In a recent article I shared that I recently refinanced my mortgage to a 2.95% fixed rate mortgage.

Some of you have reached out to ask about the thought process, and why I picked that mortgage option.

So I figured I would share how I arrived at my decision in this article.

Hopefully it may help some of you out there, who are choosing between a fixed vs floating rate mortgage right now, and the lock in period.

Mortgage options available

To share, these were the mortgage options available, after speaking to a mortgage broker.

I have split them up into Fixed Rate and Floating Rate mortgage options below.

Note that depending on your loan amount and situation, you may have a different set of mortgage options.

It’s usually best to get a mortgage broker who can help check across all the banks and propose the best options (saves you a lot of time contacting each back).

If you already have a mortgage broker you can use your contact.

Otherwise you can try Redbrick, and I extract their details at the end of this article.

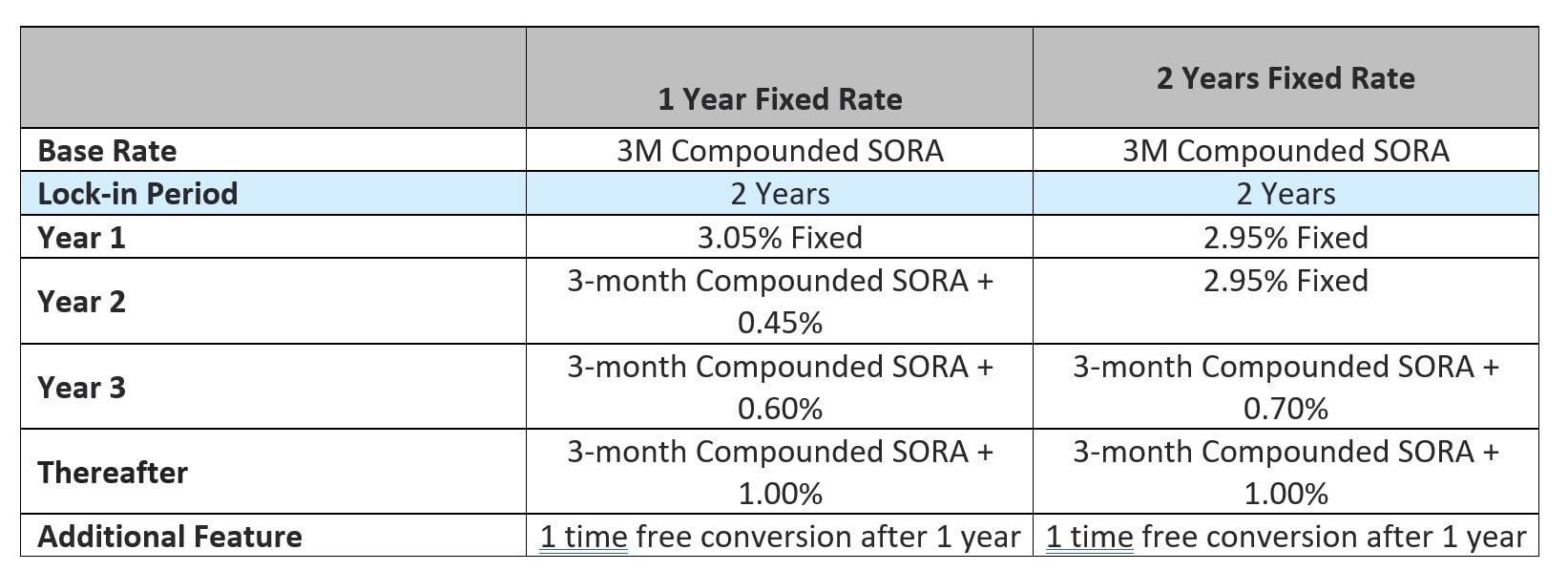

Fixed Rate Mortgage Options available

These were the best fixed rate mortgage options available when I was refinancing:

|

|

|

2 Years Fixed Rate |

|

Base Rate |

3M Compounded SORA |

3M Compounded SORA |

|

Lock-in Period |

2 Years |

2 Years |

|

Year 1 |

3.05% Fixed |

2.95% Fixed |

|

Year 2 |

3-month Compounded SORA + 0.45% |

2.95% Fixed |

|

Year 3 |

3-month Compounded SORA + 0.60% |

3-month Compounded SORA + 0.70% |

|

Thereafter |

3-month Compounded SORA + 1.00% |

3-month Compounded SORA + 1.00% |

|

Additional Feature |

1 time free conversion after 1 year |

1 time free conversion after 1 year |

In picture form below:

