As some of you will know – this week saw the blowup of a prominent Singapore hedge fund.

The fund was long China and short Japan – and down a whopping 18.8% in January alone.

Literally the day after the fund announced its liquidation.

China announced a cumulative package of $400 billion in stimulus to prop up the markets short term.

I’ve noticed a lot of discussion about China stocks of late.

Have China stocks bottomed, and it a good time to buy China stocks?

This is a FH Premium article first released on FH Premium a month or so back. I am releasing it to all (with some updates) in the hopes that it may help you in your decision making process – given the vital importance of China’s economy today.

If you find articles like these helpful, do sign up for FH Premium for more premium macro articles like this.

You can also get access to my personal stock / REIT watchlist (with price targets), and my full personal portfolio.

China as a turnaround play in 2024 because of cheap valuations?

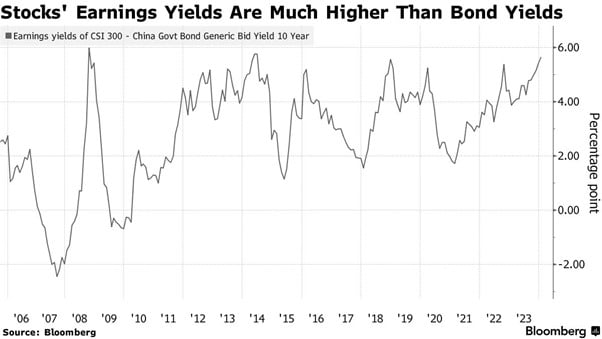

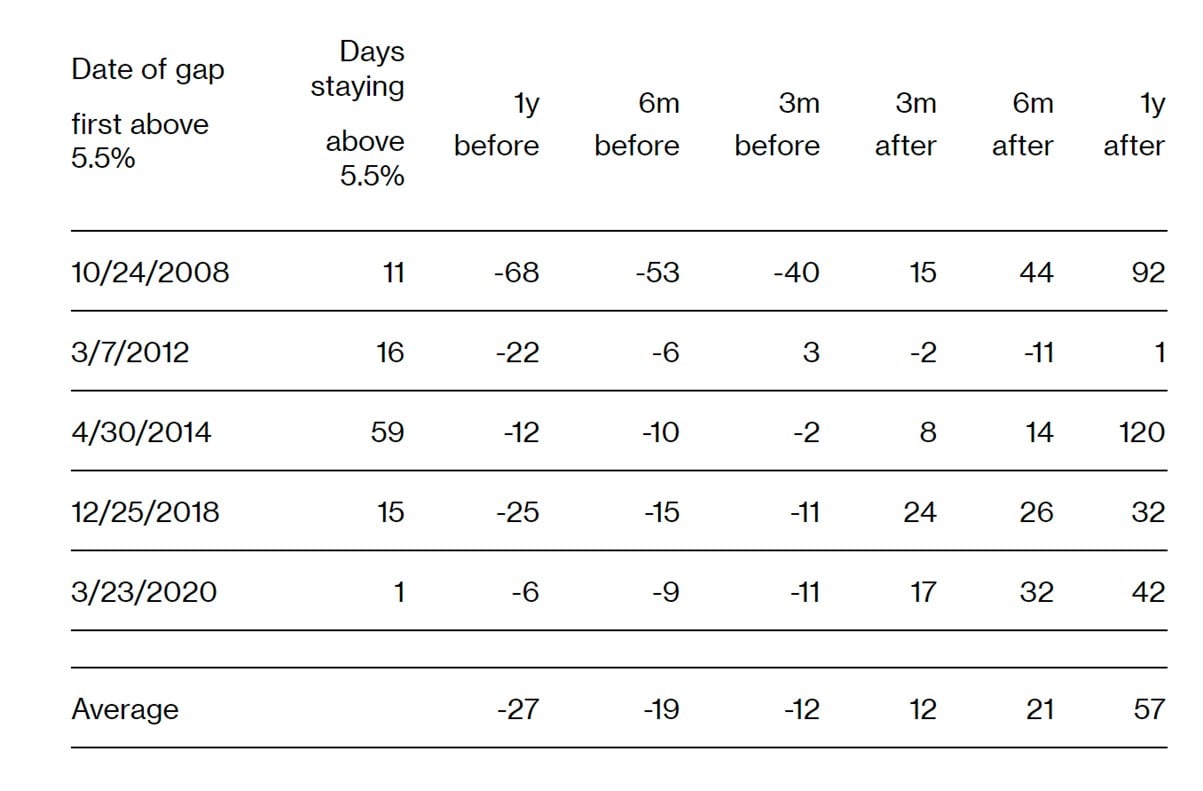

For example, here’s a Bloomberg article titled: Chinese Stock Indicator With 100% Success Rate Is Flashing Buy.

The articles goes on to discuss how China stocks earnings yields are much higher than bond yields, a spread of close to 6.00% vs the 10 year Bond Yield (the same spread for the S&P500 is 0%).

It notes that the past 5 times in history the yield spread was this high.

China stocks returned an average of 57% in the 1 year after (actual returns range from 1% to 120%):

Positioning is bullish as well – foreign investors are heavily underweight

At the same time, foreign investors exposure to China are at some of the lowest levels it has ever been.

From a technical perspective is a contrarian bullish signal (because if there is a China recovery foreign investors will have to rush to rebuild exposure).

So valuations are cheap, and positioning may be bullish.

Are China stocks an attractive buy?

LKY’s views on China

Now I was reading one of Lee Kuan Yew’s old books recently.

And his views on China, despite being given in 2013, are some of the sharpest and most insightful that I have read on China to date.

You may not necessarily agree with all the points he raises, but it’s incredibly helpful to understand his starting point (I share my thoughts further below).

I’ve summarised the key points from LKY below:

China – Politics

For 5,000 years, the Chinese have believed that the country is safe only when the centre is strong.

