Unless you’ve been living under a rock the past week, you’ve probably heard of Temasek’s 4.35% p.a. Astrea IV Class A-1 Secured Bonds. In fact, the 4 June Business Times article carried this headline: “Investors can invest in Temasek’s first retail bond to boost retirement income: Ho Ching”. With headlines such as this, my expectations were sky high when reviewing this bond.

Before we dive into the details, do note that these bonds are incredibly complicated asset backed securities. While I have tried to simplify this as best as I can, there will inevitably be certain aspects that I cannot cover in this article. If you want to fully understand your risk and liability, there is no substitute for reading the prospectus.

Basics: What are the Astrea Bonds?

Fund Supermart has a great 2-part article that gives a factual summary of the Astrea Bonds. It’s a bit technical though, so let me try my hand at it.

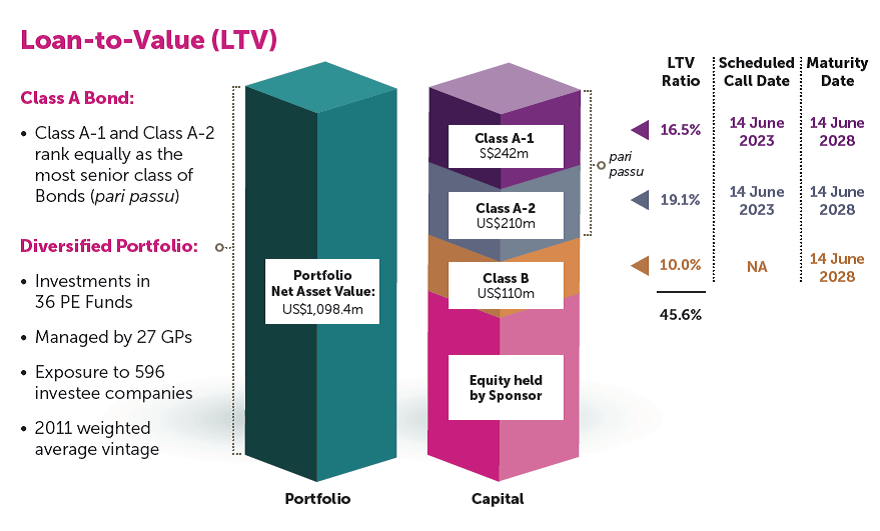

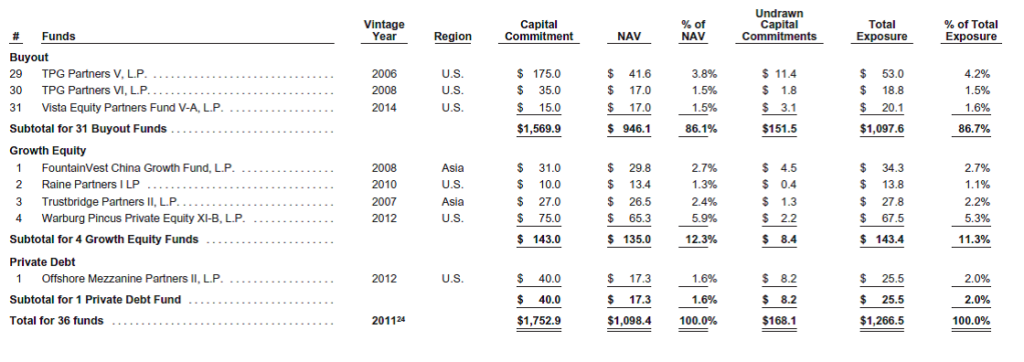

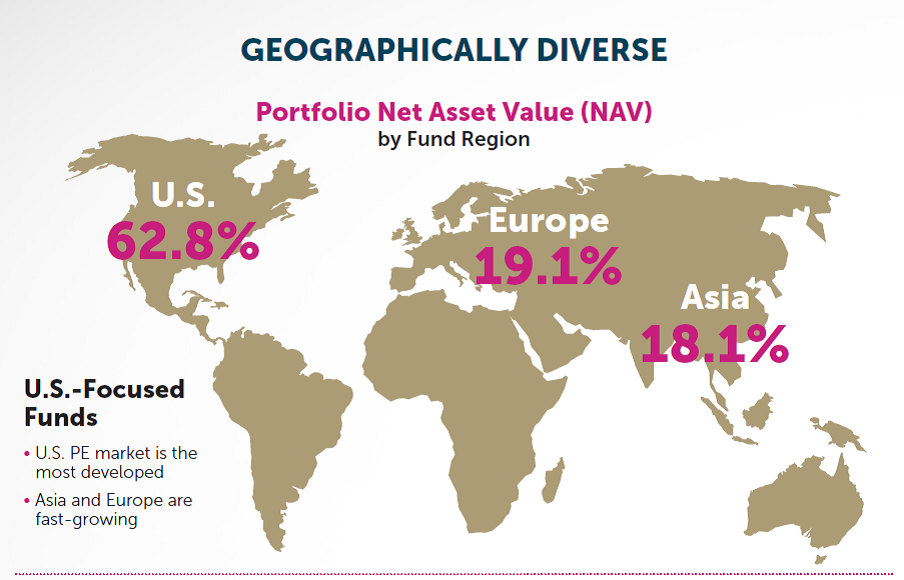

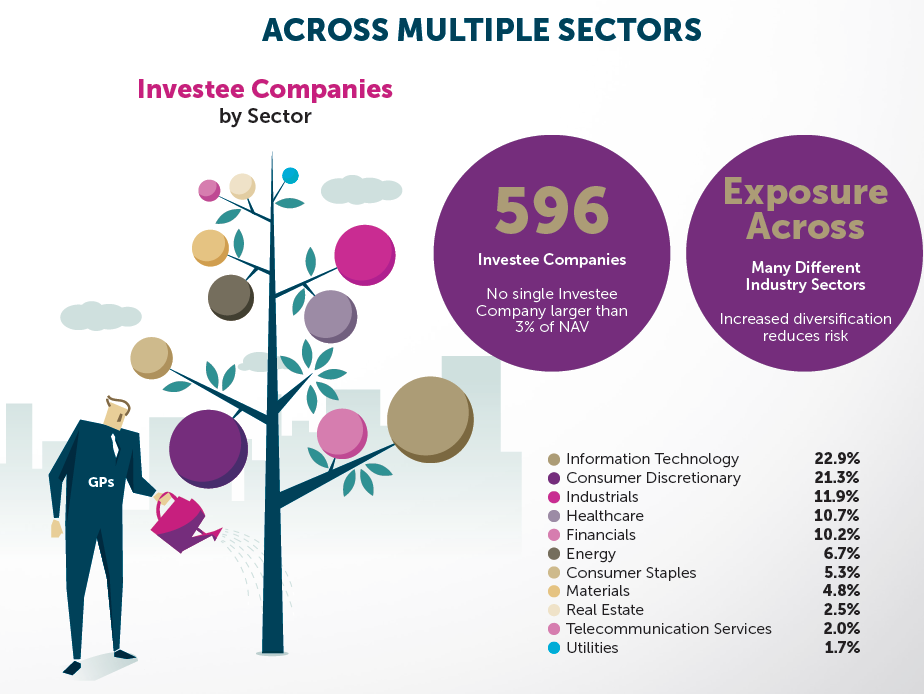

Astrea IV Pte. Ltd. (“Astrea”, this is the issuer you are buying the bonds from) is an indirect wholly owned subsidiary of Temasek. As at listing date, Astrea will hold 36 different investments in various