Okay so I have been getting A LOT of requests for a deep dive into Keppel Infrastructure Trust (KIT).

I’ve generally been cautious with KIT the past few months because they had to do an equity fundraise to fund the Ventura deal.

And with this market sentiment, it’s not a good time to be doing a fundraise.

Well, Keppel Infrastructure Trust just closed the private placement this week, and share price fell to 0.45 – the lower end of their trading range.

So I figured this was a great time to relook Keppel Infrastructure Trust.

This Business Trust trades at a 13.6% trailing dividend yield (if you include the special dividend) – 8.6% yield if you don’t.

Will I buy Keppel Infrastructure Trust after the equity fundraise?

My fear was that the equity fundraise would hit Keppel Infrastructure Trust’s share price

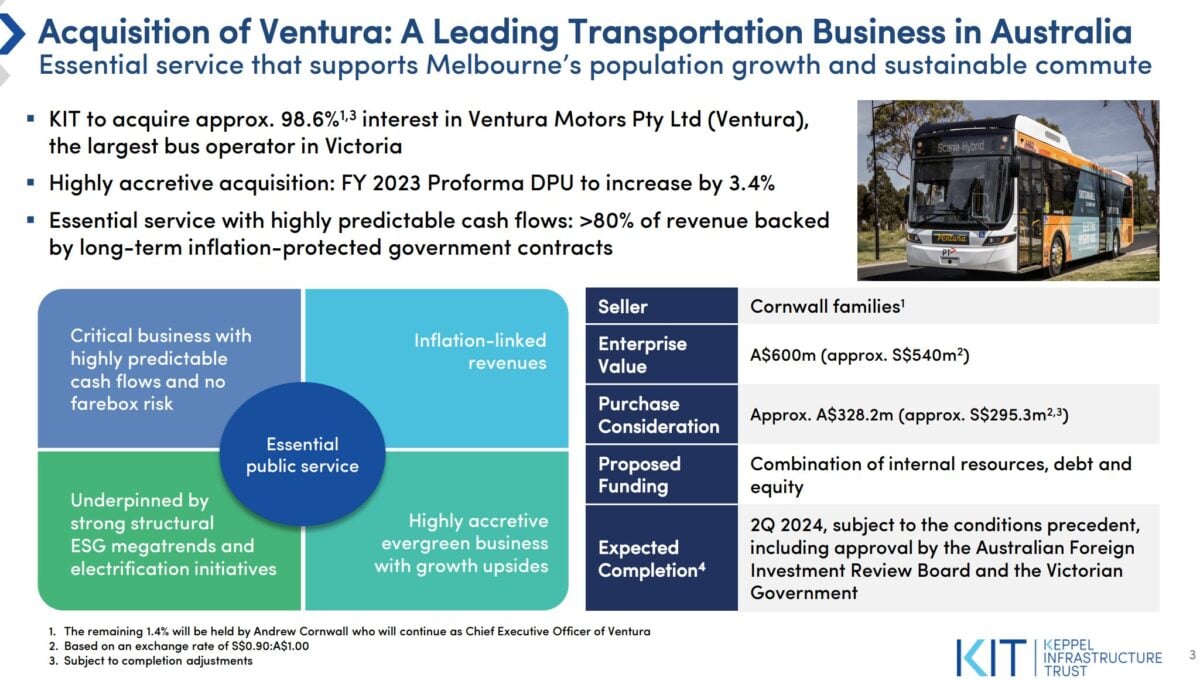

As you would know, in Feb 2024 Keppel Infrastructure Trust announced that they would be buying Ventura (an Australian Bus company).

In the acquisition assumptions, they assumed the following financing package:

- $180 million in debt

- $400 million in equity

At the time I ran some back of the napkin numbers:

- Keppel Infrastructure Trust has a $2.87b market cap

- So the $400 million equity fundraise is 14.0% of the market cap

That’s not a small amount of equity to be raising.

