Criticism on the Astrea IV Bonds

Given the massive debate over Temasek’s 4.35% p.a. Astrea IV Class A-1 Secured Bonds that is raging on this island currently, I wanted to take the opportunity to address some common criticism against the bonds. These things have really polarized investor opinion, with criticism ranging from:

- Bondholder’s get PE exposure without the upside

- 4.35% returns is too low in this climate

- The underlying assets are convoluted and toxic

- These things are overhyped and complicated, a bad combination

- 4.35% is too good to be true

- The rising interest rate environment is bad for bond prices

- So hot, how to get?

Let’s go through them individually. Do note that this article assumes that you have at least a cursory understanding of the Astrea IV Bonds. If you haven’t, you really should read my previous article that analyses the Astrea IV Bonds.

Bondholders get PE exposure without the upside

This criticism will argue that bondholders are getting exposure to the private equity (PE), but enjoy none of the upside. The allegation is that if the PE Funds do well, Temasek (as equity holder) enjoys all the upside, but if the PE Funds default, it is the bondholders who are left holding the bag.

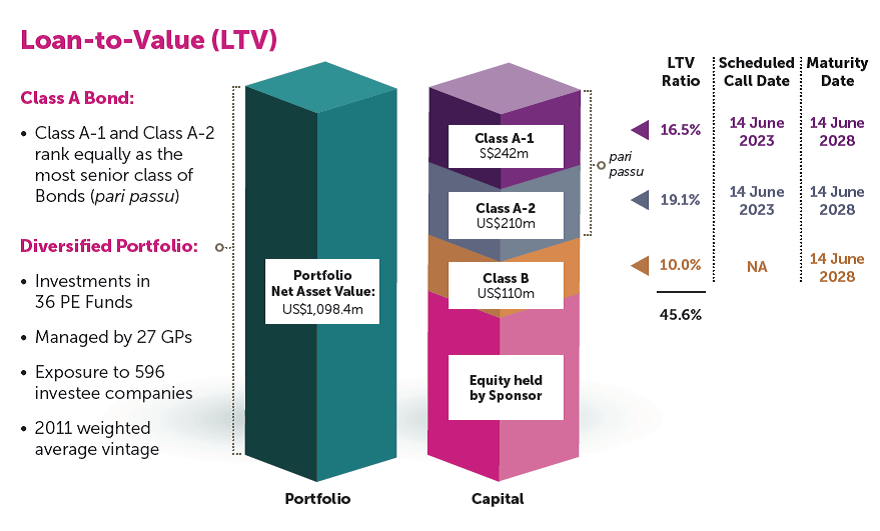

This criticism is not entirely accurate. Looking at the way Temasek sliced up the different tranches of Astrea, Retail Investors only hold Class A-1, which is the top 16.5% of the portfolio. The way to see it, if we were to look at the chart below, is that any gains or losses will grow the pink portion at the bottom (which is held by the equity holder, ie. Temasek). If the PE Funds do well, Temasek enjoys the upside. If the PE Funds suffer losses, Temasek loses. So yes, bondholders are being exposed to PE Funds, but the amount of risk they are taking on is far less than that of the equity-holders, and the Class B bondholders (both will need to be wiped out completely before retail investors suffer losses). And this is reflected in the potential returns.

On the lack of upside point, don’t forget that these are debt instruments, not equity products. Debt instruments by their very nature cap the upside to payment of interest (and repayment of principal). There is a small 0.5% additional payment if certain performance targets are met by year 5, but that’s about it.

One way to see it is this. Imagine you are a business owner taking a fixed rate corporate loan from the bank. The bank complains that if your business does well, they only earn the interest, and if your business fails, they take on all the risk. What would your response be?

For me, I would politely tell them (after some profanities) that they cannot have their cake and eat it. Either they take the benefits that comes with being a secured lender, or they become an equity holder in the company and participate in the upside (and downside) of the company. Risk and reward go hand in hand, and if you want exposure to the equity tranche, you are taking on significantly more risk.

Note: Okay I understand there are convertible securities, but valuing those are far more complex, and they are not common in the Singapore market.

4.35% returns is too low

The next criticism goes along the lines of “4.35% returns are too low, if I buy a diversified stock ETF, I will get 8% to 9% a year”.

While that may be true, it fails to take into account risk-adjusted returns. There’s no free lunch in investing, and to achieve greater returns, you have to take greater risk. The S&P500 ETF you buy may achieve an 8% CAGR for the next 5 years, but it could also suffer a catastrophic 50% loss in year 3.

As discussed in yesterday’s article, my personal view is that the default risk of these bonds is exceedingly low, and I think that retail investors are taking on less risk on these bonds than in the stock market.

