I recently chanced across an article by Turtle Investor where he described what he would do with his robo investments if the market crashed (Spoilers Alert: He would sell bonds and buy equities). It got me thinking, we have emergency plans for fires, earthquakes, aeroplane emergency landing, why not one for our investments? Where is the colourful brochure that tells investors what to do in the event of a 20% or 50% crash in share prices?

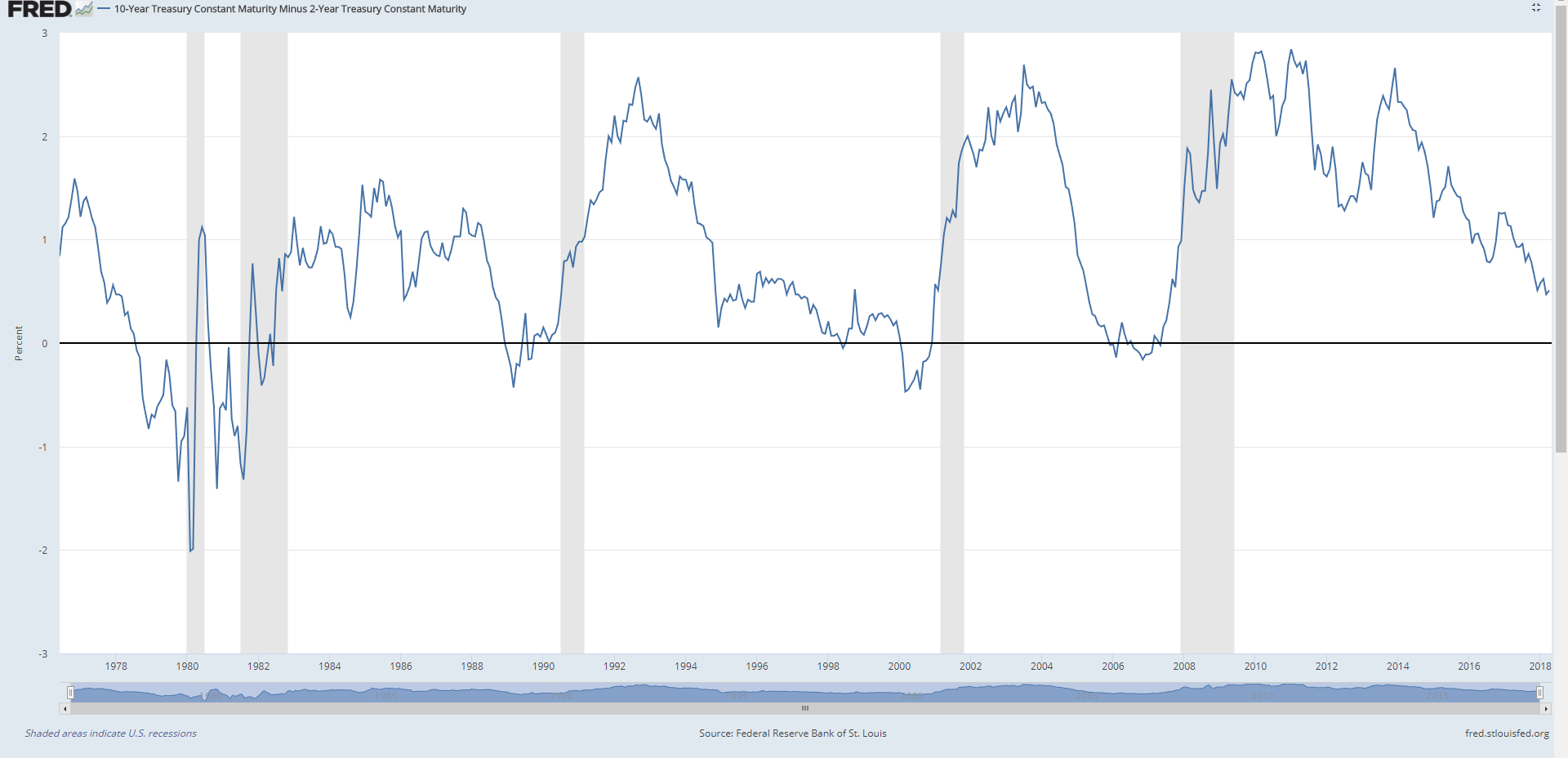

The persistent flattening of the yield curve is starting to look quite worrying. An inversion of the 2s10s US treasury yield curve has preceded every single one of the past 5 recessions, and with the fed on its crusade to raise interest rates, we may be getting to that point sooner than we think (Macro Tourist has a great post here with even more curves).

Siyrce: US FRED

However, no one can predict the exact timing, or the cause of the crash. The next best alternative is to prepare for it.