And given how weak market sentiment for REITs / Fixed Income has been most of the year, it could really backfire if you do it at the wrong time.

So I’ve generally been cautious on Keppel Infrastructure Trust all year.

You just know that if share price rallies, they were going to do an equity fundraise which would hit the share price.

Equity Fundraising of Keppel Infrastructure Trust (via Private Placement)

Well, that fear is finally out of the way.

Because Keppel Infrastructure Trust closed their fundraise via Private Placement this week:

“The Placement was approximately 2.5 times subscribed, with demand coming from new and existing institutional investors, as well as accredited investors.

After a book-building process, the number of Placement Units to be issued has been fixed at 456,622,000 new Units. The Placement Issue Price has been fixed at the highest end of the range at S$0.438 per Placement Unit. Accordingly, the total gross proceeds to be raised from the Placement is approximately S$200.0 million.

The Placement Issue Price of S$0.438 per Placement Unit represents a discount of: (a) 6.0% to the volume weighted average price (“VWAP”) of S$0.4662 per Unit ; and (b) (for illustrative purposes only) 4.6% to the adjusted VWAP (“Adjusted VWAP”) of S$0.4592 per Unit.”

Generally speaking this was a decent showing by Keppel Infrastructure Trust.

The placement was 2.5 times subscribed, which is pretty decent demand.

The issue price also was fixed at the highest end of the range, which amounted to a 4.6% discount to the adjusted VWAP.

Again this is okay-ish.

Only $200 million raised? Where does the rest of the money come from?

Some of you may realise that the original assumption was that $400 million would be raised via equity fundraise.

Yet only $200 million was raised in the end.

Where did the shortfall come from?

As it turns out, via perpetuals:

“On Aug 2, the trustee-manager issued $200 million perpetual securities at 4.9 per cent, under its $2 billion multi-currency debt issuance programme. As at Aug 27, it paid down about $198.6 million of the term loan facility. It aims to repay the remaining amount with the proceeds of the private placement.”

$200 million was raised via perpetuals instead of equity

I’m not sure what I think about this.

I suppose given the weak market sentiment this year, management felt that it would be too risky to go to market with a $400 million equity fundraise – almost 14% of their market cap.

So they cut it in half, and raised the rest via perps.

I suppose when your equity is paying 8.6% dividend yield those 4.9% yielding perps are still cheaper than equity.

But on the flip side, you’re locking in 4.9% interest rates (and not being able to benefit from any fall in interest rates).

And this will have to be refinanced eventually.

It’s kinda like kicking the can down the road.

