I’ve been getting quite a few questions on the best fixed deposit interest rates in Singapore right now.

A number of banks have slashed their fixed deposit rates lower the last few weeks, so an update was way overdue.

At the same time, I also wanted to address 3 key questions:

- Which is the best Fixed Deposit interest rates in Singapore right now?

- Will fixed deposit interest rates keep going down?

- Is Fixed Deposit a better buy than T-Bills / Singapore Savings Bonds / Money Market Funds for your cash?

Which is the best Fixed Deposit interest rates in Singapore right now?

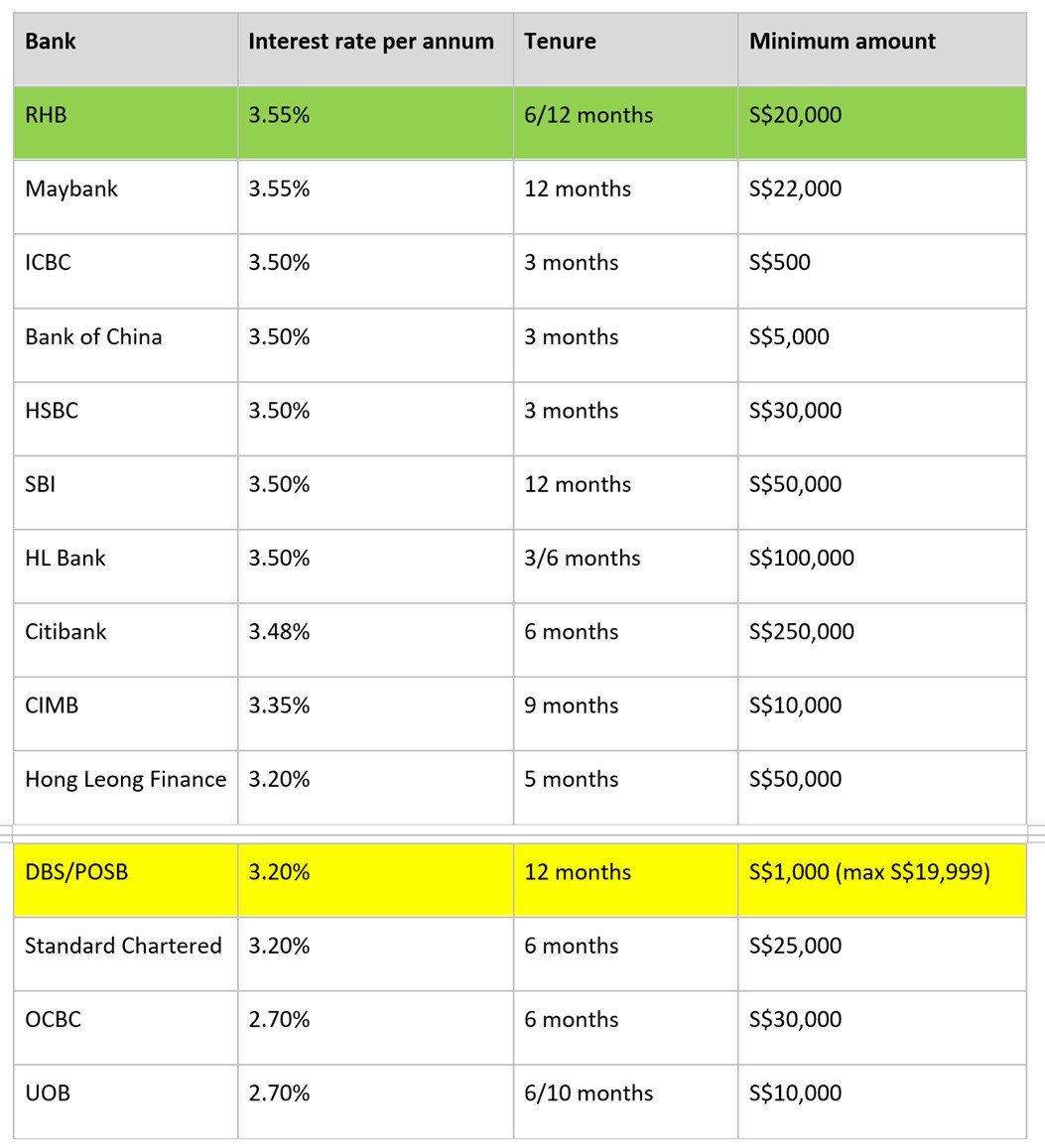

I’ve compiled the list of best fixed deposit interest rates in Singapore below (as at June 2023).

