Debrief on Astrea IV Bonds

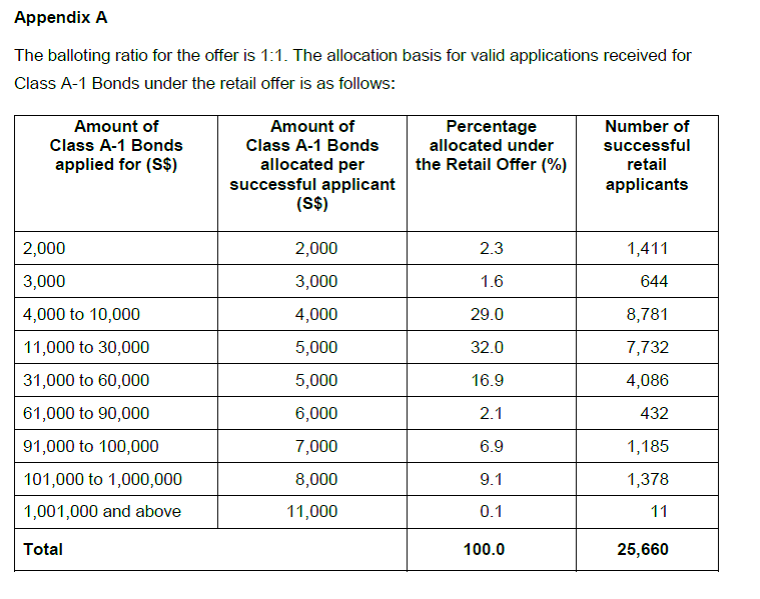

For those who are not aware, the retail offering of the S$121 million Class A-1 Bonds was 7.4 times oversubscribed. The allotment table is set out below:

To be very honest, this take-up wasn’t as strong as I expected. I applied for S$10,000 and received S$4,000, which is actually pretty decent. It’s strange because literally everyone I knew applied for these things, which leads me to think that my social circle is not entirely representative of the retail investors as a whole.

Perhaps it was the entire Hyflux saga that deterred the rest of the crowd.

In any case, I am glad that investors have considered the bonds, and not rushed out to subscribe simply because it is a “Temasek” bond. It is never a bad thing when you understand an investment, and after critical analysis, decide that you are not comfortable taking on the risk. There are no sure things in investing, and if you feel that the risk-reward does not fit your financial objectives, you should never be forced into an investment regardless of what someone else may say.

While we are on this topic, one commenter left a very well thought out rebuttal to my previous article on Astrea IV Bonds. I felt it was worth replicating in full here. As always, I will share my thoughts after.

Comment from reader

I think the risk from point 3 [Underlying assets are opaque and toxic] and 6 [Rising Interest Rate environment will affect bond prices] is quite understated.

Firstly, by buying Astrea IV bonds, you are financially leveraged twice. Not only are you exposed to Azalea’s 50% LTV, you’re also exposed to the 70-80% LTV these funds typically invest at. So your actual effective LTV is much higher.

Secondly, the fund that is investing in these PE firms are doing so at a time when valuations are at an all time high. Meaning that if there is some modest downward revision of multiples, Azalea’s equity in the funds can be easily wiped out. The saving grace is that there may still be ample cash flows to support interest payments. However, come redemption time, you might run into a brick wall if the market has not recovered.

Thirdly, a rising interest rate environment would impact these fund’s ability to refinance debt. So pray hard that the bull market continues because a downward revaluation and an increase in interest rates spell for a bad time.

To the comment in the article about buying an ETF instead. If the market heads south, I highly doubt your extremely leveraged instruments would fair well if the broader equity market collapses (remember, your principal depends on cashing out of the funds which in turn depend on them exiting their investments).

The final point regarding all bond investing cannot be overstated enough. The test of the quality of a bond is during a crisis, not during a bull market. As the global bond market is entering a bear market just as the same time that the PE market is in the midst of one of its greatest bull markets, you cannot underestimate the refinancing risk these PE boys face.

Financial Horse Response (interposed in the response)

I think the risk from point 3 [Underlying assets are opaque and toxic] and 6 [Rising Interest Rate environment will affect bond prices] is quite understated.