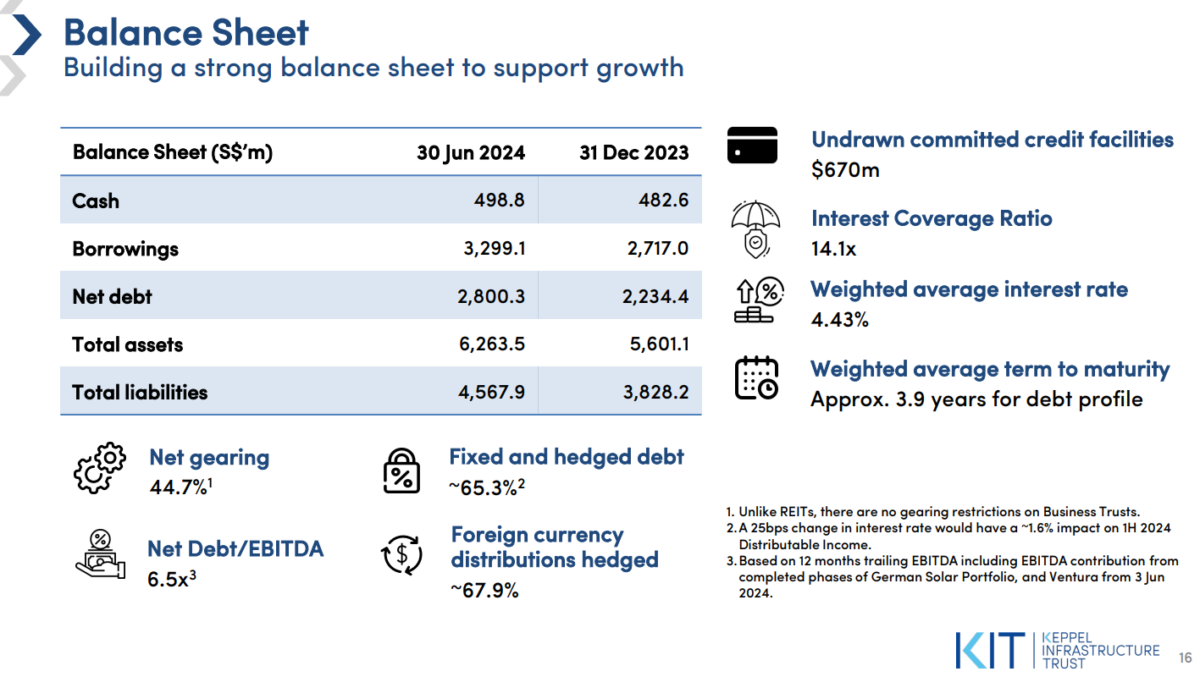

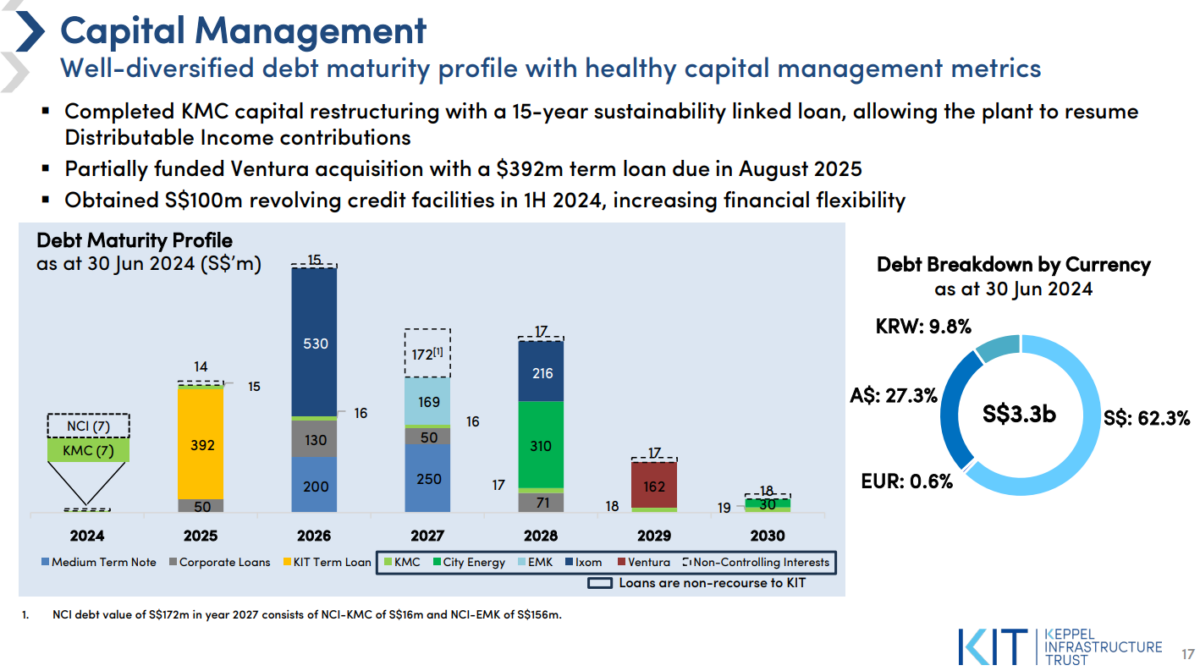

Keppel Infrastructure Trust is running a 44.7% net gearing even before you include the perps, so that’s quite a lot of debt on the balance sheet (although this includes the term loan for the Ventura acquisition, but you get my point).