private equity (PE) funds with a total net asset value (NAV) of S$1,098.4 million as of 31 March 2018. These PE funds are diversified across regions, sectors, and PE strategies, and cover a total of 596 underlying investee companies.

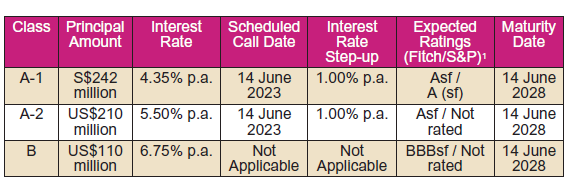

The Astrea Bonds being sold to the public, are asset backed securities (ABS) secured against the cash flows and asset value of the underlying investments in the PE Funds. The portion being sold to retail investors is half (S$121 million) of the class A-1 portion below.

To illustrate this very simply, imagine that Astrea owns a “house” that is worth US$1.1 billion. It wants to mortgage the house to borrow US$500 million. Within this US$500 million, it splits the borrowings into a Class A loan for US$400 million and a Class B loan for US$100 million. Class A has priority over Class B in the event of insolvency, so it is a safer investment. Accordingly, Bank A, that provides the Class A loan, is entitled to a lower interest rate than Bank B, that provides the Class B Loan. In this example, retail investors are given the chance to become Bank A, and “loan” Astrea money. It’s a bit of a simplistic explanation, but swap the “house” out for 36 PE Funds, and you get the rough idea of what these bonds are.

