So it’s also tough to predict with a high level of uncertainty what happens going forward.

Great comment, appreciated!

Hi FH. With interest rates so low, a good window has opened up for those lucky enough to be in less affected sectors. This would be civil servants (bonus cut but job still safe) and those working in tech as you correctly pointed out. Wondering what your thoughts are on how long it generally takes the banks to pass on interest rate cuts to mortgage rates? With interest rates at historic lows, the cost savings are actually quite substantial, especially if you manage to fix a good rate for the first few years. So far the longest in the market is DBS @ 5 years at 1.5%.

Also wondering what your thought are on COE prices. Was expecting prices to crash post CB, but surprise surprise, they have held up!

I think over the next 6 to 12 months, we’ll see interest rates trend down until they hit a bottom. I frankly don’t see interest rates every going up for the next 3 years, so they’re probably going to stay there for a while. This would traditionally be a powerful tailwind for property and asset prices – Provided that consumer income doesn’t get impacted too badly by COVID19.

COE is interesting. I was tracking a number of other countries, and post-lockdown, car sales always spiked because people were afraid of taking public transport. I was expecting the same to happen here, and it’s held up so far. Although to be fair, the government did defer some of the lockdown supply, so technically the supply this year was cut, which pushed prices up too.

The big question is what happens next. Do they stay elevated, or do they trend down? Gun to my head, I suspect the same analysis in this article will play out, so it trends down slightly, but no big crash. Really goes back to consumer incomes again – which itself goes back to government policies. We need to watch the next budget very closely for clues on the next phase of stimulus.

4th Wildcard – Vaccine approval in US leads to Treasuries Sell-off. US interest rates go up, SIBOR goes up. But Singapore does not have vaccine yet. Mortgage cost goes up & property prices go down.

https://www.theedgemarkets.com/article/goldman-warns-covid19-vaccine-approval-could-upend-markets

Oh yes that’s a good one, really unique fact pattern that could be entirely possible. Thanks for raising this.

I like the article. One point is to watch vacant level. If the vacant level goes up again, the rent will continue to drop. It makes property less attractive as investment from income perspective.

Good point. Technically speaking, vacancy rates should go up because of foreigners/expats being unable to come in, and existing ones eventually returning back to their countries due to attrition. But the world is seldom so straightforward, and a lot of times we just don’t know what we don’t know. So I am maintaining a good amount of humility over my forecasts. 🙂

I think interest rates are pretty key here tho. I used to pay 2% interest on my mortgage pre covid, but now it’s sub 1%. there may be bankruptcies, but rentals may be able to cover mortgages for quite a number of people who face issues. I agree with your take on interest rates being low for an extended period of time, and even if a vaccine is produced as mentioned in a comment below, it might be like the flu vaccine where u have to take one every year, so things may never be the same. On the point of property prices, it might make more sense to use resale property prices instead of new launch property prices, as the gap is one of the widest it’s ever been. also with primary sales there could be things like reissuing of OTP and hidden kickbacks that allow prices to remain artificially elevated.

also in terms of coe, the government severely limited supply, putting in one third of the CB quota in July-September, while releasing the remaining over the next 9 months. frankly in this scenario, the only person that wins is the government. I agree that prices will also start to trend lower in time to come.

That’s a really good comment, thanks for sharing.

I do agree with you, interest rates really matter as well. The tailwind from lower interest rates should also drive asset valuations up. I think we’re seeing the same dyanmics play out in capital markets – massive deflationary forces from COVID19 on incomes, but massive inflationary forces from rock bottom interest rates and easy liquidity. The million dollar question is which will win out in the short term, and then medium term.

Yeah agree on the resale vs new launch. This article was looking more specificically at resale launches rather than new launch, so my apologies for not clarifying that point. New launches are tricky because developers have holding power, and none of them really want to tank the market by slashing prices (which also affects their unsold inventory). If the thesis in this article holds, resale prices will come down first, then new launches (if at all).

Interesting how this time around lower interest rates have inflated financial assets but not property prices. Perhaps the two are not as fungible.

Well this time around there are massive deflationary forces because COVID19 has impacted incomes for certain groups of people. Short term, this deflationary force could prove to be more powerful than interest rates, but of course, it is in turn being countered by all the massive budget stimulus we are running – with another to come on Monday.

Prices still went up in the worst recession. People are snapping up but some are not paying their mortgages. This is really weird.

Haha so far I have been completely wrong on this call. Let’s see how things play out this year, there’s still time for things to change. Govt made some really interesting comments on the housing market recently. 🙂

Hi FH. I was interested to see that vacancy rates actually trended downward slightly in 2020Q4 for RCR and OCR.

I am guessing that with rents trending downward and new requirements to work from home, more singles are actually moving out of their family homes and renting small apartments to live and work. So this decrease in average local household sizes may actually be compensating for the departure of foreigners and keeping vacancy rates relatively stable.

Yeah I think this call has turned out to be very wrong so far.

The government has done a very good job in the stimulus, and cushioning the impact of COVID. Just like the US, we’re seeing very strong home sale prices in COVID.

Oh man its 2022 and im gg homeless