I have prepared a personal list of 10 stocks that I will buy when the next recession, and market crash, inevitably comes around. The assumptions I used are as follows:

1. Blue Chip Stocks only – The stock must be a blue-chip stock. In a market crash, no one knows which of the smaller operators will survive, and you want to stick with the bluest of the blue chips. If it is temasek linked, even better.

2. 5 to 10 year holding period – The anticipated holding period will be 5 to 10 years, purchasing deep into a market crash and holding until signs that the next cycle is nearing its end. This requires the company to have a sound business model and good investment moat.

3. The world is your oyster – Any stock exchange or asset class is acceptable.

With the technicalities out of the way, let’s dive into the shopping list!

DBS Group Holdings Ltd (D05.SI)

When the market tanks, there is no stock that gets clobbered harder than the bank stocks. Expect to see DBS/OCBC/UOB hit huge, double digit declines as investors worry about slashed interest rates and bad debts. At the same time, this means that the potential of gains is the highest for bank stocks.

Of the 3 local banks, I like DBS the most as detailed in a previous article. They have done very well under Piyush Gupta, and I believe their massive overhaul and modernisation of their back end will reap massive dividends in the future. This digisation and automation of their back end will allow them to keep their bottom line low, and place them in a strong position to rebound from the recessionary depths.

Worst case: Its not called the Development Bank of Singapore for no reason. This bank has strong ties with Temasek (and the government), and is unlikely to ever go bust.

CapitaLand Mall Trust (C38U.SI)

The granddaddy of all S-REITs. CMT was the first REIT to be listed on the SGX, and as they say, the rest is history. Singapore has become one of the deepest and most diverse REIT markets in the whole of Asia since then, but none of them come close to competing with CMT in the retail space.

My personal take is that CMT is by far the best retail REIT you can buy on the market, hands down. All its assets are well situated next to an MRT, and it holds classic Singapore icons such as Plaza Sing and Raffles City. It is also managed by (in my opinion) the best retail operator in town, CapitaLand. I haven’t built up a large position in CMT because I never thought the entry price to be attractive, but with gems like this, sometimes you just have to bite the bullet. In a market crash though, this REIT is one of the first I will be looking to pick up.

CapitaLand Commercial Trust (C61U.SI)

Another no brainer for me. This is basically the CMT of commercial office properties. It holds a good portion of the CBD, and its recent addition of Asia Square Tower 2 is pure icing on the cake. In a market crash, commercial real estate prices can really dive, and picking up this commercial REIT on the cheap will make you a lot of money when the cycle eventually rebounds and office rents pick up.

Mapletree Commercial Trust (N2IU.SI)

MCT is less straightforward. It’s a bit of a hybrid between CMT and CCT as it holds retail, business park, and office buildings. I really like Mapletree as a developer and operator, and I really like the assets and long term potential of this REIT (read here). However, one can always skip this if you have already purchased CMT and CCT. If I were to skip this, I will replace it with a global hospitality REIT, of which Ascott Residence Trust is a solid choice.

Ascendas Real Estate Investment Trust (A17U.SI)

While we are shopping for REITs, let’s pick up some industrial land on the cheap as well. Ascendas REIT is one of the largest operator of industrial land in Singapore, with more than S$10 billion AUM and 130 properties. Temasek backed as well, so no need to worry about any liquidity issues.

In a market crash situation, you want to stay away from the smaller operators such as Viva or AIMS AMP, as you never know when they may face liquidity issues and do a massively dilutive equity fund raising.

Singapore Telecommunications Limited (Z74.SI) / StarHub Ltd (CC3.SI) / M1 Limited (B2F.SI)

I am going to cheat a little here. I really like the telecommunications space. I view it as a utility that will generate solid yield in the years to come. However, this space is a bit too murky for now, given the upcoming entry of a new market participant. A lot of these players have unsustainable dividend payout ratios with declining cash flow, and it is only a matter of time before they start cutting dividends. I also suspect that we may see some consolidation in the years to come.

I need more time to observe how this space plays out, to see which of the 3 will survive, and emerge stronger. I plan to buy the winner. Readers of Financial Horse stay tuned, because once I locate a winner, I will be writing an in-depth article on this.

Alibaba Group Holding Limited (BABA)

I recently wrote a long article professing my love for Jack Ma’s Alibaba. The demographics of this company’s core markets just blow me away. With the proper execution, the potential for this company is limitless. A lot of its relatively younger ventures such as AliPay, AliCloud, E.Lema, all need time to grow to maturity. I would love the opportunity to accumulate on the cheap.

Tencent Holdings is another very solid tech company in the China space. Its Wechat app seems to have almost unlimited usage. Personally I prefer Alibaba as I think the road ahead is a lot clearer, but I can totally understand if readers would prefer to pick up Tencent instead. That is perfectly fine.