Is Keppel Infrastructure Trust a good buy after the Equity Fundraise?

Whatever the case, now that the equity fundraise is done and dusted – it removes a big overhang over the stock.

Which leads to the question – is Keppel Infrastructure Trust a good buy today?

Trailing Dividend Yield of Keppel Infrastructure Trust is 13.6%

The dividend yield is very juicy.

Total dividend payout the past 12 months was 6.21 cents, which works out to a mind blowing 13.6% dividend yield.

A more realistic dividend yield? Annualised yield is 8.6%

Of course, that includes the special one-off dividend.

If you strip it out, and annualise the latest 1H dividend yield, that works out to a 8.6% dividend yield.

Which is still pretty good as things go.

If they can maintain this dividend (and that’s a big if), you’re getting a 8%+ return a year even if share price stays completely flat the next year.

I myself bought Keppel Infrastructure Trust in 2023, and I’m up about 15-20% since just from dividends alone.

What are the risks with Keppel Infrastructure Trust

I’ll sum up 3 key concerns with Keppel Infrastructure Trust:

- What are they doing buying a bus company?

- Financial performance may weaken if inflation cools

- Short lease expiry for many key assets

Keppel Infrastructure Trust bought an Australian bus company?!

My biggest fear with KIT was always that they would go out and buy a big asset that they have little experience running.

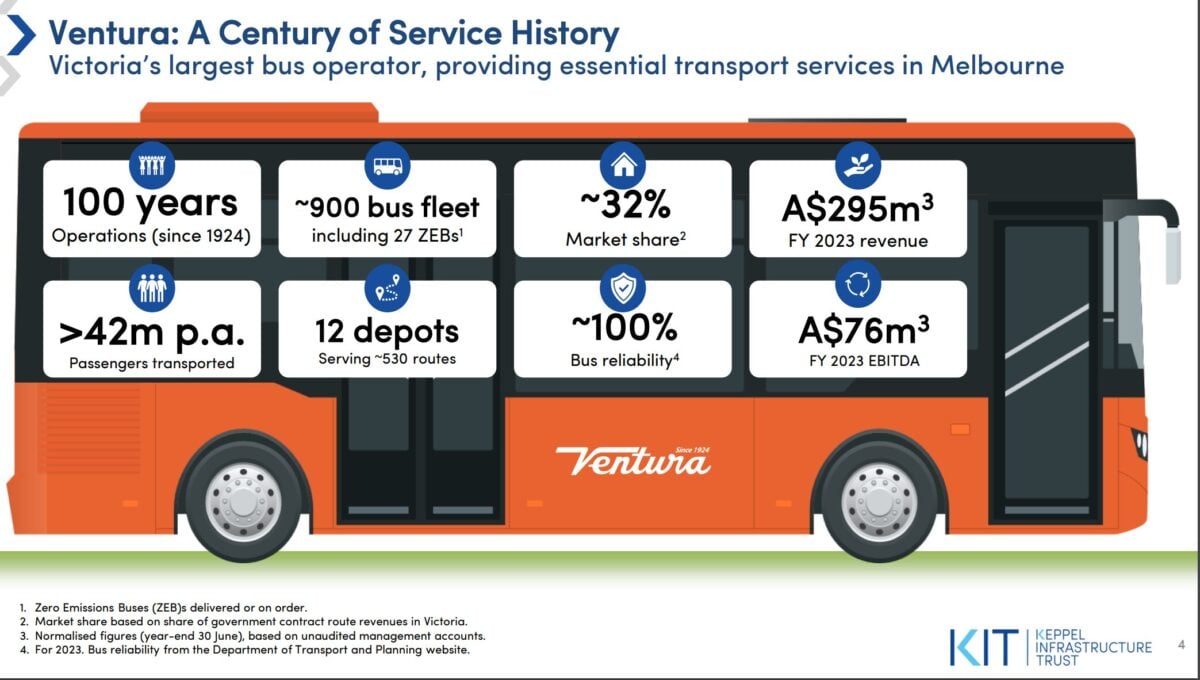

And boy, that was exactly what they did – buying an Australian bus company (Ventura).