To put it simply:

- Highest Fixed Deposit Rate for a foreign bank – RHB Bank at 3.55%

- Highest Fixed Deposit Rate for a local bank – DBS Bank at 3.20%

Here’s the same in text form:

|

Bank |

Interest rate per annum |

Tenure |

Minimum amount |

|

RHB |

3.55% |

6/12 months |

S$20,000 |

|

Maybank |

3.55% |

12 months |

S$22,000 |

|

ICBC |

3.50% |

3 months |

S$500 |

|

Bank of China |

3.50% |

3 months |

S$5,000 |

|

HSBC |

3.50% |

3 months |

S$30,000 |

|

SBI |

3.50% |

12 months |

S$50,000 |

|

HL Bank |

3.50% |

3/6 months |

S$100,000 |

|

Citibank |

3.48% |

6 months |

S$250,000 |

|

CIMB |

3.35% |

9 months |

S$10,000 |

|

Hong Leong Finance |

3.20% |

5 months |

S$50,000 |

|

DBS/POSB |

3.20% |

12 months |

S$1,000 (max S$19,999) |

|

Standard Chartered |

3.20% |

6 months |

S$25,000 |

|

OCBC |

2.70% |

6 months |

S$30,000 |

|

UOB |

2.70% |

6/10 months |

S$10,000 |

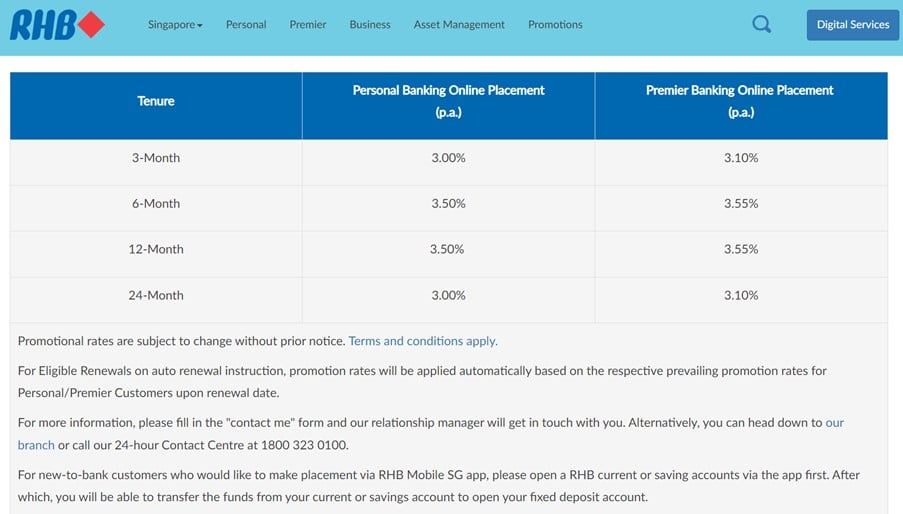

Highest Fixed Deposit Rate for a foreign bank – RHB Bank Fixed Deposit at 3.55% interest rate for 6 or 12 months

Remember just a few months ago when local banks like OCBC were offering 4.08% in one of the highest fixed deposit interest rates in the market?

And UOB was offering 3.85%?

Boy those days are long gone – both OCBC and UOB have slashed to 2.70%.

Today if you want the best fixed deposit rates you must go with a foreign bank, the local banks are nowhere to be seen.

RHB Bank is offering 3.50% on a 6 or 12 month fixed deposit, going up to 3.55% if you are premier banking.

Minimum deposit is $20,000.

