In the earlier part of this series, I examined StashAway and AutoWealth and explained why Financial Horse would not use a robo-adviser in its current form. But Financial Horse is an investing enthusiast who spends every waking hour reading up on investment strategies and annual reports. I recognise that not everyone is this obsessive.

In this article, I will propose a simple DIY alternative that doesn’t require too extensive financial knowledge, or effort from the part of the investor.

Let’s imagine a hypothetical investor John. John is 25 years old. He has just graduated from NUS (with an engineering degree!), and earns a nice S$4,000 a month that he is very proud of. He wants to start investing, but he doesn’t really know much about financial markets or how to read a financial statement. He wants to park his money somewhere, make regular investments, and collect it in 30 years when he wants to retire. In fact, he is unconcerned with financial markets that he will only make new investments or sell securities on one trading day each year (his auspicious trading day). To minimise costs, he decides to open a Standard Chartered Trading Account, because the minimum commission is USD10, and there is no additional charge per quarter for US shares (John is really picky you see).

For John, I propose the following asset allocation, which I shall call the Financial Horse Alternative to Robo Advisers (FHARA):

As John is young, he can afford to have an outsized allocation to equities. The split will be 20% bonds and 80% equities, subdivided as follows:

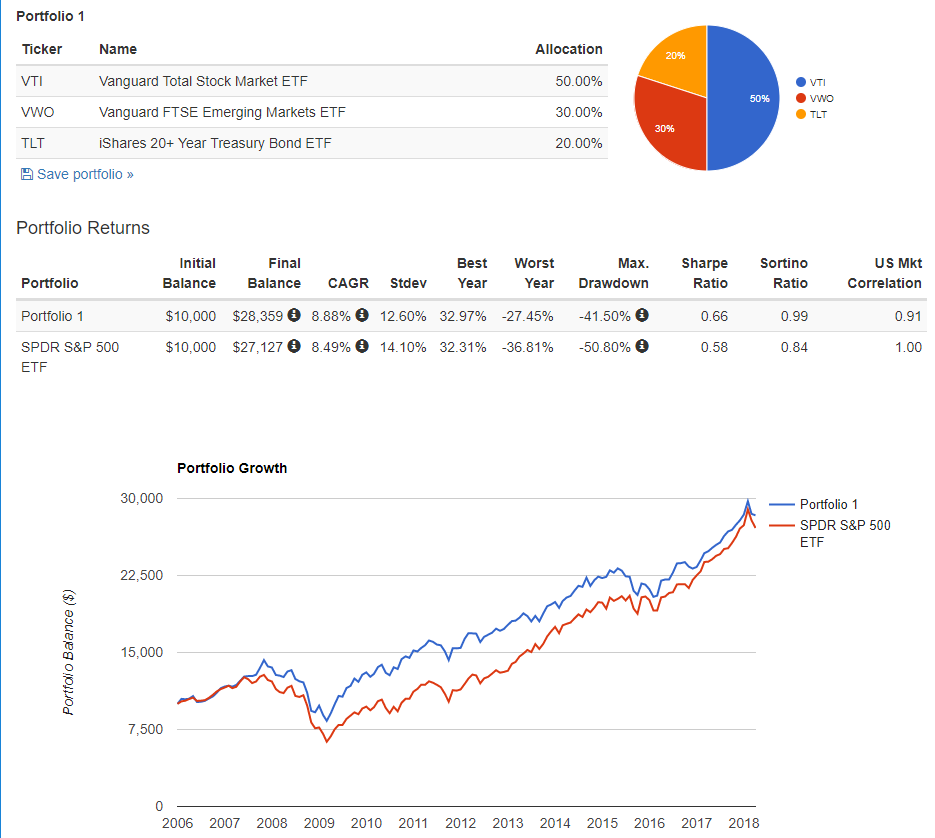

| Asset Class | ETF | Allocation |

| US Equities | NYSEARCA: VTI | 50% |

| Rest of the World | NYSEARCA: VWO | 30% |

| Bonds | NASDAQ: TLT | 20% |

When coming up with this portfolio, I kept it as simple as possible, so that John does not need to keep track of too many counters, but at the same time trying to maximise his diversification.

Let’s backtest this allocation over the past 10 years (assuming a 10,000 starting investment, rebalanced annually).