This was what I wrote back in Feb:

“yes, logically I understand the appeal of the deal, it being DPU accretive on a 10 year contract blah blah blah.

But the key question in my mind – what the heck is the competitive advantage of Keppel Infrastructure Trust, owning a bus company in Australia?

If this were Comfort Delgro maybe I get the story.

If this were Keppel Intrastructure buying a rubbish disposal company in Australia maybe I get the story.

But a bus company in Australia is about as operational and local as it gets.

It’s a tough business, without any real long term economic moats. And not to mention all the headache from having to deal with local labour markets, manage local stakeholders, bid for renewal contracts and so on.

Keppel Infrastructure Trust’s expertise so far seems to lie in infrastructure assets (think chemicals, rubbish, electricity generation, water so on).

A bus company, I’m really not sure where the competitive advantage lies.

I know the numbers look good, but I’m truly not a fan of this deal.”

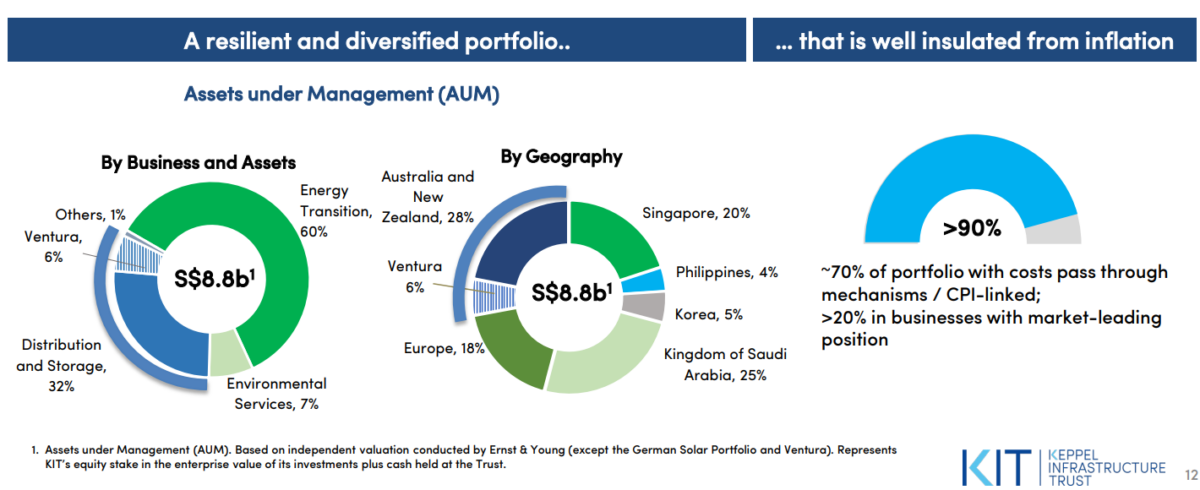

On the bright side… this is only 6% of KIT’s AUM

It’s been half a year since then, and I still am not a big fan of the transaction.

On the bright side though, this acquisition only makes up 6% of Keppel Infrastructure’s asset base.

So it’s not like Mapletree Pan Asia Commercial Trust where 1 bad asset can ruin the entire REIT.