Alphabet Inc. (GOOG)

In the US tech space, Google is my number 1 choice of the FAANGs. I always felt Amazon was slightly overhyped, and it is only a matter of time before gravity catches up (because Blue Origin…get it?). There’s a lot of talk about how Amazon and Facebook search are slowly replacing Google search, but I think such talk is premature. Google still controls Android (more than half the smartphone market), Google Maps, YouTube, DeepMind and self-driving car company Waymo (which is way ahead of its competitors). There’s still a lot of room to monetise their other core functions. However, I do acknowledge that there is always the risk of a radical new technology replacing search entirely, and it is vital to keep an eye on this stock to ensure that Google is actively innovating, and not sitting on its laurels.

I think it is fine for now, and the recent pullback in share price actually provides a great entry point into Google, if you were so inclined.

SPDR® S&P 500 ETF (SPY) / PowerShares QQQ ETF (QQQ)

I am going to cheat a little here again. As Singaporeans, it is hard for us to keep track of US counters on a day to day basis, and the US markets are far more volatile than the sleepy SGX-ST. A bad quarterly results can easily see your share price tank 20%. Spare yourself the headache, and admit that you cannot beat the market. Buy the SPY if you are inclined towards the broad US market, or QQQ if you are more tech inclined. Or better yet, buy both, take 5 years off, and make massive profit. Alternatively, if you want to use ETFs to create a buy and forget investment portfolio, check out a simple portfolio I created here.

Cryptocurrencies

This last choice may be quite controversial for some. I have to admit, when I first learnt about Cryptocurrencies, I was highly sceptical as well. Virtual currency via a distributed ledger, and authenticated via the cloud? Who would want to hold that?!

But a lot of successful investing requires having an active imagination, and spotting trends before they happen. You can say what you want about crypto, but if you had bought S$10,000 worth of ether in early 2016, you would now be retired instead of reading this article (its now worth S$6.5 million).

A lot of people thought paper, or fiat currency, was lunacy when it was first introduced. Look where we are today. There is a lot of appeal in a borderless currency that is not answerable to any government. Just look at the recent moves where countries such as Iran are banning cryptocurrencies when faced with a depreciation in the local currency. In the next recession, a lot of citizens in smaller countries may move money into crypto to escape rampant domestic inflation, and you may see cryptos really take off.

It’s a dangerous space for sure, but at the end of the day, investing is about risk vs reward. If you put 0.1% of your net worth on cryptos, your downside is limited, but if crypto takes off, the rewards are limitless. Browse the full list of cryptos here.

Closing Thoughts

My personal thoughts are that we may be nearing the end of this economic cycle. With the amount of debt accumulated in global financial systems, rising interest rates will raise interest repayments and make it harder to finance debt, eventually triggering a wave of default that will reset the financial system. Economic recessions are a healthy part of the business cycle, to clear out the excesses and pave the way for future growth. Unfortunately, in the previous financial crisis, the Feds shortcut this process with artificially depressed interest rates for many years.

No one knows when or what will spark the next recession. The inversion of the yield curve gives investors about a 12 to 18 month warning. The yield curve has not inverted yet, so we are at least 1 to 2 years away from such a crash. There’s some talk about how central bank manipulation of interest rates has destroyed the yield curve as an indicator, and that there may be no need for an inversion to trigger a recession. I leave it to the reader to determine the veracity of such claims, but I personally am not a believer.

Either way, it is vital that we as investors start preparing for what to do when the next financial crisis comes. You do not want to be caught unprepared when it happens.

Thinking about setting up an ETF portfolio instead? Check out the simplified Financial Horse portfolio!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles!

Hi Financial Horse,

Wow! First time seeing a Singapore financial blogger “show hand.”

Now I’m tempted to show hand too! XD

Hi Unintelligent Nerd,

Haha I have always believed in the open sharing of information, and that we are all the richer for it. Ask, and you shall receive!

Yes, I would love if you would “show hand” too. 🙂

Financial Horse, in your opinion what would you do with your current portfolio of stocks when a financial crisis hits? Will you sell them to cash out the profits gathered in the current bull cycle that has spanned for nearly 10 years, and then look to accumulate on the stocks you have discussed above? Thanks!

Hi James,

I am currently monitoring the yield curve very closely. Once it inverts, I will look to exit all my higher risk equity positions (keeping only a few core, blue chip positions) within the 12 months following inversion, and maintain a higher cash/bond buffer.

Once yield curve inverts, I am prepared to sit out a bit of equity gains out of caution, as I think those gains are akin to picking up pennies in front of a steamroller. The risk-benefit analysis will no longer work out.

Of course, there are many strategies that one can employ, and you should decide which is the most appropriate for your personal situation. For example, Sinkie below has shared a great alternative.