3M Compounded SORA is 3.744% today.

So the floating rate in Year 2 of the 1 Year Fixed Rate option would work out to 4.19% for the second year (based on today’s rates).

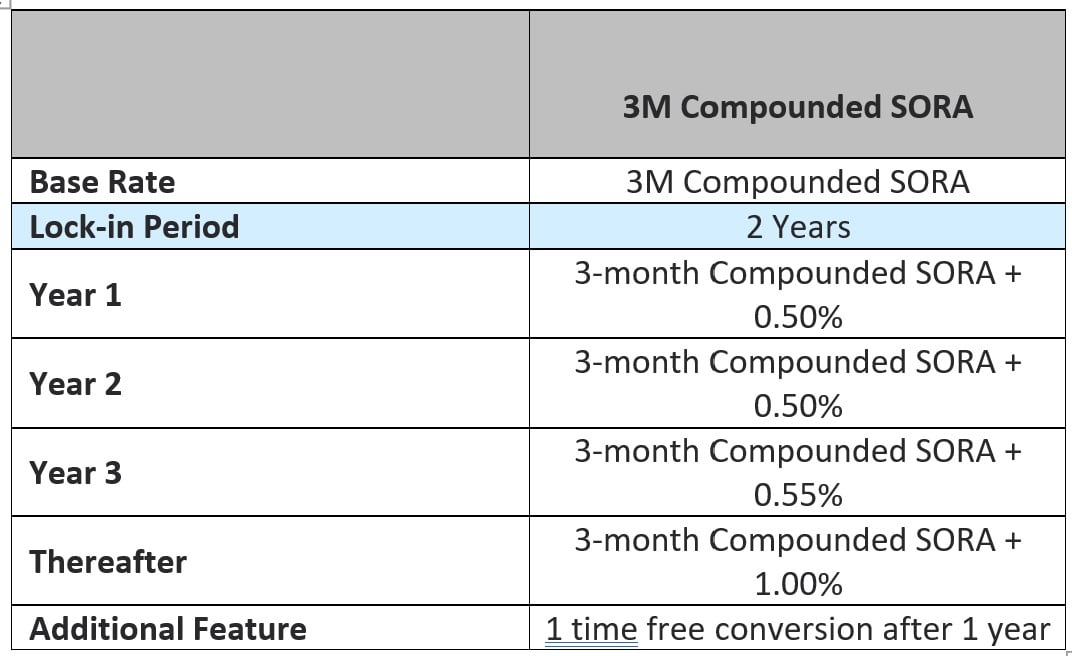

Floating Rate Mortgage Options available

This was the best floating rate mortgage option available:

|

|

|

|

Base Rate |

3M Compounded SORA |

|

Lock-in Period |

2 Years |

|

Year 1 |

3-month Compounded SORA + 0.50% |

|

Year 2 |

3-month Compounded SORA + 0.50% |

|

Year 3 |

3-month Compounded SORA + 0.55% |

|

Thereafter |

3-month Compounded SORA + 1.00% |

|

Additional Feature |

1 time free conversion after 1 year |

In picture form below:

3M Compounded SORA is 3.744% today, so the floating rate would work out to 4.24% today.