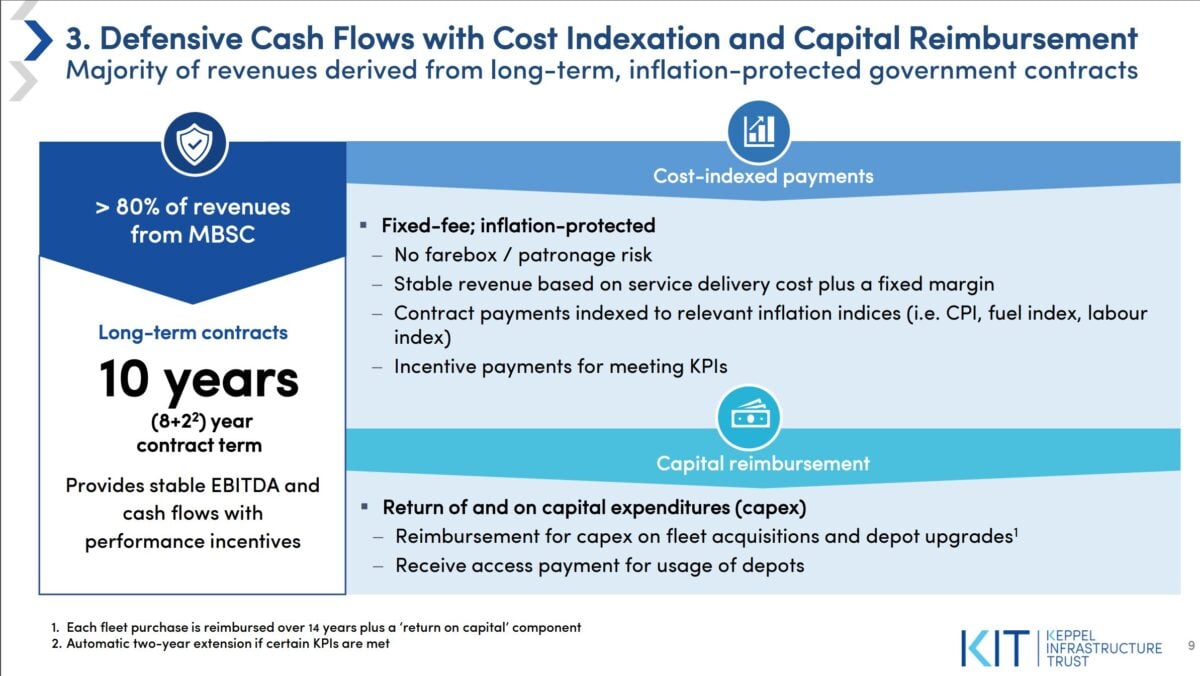

And because 84% of the revenue is locked into a 10 year contract on a cost plus basis.

Hopefully the room to (for lack of a better word) “screw up” in the short term is minimised.

But in the longer term, I really have my concerns whether Keppel Infrastructure Trust is best placed to manage an Australia bus company.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

KIT’s Financial performance may weaken if inflation cools

For what it’s worth, the H1 earnings are not amazing.

Distributable Income is down 31.5% on a year on year basis.

But this is a Business Trust – requires a slightly different method of analysis

That being said, because Keppel Infrastructure Trust is a business trust and not a REIT.

The analysis is slightly different from a REIT.

So if you look deeper into the numbers, you’ll find that if you adjust for certain one-offs, the financials do look a lot better:

1H 2024 would increase by 2.1% y-o-y to $117.8m, after adjusting for one-offs

§ 1H 2024 DI would be $117.8m after adjusting for performance fees ($13m), growth capex ($8.9m) and upfront financing fee ($6.5m) net of base fees

§ 1H 2023 DI would be $115.4m after adjusting for BKR2 debt repayment ($22.4m), upfront financing fee ($2.2m) and growth capex ($0.7m) net of base fees

And based on DPU – DPU is actually up 1% on a year on year basis.

Keppel Infrastructure Trust’s assets do well in an inflationary climate…

The problem as I see it though.

Is that many of KIT’s assets do very well in an inflationary climate.

KIT themselves pointed out that >70% of the portfolio has costs pass through mechanisms / CPI linked.