- “A weak centre means confusion and chaos. A strong centre leads to a peaceful and prosperous China. Every Chinese understands that. It is their cardinal principle, drawn from deep-seated historical lessons. There will not be a deviation from this principle any time soon. It is a mindset that predates communism. It has existed for centuries, for millennia.”

- Because of this, even if there is political change in China, it will not be for one man one vote, but another uniquely Chinese variant.

- Technology has enhanced the ability of China’s leadership to monitor their people, and you should not underestimate the will of the central government to retain control.

On Taiwan – his view is that reunification is inevitable, but there is significant uncertainty over how long it will take.

- The way he sees it – No Chinese leader can survive if Taiwan is lost under their watch.

- Is US prepared to pay the price that China is willing to pay over Taiwan, all while projecting force across the Pacific? China will fight, and fight again, and again, over Taiwan, until they win. Is the US willing to pay that price for Taiwan’s independence?

China – US relations + Economy

Economically, technologically, militarily, China will catch up with the US eventually on an absolute level simply because of their sheer size and talent of the population (he believes within 10 – 20 years).

- However success is not guaranteed, and he sees maybe a 20% chance of failure.

- Significant domestic challenges remain such as:

- Inequality – Geographically, the inland areas can never be as rich as the coaster regions. Hukou system exacerbates this.

- Instability – Control is paramount.

- Productivity – Their system cannot foster innovation the same way as US. SOEs are not as efficient as private enterprise, but it cannot be easily privatised or revamped. Lack of IP controls to protect ideas, system to foster and protect creativity.

- Because of all these inefficiencies, China may never operate at maximum capacity.

- On a per capita basis China may struggle to surpass the US.

China’s weakness comes in two ways:

- No Rule of law – China’s system does not pay heed to rule of law or governance institutions.

- No governance institutions – The man is greater than the rule of law / institution, hence the importance of guanxi and corruption. If the man is weak, the system will fall apart quickly. Unlike US/SG where the rule of law and governance institutions will support the man.