Default Risk

To be 100% clear, Temasek is not guaranteeing this bond. I cannot stress this enough. If the underlying assets are impaired and the retail bonds are affected, Temasek (or taxpayers) will not be stepping in to ensure that your bonds don’t go bust.

How then, do we determine the risk of default? Again, these asset backed securities are really complicated stuff, but broadly, there are 2 key elements to look at.

Underlying Assets

The first is to examine the underlying assets that the bonds are secured against. To use the house analogy, this would be examining the house to ensure that it is actually a house, and that it has real value.

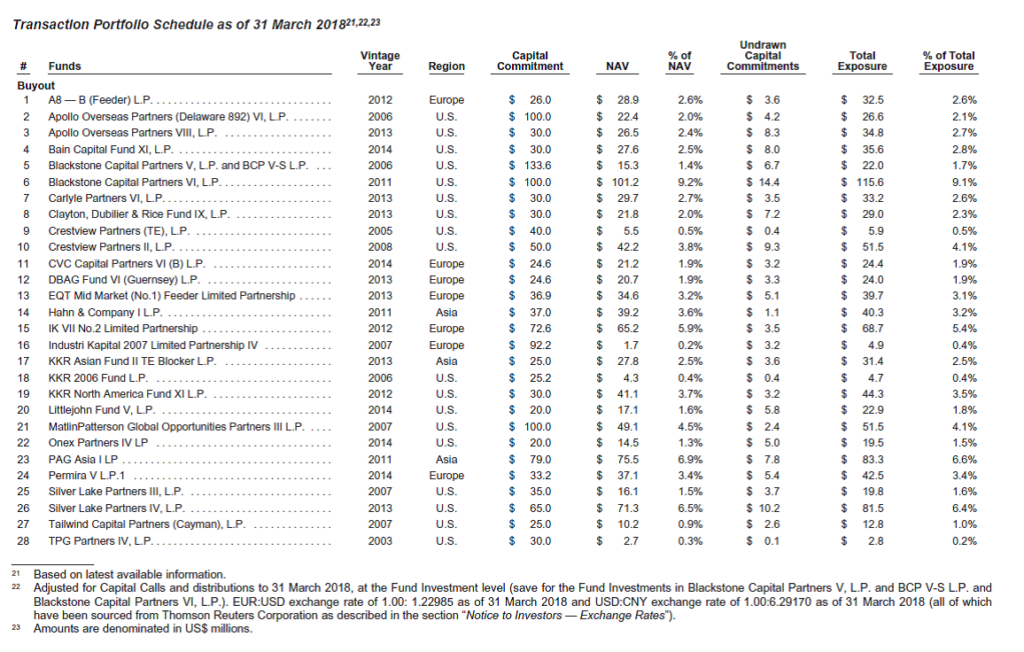

The underlying assets for Astrea, are 36 different PE funds, investing in 596 different companies. The 36 PE Funds are extracted below.

Unfortunately, the PE Funds are not publicly listed entities, so they have no obligation to report comprehensive financial data. Further, there is no easy way to dig up the financial information of the underlying companies that these PE Funds invest in (most of them are private companies that do not have to disclose financial information).

Even if we somehow managed to get access to the full list of underlying companies invested in, and the full financial results of the underlying companies, these will only be historical data. To determine the default risk for the bonds going forward, we will need to forecast the future cash flow and financial performance of these companies, which in many cases is an exercise in futility.

The saving grace, is that these assets are well diversified across industry groups, geography, and strategy, as you can see from the gatefold extracted below. The funds are also some of the biggest and most well respected names in the world, including Blackstone,Silverlake, Warburg Pincus, Apollo etc.

However there is no getting around the fact that at the end of the day, the performance of the underlying assets will require some guesswork.

The nature of the underlying assets makes me a bit uneasy, because I really do not know what goes into them. Where it gets more straightforward, is the structuring of the securitization. To use the house analogy, this would be how the bank sets up the mortgage.

Structuring of the Bonds

The bonds are structured to minimize the chances of them going bust. There are 4 key characteristics that make this the case, let’s go through them individually:

Loan to Value (LTV) ratio of 45% – Astrea starts with a LTV of 45.6%. Very simply, this is the amount of debt Astrea is borrowing, against the value of its underlying assets (in REIT speak, it is gearing). A 45% LTV is great because this gives you essentially a 55% buffer to play with, before the bond holders start getting affected. And don’t forget, the Class B bonds will get affected before Class A.