As you can see, had John started doing this in 2005, he would have a CAGR of 8.88%, and his initial S$10,000 would have turned into S$28,359. His worst year would have been 2008 when he lost 27%, the worst drawdown would have been 41%. He actually outperformed the benchmark S&P500, which had a CAGR of 8.49%, but the S&P took on much higher risks (it lost 36% in 2008, and the max drawdown was 50%).

Source: Portfolio Visualiser

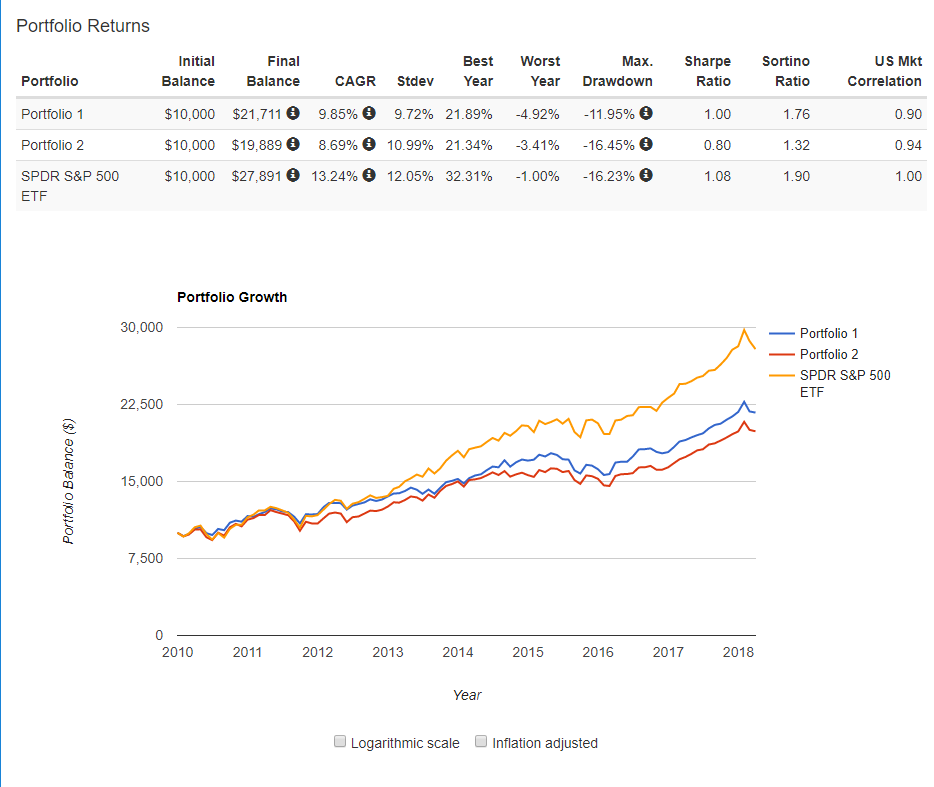

John also decides to compare his returns with his friend who used a Robo-Adviser (let’s call this imaginary 2005 robo-adviser Magic Wealth). Magic Wealth used a far more complex asset allocation (which just for kicks, I used the allocation that AutoWealth gave me from Part I).

Since 2009, John would have returned a 9.85% CAGR, while his friend in Magic Wealth had an 8.69% return. After 0.5% fees, his friend in Magic Wealth would have made about an 8.2% CAGR. So John outperformed his friend by a mind-blowing 20%.

Of course, the S&P500 outperformed both John and MagicWealth because there has been no financial crisis since 2009. As you can see from the 2005 returns above, once a financial crisis kicks in, John/MagicWealth’s portfolio will outperform a pure equity allocation because of the stabilising effect of bonds. I wanted to backtest it further to illustrate this point, but unfortunately the IGOV ETF that Magic Wealth used doesn’t go back beyond 2009.

Chart: Portfolio 1 is Financial Horse, Portfolio 2 is Magic Wealth.