China needs to invest in basic research – space, military, semiconductor technology to avoid getting outmanoeuvred by the US economically

To drive long term sustainable economic growth, China needs to transition from an export driven economy to domestic consumption. However this requires a deep change in their psyche, as Chinese would prefer to save, and only spend once they feel secure.

- The low hanging fruit of cheap manpower and infrastructure/real estate has run out.

- The sustainable path going forward is domestic consumption.

- This path also requires redistribution of wealth.

- All these reform needs to be done if they don’t want their growth to stall.

The book is One Man’s View of the World for those interested. While I have tried my best to summarise, there are certain nuances I was not able to fully capture, so it’s worth reading in full if you want a deeper dive.

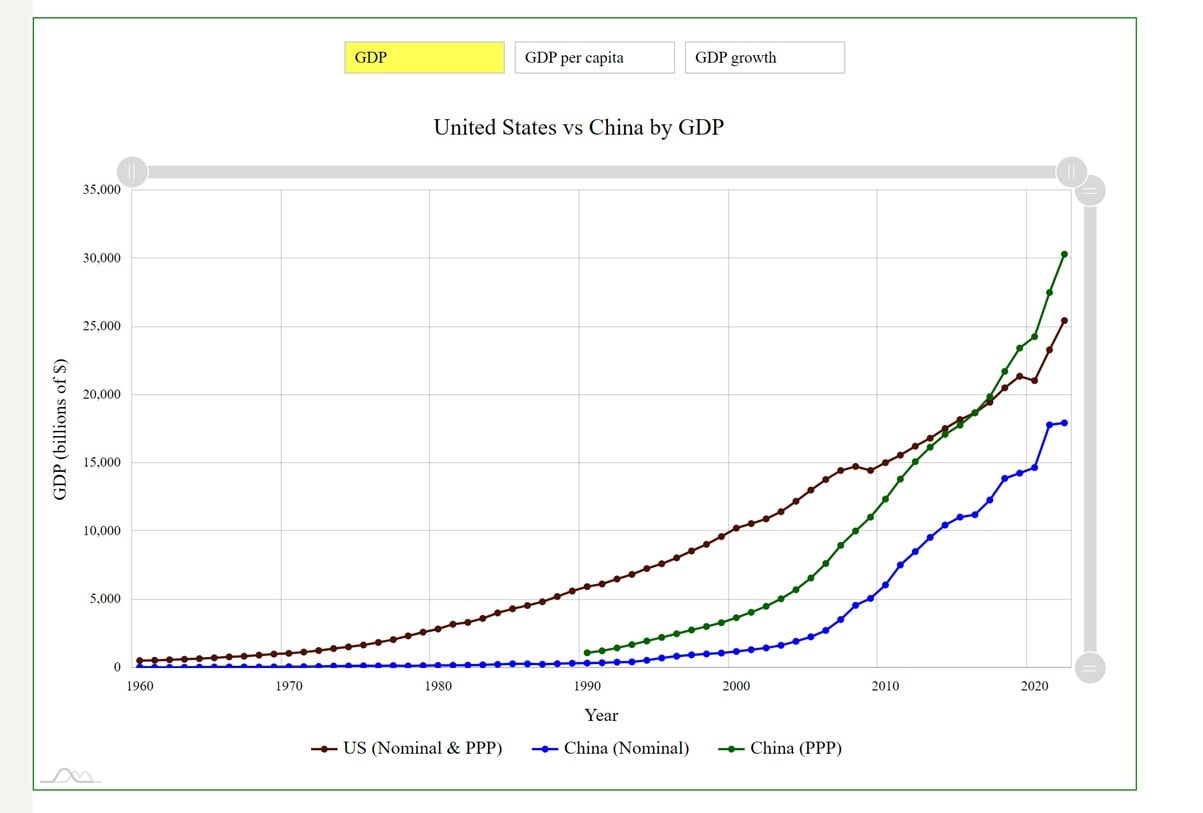

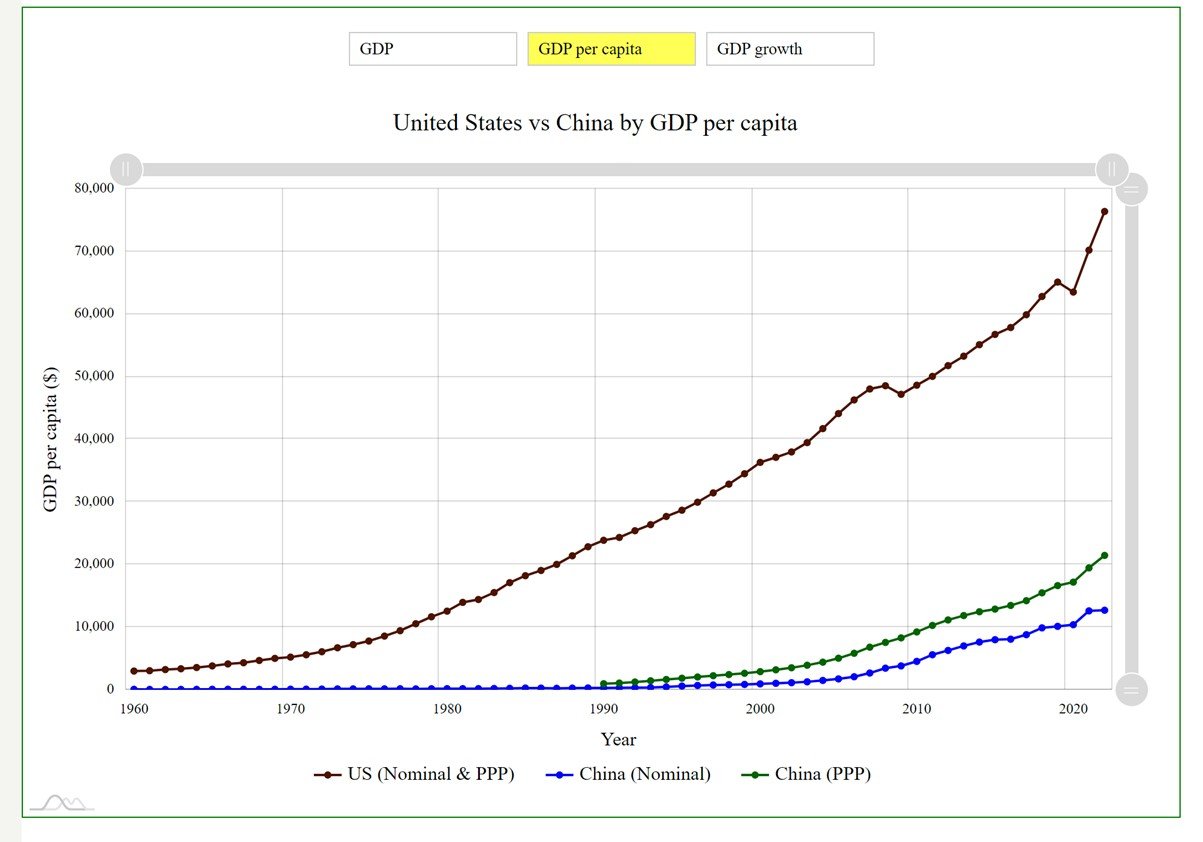

China’s GDP vs the US (nominal vs per capita)

There are a couple of charts below to illustrate this point.

On a purchasing power parity basis (green line), China’s GDP has already surpassed the US.

On a nominal basis (blue line), China’s GDP is about 70% of the US.

But China’s population is 1.3 billion vs US’s 300 million.

Even if China’s GDP surpasses US on a nominal level, that could be simply down to a larger population alone.

The chart below illustrates this well.

On an absolute level China is fast catching with the US.

But on a productivity / per capita basis, China is still well, well behind the US regardless of what metric you use.

