Over the past week, we’ve seen:

3 US Banks fail.

The Feds rush in to bail out all depositors at 2 US banks.

A potential run on a Global Systemically Important Bank in Credit Suisse.

That resulted in the Swiss Central Bank coming in to provide an emergency liquidity line.

A lot of commentators are talking about a banking crisis like 2008.

But the more I think about it – the more I think that’s misreading the situation.

Let me explain why.

This is a premium Patreon post. I am making it available to all readers in the hopes that this might help you make sense of what is going on.

If you find this useful, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

My Views on the “Banking Crisis” – Why I still don’t see this as 2008

The more I think about it, the more I think the ground zero this time round, is not the banking sector.

The ground zero this time around, are the industries that have gorged on a decade of easy money.

And which are now paying the price of higher interest rates.

They are:

- Cash burning startups

- Venture Capital (VC)

- Private Equity (PE)

- Private Commercial Real Estate (CRE)

Failure of Silicon Valley Bank is a warning signal for startups / VC

Silicon Valley Bank made 2 cardinal sins.

First – they were overexposed to a single type of depositor: venture backed startups.

This meant very little diversification in their funding base.

When venture backed startups ran out on cash and drew down on their bank deposits, Silicon Valley Bank was very exposed.

Second – they put all the money into a single asset class: long duration US Treasuries / Mortgage Backed Securities.

This means very little diversification in what they invested in.

When interest rates went up rapidly the past year, they suffered massive losses that wiped out their equity base.

This meant Silicon Valley Bank was exposed to the 2 “Ground Zeros” of this cycle:

- Venture backed startups

- Rapidly rising interest rates

Silicon Valley Bank’s failure therefore is not a warning bell for the banking sector.

It is a warning bell for acute funding stress on startups – exacerbated by rising interest rates (and a healthy dose of incompetence on interest rate risk management).

Credit Suisse troubles have been long time coming

Now let’s talk about Credit Suisse.

The incompetence at Credit Suisse is nothing new.

This has been going on for close to a decade.

What changed this week was the failure of Silicon Valley Bank.

Sparking a run on Credit Suisse deposits, and causing credit default swaps (CDS) to blow up.

This threatened to become a self-fulfilling doom loop, forcing the Swiss Central Bank to provide an emergency backstop.

But the “troubles” of Credit Suisse are not from any underlying systemic risk.

It is just from a decade of incompetence.

In any other world they would have been forced to solve their problems years ago.

The only reason why this problem is still playing out, is because we had a decade of zero interest rates that delayed the day of reckoning.

You start to see my point?

You start to see my point here?

Silicon Valley Bank and Credit Suisse are not symptoms of a weak banking sector.

They are the first dominos to fall in an economy that has been conditioned to believe that low interest rates will stay forever.

The underlying problem here is not the banking sector.

The underlying problem here is the investors who made bets that low interest rates will stay here forever. Think loss-making startups, VC, PE, private CRE.

So… what happens next?

With the actions from the regulators the past week.

The fallout from Silicon Valley Bank and Credit Suisse should be contained in the short term.

You might even see a big relief rally.

BUT – doesn’t mean we’re out of the woodwork

That being said, this doesn’t mean we are out of the woodwork just yet.

It’s fairly clear with the events of the past week.

That we are now at the part of the cycle where rising interest rates will start to break things in the real economy.

Silicon Valley Bank and Credit Suisse were the weakest players this cycle – and the first dominos to fall.

They will not be the last.

Risk of Policy Mistake here is very real

Up to this point in the cycle, Jerome Powell could talk tough on interest rates and fighting inflation – because there were no real world consequences associated with it.

Sure, you had some crypto bros losing their fortune, and some frauds being exposed (SBF).

But nothing big in the real economy.

Well, that just changed this week.

When banks start to fail, it’s a whole different ballgame.

From here on out, the real world consequences of higher interest rates start to get very real.

I would be watching Powell very closely from here.

To get clues on how he will balance the inflation fight, vs the need to avoid broader damage to the real economy.

How am I investing in 2023? (as a Singapore Investor)

The million dollar question – how to invest in this climate?

Let me just share what I plan to do.

And then I’ll walk you through my thought process.

As always, investing is about risk-reward, and shifting probabilities.

Nothing is set in stone, and never be afraid to change your mind if the facts change.