Source: Portfolio Visualiser

MagicWealth’s Allocation

| Ticker | Name | Allocation |

| VTI | Vanguard Total Stock Market ETF | 43.50% |

| VWO | Vanguard FTSE Emerging Markets ETF | 9.20% |

| VGK | Vanguard FTSE Europe ETF | 17.50% |

| VPL | Vanguard FTSE Pacific ETF | 9.80% |

| IEF | iShares 7-10 Year Treasury Bond ETF | 6.90% |

| IGOV | iShares International Treasury Bond ETF | 13.10% |

So now John is a very happy man indeed. Because even though he didn’t know anything about investing and financial statements, and he only looked at his investment 1 day a year, he has outperformed his friend in Magic Wealth, he has outperformed the benchmark S&P500 (since 2005), and he has destroyed the returns that his hedge fund friends had.

Note: A reader reached out to me with great clarificatory questions, that I felt was worth replicating here. The original questions, and my responses, below:

1) Your backtesting is based on a single investment with yearly rebalancing. For retail investors, we make multiple investments. How would you deal with the fees vs. opportunity cost (from holding cash) trade-off? In other words, how often would you invest in VTI, VWO, etc.?

Response: When backtesting, I noticed that when rebalancing quarterly, the performance over the past 15 years actually dropped to 8.38% (vs 8.88%). I guess the point is this, rebalancing is important over long periods of time, but to rebalance too often can actually be counter-productive.

For retail investors, I would suggest annual/semi-annual rebalancing, and to allocate a small percentage of your portfolio into risk capital. This risk capital can be used to invest in specific counters you are interested in. I find that this helps to keep one away from excessive tempering with the core portfolio, and serves as a “creative outlet” for trading.

2) Converting SGD to USD (and back to SGD) result in large bank currency fees for retail investors. Do you think Robo Advisors have economies of scale (from narrower bid-ask spreads) from SGD-USD conversions that outweigh their fees?

Response: The Robos typically use Saxo as a broker, and I suspect they have much narrower bid-ask spreads than available to retail. However, I would be highly surprised if this makes up for their hefty fees.

If you are concerned with fees, DBS Vickers/Interactive Brokers provides a very competitive forex spread. There are certain minimum charges that comes with both, but with larger investment sums, these costs as a percentage of your portfolio become trivial.

3) By investing in USD, there’s exposure to FX risk. Returns get eaten up when USD depreciates against SGD. How should a retail investor deal with this risk? Is there a cheap way to hedge?

Response: I do not advise hedging the USD position fully, because part of the intention behind a USD investment is to diversify the portfolio away from Singapore, and you do want the exposure to USD.

However, to address your question, there is no cheap way for retail investors to hedge, as we are not companies like Mapletree with easy access to sophisticated financial products.

The future of Robos

I chanced upon this great article from Wired that I highly recommend you to read if you are serious about investing in a Robo. Basically, it tells the story of Wealthfront, a large US robo adviser that when faced with the prospect of low fees, eventually decide to:

invest 20% of its investors’ funds into an internal “risk parity” fund, which in turn is invested mostly in complex derivatives known as total return swaps. The fees associated with the old strategy averaged out at 0.09%; the new strategy, by contrast, carries a fixed fee of 0.50%, all of which goes directly to Wealthfront, plus the costs associated with buying the swaps. Informed observers say the cost of the swaps could be as much as 3% or even more, depending on the amount of leverage involved.

And it gets better, because

Wealthfront is implementing this change on an opt-out basis rather than an opt-in basis, many investors who signed up for passive management will find themselves put into an active strategy unless they explicitly tell their fund manager that they don’t want to follow its recommendations. Which is a pretty awkward thing to do, especially when a large part of the reason for signing up with Wealthfront is precisely because you don’t feel qualified to make such decisions.

I am not saying that AutoWealth or StashAway will one day go down the same route. But the crux of the issue is that at the kind of fees that the Robos are charging, the business model does not look sustainable.

The problem is that Robo-advisers occupy a very strange place on the spectrum of financial products. Unsophisticated investors are more likely to purchase a product from a financial adviser, because they don’t really understand this space, and they prefer to have a human being to walk them through their investment, and whom they can call when shit hits the fan. You can try to sell them the merits of a robo-adviser, but at the end of the day, investing is not like online shopping. Its not like buying a laptop off Lazada where you immediately save 5% on the purchase price and are pleased. Investing, and compounded returns / superior asset allocation strategies only manifest themselves over multi-decade periods.