My views on China – real structural problems to be solved

China’s economic miracle the past 30 years was largely driven by 2 powerful economic drivers:

- Export growth (due to cheap labour and high productivity rate)

- Real Estate / Infrastructure growth

Export Growth

We are now at the point in the cycle where everything that can possibly be built in China, is already being built in China.

And because of a combination of (a) higher labour costs and (b) geopolitical risk of China supply chains, MNCs are actually trying to move production out of China and into the rest of Asia.

China understands this, and to avoid the middle income trap, China is trying to upskill into higher value added manufacturing like renewable energy, electric vehicles, semiconductors etc.

But this will take time, and it’s not an overnight transition.

And don’t forget, because of China’s much larger base today, growing the economy by 5% today is actually a much bigger number than 5% growth in 2010.

To drive this much export growth to move the needle, will inevitably come at the expense of other countries.

And in this new age of protectionism if any country loses that much market share to China you will inevitably see trade barriers being erected against Chinese imports.

Long story short – China cannot rely on export growth to the same extent going forward.

Real Estate / Infrastructure growth

This was the saving grace for the past 20 years, and what pulled China (and the world) out of 2008’s financial crisis.

Massive real estate / infrastructure growth, funded by debt.

The problem is that we are at the point in the cycle where you get diminishing marginal returns from real estate / debt.

If China continues growing their real estate bubble, the bubble will inevitably burst at some point, and China will follow a similar path to Japan in the lost decade.

China’s leadership has studied Japan’s case study extensively, and they are keen not to repeat the same mistakes. The focus on bringing down real estate debt has been in play ever since 2018.

China’s problems are structural and very real

Because of the above.

All the western commentators that call for China to “print money” and stimulate the economy fail to understand the underlying problem in my view.

China is not like the US in 2008, where the key issue was too much debt that had gone bad. Once you solve the debt issue, US’s fundamental competitiveness came back to the forefront, and powered the economy ahead.

The underlying problem here – is that what got China’s economy here, will not work going forward anymore.

Export growth and growing real estate bubbles – they won’t allow China to surpass the US.

New engines of growth are required.

What is the sustainable path going forward?

The sustainable long term growth solutions in my view are:

- New areas of technological growth – for eg. In electric vehicles, semiconductors, AI, battery technologies

- Domestic consumption – to get local Chinese to save less, and spend more

Which if you’ll notice, is exactly what the Chinese government has been focussing on of late.

But the solution again is not straightforward.

Real estate is 30% of China’s economy.

That whole area is at best going to stay flat for the next few years (at worst negative).

To offset the real estate slowdown, you will need new areas of growth and domestic consumption to offset that.

But (1) is not something that you can grow overnight, and we discussed how other countries are likely to respond with trade barriers if you are too aggressive.

And (2), LKY rightly pointed out how the Chinese love to save. This is not a mindset that you can change overnight, but it is something that they will need to work on.

The inevitable conclusion here, is that unless China opens the monetary spigots to reinflate the real estate bubble, China’s economy will stay slow for a while.

To blame Xi for all the problems, is not entirely accurate

Going by the logic above, to blame all of China’s problems on Xi today is not fully accurate.

Even if you replace Xi tomorrow, the same underlying structural problems of slower export growth and real estate debt will still be in place.

You can even argue that Xi’s job today is extra challenging because his predecessor Hu Jintao was too slow to transition China’s economy away from cheap exports and real estate, and relied too excessively on real estate debt (this is something that Xi has hinted towards as well, that the problems China faces today were created by his predecessors).

In fact if you were serious about trying to effect the 2 solutions above.

What you would need to do is to consolidate your control.

This is because the solutions above require a redistribution of wealth, and the growth of new sectors (at the expense of old sectors).

This is a serious threat to the existing elites in China (eg. the property developers, construction builders, infrastructure players etc) and you can be sure they would mount some kind of challenge to prevent this economic restructuring from taking place.

What does all this mean for investing?

