Did you know? Most people accumulate 90% of their net worth after age 40.

This is why it is important to be financially savvy in your 20s and 30s, to get the ball rolling for that wealth accumulation in your 40s.

Today’s post explores 6 money traps to avoid in your 30s.

1. Expensive Car

While cars are seen to be a normal expense in many other countries like the US, cars are definitely a luxury item in Singapore.

We’ve seen the reactions of the stars of Fast & Furious to prices of cars in Singapore, and chuckled at their stunned faces.

It doesn’t help that COE premiums are reaching record highs.

To combat this, there’s a new counting method, such that the COE quota for August to October will be 11.5% less.

Fundamentally, cars are a big-ticket item that needs to be planned carefully.

From the moment you drive a brand new car off the lot, it depreciates in value drastically. So a wise option to consider are second-hand cars.

Other important considerations include functionality of the car, the costs of car maintenance and repairs, and financing.

If your lifestyle doesn’t necessitate it, renting a car on occassion, or just taking Grab/Gojek can actually be way more economical.

2. Not maximizing your home loan

While many people warn of buying “too expensive” a home, if you want to build serious wealth, it is actually not a bad idea to stretch yourself when purchasing a home (in a smart way).

In Singapore, home ownership is often seen as a key pillar of financial security.

As first-time home owners, you often get plenty of great benefits such as enhanced CPF housing grants, and more leeway for you to borrow money (in terms of both TDSR, and the amount of time you can take a loan e.g. 30-year mortgage).

The total debt servicing ratio (TDSR) is a maximum threshold set by MAS.

In your early 30s, this is likely to be the best time for you to take a housing loan – and you should maximize it.

By maximizing your home loan, you get to own an asset that can appreciate while taking advantage of cheap financing.

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

There’s a by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try .

3. Spending too much on booze

Another common money trap for people in their 30s is to spend too much on going out – especially when this is coupled with spending on alcohol.

According to Statista, Singapore is one of the most expensive cities worldwide for consuming alcohol, averaging at around 24 USD for a bottle of table wine and eight USD for a pint of beer.

Studies have also uncovered the problem of ‘pandemic drinking’, where people drink to cope with the boredom and stress of Covid-19.

This is exacerbated by online delivery services, which makes obtaining alcohol easier than ever before.

Be mindful about over-spending on booze – since this also has a detrimental effect to your health!

4. Credit card debt

Everyone knows that credit card debt is bad.

If you had any credit debt in your 20s, this is the time to settle it once and for all.

In our interview with Redbrick, one of the unexpected woes that home-buyers faced was their credit score being ruined by small or forgotten credit card loans in their 20s.

A simple late fee or forgetting to cancel a card in their 20s, has gone on to ruin their credit standing with banks, and affecting their home loans in their 30s.

If you are facing difficulties with your credit card debt, you can get help & resources through Credit Counselling Singapore (CCS).

5. Not investing aggressively enough

Most people are aware of the importance of investing, but they are often not investing aggressively enough.

Especially with having more financial responsibilities in general, many people in their 30s are too conservative when it comes to investing.

Of course, everyone’s risk appetite is different – and you should do what’s comfortable for you.

But there are some ways to push yourself out of your comfort zone – so that these investments can pay off big later in life.

Especially if you chose conservatively regarding home ownership, you are likely to have more leeway to build a more aggressive stock portfolio.

Remind yourself that in your 30s, you can afford to hold stocks for 10, 20 years, and therefore it’s OK to accumulate a higher proportion of growth-oriented stocks into your portfolio.

At the very least, try to make sure money isn’t just sitting in the bank. Put your cash in higher-interest savings accounts, SSBs or Temasek-linked bonds.

You can also consider topping up your CPF SA to enjoy higher interest rates and tax relief.

You get up to $8,000 tax relief when you top up for yourself and another $8,000 when you top up for your family.

Quick tip from CPF: If you top up early in the year, you can earn more interest through the power of compounding. By topping up in January rather than December, you could earn up to 20% more interest on your top-ups in just 10 years.

6. Not planning holistically for retirement

Finally, the biggest money trap is not planning holistically for retirement.

Our 30s is where big life choices tend to be made – which seriously affect how our retirement looks like.

The top 2 factors would be: (1) career ; and (2) family planning.

In your 30s, your career trajectory tends to be on the upward rise, you have opportunities to really push yourself into a senior position, to change careers, or even start a business.

You also make important decisions on family planning.