At the same time, a true DIY investing enthusiast would not invest in a Robo because he resents the high fees paid, and he values the greater control over his asset allocation that comes with a direct investment in the underlying securities.

To me, the Robo’s ideal target audience is a millennial. Millennials are more likely to trust a computer with their investment than the older generation, they are somewhat financially savvy and can understand the merits of a passive investing strategy. The ideal millennial is also one who doesn’t have the time to monitor his investments closely, and prefers to leave it all to a Robo to do the rebalancing. But as we have seen above, a simple DIY portfolio with annual adjustments can achieve returns that are highly competitive with robo-advisers, and that’s before we include fees. Which I why I suspect that over time, these Robos may need to amend their business model to further appeal to this crowd, because they really do not do enough to justify their 0.5% fees currently.

Fee based income from investment funds are a thing of the past. Hedge funds are facing massive fee compression as they are finding it harder and harder to justify their 2+20 fee structure (2% of asset base and 20% of returns) when a broad index fund charges 0.2% fees and outperforms the hedge fund. The simple truth is that when a hedge fund that charges 2+20 fees, it has to outperform the market by more than 2%. With an S&P500 return of 8%, the fund must return more than 10%, which can be incredibly hard to do.

Here’s a radical idea. What if we throw all our preconceptions about robo-advisers out the window, and restart from the ground up. Financial Horse did exactly that, and here is what I came up with:

The Financial Horse Robo-Adviser

When opening an account, you answer a small list of questions about your income, age and goals. This is used to generate an initial portfolio. However you are completely free to amend the asset allocation as you please. At any time during the year, you can also choose to amend your asset allocation. Based on this allocation, the Robo will perform quarterly rebalancing. The annual fees for this Financial Horse Robo-Adviser is a grand total of 0.0%. Of course, there are premium products being sold. You can choose to take up margin, purchase derivatives to hedge your position (forex risk for example) or purchase cryptocurrencies for a small fee, but the base product is free.

If you thought this was crazy, think again. Robin Hood pioneered zero fee stock trading which everyone though was insanity, and today they are valued at US$5 billion.

I don’t know about you, but I would strongly consider putting my new investments into this Financial Horse Robo-Adviser. What are your thoughts? Let me know if there is demand in the comments section, and I will explore the creation of such a product.

Closing Thoughts

Robo-advisers take the concept of passive index investing and turn it into a product where they can earn fees. I view them as evolutionary, rather than revolutionary. However, in their current form and at the current price point, I don’t see them surviving over longer periods. The margins are just too small.

There are only 2 ways to progress: (1) Increase the fees (which turns them into a pseudo-active managed fund, and is the path WealthFront took), (2) Decrease the fees, to 0.1 to 0.2% (or even better, free or charge). The former allows them to invest heavily into sales and marketing costs to target retail investors, and the latter allows them to target DIY investing enthusiasts and millennials.

The US market is ahead of Singapore in many ways, and I think we are already starting to see these changes manifest themselves in the US Robos.

I will give AutoWealth a 2.5 Financial Horse Rating. I like it more than StashAway because there is no “reoptimisation”, and the fees are lower (for sums below S$450,000). However, a lot of the limitations remain. These are deceptively simple products, but there are a myriad of considerations that go into choosing which product to use. Invest carefully, and keep an eye on this space going forward, because my suspicion is that over the next 5 years, we may see a change in the business model for roboadvisers.

AutoWealth – Financial Horse Rating

![]()

Read my original article on StashAway.

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles!

Well, robos in Singapore will tell you that you’re able to invest with low sums & get fractional shares, hahaha!

Yeah, with the no-brainer tax system in S’pore (actually taxless for local financial assets), fees for local robos are rather expensive. Guess that’s why Stashaway is attempting to add extra with some quantitative active allocation. I’ll be happy to pay local robos’ fees if they can make the 30% dividend WT disappear haha.

Unlike in US, where taxes are a nightmare for US investors & even simple rebalancing has to be done carefully lest you get hit with higher short-term capital gains tax. Robos there also do tax loss harvesting that helps to lower CGT. By helping to minimize taxes, US robos help to justify their fees.