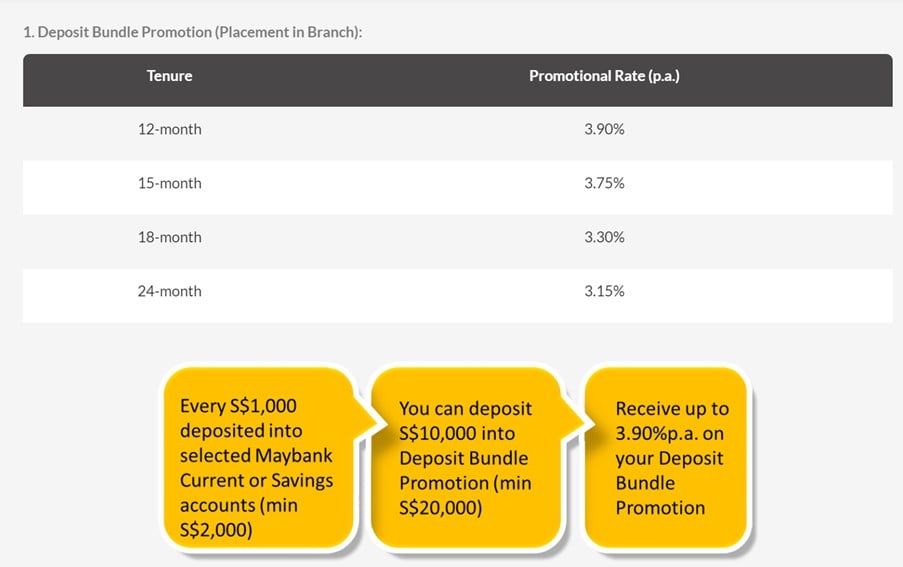

Maybank Fixed Deposit at 3.55% blended interest rate

Alternatively you can go with Maybank Fixed Deposit.

However Maybank does require you to jump through a hoop in that for every $1,000 in a Maybank account, you can deposit $10,000 into their “Deposit Bundle Promotion”.

Effectively, this gives you a 3.55% blended interest rate on the total amount (if you count the $1,000 sitting around earning no interest).

Which is higher than RHB Bank (if you are not premier banking), so it might be worth jumping through this hoop.

Do note that Maybank does require you to do the placement in the branch in person though.

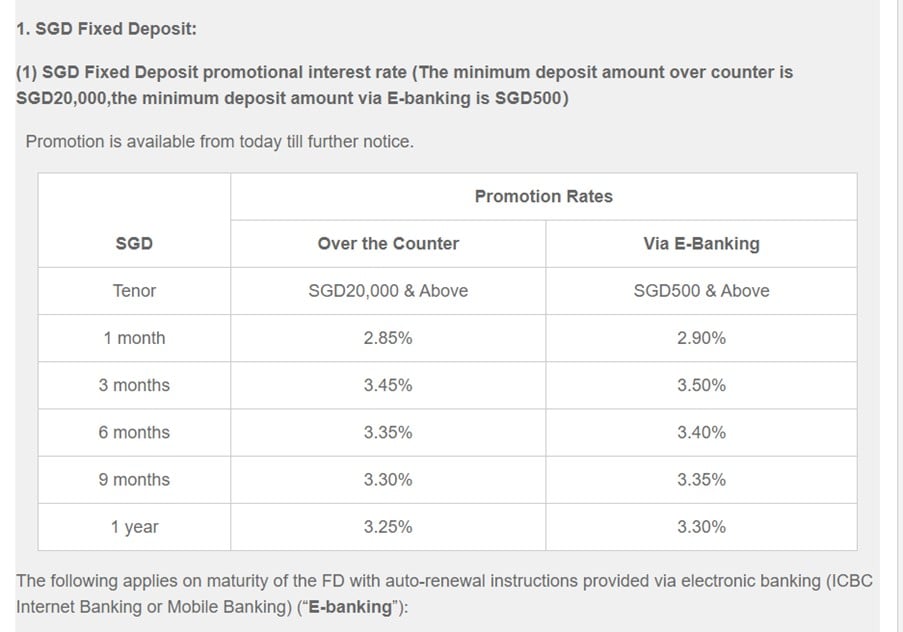

ICBC, Bank of China, HSCB etc Fixed Deposit – 3.50% interest rate

Alternatively if you’re fine with 3.50% fixed deposit rates.

Then you’re spoilt for choice – with ICBC, Bank of China, HSBC, State Bank of India and HL Bank all offering fixed deposit interest rates at 3.50%.

Here’s the promo from ICBC below:

Best Local Bank Fixed Deposit – DBS Fixed Deposit at 3.20% interest rate for 12 months

If you want to go with a local bank, your best bet is DBS at 3.20% for 12 months.

Sadly the maximum is $19,999, anything above and the interest rates drop to 0.05%.

If you want to try your luck with UOB or OCBC, their fixed deposit interest rates have been slashed to 2.70%, which is just tragic.

So you’re much better off either going with a foreign bank or T-Bills instead.

Fixed Deposits with foreign banks are SDIC insured up to $75,000, so you don’t need to worry about counterparty risk as long as you don’t deposit more than $75,000.

Will fixed deposit interest rates keep going down in 2023 – 2024?

I’ve been getting a lot of questions on why bank fixed deposit interest rates keep getting cut.

Even though the Feds are still talking about another 2 interest rate hikes in 2023.