Also, don’t forget that these bonds are great from a portfolio diversification perspective. After a certain point, I am wary of putting too much money into the equity/REIT markets given that we have had a 10 year bull run, and the Fed hell bent on raising interest rates. These bonds are a nice alternative to diversify my portfolio.

There is a more sophisticated variant of this argument that argues that the spread on Astrea IV is too low compared to Astrea III. Fund Supermart summarises this point well:

The ASTLC 3.900% 08Jul2019 Corp (SGD) – Class A-1 notes were issued at a spread of 218bps above the three-year SGD swap offer rate in 2016. Having considered the factors in the preceding paragraphs, we think the Astrea IV Class A-1s’ 4.35% price is less attractive than its predecessor. The pricing offers a spread of 200bps over the five-year SGD SOR.

Coincidentally, they also go on to address their own concern, which I agree with.

Nevertheless, the 4.35% coupon rate compares favorably to the broader SGD corporate bond space. As a reference, the NAB 4.150% 19May2028 Corp (SGD) is trading at yield to worst (ask) of 3.511%, indicating a spread of 125bps above swaps. The NAB 4.15% ‘28s are also maturing in ten years (May 2028) with a five-year callable date (May 2023). It is rated Baa1, BBB, and A+ by Moody’s, S&P, and Fitch.

As retail investors, we have to accept products as we see them, and our only decision point is whether to walk away. On balance, these bonds are still attractive when compared to competing debt instruments available on the market.

Underlying assets are opaque and toxic

This argument alleges that the underlying assets are 36 PE Funds investing in 596 investee companies. There is no clarity on the financial performance of the investee companies, both historically and going forward. The fact that it is diversified across 36 PE Funds does not change the fact that they are PE Funds with what is likely to be a high correlation in prices. As illustrated during the subprime mortgage crisis, once things start going bad, they go bad all at once, and illiquidity in asset classes can make an ultra safe “AAA” rated investment can look very risky overnight.

Actually, this is the argument I am most inclined to agree with. In my original article, I also expressed the concern that that at the end of the day, I really didn’t know what companies I was investing in.

But I think that we need to view the bonds more holistically. The structural safeguards in play, being the initial LTV, the 50% maximum LTV covenant, the reserve accounts and sponsor sharing, all contribute to reducing default risk on the retail bonds. If all else fails, don’t forget the loan facility granted by DBS to Astrea, that can be tapped on to meet shortfalls in funding.

And finally, Ho Ching herself came out to tout these bonds as an option for retirement planning. Read into that what you will, but given the structural safeguards in place, I am inclined to agree with her.

Overhyped

This argument will go along the lines of “The bonds are too hot, and overhyped. Buying them is a recipe for disaster”.

This is the easiest argument on the list to deal with, simply because it doesn’t raise any substantive concerns. This is an IPO, and the number of people applying for it doesn’t affect the pricing of the bonds. While it affects the chances of me getting these bonds, it has zero impact on the attractiveness of the investment if I were to get them.

Being contrarian does not mean being different for the sake of being different. Just because a lot of people are doing something does not automatically make it wrong. It is important to understand an investment product and develop your own opinion.

4.35% is too good to be true

This argument alleges that 4.35% is too good to be true, and that something is wrong.

It’s a bit too vague of an argument to fully respond to, but I will concede that with June 2018 SSBs yielding 2.63% p.a. to hold to maturity, the 172 bps spread does give one an idea of the risk premium in play.

Where does this risk come from, and is the market properly pricing this risk? Without full price discovery in the open market (this is the process by which market forces are allowed to value an investment), there really is no way to know for certain. However, given the small retail float and what is likely to be a small allocation to each investor, the liquidity on the secondary markets may be poor and I suspect there will be large bid-ask spreads. This makes it even harder to have efficient price discovery.

There’s always an element of risk involved in every investment, short of buying government bonds or putting your cash in a bank. If you are not comfortable with this risk, there really is no obligation to buy this bond.

Rising Interest Rate environment will affect bond prices

This argument will read “Interest rates are going up. No point buying bonds now because the price will drop.”

There is some element of truth in this. Interest rates in the US are going up, and eventually it will spill over to SGD denominated debt. There is a possibility that bond prices may fall in the coming years. However, just because the prices fall on the open market does not mean one has to sell their bonds. If you hold these things to maturity and there is no default, you will get back your initial sum with a nice 4.35% return a year.

Personally I have no intention of selling these bonds before maturity. So the key question for me is whether I am comfortable with the 4.35% returns as compensation for the risk I am taking on. And to me, the answer is clear.

So hot, won’t get lah!