Actually I think the simplest, low cost method for local investor is to stick to 2 ETFs trading on local bourse — a global stock ETF & a bond ETF. No fuss about dividend WT & currency exchange. The only downside is that that only local bond ETF I can think of is not that fantastic … almost like short term Treasuries.

TLT, while great when SHTF, is bad for Sinkies when USD has been generally depreciating against the maturing SGD over the last 20 years.

Hi Sinkie,

Great comment! You raised an absolutely great point, that capital gains tax in US means that robos actually play a great role in acting as a psuedo tax adviser.

Interesting suggesting about the 2 local ETFs. The problem is that the local bond market is not as deep or as liquid as the US treasuries market. I’ve been hunting around for a while, but I find that when building a long term portfolio, there is no true alternative to US treasuries available at the moment. Each has their own limitations.

Cheers. Great comment.

hmmm.. interesting proposition…. if say, hypothetically, all the clients only take up the base product ( singaporeans right?.. must take free) , how is the robo going to make any money?

Hi FC,

There are many ways to make money from a free product. Apart from the usual fundraising as a fast-growing startup, the robo can also do targetted advertising, product placement etc. More “creative” methods would include raising built-in transaction fees or a higher forex spread.

Cheers.

Can we reduce withholding stocks through buying through etfs listed in Ireland? Which ones and how much can we save?

Hi Ken,

I believe that James has answered your question below. But if you have any queries, feel free to let me know!

Cheers

I agree with the first point re local ETFs, and would also appreciate if local REITs could be introduced to assist with diversification. I also think an important advantage of the robos is that they strip human emotions out of investing, and there are many books which explore the advantages of back-tested algorithms, which remove much of the investment risk with minimal impact on gains.. Something which would appeal to the over fifties for sure.

Agreed. I actually thought that a huge plus point about robos is that they automate the entire process and strip the emotion out of investing. The problem though, is that there is no lock up period, and minimal costs associated with withdrawing all your assets from a robo. I can see a situtaion where the next market crash comes, and investors who see 30% losses on their portfolio will just pull out entirely.

I think there is a better alternative than investing in the Vanguard ETFs based in the U.S due to its 30% withholding tax. Which is to buy the IShares variant found on the london stock exchange which is subjected to 15% withholding tax instead of the 30%. For instance the iShares Core MSCI World UCITS ETF (IWDA) and iShares Core MSCI EM IMI UCITS ETF (EIMI) as an alternative to VTI and VWO respectively.

would like to point out additionally that both ishares etf mentioned above are denominated in usd as well, and they reinvest the dividends given so returns might be better than the vanguard ones in the long run

Hi James,

Great comment and thanks for pointing these out! You have inadvertently answered the query from a commenter above!

Cheers

Great article! I deeply appreciate the efforts made to present this idea so clearly. Also, a big thanks to James for an interesting concept. A follow up question, would the London based variants of the US ETFs also bypass the estate taxation laws? Looking forward to hearing your thoughts, NSAC

Hi NSAC,

Thanks for the question, and welcome to Financial Horse! Tax regulations are always tricky, but the prima facie position is that you will not be subject to inheritance tax if you are not resident or domiciled in the UK. Even if you are, there is a £325,000 threshold before inheritance tax kicks in, so if your UK assets are purely ETFs, it should not be a huge problem. There are a couple of great articles at https://www.bogleheads.org/forum/viewtopic.php?t=221000 and https://www.turtleinvestor.net/inheritance-tax-for-index-investors-is-important/ that you can take a look at if you are serious about the risk of inheritance tax. Do note however, that this shouldn’t be a replacement for formal tax advice. 🙂

Truly valuable insights on the Robo-Advisors.

When are you launching the home grown ‘Financial Horse Robo-Adviser’? 🙂

Thanks,

Jp

Thanks for the amazing article! Feeling a lot less uncertainty moving forward.

Hopefully this question isn’t too out of topic, but I had 2 questions that I was hoping for insights on.

1) I was told that the index works great in US because the markets are efficient. However, this is a lot less so outside of US, so it’s relatively easy for a fund to beat non-US indexes. Any thoughts on that?

2) On a related note, I was thinking of lowering the portfolio’s reliance on US stocks, and adding more weight to global indexes instead. Anything I should think of other than where I think the economies are heading?

Thanks again for any thoughts anyone might provide!