Cheers!

I would say also make hay while the sun shines & accumulate a sizeable warchest … maybe 25% to 40% of your overall portfolio. For those with bonds allocation, those can be part of your warchest.

Since I had most of my portfolio in equities, besides accumulating dividends when there is nothing good to buy … I’ve also been practicing “harvesting” whereby I’d sell about 3% whenever an asset’s weekly price reaches overbought / euphoric levels.

You can use any overbought / oversold indicator that you’re comfortable with, but ideally it shouldn’t trigger that often. I use a simple one which is simply a certain % above an asset’s moving average. Of course this will be unique to each particular ETF or stock, and I just backtested over past market cycles to determine the “appropriate” numbers.

So for e.g. an Asia ex-Jap fund that I hold had 5 overbought triggers in 2017, and twice in Jan 2018.

The Fed seems adamant in increasing short term rates over the next 2 years. Likely that we’ll have 4 hikes this year, which will see the Fed Funds Rate at 2.5% by end-2018. Currently the 2s are at 2.48% …. if it doesn’t go up higher, we may see a yield curve inversion on the short end by end-2018. It would seem that the Fed has run low on bullets & are themselves trying to build up their warchest of tools by increasing rates as much as possible, and to run-off outstanding QE as much as possible before the next big downturn.

The worry, as already expressed by most analysts, is the high level of credit stress by companies, and the fact that the vast majority in the last 5 years are either BBB (lowest investment grade) or junk bonds. A lot of the BBBs will be downgraded to junk, and companies will have greater difficulties avoiding defaults as they try to rollover debts at ever-increasing yields. I won’t be surprise if another credit crisis were to initiate the next downturn.

Hi Sinkie,

Amazing comment, and thanks for sharing your investment strategy. I am with you on this. It is starting to look like the Fed will hike the economy into the next recession. However, in some ways this is understandable, because as you pointed out, given how low interest rates are, if a recession were to hit now there are few tools left in the kit apart from negative interest rates and helicopter money.

Given how much debt governments and corporations around the world have accumulated, it is only a matter of time before the rising interest rates triggers a cascading default and the next recession. Unfortunately, the exact timing is anyone’s guess, and I suspect the market may actually see new highs before that point. Interesting to see how this plays out.

Great list FH! Would you also have a target price on these when the crash does hit? Or is it that in the scenario like GFC repeating itself no price is too Low for these marquee names?

Hi Learnitall,

Welcome to Financial Horse! You are absolutely right, I do not have any target price, because how low these names fall would depend on the severity of the recession. If its a mild one it could be 20 – 30% from highs, a severe one could see 50% losses. Each counter would also need to be evaluated on its own basis. For example, while I would normally buy blue-chip REITs when they are trading at a discount to book, in such a crisis commercial real estate prices could take a real dive and the book value of the properties will not be clear. But the point of selecting these blue-chip stocks is to be certain that they will not go under, and that once the storm passes, they will eventually recover their prices once the market recognises their value.

Another way to sidestep this issue is to start dollar cost averaging into stocks over a 12 month period once a crisis hits, because nobody knows when it would bottom out.

Great question!

Hiya!

Really glad to see your list. I have a few of the stocks you mentioned so I’m looking forward to accumulate more. I know you switched from using SC did you ever search for TENCENT from ASE? (Believe the stock code is TCEHY) I couldn’t find it and am really puzzled.

Thank you.

Hello!

Interesting question, why not just buy Tencent Holdings direct from the HKex? Why go to US and buy the ADR?

Cheers.

I don’t have a HK securities account with SC (but have USD). Guess I’ll open one soon 🙂

Hi Financial Horse,

How would you define a “market crash” in the simplest manner to a newbie like me? Thanks!

To keep it very simple, a 50% fall in the S&P500 or the STI, measured from top to bottom. Of course, you can vary the percentage threshold, as well as the index to monitor, but the concept will stay the same. 🙂

Thanks Financial Horse. Your articles are super helpful to a newbie in investing.

May I ask what you do in anticipation for the crash? Remain un-invested totally? Or do you re-allocate into bonds/REITS/dividend stocks etc.? Thanks, really new to this!!!

Thank you and welcome to Financial Horse, Mandy! Really glad they’ve been helpful for you.

The answer depends a lot on your personal situation. I would say if you have spare cash and dont need it for at least 5 to 10 years, then just invest it. There were a lot of people who have been waiting for a crash to buy shares, and they’ve been waiting since 2011.

Nobody knows when the next recession will come, and while I think we are nearing the end of this business cycle, I still think there’s at least some time to go before then. What I’m doing personally is to continue to invest opportunistically, while moving my portfolio to a more defensive position with more cash and government bonds.

Hope this helps. Cheers!