This is what I think as of today, but if Powell does something out of the blue next week I will throw my entire playbook out the window.

As should you.

For Long Term Investors

For long term investors, I would still stay heavy cash for now.

I would stay heavy cash until the big stuff starts to break (it will be obvious when it does).

But don’t stay in cash for too long too.

Because I think in the next phase of this crisis, the Feds are going to accept a higher level of inflation (and may even bring back rate cuts / QE).

This will depreciate the value of money itself, and you need to have exposure to stocks / commodities to hedge against inflation.

For Short Term Investors

For short term investors… boy, the next 6 – 12 months are going to be like Disneyland.

I think there’s going to be massive volatility across the board.

A trader’s paradise (if you’re right), or downfall (if you’re wrong).

Short term when the dust settles you may see a relief rally on rate cut / Fed pivot euphoria.

Followed by a bigger drop later when inflation fears return, or bigger stuff starts to break in the economy.

So that’s the TLDR, let’s walk through my reasoning.

I will split this up into the short term, and then the mid term.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Short Term – What is Powell likely to do next week?

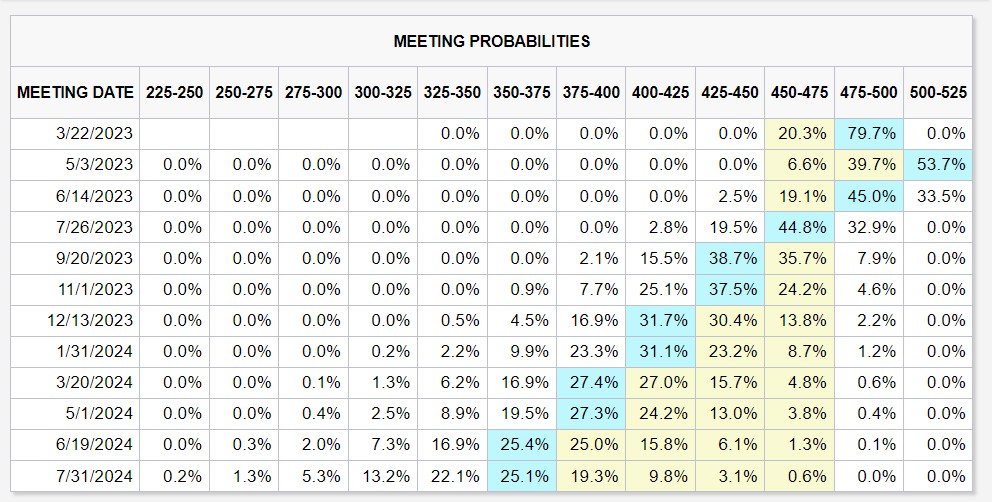

Next week’s FOMC is going to be a massive one to watch.

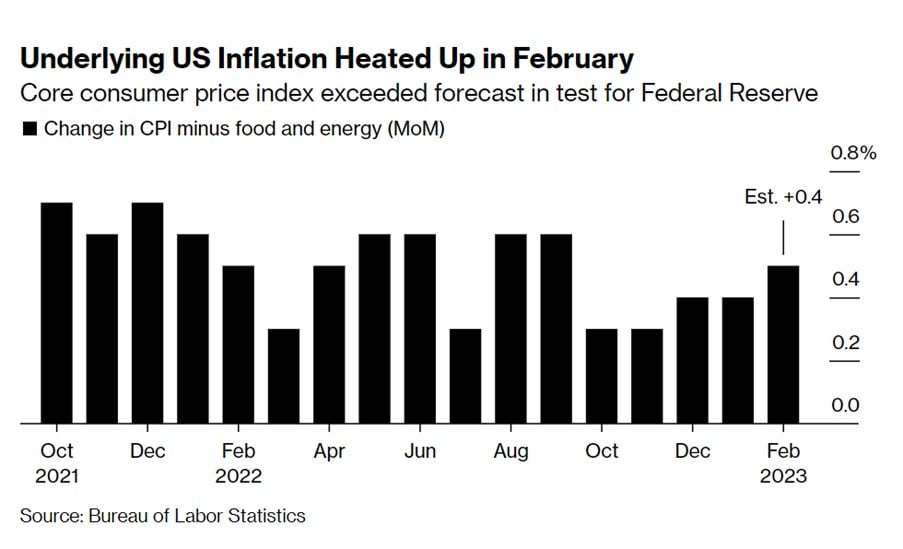

February Core CPI came in very hot at 0.5% month on month, which puts the pressure on the Feds to act on inflation.