Great comments! Couple of my thoughts below:

1) It really depends on what index you use, and whether you factor in the fees of the funds. If its a big index like the Hang Seng Index, I’m not sure if you can find many funds that beat the Hang Seng, after deducting the fund fees. The STI is a trickier one because it’s really not a good index, and I shared my thoughts on this previously. If you use a different index like the one used by the recent Phillip Sing Income ETF, I find it hard to find any fund that would outperform after fees.

2) That’s absolutely fine, if you prefer to have less weight on US. Don’t forget that US stocks do form a pretty hefty portfion of a global index as well. To be honest, in this day and age, financial markets are so closely intertwined that if one country such as China doesn’t do well, global stocks don’t do well either.

Really good questions though, I really enjoyed them! There will be no definitive answer to these questions, but I do hope t hat I’ve provided some food for thought!

Assuming we plan to buy vanguard etf. How do you propose to purchase them? Do we do a 1 lump sum per Yr ($1000 to $20000 per year) becos of the trading cost? What should the strategy be?

Any recommendations?

Great question!

I would recommmend doing quarterly purchases to save on transaction costs. It’s also a form of dollar cost averaging that’s easy to implement, as you just have to remember to make the puchase at the end of each quarter. For rebalancing, once a year is fine, just do it whenever you’re freer in the year (eg. December).

For stock brokers to use, you can check out my recent article here: https://financialhorse.com/stock-brokers/

Cheers!

Hi Financial Horse, I am 38 years old (starting late!) and totally new to DIY investing (in process of reading up on building a 3-fund portfolio).

My asset allocation will be 50% in US equities (IWDA), 30% for rest of the world (EIMI), and 20% in bonds (which I am not sure which to consider yet). After deducting 15% withholding tax (for an Ireland domiciled bond), the returns will be pretty mediocre? Hence, will taking on an SG bond (looking at ABF SG Bond ETF) be recommended instead?

Hi!

Welcome to Financial Horse!

I’ve always had the same problem you have with bond funds. US Treasury funds are subject to withholding tax, which takes out a chunk of the returns. Singapore Bond funds have poor liquidity (can be hard to exit), and because of the poor liquidity they don’t trade inversely with stocks very well (which is part of the purpose of the bond funds, to reduce stock volatility).

So ultimately, it’s really about picking the least bad alternative, and your financial objectives. If you want a bond portfolio to smooth out equity volatility in the next crisis, you’ll probably want a treasury bond fund. If you just want a bond portfolio as an emergency fund that also pays interest, something like SSBs actually work very well, as you sidestep the whole liquidity issue involved when ABF SG Bond ETF.

Hope that this help, and good luck with your investments! 🙂

Financial Horse Robo-Adviser? Yes please!

Haha, I’ll let you know when I get it up. 😉

Hi FH, I have read quite a bit of your posts and it’s really informative and helpful! But on this topic, I am a bit hesitant because some of your posts are quite pro-StashAway (SA) and some pro-AutoWealth (AW). Understood both might have upgraded versions improving their selling points. I am still rather torn in-between. Do you think it’s silly if I just decide to put $10k each to try out both SA & AW for a short period of say, 5 years and measure the outcome from there? Or do you think it would be better if I just select one (either SA or AW) and pump in $20k in order to generate me higher returns after 5 years?

Absolutely not. If you’ve done your due diligence and are still split between the two, splitting your money in both could be a great option. Unfortunately I havent been keeping up to date with the changes on either of Autowealth and StashAway, so I’m not able to comment meaningfully on the performance/asset allocation of either as they likely would have changed significantly since the time of my article. 🙂

I must say you run a great blog which is very informative. I had a query with regards to wills and estate tax. I understand that you can benefit from using Irish domiciled ETFs which give you the lower dividend distribution tax as well avoid US estate tax which you would if you use US domiciled ETFs instead. However in terms of one’s family accessing your funds/ investments in case of account holder’s death, how would that work. Since you are not allowed to nominate a beneficiary, would the family need a will and will it be a hassle free process to claim the investments?

Not legal advice of course, but my thoughts:

1) If your family has your account details, that’s the easiest (but this would be tax evasion, wink wink)

2) If not, then the shares become part of your estate, and your testator will deal with them as part of the estate.