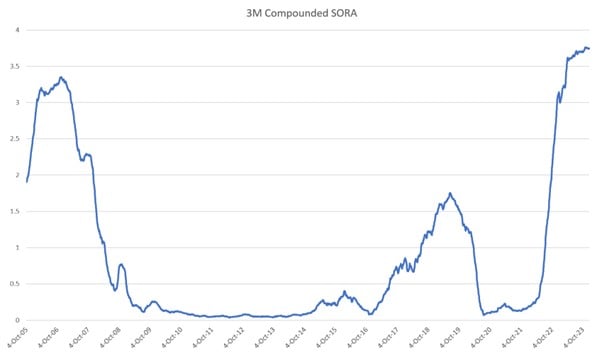

How does the 3M Compounded SORA move over time? For Singapore mortgages?

For reference, this is the 20 year chart of 3M compounded SORA and how it moves over time.

You can see how current levels of 3M SORA is higher than even 2007.

While it sits at 3.744% today.

Most of the past 10 years when interest rates were at zero – the 3M SORA was at 0.2%

How to pick between fixed and floating rate mortgages?

Now the general rule is that you pick a fixed rate mortgage if you think interest rates are going up.

And you pick a floating rate mortgage if you think interest rates are going down.

But you have to realise the banks themselves are not stupid.

If everyone thinks that interest rates may be headed lower.

You can bet that the bankers know that we think that too.

Why I took a 2.95% fixed rate mortgage in 2023? Instead of floating rate mortgage? (as a Singapore Investor)

So the problem with taking a floating rate mortgage today.

Is that the 3M Compounded SORA is 3.744% today.

The floating rate is a 0.50% spread on top of the 3M Compounded SORA.

That’s an interest rate of 4.24%.

Way, way higher than the fixed rate of 2.95%.

Interest rates need to fall A LOT for floating rate mortgages to make sense

Let’s say 3M Compounded SORA falls to 1.5% 1 year later.

That means for the second year of the mortgage you are paying 2.0% (1.5% + 0.5% spread).

That means an average of 3.12% for the 2 year fixed term.

Which means that you were better off just taking the 2.95% fixed for 2 years.

The risk with floating is what if interest rates don’t go down

The risk with floating rates today is that yes, everybody thinks interest rates are going down in 2024.

But what if you’re wrong?

What if interest rates stay at this level for the next 2 years?

Then suddenly you’re stuck paying 4.24% for 2 years, when you could have locked in 2.95%.

Floating Rate Mortgages – Bird in hand vs two in the bush?

So the big problem with floating rates in my view, is that you are paying a premium today, for the hope that interest rates will come down enough in the next 2 years, to create an average interest rate that is lower than the fixed 2.95% rate.

It’s a bird in hand, vs two in the bush kind of logic.

And while I personally think interest rates are coming down, I’m much less certain on whether they will come down enough to justify paying a higher upfront interest rate.

So between fixed and floating rates, I chose to go with fixed rates.

Bird in hand vs two in the bush?

I rather go with the bird in hand.

How to pick between Fixed Rate mortgages?

Between the fixed rate options, it was down to the two below.

Both with a 2 year lock-in period.

I could either get 3.05% fixed for the first year, and floating for the second.

Or I could get 2.95% fixed for two years, with the right to reprice after the first year.

|

|

|

2 Years Fixed Rate |

|

Base Rate |

3M Compounded SORA |

3M Compounded SORA |

|

Lock-in Period |

2 Years |

2 Years |

|

Year 1 |

3.05% Fixed |

2.95% Fixed |

|

Year 2 |

3-month Compounded SORA + 0.45% |

2.95% Fixed |

|

Year 3 |

3-month Compounded SORA + 0.60% |

3-month Compounded SORA + 0.70% |

|

Thereafter |

3-month Compounded SORA + 1.00% |

3-month Compounded SORA + 1.00% |

|

Additional Feature |

1 time free conversion after 1 year |

1 time free conversion after 1 year |

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

How does free mortgage conversion work?

After a bit of discussion with the bank / mortgage broker, and some googling.

I finally pieced together how the free mortgage conversion works.

Basically if you take a 2 year fixed rate mortgage at 2.95%.

After the first year, you can ask the bank for a free mortgage conversion.