Going back to the house example, you as the bank are lending money 400 million to Astrea against the mortgage. If the house halves in value, it is now worth 550 million, which is still more than the 400 million you have lent to them, so you can always sell the house and pay yourself back with the proceeds without suffering any loss. The only situation where you lose money is for the assets to lose about 70% of their original value. While this is not impossible, the chances of this happening are slim.

Maximum LTV Ratio of 50% – The next feature is a maximum LTV ratio of 50%, which means that Astrea cannot allow its debt ratio to cross 50%.

To build on the house analogy, this would mean that Astrea cannot borrow more than 50% of the valuation of the house, being 550 million. With their 45.6% starting LTV, they are pretty close to the limit, so they are unlikely to gear up further. What this also means, is that if the house falls in value such that their LTV crosses 50%, they will need to pay off debt (starting with the Class B Bonds), to bring down the LTV.

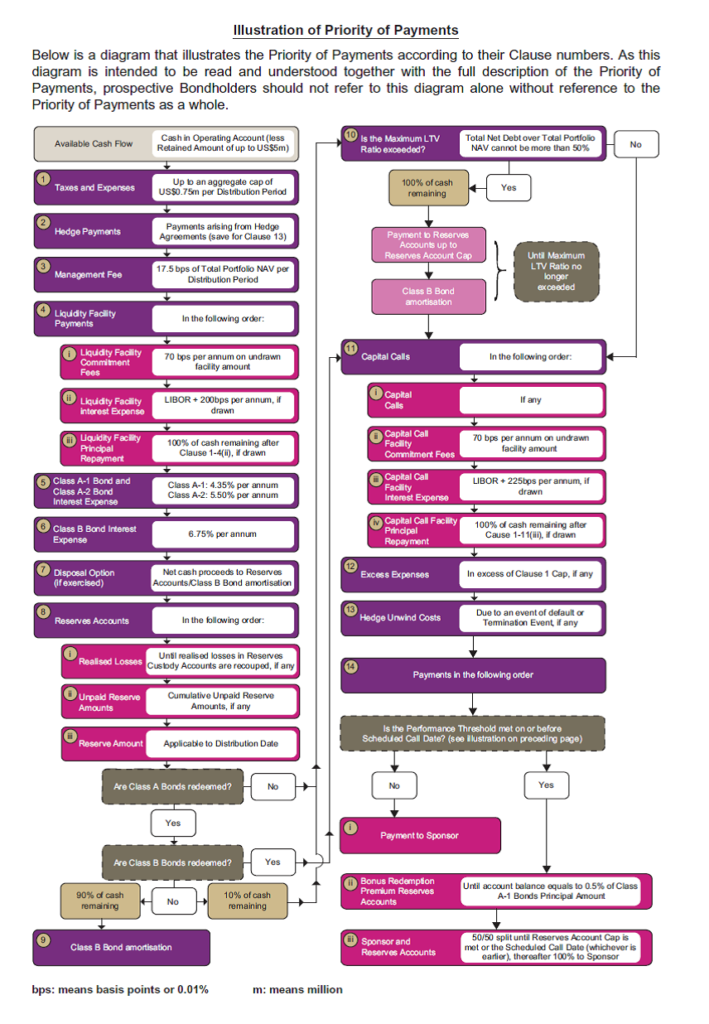

Reserve Deposits – All cash distributions that Astrea receives from its underlying investments, after deducting expenses and interest repayment to bondholders, will have a portion contributed into a reserve accounts to build up a cash buffer, that will be tapped on to redeem the bonds upon maturity. This creates a cash buffer that further reduces insolvency risk.

Using the house analogy, this would be a case where Astrea leases out the house, and a portion of the rental income, after paying expenses and interest repayments, is paid into a separate account that is locked away to repay that mortgage when it becomes due.

Of course, in reality the actual priority of payments is a bit more complicated than that (take a look at the diagram below for an illustration), but you get the idea.

Liquidity and Capital Call Facility – There is also a Liquidity Facility and Capital Call Facility granted by DBS bank to meet any shortfalls in expenses or interest repayment, or if there is insufficient cash to redeem the bonds.

To use the house analogy, this is akin to Astrea going out to a Bank C, and getting a separate loan facility. This loan can then be drawn upon if for some reason they didn’t have any money to repay their mortgage to Bank A or B. I don’t want to call this a DBS backstop, but it does look kinda like one.

Sponsor Sharing – There is also a sponsor sharing feature. I won’t go too heavily into the details, but simply, all excess cash does not go to Temasek entirely. 50% of it will go into a reserve account, to enable the faster build-up of reserves to redeem the bonds. It’s quite a nice touch by Temasek now that I think about it.