Just for kicks, I am going to address this last concern. To put it very simply, it is the thinking that: “These bonds so hot, confirm won’t get. Waste my S$2. Even if get, sure get so little, how to make money”.

And to that, my response is: “Wahlao eh, 2 dollars cannot even buy bak chor mee. Live a little lah!” And also: “Knn, give you too much you scared lose money, give you too little you also not happy, next time u join temasek and do okay?”.

Top Weekly Links

All Financial Horse does in his free time during the week is read financial news. With this new initiative (The Weekly Horse), hopefully some good can come out of it. During the week, I post articles that I enjoyed on the Facebook Group (do join if you want a sneak peak), and every Sunday I will collate the links for readers. I also take the opportunity to address queries from readers, or share any thoughts that I have for the week. If you enjoyed this post, do share your thoughts in the comments below!

The Growing Crisis in Modern Finance (Forbes.com)

It’s only Monday, but I already have a contender for article of the week.

Ever since I first started investing, the concept of technical analysis befuddled me. Reading historical chart patterns, and predicting future price movement from that, seemed nothing more than reading tea leaves. Yet countless investors out there will swear by this discipline.

Just like fengshui or any mystical art, it will never be possible to conclusively debunk technical analysis. But this article does a fantastic analysis, and is one that I believe all investors should read.

Note: It’s the end of the week, and this is still my article of the week. If you only read one article this week, it should be this.

The Big Read: No easy answers to HDB lease decay issue, but public mindset has to change first (TodayOnline.com)

Nice read on the perils (or opportunity) behind buying a HDB with a shorter remaining lease tenure.

Does Private Equity Deserve More Scrutiny? (awealthofcommonsense.com)

http://awealthofcommonsense.com/2018/06/does-private-equity-deserve-more-scrutiny/

With all the excitement surrounding “Temasek’s” PE Bonds, I enjoyed this measured take on the promises of private equity going forward.

There’s no free lunch in investing, and high returns mean that you are taking on greater risk.

Great Things Take Time: Why Focusing on the Long Term is More Important Than Ever (ofdollarsanddata.com)

https://ofdollarsanddata.com/great-things-take-time-7b509f4d5e03

Modern society is built around the concept of instant gratification. But most of the best things in life, career, family, hobbies, investing, require time, and cannot be rushed.

Sheep Logic (epsilontheory.com)

http://epsilontheory.com/sheep-logic/

It’s a long read (with some hyperbole), but if you can get through it, there is a powerful message here.

“How do we “see” a crowd in financial markets? Through the financial media outlets that are ubiquitous throughout every professional investment operation in the world — the Wall Street Journal, the Financial Times, CNBC, and Bloomberg. That’s it. These are the only four signal transmission and mediation channels that matter from a financial market Common Knowledge Game perspective because “everyone knows” that we all subscribe to these four channels. If a signal appears prominently in any one of these media outlets (and if it appears prominently in one, it becomes “news” and will appear in all), then every professional investor in the world automatically assumes that every other professional investor in the world heard the signal. So if Famous Investor X appears on CNBC and says that the latest Fed announcement is a great and wonderful thing for equity markets, then the market will go up. It won’t go up because investors agree with Famous Investor X’s assessment of the merits of the Fed announcement. The market will go up because every investor will believe that every other investor heard what Famous Investor X said, and every investor will be forced to update his or her estimation of what every other investor estimates the market will do. It doesn’t matter what the Truth with a capital T is about the Fed. It doesn’t matter what you think about the Fed. It doesn’t matter what everyone thinks about the Fed. What matters is what everyone thinks that everyone thinks about the Fed. That’s how sheep logic, aka the Common Knowledge Game, works in markets.”

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

if Azalea issues an Astrea V one year later, what do you think?

Well, I would evaluate Astrea V on the merits of Astrea V. If it is structured as an attractive investment, I would still invest with them.

Leong Sze Hian

10 hrs

Today”s Sunday Times one full page on Temasek’s first retail bond offering – never say clearly what is arguably, the greatest risk – like what happened to private equity in the last 2008/09 financial crisis. 4.35% annual yield (5.35% from the 6th year) to retail investors mature after 5 or 10 years they get back their capital, but if the markets crash – the retail investors bear the risk, any upside all goes to the issuer! This may go down in the annals of financial history as the most unique “use” of ordinary citizens’ savings!

SHOULD RETAIL INVESTORS INVEST IN THESE BONDS?

Considering the risk in private equity, the yield of 4.35% on the Class A1 bonds is not attractive.

The structure of this bond reminds me of the collaterized debt obligations (CDOs) that were launched prior to the Global Financial Crisis in 2008. They were also structured into different layers. During the crisis, all the different layers were affected and suffered large losses.