Now I know that I’ve gone on a very long about way of trying to explain the problem with China today.

But I felt it was vitally important to understand the problem at a high level.

Once you understand the framework, you can then understand what will work, and what won’t work, to solve the problem.

And given China is the probably the most important global economy to understand today after the US, it’s worth taking the time out to properly appreciate the issue.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

China’s problems are structural and very real

Long story short – China has a lot of very real, structural problems on their hands.

And the problems are somewhat nuanced, and not prone to the broad generalisations you see in the media.

If they simply continue doing what they’ve been doing the past 30 years, they will never surpass the US.

In fact, as LKY put it, even if China manages to solve all these problems, they may never surpass the US on a per capita basis because of their fundamental problems of (1) need to maintain control, and (2) inherent inefficiencies in the system.

But given the determination of the local population, and the amount of talent they have.

And the fact that most of their debt is denominated in RMB that can be dealt with domestically (only exception is their reliance on foreign oil/commodities – hence their obsession with securing supply).

There is a good chance China will be able to address these problems over time.

But key being over time.

These are structural problems that cannot be solved over 1 – 2 years.

These problems require reform of the entire system, and will play out over a much longer period.

Bloomberg’s Analysis – Looking at the past 15 years is not necessarily accurate

Once you understand the above, you start to appreciate the problems with the analysis run by Bloomberg above.

Bloomberg runs the analysis on the past 15 years, which was a regime where China was still relying on exports and real estate debt for growth.

Back then, China could easily turn on the monetary spigots for real estate, and growth will reaccelerate to whatever level they want it to be.

Ie. Long term growth was fine, and once they solve the short term problem growth will recover.

The problem today, is the opposite.

If they don’t address the fundamental problems – They can keep juicing short term growth via debt, but long term growth will falter.

Ie. You may be able to solve short term growth with debt, but without making the hard reforms, long term growth will not recover.

This is a key point that Bloomberg’s analysis fails to incorporate.

Just looking at valuations alone, tells you nothing about where / when the turning point will come.

China has been very conservative with short term stimulus

China has been very conservative with short term stimulus the past year or two.

All of their liquidity injections have been to the tune of $50 – $100 billion.

Stuff to keep things afloat, and prevent anything big from breaking.

But you don’t see anything like the massive 2008 or 2015 liquidity injections that lifted the entire economy.

Where is the catalyst for China?

Short of massive liquidity injections.

You’re just stuck with the inevitable conclusion above.

That short term, China’s economic growth will remain weak, as the structural reforms will drag on economic growth.

What are the stimulus measures released this week? (as of 25 Jan 2024)

China released additional stimulus measures this week after the broadening stock market sell-off.

They are:

- Reserve Ratio Requirement (amount of cash banks have to keep in reserve) cut by 0.5%, to provide 1 trillion yuan ($139 billion) in long-term liquidity to the market

- Mobilisation of 2 trillion yuan ($278 billion), mainly from the offshore accounts of Chinese state-owned enterprises, as part of a stabilization fund to buy shares onshore through the Hong Kong exchange link

- Jack Ma / Joe Tsai buying more than $200 million in Alibaba stock

Cumulatively, they amount to close to $400 billion in liquidity injections.

However once you understand the problems facing China’s economy, you’ll realise that these treat the symptoms – not the cause.

So comparing these measures to QE is not right in my view.

QE worked because the underlying dynamics of the US economy remained strong. Solve the debt overhang, the economy roars back to life.

China’s economy today – the problem is that the underlying dynamics are no longer competitive, for where China wants to go.

To get to the next stage, they need reform of the economy.

So what the monetary stimulus above does – is that it buys China time.

If you don’t step in with the stimulus, you risk the economy running into a self-reinforcing deflationary spiral, and before you know it you have much bigger problems to solve.

These stimulus will help to address the short term pain, and (hopefully) prevent anything worse from breaking.

But they are just there to buy time. If China doesn’t solve the underlying structural issues, there will be no sustained recovery.