Hedging – As an added benefit, because the underlying assets are largely USD denominated, Astrea has also entered into fixed forward hedging arrangements to hedge against currency exposure (from receiving distributions in USD and having to pay interest in SGD).

The points above, in my view, drastically reduce the chance of a default on these bonds. For a default to occur, there would need to be a sharp drop in global asset prices, coupled with a freezing of global financial markets. Note that even a gradual drop is insufficient, because if there is a slow decline, the LTV covenant would be triggered forcing Astrea to repay debt. The only situations I can think of that can result in such a scenario would be a massive global financial crisis, a global pandemic, a nuclear war, you get the idea…

S&P models about a 1.6% chance of default on these bonds. I don’t know how they arrived at this number, but given the number of assumptions they would have had to make to arrive at this conclusion, I would caution against placing too much reliance on this.

At the end of the day, my personal view is that the risk of default on these bonds is exceedingly low. The underlying assets are some of the most well respected private equity names in the world. They are also well diversified across asset classes and geographically, and should generate sufficient cash flow going forward. The structural safeguards put in place by Temasek further contribute to the safety of these bonds.

Redemption

The Astrea bonds have a soft maturity date of 5 years (2023), and a hard maturity date of 10 years (2028). If Astrea has sufficient cash at the end of the 5 years, it will redeem the Class A bonds in full (if it hits certain performance targets, there is an additional 0.5% incentive payment). If it does not, it will not redeem the bonds, but the interest rate payable on the bonds will step up by 1%.

Whether they will be redeemed ultimately depends on the performance of the underlying PE funds, and whether they can generate sufficient returns. This is tricky because it is hard to model the performance of the PE funds going forward.

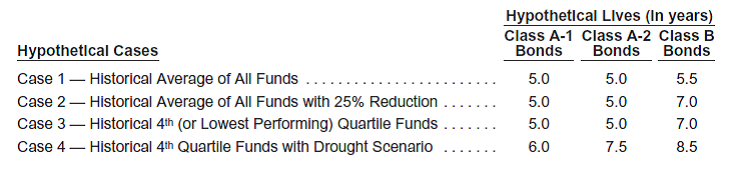

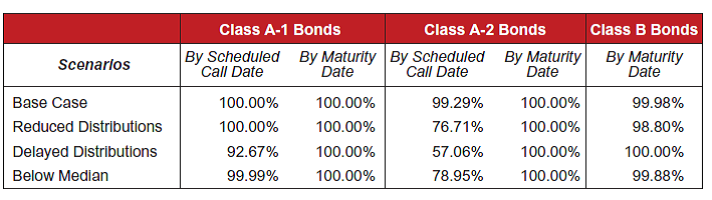

In the prospectus, Astrea models that in a worst case scenario, the Class A-1 retail bonds will be redeemed in the 6th year. The Independent Research Consultant (Bella Research Group) models that in their worst case scenario, there is a 99.99% chance of the bonds being repaid after 5 years, and a 100% chance of the bonds being repaid after 10 years. Extracts below if you don’t believe me.

As a rough gauge, looking at the Astrea III bonds, as at 31 Dec 2017 (around 1.5 years since issue in July 2016), they have received enough cash to cover their Class A1 bonds due in July 2019. So I guess the above modeling is not entirely without historical backing.

My personal opinion is that the bonds will be redeemed after 5 years. With the structural safeguards in place, there is a high likelihood that there will be sufficient cash built up to redeem the retail bonds fully after 3 years. The way I see it, default risk is almost non-existent, so even if the bonds are not redeemed, I get to enjoy to step-up interest rate, and it’s not the end of the world.

Yield

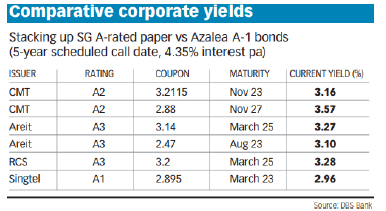

The business times has a nice table that compares the yields of other retail bonds. Surprisingly Astrea’s 4.35% p.a. far surpasses any of its comparison, given a largely similar credit rating. Granted, some of the benchmark bonds below were issued at a time when prevailing interest rates were lower, but that is still quite a huge rise. It looks like Temasek has “left some money on the table” here. They could probably have gone out to institutional investors entirely and filled their books 10 times over with this product, but they stuck with us retail investors. Massive kudos to them for doing so.