Market is pricing in an 80% chance of a 25bps rate hike.

But market also thinks we only see 1 more rate hike after next week (and only a 50% chance at that).

With interest rate cuts as early as June.

As shared on Twitter, my base case for now is a 25 bps hike by the Fed.

A 50 bps is not off the table, but given the volatility across the board it may be counterproductive.

More likely is 25bps, with language from Jerome Powell suggesting a slower pace of hikes until the volatility from Silicon Valley Bank subsides.

This could spark a short term relief rally, that dies down when fears over inflation / economy return.

A repeat of the December 2022 to March 2023 period if you will, where you had a massive rally, followed by a full reversal.

What about inflation?

The problem though.

Is that it’s fairly clear the fight against inflation is not over.

Core CPI at 0.5% month on month is reaccelerating, not slowing down.

But it’s also fairly clear that the economy cannot take the level of interest rates required to stop inflation, without something serious breaking.

We’re only at 4.75% in a rate hike cycle that is less than 12 months, and you’re already seeing 3 bank failures.

Sure – maybe the market is wrong on market pricing and we go to 5.5% or even 6.0% on the Fed Funds Rates.

But after the past week, it’s fairly clear it’s just a matter of time before something bigger breaks in the real economy.

Then what next?

What will Powell do when push really comes to shove?

Now let’s say we’re in 2H 2023.

Fed Funds Rate is at 5.5%.

And something big in the economy breaks, to the point where you have systemic risk and panic across markets.

What happens next?

With the events of the past week, I think it’s starting to become painfully obvious that when push really comes to shove.

Jerome Powell will favour avoiding systemic risk, over crushing inflation.

Jerome Powell is no Paul Volcker, despite what he may say.

If he folded this quickly when it’s the failure of a regional bank.

He will fold even quicker when you have real systemic risk on the table.

So how will this play out in the short term?

So the only question that remains is how do we get from where we are today, to the point where Powell folds like a cheap suit.

You probably need to have something big break in the economy, that creates systemic risk and panic.

I don’t know what exactly this can be.

Every cycle is the same. You can see the stresses building, but you won’t be able to predict the exact catalyst that breaks it.

Timing wise, Ray Dalio wrote in a piece this week that he sees rate cuts and QE probably within the next 12 months.

After the past week, I think that’s a fair enough assessment.

In 2008 terms, we are probably in late 2007 or early 2008.

Mid Term – Path ahead is for money printing and higher inflation?

The inevitable conclusion here though.

Is that the economy won’t be able to take the level of interest rates required to bring inflation down, and when push comes to shove Powell will prioritise the economy (over inflation).

This means that the most likely path in the mid term – is for a return to “easy” monetary policy.

It may not be zero interest rates and unlimited QE.

But it will be easy monetary policy in the sense that it will not be sufficient to bring inflation down to the 2% target.

Because of this, I think you may see inflation stay in a 3-4ish % range for the mid term.

What happens when markets realise this?

And when the markets realise this, that’s when I think all hell breaks loose.