So that would be the key for long term investors to watch.

How to invest in China?

So China stocks are cheap, but they are cheap for a reason.

How do you invest in a climate like that?

The options are:

- You don’t

- Buy stable dividend payers – you get paid to wait

- Buy areas that China will focus on – new energy, domestic consumption, semiconductors

To me, all 3 are viable strategies.

If after reading all of the above, you decide China is not for you, you can just skip China as a market entirely.

But if after reading all of the above, you decide China is still worth investing in due to its lack of correlation with the rest of the world (diversification benefits).

Then you can either buy the stable dividend players where you get paid a 8% yield to wait – for eg. the 4 local banks, or SOE like telcos, energy, real estate etc.

Or you can buy the volatile high growth areas China will focus on, like new energy, domestic consumption, semiconductors.

Will I buy China stocks in 2024? (written as at Dec/Jan)

Looking at my latest portfolio, total exposure to China (from a portfolio basis) sits at 12%.

About half of that is dividend plays (real estate and banks), the rest is domestic consumption plays (tech).

If I were to increase exposure to China, it would likely be via Option (2) above.

China’s market is too volatile, and I lack the on the ground knowledge, to stock pick the new sector players.

Better to just buy a 8% yielding SOE and collect the yield, and hope the price remains flat 5 – 10 years later.

But would I increase exposure to China in a big way today (as a long term investment, not trading)?

I’m not sure frankly.

Short of valuations, I don’t see the fundamental catalyst to spark a turnaround / rerating in China stocks.

If that changes, then yes of course I would add in a heartbeat, because cheap valuations + supportive policy + catalyst will be an explosive combination.

But for now, it’s hard to see why China would make this change and undo all their good work to bring down debt levels and restructure the economy.

Will I buy China stocks in 2024? (as of 25 Jan 2024)

I extracted my thoughts as of Dec/Jan above for your reference.

As of 25 Jan 2024, has anything changed?

The stimulus measures unveiled this week by China are unlikely to be enough to move the needle by themselves (mid – longer term).

But they are notable because they seem to be an indicator that Chinese policy makers think the rout is getting out of hand.

This could be a tradeable short term bottom.

Of course, the long term problems for China remain very real as set out above, and will not be solved by mere liquidity injections – so this is a big point to note. Whether China can effect the necessary reforms is still unclear, and I’m sure each investor will have their own views on this.

But at the same time, you’re looking at pretty unbelievable valuations for China.

The HSCEI is at levels last hit in 2005.

Some names I am looking at are trading at 8-9% dividend yields, 0.3x book value, and low 20-30% gearing, with pretty high quality real estate (full list on FH Premium).

Those are unbelievable valuations, where you’re just getting paid to wait.

Coupled with possible signs of short term liquidity injection.

Could this tempt me into the market?

Perhaps.

I will be watching closely how price trades the next few weeks before I make up my mind.

In any case, the full list of names I am looking at is shared on FH Premium.

And FH Premium subscribers will get regular updates as and when I add / sell China positions, or change my views on China.

This is a FH Premium article first released on FH Premium a month or so back. I am releasing it to all (with some updates) in the hopes that it may help you in your decision making process – given the vital importance of China’s economy today.

If you find articles like these helpful, do sign up for FH Premium for more premium macro articles like this.

You can also get access to my personal stock / REIT watchlist (with price targets), and my full personal portfolio.

– Get up to USD 3000 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 3000 free shares.

You just need to:

- Fund USD 500

- Subscribe for Moneybull (the money market fund solution) and maintain for 30 days

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Thanks for consideration:

1. Can a communist country foster innovation? History would suggest no. They copied or cloned a lot of western innovation over the decades. An argument can be made that this economic development is as far as it can go under one party rule. This is the ceiling. No real innovation without real political freedom. Economics is politics manifest.

2. Demographics. They are shrinking with no end in sight. Its the japan phenomenon except japan is a democratic free market economy with some incredible technology and real innovation.