For reference only, the yield on a 10 year SSBs for June 2018 yield 2.63%. SSBs are a risk free investment, so the risk premium for these bonds is about 172 bps. A blue-chip REIT such as Mapletree Commercial Trust is yielding about 5.6%, but the risk of capital loss for a REIT is far higher.

Post Listing Liquidity

The Astrea IV bonds will be listed on the SGX-ST post listing, so technically you can sell them on the SGX. However, my suspicion is that the trading volumes will be quite thin, and the bid-ask spreads are going to be quite high. This means that you cannot exit your investment easily without taking a loss (I could be wrong though).

That said, you probably shouldn’t buy this bond unless you are prepared to hold it to maturity. These are not equity instruments that are designed to be traded.

How likely are you to get it?

The amount available to retail investors is a grand total of S$121 million. Based on my albeit anecdotal evidence, it seems like every Singaporean and their pet dog will be applying for these bonds. “Temasek” mah… right?

The allocation of bonds is entirely up to the issuer. I have a nagging suspicion that the allocation will be similar to what is being done for SSBs, that each person who applied will get a small amount. My suspicion (again I could be wrong), is that every investor will be getting 2 lots each.

Assuming each investors gets 2 lots, that means a total of 60,500 retail investors in Singapore will be allocated their magical Astrea IV bonds. That’s really not a lot of people.

What is the true purpose of these bonds?

I’ve been doing quite a bit of thinking about the role of these bonds. So I went back and reread the speech by Ho Ching. Extracted below, as reported by the Business Times

“So we worked very hard to kick-start the real estate investment trust (Reit). The idea of Reits is to democratise, unitise the possibility of investing in different kinds of assets in very small quantities, so the first Reit was to use shopping malls and convert them into Reits.”

“The reason why we did that was we said for the individual investors, the mom and pop investors and the young man or the old lady who wants to invests in the Reit of shopping malls… he or she can go to the shopping mall to see whether the shopping mall thrives, whether people are carrying shopping bags and so on,” said Ms Ho.

“As you know these funds are open and accessible to many of you but not necessarily to the broad masses.”

“But by creating a product which is diversified and therefore provides a better risk adjusted return for the individual, we can bring a new category of product to the market for the retail investor,” said Ms Ho.

“So quite apart from things like housing this is another way that we as an institution, …try to bring our skills and knowledge to create products in the future for those who want to invest for their retirement,” said Ms Ho.

I also read the comments from group CEO of the Azalea platform, Ms Margaret Lui-Chan, as reported by FundSupermart.

In our meeting with Azalea’s management team, Ms Lui-Chan advised us that the biggest risk in PE bonds comes from the unpredictable nature of the cash flows from private equity funds. Azalea seeks to mitigate that (and other risks) through over-collateralization and the structural safeguards of Astrea IV.As with any debt investment, the extent of leverage employed by the issuer is an important consideration. The more borrowings behind the same pool of assets, the riskier the structure is.

…

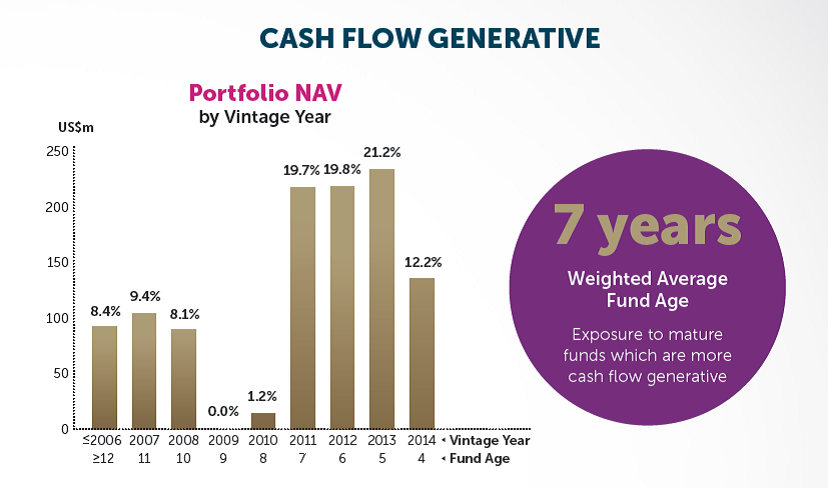

The transaction portfolio is also well-diversified across different vintages, with the weighted average age of each PE fund being seven years old. This increases the probability that the portfolio stays cash generative throughout the life of the transaction. The older funds help to stabilize near-term cash flows, while the younger funds are still in investment mode. Ms Lui-Chan said, “Cash flows from one fund can be unpredictable. But cash flows from 36 PE funds have significant reliability.”