You may also start thinking about supporting your parents who are retiring. Will they be able to cover their own health costs?

All in all, it is important to think holistically about retirement:

- How do you foresee your career trajectory?

- How do you foresee family planning?

and

- When do I want to retire?

- What kind of retirement lifestyle do I want?

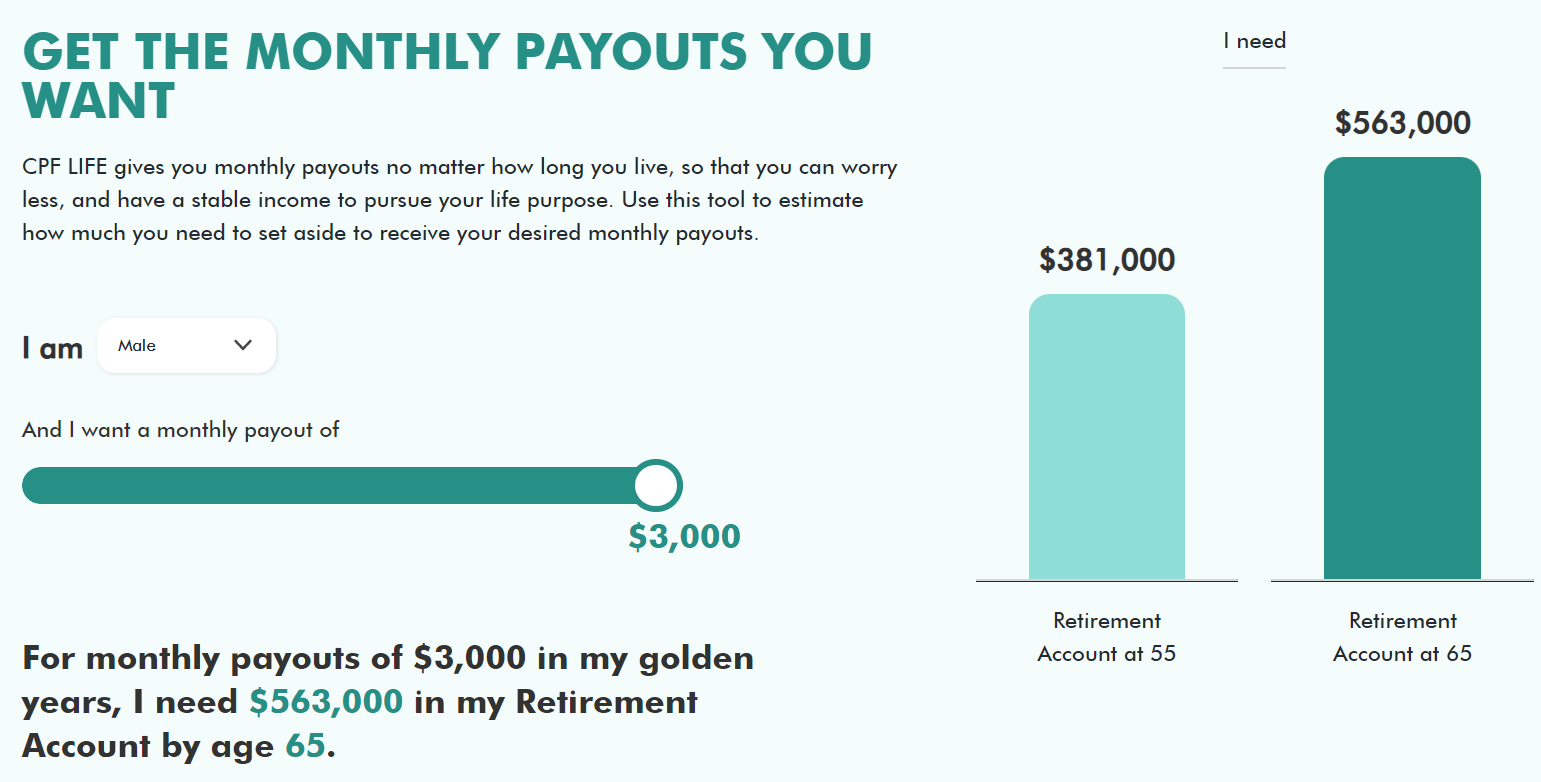

Play around with the Be Ready with CPF calculator to figure out how much you need in your retirement account.

With some strategic planning, know that you can live a comfortable retirement if you manage your expenses, invest well and plan ahead.