Firstly, by buying Astrea IV bonds, you are financially leveraged twice. Not only are you exposed to Azalea’s 50% LTV, you’re also exposed to the 70-80% LTV these funds typically invest at. So your actual effective LTV is much higher.

Financial Horse: Agreed. I do acknowledge that it’s not entirely clear what the underlying assets are. Given how leveraged PE Funds are, it is highly likely that effective gearing is much higher.

Secondly, the fund that is investing in these PE firms are doing so at a time when valuations are at an all time high. Meaning that if there is some modest downward revision of multiples, Azalea’s equity in the funds can be easily wiped out. The saving grace is that there may still be ample cash flows to support interest payments. However, come redemption time, you might run into a brick wall if the market has not recovered.

Financial Horse: Let’s go back to the structuring of Astrea IV. Under the priority of payments, a portion of the cash flow, after payment of expenses, will be routed into a reserve account and kept there for redemption of bonds upon maturity. The way it is set up, after 2 to 3 years of “business as usual”, there should theoretically be sufficient funds built up in the reserve account to redeem the bonds after the 5 year soft maturity date. Once this happens, Class A-1 bondholders are “risk-off” and it doesn’t really matter if PE assets nose-dive after that point.

Another point is that Class A-1 bondholders have first priority in repayment. With the S$200 million bonds on a S$1 billion portfolio, it would require something to the tune of an 80% impairment in value for Class A-1 to suffer losses (leaving aside the cash reserve). Given that Astrea is quite well diversified across PE Funds, this 80% impairment would imply that there has been a complete destruction of PE as an asset class. It’s not impossible definitely, but when you pair this with the fact that this has to happen in the next 2 to 3 years, and the fact that there is also a DBS loan as a safeguard, my opinion is that holistically the risks are low.

Thirdly, a rising interest rate environment would impact these fund’s ability to refinance debt. So pray hard that the bull market continues because a downward revaluation and an increase in interest rates spell for a bad time.

Financial Horse: Continuing on the previous point, Class A-1 bondholders only need the bull market to continue for another 2 to 3 years, after which we are risk-off.

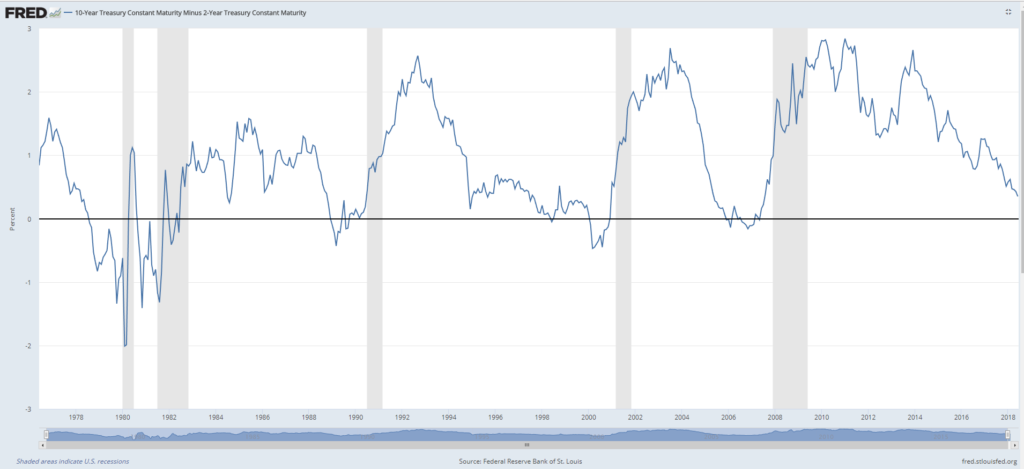

The US Treasury 2s10s yield curve has inverted before every recession in recent history, with about a 12 to 18 month lead-time to the next recession. The yield curve has not inverted yet, giving us some indication that that there is at least 12 to 18 months more to run on the current economic cycle.

I can’t rule out the fact that rising interest rates won’t affect PE Fund performance even before the next recession. So let’s examine what would happen in such a scenario.

Starting with the worst case, let’s assume that rising interest rates affect PE Funds, and there is a recession after year 2 that causes the PE Funds to go insolvent. Apart from the “I told you so” from my readers, my next best bet is to hope that (1) the cash reserves built up, (2) the remaining assets that did not go insolvent, and (3) the DBS bank loan, are sufficient to generate the S$200 million required to redeem the bonds after year 10 (this is the absolute worst case scenario, so hoping to get repaid after year 5 is a bit optimistic).