And then it struck me. These bonds should not be viewed as a be all and end all in retirement planning. Rather, they should be viewed as the dawn of a new asset class for retail investors, much like CapitaLand Mall Trust (CMT) was, when it was the first REIT to be listed in Singapore back in 2001.

Let’s say you are Temasek, and you want retail investors to have access to asset backed securities to diversify their investment portfolio. How would you go about doing it? If it were me, I would give the public an ABS to introduce them to such products. However, this ABS would need to be structured such that it is as safe as it can possibly be, and yet offer attractive yields to entice investors to take it up. Sound familiar? This ABS would then have a dual purpose of (1) introducing retail investors to this new asset class, and (2) sending out a strong signal to the private sector that there is retail demand for such bonds.

If we take a step back and look at this more broadly, it is actually possible to construe the Singapore Savings Bond as the first product under this philosophy, and the “Temasek” retail bonds as its worthy successor.

Closing Thoughts

Investors really should not look at this as a sure-win investment. A 100% risk free investment is the Singapore Savings Bond, currently yielding 2.63% p.a. over 10 years (June 2017 bonds). This means the risk premium for these bonds is about 172 bps, which should give you some kind of indication of the kind of risk you are taking on.

However, holistically, my personal opinion is that the risk of a default is exceedingly low. Temasek has really gone out of their way to structure a safe investment for mom and pop investors like us. I truly think that they could have gone out to institutional investors all filled their books 10 times over with far less hassle.

From that perspective, I want these bonds to succeed. I want to send a strong signal to Temasek that we appreciate their efforts in making this product available to retail investors. I want to send a signal to the private sector and investment banks who are watching that retail investors will subscribe for products if they are safe and well structured. Too many instruments are designed solely for institutional investors these days. Someone please throw us retail investors a bone too.

This humble financial blogger will be subscribing for “Temasek’s” Astrea IV Bonds, (I’ll pop 10k on it, although I expect to receive none or at best 2 lots). There’s no such thing as a perfect financial investment. But from a risk-reward, portfolio diversification perspective, I think you’ll be hard pressed to find anything comparable on the market today. With this in mind, I will be giving this my very first perfect 5/5 Financial Horse rating.

Note: In Part II of this article, I also go on to address some common criticism on the Astrea IV Bonds.

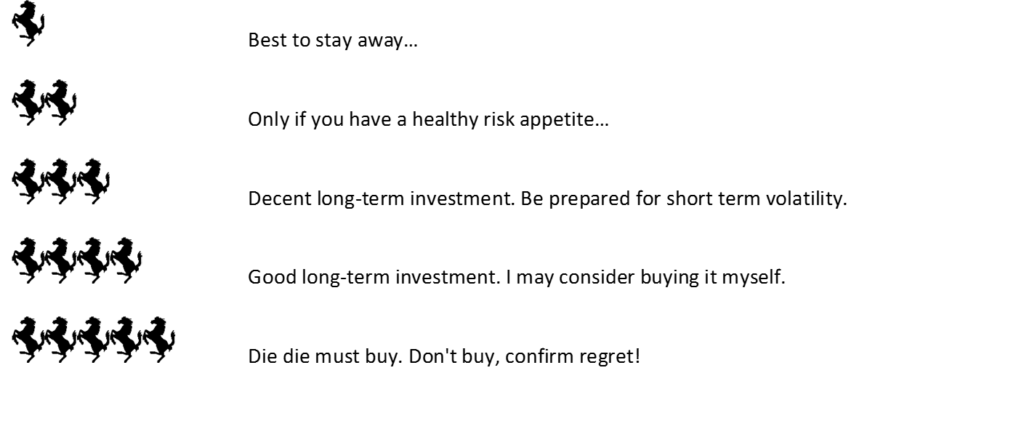

Astrea IV Class A-1 Secured Bonds – Financial Horse Rating

Note: Please don’t blindly follow my recommendation and rush into these bonds. These are yield products, so don’t expect their prices to “pop” on day one. I am buying in with the intention of holding these investments for 5 to 10 years, and the possibility of entire loss of capital. Investors should understand their own financial objectives.

Financial Horse Rating Scale

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Lehman bonds was structured as a CDO and it’s assurance then was the default risk was low as it is diversified across different categories of mortgage loans. We all know what happened then. Everything is fine and dandy until a crisis comes your way.