POTENTIAL RISKS

Briefly, the risks are:

•Fluctuating interest rates may affect the bond price

•Uncertainty on cash flows

•Adverse market conditions could impact distributions

•Limited trading market

•Illiquidity of private equity investments and reliance on key private equity professionals

•Limited disclosures from underlying private equity funds

HOW SHOULD YOU INVEST YOUR SAVINGS

You can put your money into the special account in the Central Provident Fund and earn a guaranteed 4% per annum.

If you wish to have a higher return and are willing to take the risk, you can invest in the index fund of blue chip shares, i.e. the STI exchange traded fund. If you invest for the long term, you can ride out the fluctuations in the market and get an attractive return. The average return over the past 20 years is 9% per annum (or maybe slightly lower).

Tan Kin Lian

Hi,

Regarding the interest rate arguement, would it make sense then to wait for the bond price to drop and buy from open market which will also give you high yield?

There are no guarantees that will work, because I expect liquidity on the secondary markets to be thin. It really can go either way in such thin liquidity conditions.

thanks, great sharing!

Another feedback for you.

Your positiveness might rub on to retail mom and pop who needs Return of Capital more than Return of Investment.

You might be able to withstand the capital loss, but they might not and will put them in hardship.

When structured bond(this is not even a plain vanilla bond) are targetted at retail mom and pops , selling them a higher interest rate and you use “Names” not facts to backstop your argument on it being safe, you are not doing the mom and pops who read this a service.

Hyflux was a overleveraged company and people who enticed into the high yield bond because Hyflux is well known and CEO is the founder blah blah blah and people compare the yield to a fixed deposit..

that’s when they lost the plot.

A bond yield should be compared to a bond yield.

A structured bond yield should be compared to a structured bond yield.

And then you decide whether the trade off of just buying a straight bond is better than buying a structured bond.

for 4-5%, you could get straight bonds from well-established foreign companies.

However, that is not available for the retail investors, that is why they are so enamoured by the ordinary yield in such a complex product with so many layers of intermediaries.

Another feedback..

“Retail investors who want to diversify and try their hand in private equity can now do so via the newly launched Astrea IV private equity bonds.”.

It looks enticing to the retail investors to get something so “Exclusive” – the private equity.

But hey, you are not getting your hands into private equity.

You are BUYING A structured BOND.

To be clear, when you are getting your hands in private equity, it usually means getting into the equity part of the private equity component.

I am sure you don’t consider someone buying bond of hyflux to be trying their hands in water treatment sector. They are getting a bond, not getting the equity exposure of the water treatment sector.

Thanks for sharing your thoughts Sir. 🙂

Thank you for a great review and analysis. I also think that since Temasek has deemed this good enough for the public mom and pop to invest their retirement funds, it is also their responsibility if anything untoward should happen.

So in the same vein, you as a reviewer, should not be held responsible for any of their potential losses after your disclaimers. Caveat Emptor mah…

I think the risk from point 3 and 6 is quite understated.

Firstly, by buying Astrea IV bonds, you are financially leveraged twice. Not only are you exposed to Azalea’s 50% LTV, you’re also exposed to the 70-80% LTV these funds typically invest at. So your actual effective LTV is much higher.

Secondly, the fund that is investing in these PE firms are doing so at a time when valuations are at an all time high. Meaning that if there is some modest downward revision of multiples, Azalea’s equity in the funds can be easily wiped out. The saving grace is that there may still be ample cash flows to support interest payments. However, come redemption time, you might run into a brick wall if the market has not recovered.

Thirdly, a rising interest rate environment would impact these fund’s ability to refinance debt. So pray hard that the bull market continues because a downward revaluation and an increase in interest rates spell for a bad time.

To the comment in the article about buying an ETF instead. If the market heads south, I highly doubt your extremely leveraged instruments would fair well if the broader equity market collapses (remember, your principal depends on cashing out of the funds which in turn depend on them exiting their investments).

The final point regarding all bond investing cannot be overstated enough. The test of the quality of a bond is during a crisis, not during a bull market. As the global bond market is entering a bear market just as the same time that the PE market is in the midst of one of its greatest bull markets, you cannot underestimate the refinancing risk these PE boys face.

Hi David,

Thanks, that’s a very well thought out and articulated rebuttal.

I take your point, esp on the quality of the underlying investments. Where I disagree though, is on the default risk, as I believe the structural safeguards should offset the risk, assuming there is no crisis in the next 1 to 2 years.

Very good arguments though, and thanks again for sharing. I’ll mull over them a bit more, and share some further thoughts during my weekly sharing post.

Cheers.