As long as the underlying assets don’t go insolvent completely, then there is between year 2 to year 10 to hope that eventually these assets pick up to the point where they generate sufficient cash or can be sold to generate sufficient cash reserves to repay the bonds.

10 years is a really long time. If these S$1 billion in PE assets cannot generate sufficient cash over 10 years to repay S$200 million worth of debt, that signifies a complete destruction of the PE asset class, that would have had disastrous effects on global asset prices. I would be more worried about my job than a paltry S$4,000 in bonds at that stage. And don’t forget, Temasek is the “equity holder”, so if these bonds were to default, it would mean that Temasek, the Class B bondholders, and Class A-2 bonder holders have been completely wiped out. Before you get too happy about that, don’t forget that Temasek is our sovereign wealth fund, so their loss is Singapore’s loss.

To the comment in the article about buying an ETF instead. If the market heads south, I highly doubt your extremely leveraged instruments would fair well if the broader equity market collapses (remember, your principal depends on cashing out of the funds which in turn depend on them exiting their investments).

Financial Horse: Again, the key here is timing. As long as the market doesn’t head south in the next 2 to 3 years, I should be risk-off by then. And to be 100% clear, my principal depends on there being sufficient cash in the reserve accounts to repay principal. So where PE asset prices are in 5 years or 10 years is immaterial, because the only thing that matters is whether they have generated sufficient cash in the reserve accounts to repay the bonds by that time.

The question to me is whether the risk adjusted returns with these bonds is higher than that on a stock ETF. My answer is yes, but as always, feel free to disagree.

The final point regarding all bond investing cannot be overstated enough. The test of the quality of a bond is during a crisis, not during a bull market. As the global bond market is entering a bear market just as the same time that the PE market is in the midst of one of its greatest bull markets, you cannot underestimate the refinancing risk these PE boys face.

Financial Horse: Okay, noted. To be clear, I have no intention of exiting my Astrea IV Bonds any time before redemption. So it doesn’t really matter how the bonds trade on the open market, because my sole concern will be default risk on the bonds.

Investing is about weighing risk and reward, versus other alternatives. Let’s say I don’t invest the S$4,000 in these bonds. Where would I put my money instead? I already have REITs, Singapore shares, US shares, Singapore property, CPF, and a cash buffer. I’m not entirely comfortable going all in on any of those asset classes given the current stage of the economic cycle. But to go all-in on cash isn’t wise either, because I could well be wrong and miss out on a huge rally over the next few years.

To me, these bonds offer an attractive risk-reward proposition, when compared against the other alternatives available. They are also decent from a portfolio diversification basis. And I have invested accordingly on that basis.

But I am an anonymous blogger who writes under an animal based screen name. What could I possibly know about investing?

On a separate note, the US Federal Reserve just raised interest rates by 0.25% this week, and projected another 2 rate hikes for the year. At the same time, the ECB announced that QE bond buying will halve to €15bn from €30bn per month from September 2018, end in December 2018, and interest rates will start going up in 2019. It sure looks like the end of easy central bank monetary policy is here. I actually wanted to share my thoughts on this, but I am a little out of time here. I’ll share my thoughts in next week’s “The Weekly Horse”, as that gives me a bit more time to mull over this.

Long Weekend Giveaway

Financial Horse is doing a giveaway for the Hari Raya Long Weekend! I have 3 tickets to Seedly’s Exclusive Meetup: Coffee Meets Investing to giveaway (normal price is S$30 per ticket).

The rules are simple:

- Like the Financial Horse Facebook Page or join the Facebook Group

- Comment on the Facebook post on 1 stock, ETF or investment platform that you want Financial Horse to review (Hint: I will write an article on the winning stock).

Note: There is 1 thread on the Facebook Page and another on the Facebook Group, so feel free to use either.

The comments that receive the most likes (or that I like the most) will win the tickets. The winners will get to choose between either a pair or a single ticket. Competition closes on Monday, 18th June!