The bank will then give you a couple of options you can choose from.

For example:

- A fixed rate at x%, or

- A floating rate at 3M Compounded SORA + x% spread.

Of course, because you are still in lock-in period, you wouldn’t expect the options to be as good as if you were a new customer / out of lock up.

But if interest rates plunge over the next 12 months for example, and new fixed rate mortgages are going at 1.5%, you could probably get the bank to give you something in the 1.6% – 1.8% range.

So that’s my understanding of how the free mortgage conversion works – but please do correct me if you have a different understanding.

Why I took a 2.95% fixed rate mortgage in 2023?

With that in mind this became quite a simple decision for me.

I picked the 2.95% fixed for 2 years, with the free conversion after 1 year.

Worst case if interest rates stay high for the next 2 years, I am protected because I am locked in for the 2.95% for 2 years.

Whereas if I had taken the floating rate in the second year, I would have sleepless nights if interest rates shot up a year from now.

And with this option, if interest rates do go down in the next 12 months.

I can get a free conversion into either a fixed or floating at the time.

|

|

|

2 Years Fixed Rate |

|

Base Rate |

3M Compounded SORA |

3M Compounded SORA |

|

Lock-in Period |

2 Years |

2 Years |

|

Year 1 |

3.05% Fixed |

2.95% Fixed |

|

Year 2 |

3-month Compounded SORA + 0.45% |

2.95% Fixed |

|

Year 3 |

3-month Compounded SORA + 0.60% |

3-month Compounded SORA + 0.70% |

|

Thereafter |

3-month Compounded SORA + 1.00% |

3-month Compounded SORA + 1.00% |

|

Additional Feature |

1 time free conversion after 1 year |

1 time free conversion after 1 year |

2.95% fixed for 2 years is pretty cheap all things considered

2.95% lock up for a 2 year mortgage, frankly it wasn’t as bad as I expected.

Considering that Singapore Savings Bonds were paying 3.4% just a month or two back.

I could literally have taken the mortgage, put my spare cash into SSBs, and earn the 0.45% spread risk free.

With latest T-Bills paying 3.73% risk free, mortgage rates still remain below the other yield options.

A reminder that despite the huge rise in interest rates, real interest rates actually remain quite manageable.

And with the Fed pivot now and possibly lower interest rates in 2024.

It would be interesting to see what happens next with the economy.

But… there’s no right or wrong here

So that’s how I settled on my mortgage option.

But I do want to stress there is no right or wrong here.

You may decide to go with a floating rate, and if interest rates plunge in the next 6 months you could well look like a genius.

There are pros and cons with each option.

And considering all the facts I know about the macro environment, and my own risk appetite, this was the option I settled for in the end.

I encourage investors to think through the same for yourself, and decide what works for you.

Mortgage Brokers are worth it if you’re looking to refinance / take a new mortgage

Whatever the case, I have found that it’s usually worth it to get a mortgage broker if you are looking to refinance / take a new loan.

The mortgage broker can easily help you check on the most competitive rates available to you – based on your age, loan amount, and financial situation.

It sure beats having to approach each bank individually to check on the rates.

They don’t come at any additional cost to you too, they earn from the referral fee paid by the bank.

If you know any mortgage brokers you can just use the ones you’re familiar with.

Otherwise you can try Redbrick, and I extract their details below.

There is a tool you can use to check on the rough ballpark latest rates (it’s not super updated, so best to still contact the mortgage broker for latest rates).

You can leave your contact details below, and the broker will reach out to you to suggest possible options.

Full disclosure that this post is NOT being sponsored by Redbrick. Views in here are my own.

This article was written on 22 Dec 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

– Get up to USD 5000 worth of shares (Best promo of 2023 – Now Extended)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Not sponsored but can embed their code in this article. Duh..

Actually if you have code for another broker that can compare mortgage rates across multiple banks – more than happy to embed in this article as well.

Wanted to give readers a way to quickly compare rates across all the banks, to know which are the lowest.