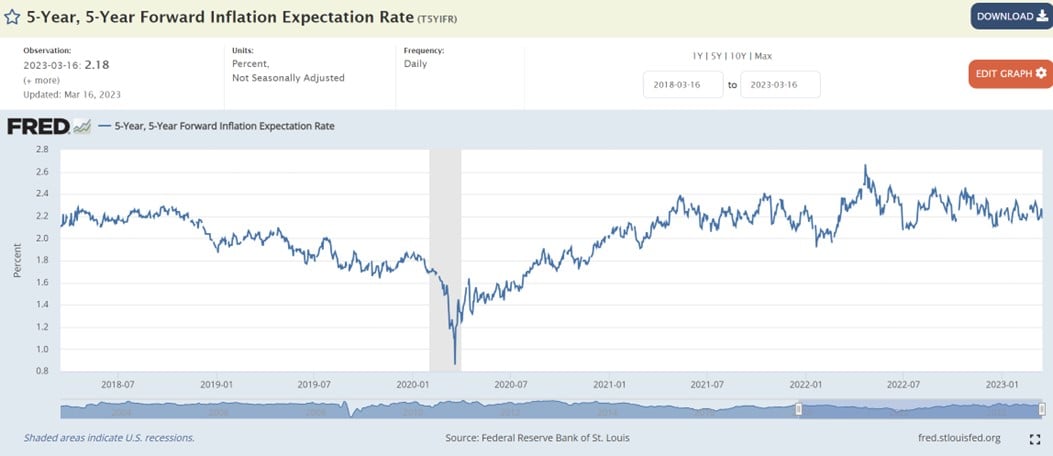

Right now – long term inflation expectations are relatively well anchored because investors expect the Feds to control inflation.

This is the 5 year, 5 year forward inflation expectations.

Which is just a fancy way of saying what the market expects inflation to be in the 5 year period that begins 5 years from now (2028 – 2032).

You can see how over this entire cycle, from 2021 all the way to 2023 – long term inflation expectations never went above 2.5%.

In simple English – the market never for once this cycle, doubted Jerome Powell’s ability to bring inflation down to 2% in the long run.

What happens when that changes?

And here you have 10 Year US Treasuries.

If you hold a 10 year US Treasury to maturity, you will only get a 3.51% return a year.

This only makes sense in a world where inflation is at 2%.

If inflation stays at 4%, you’re basically guaranteed to lose money on a 3.51% yielding Treasury.

When markets realise inflation is not going away, all hell breaks loose…

Once market realises inflation is not going away.

That’s when you have bigger problems.

Because when that happens, investors will start to sell down on long term treasuries.

But remember, if interest rates cross a certain point the economy starts to break.

This forces the Feds into play, to print money and buy Treasuries to prevent yields from going up too much.

More money printing, into what is already higher structural inflation.

That’s when things really get messy.

The value of money itself may depreciate in the next phase.

You will want to hold hard assets like gold, commodities, real estate, the right stocks, to hedge against that.

But… timing is everything

But don’t get ahead of yourself.

Before the Feds can pivot for real, something big in the economy needs to break first.

So for long term investors, I probably still stay heavy cash until this first phase is over and the Feds pivot for real.

For short term investors, feel free to go crazy trading the volatility.

Ray Dalio on how to invest for this new paradigm

Ray Dalio penned quite a meaningful article this week when asked how to invest in a climate like that.

He basically advocates for a balanced portfolio with assets that (1) do well when there are productivity gains (equities) and (2) do well when there is devaluation of money (hard assets like gold, commodities, real estate).

I really like that.

For investors who don’t want to market time and monitor macro risks on a daily basis.

That’s basically the best alternative.

A balanced portfolio to hedge against both scenarios – growth and inflation.

For more specific views on what to buy, and how I am positioning my own portfolio, you can check out my Patreon.

Closing Thoughts: The Europeans are having a field day over this very un-capitalist bailout

This might come across as quite a bleak piece, so I wanted to end off on a lighter note.

What absolutely stole the show for me this week – was this comment from the European Regulators:

One senior eurozone official described their shock at the “total and utter incompetence” of US authorities, particularly after a decade and a half of “long and boring meetings” with Americans advocating an end to bailouts.

“This is the US version of the small Venetian banks,” said one French policy expert, referring to the US’s criticism of Europe’s handling of the failure of Banca Vicenza and Veneto Banca in 2017, where senior bondholders were protected from losses. “You are always systemic for somebody.”

“From a financial stability perspective, they really killed a fly with a sledgehammer,” said Nicolas Véron, a regulation expert at the Washington think-tank the Peterson Institute. Designating SVB as systemic was, Véron added, a “very questionable” decision that set a dangerous precedent for further bailouts of uninsured deposits.

Boy… that’s absolute gold right there.

The Europeans, after bailing out their entire banking sector over the past decade.

Are now criticising the Americans for doing the exact same thing they did (and which the Americans were so critical of the Europeans of doing).

I mean… just reread this line:

One senior eurozone official described their shock at the “total and utter incompetence” of US authorities, particularly after a decade and a half of “long and boring meetings” with Americans advocating an end to bailouts.

Definitely put a smile on this horse’s face.

This is a premium Patreon post. I am making it available to all readers in the hopes that this might help you make sense of what is going on.