Ixom for example which makes chemicals, or the electricity / waste management plants – these assets can do very well in an inflationary climate.

So KIT’s assets performed very well in 2022/2023, as that was an inflationary period.

But inflation is coming down…

And I quote from Jerome Powell at Jackson Hole:

“Overall, the economy continues to grow at a solid pace. But the inflation and labor market data show an evolving situation. The upside risks to inflation have diminished. And the downside risks to employment have increased. As we highlighted in our last FOMC statement, we are attentive to the risks to both sides of our dual mandate.

The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.

We will do everything we can to support a strong labor market as we make further progress toward price stability. With an appropriate dialing back of policy restraint, there is good reason to think that the economy will get back to 2 percent inflation while maintaining a strong labor market. The current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of unwelcome further weakening in labor market conditions.”

The problem today.

Is that between inflation and economic slowdown.

The risks appear to have tilted towards the latter.

And that’s an economic climate that may not be so favourable for Keppel Infrastructure Trust’s assets, at least in the short term.

Lower Interest Rates may not help Keppel Infrastructure Trust in a big way

If you look through at Keppel Infrastructure Trust’s financing structure.

You’ll find that most of the debt is not up for refinancing until 2026 (the 2025 refinancing is mainly the term loan for the Ventura acquisition which has been repaid).

While 65% of the debt is fixed rate.

This suggests that Keppel Infrastructure Trust may not be able to benefit in a big way from falling interest rates.

While lower inflation from any economic slowdown may hit their topline revenue (more than the interest saving from lower interest rates).

This may be a problem going forward, especially compared to a plain vanilla REIT.