Even hedgefunds which promised absolute returns during the heydays freezed redemption. Some went bust and liquidated far below the NAV of the peak. So, you were forced to take a substantial haircut on your investment against your will.

A PE fund is no different, if you diversified into 36 PE funds, you are not really diversified as it is the same asset class and correlation would still be high. If a crisis do come, PE funds can choose to freeze redemption(best case) or to liquidate their holdings (worst case because you take significant haircut on the NAV of the fund).

Assuming a crisis come along, a $1bil AUM PE Fund of Funds took a haircut of $500million (due to funds liquidation). I am interested to know the realistic scenario of whether the equity holders will take the loss or would the company negotiate for bonds holders to take the loss? In real life, we have seen countless companies asking bond holders to take haircuts by converting into equity or to exchange the bonds for lower paying bonds or even total liquidation.

Imho, this is not a plain vanilla bond and the spread is too low to justify the risk. It is more about de-risking their PE portfolio than it is to fund your retirement.

Agreed with most of your points above. However I think the key difference is that these bonds are issued by an indirect wholly-owned subsidiary of Temasek. For them to go to retail bondholders and ask for a haircut is something that is frankly quite unlikely to me. Don’t forget DBS has granted Astrea a loan facility that can be drawn upon if there is insufficient funds.

Astrea 1 went through the GFC without any creditor having to take losses. The fact that Ho Ching came out to implicitly back these bonds (please don’t quote me on this) further supports this thinking.

If you’re referring to the Lehman minibonds fiasco, they weren’t actually low risk. In the notes, it is clear that if any one of the 10 entities in the list defaults, the investors loses everything. In a first to default scenario of 10 firms, it is a risk concentration not diversification despite what the pretty little salesppl said…

The main air bag is the reserve account mechanism, which aims to build up cash sufficient to redeem the A class bonds in 5 years.

In fact for the A-1 class bonds, Astrea just needs 5 semi-annual top-ups into the reserve account to fully fund redemption of both retail & institutional A-1 bondholders.

The 2nd big safety device is the overcollateralization of initial >2X and covenant of LTV not more than 50%.

Icing on the cake is the revenue sharing to accelerate the build up of reserve account.

Of course if Trump & Kim go for each other’s throats on June 12 then all bets are off!!

Spot on as always Sinkie! Don’t forget the loan facility granted by DBS, that can be drawn on to repay bondholders if all else fails.

Agreed though, if there is a global liquidity crisis within the next 1 or 2 years, these bonds could be in a lot of trouble. Once we cross the 2 to 3 year mark, there should be sufficient cash reserves built up such that default risk becomes inconsequential.

This is a mezz like instrument wrongly priced! How could mom and pops understand such a sophisticated product?

Haha what do you think the correct pricing should be? But I do agree that this is quite a sophisticated product, it did take me a while to really grasp the structuring.

Hi there, if class B is redeemed first when maximum LTV is breached, doesn’t this mean that in the case of falling net asset value of the underlying funds, class B will be redeemed prior to class A, leaving class A bondholders exposed to potential default?

Great question. The way it works is that under the priority of payments a certain amount will always be put into the Reserves account, to be used for redemption of Class A bondholders. The LTV covenant only kicks in after this step (ie. After paying the designated amount into the Reserves account, Astrea will check if the LTV has been exceeded. If it has, the remaining cash will be used to redeem Class B bonds to reduce the LTV. So Class A bondholders will still be safer than Class B.

Extract from page 108 of the Prospectus below:

“If the Maximum Loan-to-Value Ratio has been exceeded, payment of 100% of the cash flow remaining after application of Clause 1 through Clause 9 of the Priority of Payments to the Reserves Accounts (or, if and after the Reserves Accounts Cap is met (regardless of whether the Class A-1 Bonds or the Class A-2 Bonds have been redeemed), to the repayment of the outstanding principal amount of the Class B Bonds) until the Maximum Loan-to-Value Ratio is no longer exceeded.”

[…] was really excited by last year’s Temasek’s Astrea IV Bonds. In fact, since this site was created, the 2018 Astrea IV Bonds was the only investment to have […]

[…] was really excited by last year’s Temasek’s Astrea IV Bonds. In fact, since this site was created, the 2018 Astrea IV Bonds was the only investment to have […]

[…] was really excited by last year’s Temasek’s Astrea IV Bonds. In fact, since this site was created, the 2018 Astrea IV Bonds was the only investment to have […]

[…] Financial Horse: Temasek’s 4.35% p.a. Astrea Bonds: A free lunch in investing? […]