If you find this useful, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

As always, this article is written on 17 March 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

There is one big assumption here, that the US economy will continue to do well despite what is happening now……and hence inflation continues to rise. But if economy starts to respond to the multiple hikes and current banking issues (which might translate to lesser liquidity in the system as banks reduce lending), we might not see a jump in inflation going forward. Possible?

Yes, that is absolutely right.

I didn’t delve into that discussion in this article, but there is a good piece of research from Bridgewater that discuses this: https://www.bridgewater.com/research-and-insights/the-tightening-cycle-is-approaching-stage-3-guideposts-were-watching

I think the underlying problem here is that the pain required to bring inflation down for good, is too high for the economy (or politicians) to bear. For the simple reason that they allowed inflation to run too hot this cycle.

Had they started hiking in 2021, we might have a very different conclusion.

But they only started in 2022, by which time inflation was already running too hot.

In any case, if I am wrong on this, then the alternative is straightforward. Without inflation in play, you trade this like any other cycle you would the past 40 years.

Wait for the interest rate cuts + money printing, and go long cyclicals / tech / REITs / long duration.

Just to add though, another possibility is for inflation to come down in the second half of 2023 due to economic weakness and reduced bank lending like you shared.

But when the Feds ease monetary policy, inflation picks up again.

I think the market is underestimating the possibility that inflation could return in multiple waves this decade whenever the Feds ease off the pedal.

Sort of agree with you, though I think Powell is stronger than you think:

1) He says inflation is his number one priority, doesn’t want to go down in history as the next Arthur Burns. This may change when unemployment rises – but not yet…

2) The only tool he has is on the demand side (interest rates). He can’t increase energy production or stop US boomers retiring.

3) He prevented a crisis (bank run) while letting interest rates work their way through to cause a recession.

4) He must raise rates and induce a recession *quickly*, before interest payments on US govt debt roll over into higher rates. That takes 3-4 years, and he started in 2022.

5) He’s worth millions or tens of millions. Doesn’t need his job. His pay is Peanuts.

Maybe nothing systemic “breaks” and we get a normal recession. Like in 2001-02. The stock market will still be fucked. Do you remember anything big breaking in 2001-02 ?

Thanks, great comment. This is possible, at this point we are all second guessing what Powell will do.

Next week will offer more clues on his thinking.

For what it’s worth, I would prefer the scenario that you described, because then at least it has a good chance of solving inflation for good.

Rather than having to have multiple tightening cycles to combat inflation (which would be a nightmare for long term investors).

If you look at the link above (the Bridgewater one), I do have my doubts if Powell (or the politicians) have the stomach to do what it takes to truly solve inflation though. It would require quite a deep recession.

Good comment on 2000 – definitely possible. Although don’t forget that with 2000, we already had the Asian Financial Crisis and LTCM by that point. So to say nothing *big* broke that cycle is really underplaying the pain that played out!

Powell’s net worth is close to 50m based off what I rmb though. Funny that a guy who built his wealth in PE, is now in charge of raising rates that will eventually destroy the industry that built his wealth.

Life’s like that sometimes.

Thought about it a bit more on your point of what happens if there is no big break (like 2000).

In that case does Powell keep rates high, until the signs of a recession become so clear that he is forced to ease?

Possible too. But looking at the past 12 months, the past week, and considering how levered long the world is after the past decade, not sure how likely this is. But definitely possible.

And in any case, that scenario is not bullish for stocks.

“After that, you need to hold short-term interest rates steady for about 18 months” –> Maybe….this is the hardest one.

Even you meet all Bridgewater’s criteria and induce a recession, I don’t know if inflation is defeated. Until we produce more commodities/energy (usually takes 5-7 years) and finish de-globalising (or re-industrialising the US, could take a decade). Otherwise, inflation returns when demand picks up. I’d be positioning for commodity price hikes after the bust.

Meanwhile, hard to know when to recognise the turning point, but its not today.

Hi FH

It is not uncommon… “This is the US version of the small Venetian banks,” said one French policy expert, referring to the US’s criticism of Europe’s handling of the failure of Banca Vicenza and Veneto Banca in 2017, where senior bondholders were protected from losses.

These creditors had to be protected from defaulting on their own loans with other banks in an interconnected financial crises. Like Greece would almost certainly be bailed out by the ECB-IMF when Germany the major voice of the TROIKA’s money was at stake.