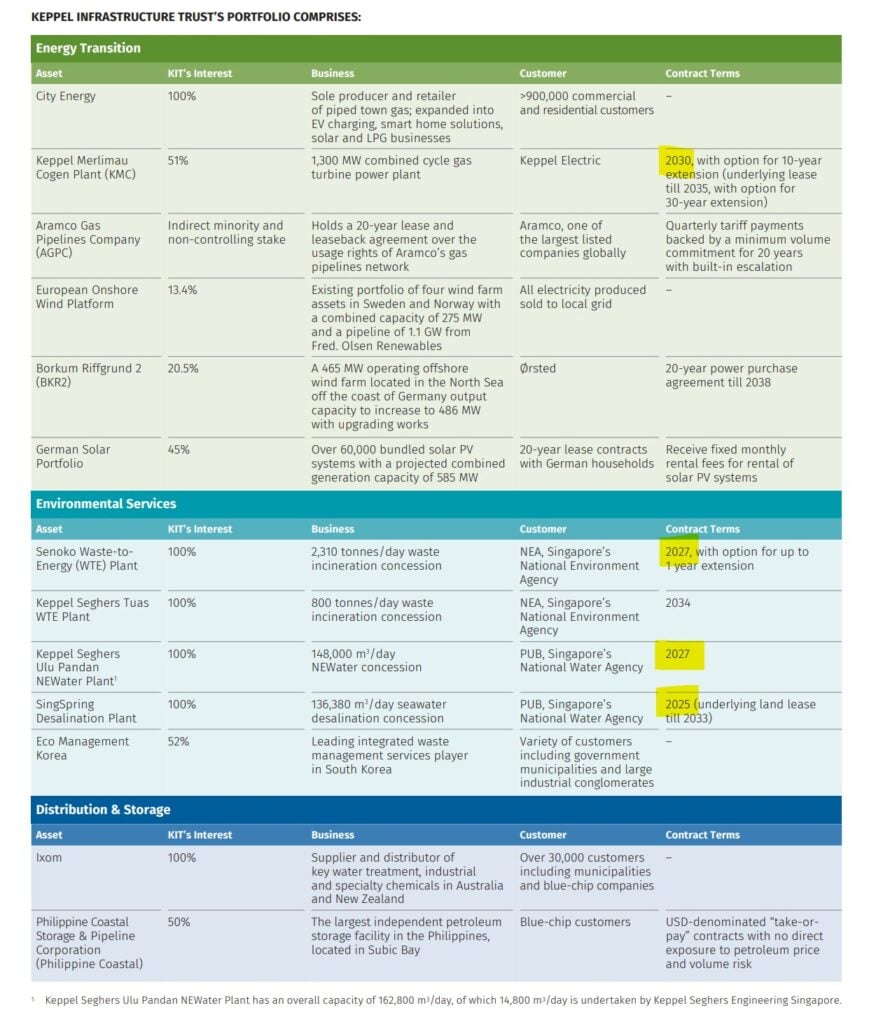

Short Assets lease expiry for Keppel Infrastructure Trust

The final problem.

Is asset lease expiry.

From their latest Annual Report below, you can that quite a few of KIT’s key assets have relatively short lease expiries:

- Keppel Merlimau Cogen Plant – 2030

- Senoko Waste to Energy Plant – 2027

- Keppel Seghers Ulu Pandan NEWater plant – 2025

- SingSpring Desalination Plant – 2025

This is quite different from a REIT that holds freehold properties into perpetuity, and the rental income is icing on the cake.

The high yield with Keppel Infrastructure Trust is partly because of the short leases, and there is a certain element of capital payout with the dividends.

There’s no way around this one unfortunately as the nature of the utilities assets held by KIT in Singapore are only granted short term leases by the regulators.

And to give credit where credit is due, KIT has gone out of their way to address this by buying longer term assets in Europe (wind platforms and solar portfolios) and Saudi Arabia (gas pipelines) – to increase the “remaining lifetime” of the overall portfolio.

Will I buy Keppel Infrastructure Trust at 8.6% dividend yield?

I’m not gonna lie – I liked this Business Trust a lot more back in 2023 when inflation was raging.

Now that inflation has subsided, and risk for interest rates is tilted towards the downside.

I actually prefer REITs a lot more.

Or a business trust with more stability on the income – like Netlink Trust for example (full list of names I like is on the FH stock watch on FH Premium).

The risk with Keppel Infrastructure Trust is that if we have an economic slowdown and rates drop as much as markets are pricing in, a plain vanilla REIT may benefit more.

As shared previously, I bought KIT in 2023, and I’m up about 15-20% since just from dividends alone.

But will I add more KIT today?

I think it really goes back to price.

Technical Analysis of Keppel Infrastructure Trust

KIT generally trades in a 44 – 48 range.

The lower end of the trading range is about $0.44.

That might be decent value for long term holdings.

But that said the stock has been in a downtrend since 2022, and if 0.435 breaks, the next support is 0.40.

Closing Thoughts – So… buy or no buy FH?

From the fundamental analysis above, there are indeed reasons to be concerned about in the near term – especially if lower inflation translates into lower earnings.

So if you’re short term trading this stock, some caution in the short term may be required, especially with the stock in a downtrend.

If you’re a long term investor, then it really goes back to whether you think Keppel Infrastructure Trust’s underlying assets will perform well this decade.

And personally I think the mid term will be inflationary, driven by US-China rivalry, supply chain decoupling, renewable energy, government money printing etc.

So I like the exposure to infrastructure assets if you look past the short term uncertainty.

At the right price, I think KIT is a decent add.

As always I share regular updates on FH Premium as and when I buy / sell KIT, or change my mind on this business trust.

You can also see my full personal portfolio and latest Stock / REIT watchlist on FH Premium.

Love to hear what you think!

This post is written on 30 Aug 2024 and will not be updated going forwards. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Follow Financial Horse to avoid missing any post!

I also send out a newsletter at 10am every Sunday – rounding up the posts from Financial Horse for the week. Sign up below!

May I know what is likely to happen when the 4 assets that you have highlighted expire on their land lease?

Similar to leasehold property – once it expires there is no lease left. It will be up to KIT whether they want to negotiate a new lease with new rates.