Those are all fair points. LKY alluded to some of these in his book as well.

We’ll watch this play out over the next few decades.

What I might add though, is that for much of human history, China was the predominant, or one of the predominant powers of the world.

So China’s return to number 1 player, if it happens at all, is not unusual from a historical context.

That said, nothing is certain in this world – we’ll see how it plays out.

This is not a fair point at all by someone with an obvious pro US anti-China bias and I’m surprised Financial Horse has not questioned it at all:

1. Tech Innovation: China has emerged as a global leader in several technological fields, including 5G technology, artificial intelligence (AI), and quantum computing. Companies like Huawei, Alibaba, Tencent, and Xiaomi have made significant contributions to these areas and have produced cutting-edge technologies.

2. Renewable Energy: China has become a leader in renewable energy technology. It is the world’s largest producer of solar panels and wind turbines, investing heavily in research and development to improve efficiency and reduce costs.

3. E-commerce: Chinese companies like Alibaba and JD.com have revolutionized the e-commerce industry, pioneering innovative solutions in mobile payments, logistics, and online retail platforms.

4. High-Speed Rail: China boasts the world’s largest high-speed rail network, showcasing its engineering and infrastructure capabilities. The country has developed its technology and expertise in building high-speed trains, significantly advancing transportation systems. It is also making continuing progress in developing the Hyperloop trains based on magnetic levitation technology, which in future are expected to be able to travel as fast as if not faster than planes.

5. Space Exploration: China has made impressive strides in space exploration, launching its own satellites, crewed space missions, and lunar exploration programs. The recent success of the Chang’e missions to the moon demonstrates China’s advancements in space technology.

6. Electric Vehicles (EVs): Chinese companies like BYD and NIO are leading the way in electric vehicle technology. They have developed innovative EV models and are investing in battery technology and infrastructure to support the transition to electric transportation. A much higher proportion of cars on the road in China are now electric cars than any other country in the world. China’s advances in the area of green technology will gradually reduce its dependence on oil.

I think as always, the truth is somewhere in the middle.

I don’t doubt that China has the potential to build cutting edge technology. This is a 5000 year old society that was the largest global economy / leading technological power for much of its history. Such a development would merely be a return to its historical strength.

But short term, a lot of that technological development (eg. clean energy, manufacturing) has been built on the back of government subsidies and export growth – achieved by supressing labour cost (increasing inequality and impacting domestic consumption).

And in certain key areas like semiconductors / advanced manufacturing, China is still a few years behind the west (although no doubt they are using best efforts to try and catch up).

I’m fairly confident that longer term, China has the intellectual talent and tenacity and resources to achieve technological parity (possibly surpass) the west. But there are a lot of things the West can do to hurt them (or slow the progress) in the short term. The real estate deleveraging + transitioning the economy to domestic consumption is another big challenge. Safe to say their hands are full in the short term.

Thanks FH, for sharing this excellent write up to the public readers.

I actually just DCA into world market index, but keep abreast with the macro-ish news for interest. (There’s so many interesting intersections between different topics, history, finance, current affairs, geo-politics, etc..)

I read, and enjoy most of your weekends posts.

I especially liked the part where the article sort of painted XJP as a misunderstood leader who may be doing the hard things now, in order for things to continue to be good/great a decade down the road.

I guess history will tell us what he really is in time. 🙂

Oh, and the indirect book recommendation to read LKY’s book. +1

Appreciate the kinds words, I’m glad you found this article helpful.

Indeed. While the Western media crucifies Xi for his actions, it is also important to realise that the Western media tends to celebrate leaders like Gorbachev that further Western interests, not necessarily the interests of the country.

If you replaced Xi with someone else, it’s hard to see what that person would do differently. China’s economy requires hard reforms, and to see through hard reforms you need to consolidate power.

I enjoyed LKY’s book. Slightly dated as it was from 2013, but his clarity of insights are unmatched.

test

Glad I’m not a China only fund manager

Fair enough!