Top Weekly Links

All Financial Horse does in his free time during the week is read financial news. With this new initiative (“The Weekly Horse”), hopefully some good can come out of it. During the week, I post articles that I enjoyed on the Facebook Group (do join if you want a sneak peak), and every Sunday I will collate the links for readers. I also take the opportunity to address queries from readers, or share any thoughts that I have for the week. If you enjoyed this post, do share your thoughts in the comments below!

http://awealthofcommonsense.com/2018/06/6-things-i-learned-from-big-mistakes/

Really enjoyed this piece by Ben Carlson.

Many first time investors focus on learning what they should do in investing. Perhaps a better approach is to first learn what you should not do.

Nice Bloomberg article on the factors that matter the most in determining portfolio performance. Picking the right stocks (No. 1) can be hard to get right, but costs and expenses (No. 2) and asset allocation (No. 3) are well within our control.

It is important to focus on controlling the factors we can control, and not lose sleep over events that are beyond our control.

http://www.morningstar.com/articles/869368/what-computer-chess-suggests-about-investing.html

Happy long weekend everyone!

A lighter article for today, which explores the impact computers had on human chess players, and extrapolating that towards artificial intelligence market players.

http://awealthofcommonsense.com/2018/06/useless-hacks/

Another great post by Ben Carlson. It’s always fun to read about “hacks” that help you get good at something. But sometimes, there’s really no shortcut to putting in the hours and hard work.

https://ofdollarsanddata.com/it-can-happen-to-anyone-1fc18db4396e

What would you do if you won 300 million dollars tomorrow? Do you think you can avoid the same fate as Jack Whittaker?

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Haha, from the multi-layered safeguards for class A-1 bondholders, can sense that the powers that be are really mollycoddling the mom & pop investors.

I mean come on, just the liquidity / loan facility from day 1 can cover 93% of class A-1?!? And this on top of LTV of a kiasu 16.5% for A-1?

All those safeguards cost money, whether upfront fees, ongoing fees, or opportunity costs.

If I’m Azalea, without overarching directions from the powers that be, I’d rather forget about retail investors … it would be cheaper, less headache & reap greater profits for me … not to mention more clearcut justification for nice bonus and promotion, hahaha.

Well, looks like Fed is now on a pace of rate increase every quarter … trying to get above 3% while the US economy can still take the heat?

Coz from studies, it seems Fed needs to be able to cut rates by at least 3% during recessions to make a difference.

Not forgetting that Fed is also reducing its US$4+ trillion balance sheet. It has reduced by US$150B since Oct 2017, and will stabilize at US$50B per month reduction from Oct 2018 onwards.

The 2s10s spread currently at 37bps is the flattest since 2007. No wonder so many are looking at 2020 to be the next recession. Plenty of time for higher highs yet 🙂

Hahaha, that’s a great point.

I also feel that Astrea has overdone it with this one. They could probably have done away with a few layers of safeguards, gone to insti investors, and still filled their books many times over. But no matter, if Temasek wants to be generous, I am happy to oblige. 🙂

The interest rate hikes do worry me though. With the Fed going down this path, a recession will eventually hit. I do suspect we have about 1 – 3 years left on this cycle though (depending on how quick the hikes are, and how the other central banks respond). So agreed, there will be higher highs yet before the next crash.

Thanks for the responses. Both of your contentions are valid.

I applied for 20k and gotten 5k. One important point which both of you miss, is the emotional and political aspect. It is Ho Ching, CEO of Temasek and Wife of our PM that put her reputation on line when she said this bond is for pops and moms retirement that I decide to apply. See the political angle?

Yes, she could have done like what Sinkie said.

Ah yes, thanks for bringing up this point. I wanted to allude to that in my article, but without making it too obvious. *wink wink*

yes, remind me of another parallel. singtel shares in 1993. Singapore Citizens were able to purchase shares at a discounted price as part of the Singapore Government’s effort to share the nation’s wealth and to enlarge the base of share-owning Singaporeans. Well, singtel is still around and has done ok for quite awhile until recent year. but still, cant see them fail even as they go through tough times like now as believe many mom and pop investors still holding some shares…., unless the political environment change and they see their obligation differently.

To be fair, had you bought Singtel in 1993, you definitely would not have lost money after factoring in dividends. Interesting parallel though. I guess one potential safeguard is that these bonds are unlikely to last for more than 5 years (10 max).

Anyway Singtel is an interesting stock. I will probably look to do an article on it one of these days. 🙂