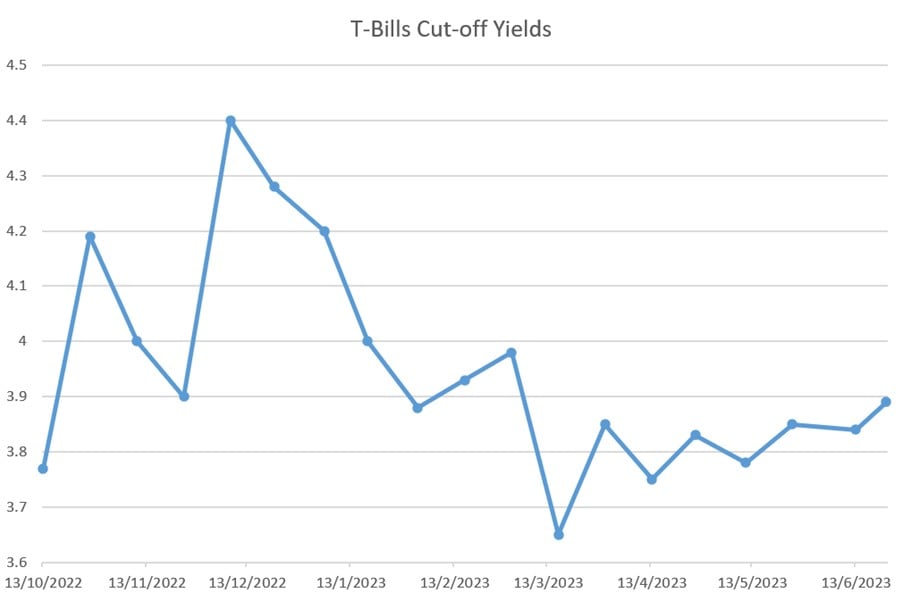

And T-Bill yields continue their march up (to 3.89% for the latest auction).

I think the key point to note here is that unlike T-Bills interest rates which are determined by the market.

Bank fixed deposit interest rates are determined by the bank officers.

If the banks need SGD funding, they will raise fixed deposit interest rates.

If the banks don’t need SGD funding, they will cut fixed deposit interest rates.

And my theory (I could be wrong), is that the local banks were bleeding deposits in late 2022 / early 2023.

Remember when everyone was going crazy and pulling bank deposits to buy T-Bills or Singapore Savings Bonds?

This worried them to the point where they raised fixed deposit interest rates aggressively to combat the outflow of cash.

And for some reason, that dynamic seems to have reversed of late.

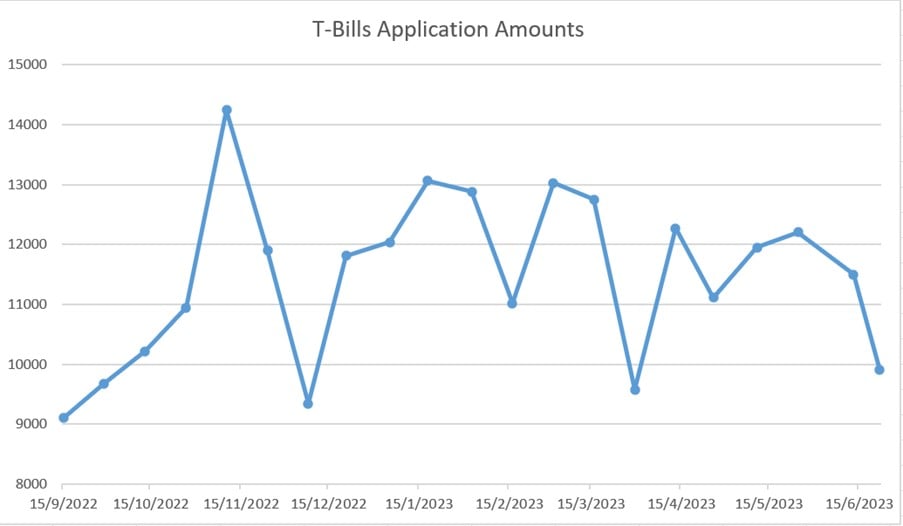

You can see how T-Bills application amounts have dropped recently too.

Throw in the fact that banks have had more time to allow their loan book to reprice to the higher interest rate environment.

And it seems that the rate of outflow of cash has stabilised, and the local banks are in much less urgent need for cash today than they were in late 2022 and early 2023.

So… where will Singapore fixed deposit interest rates go in 2023 – 2024?

Or at least that’s my theory anyway.

If I am right, then you may see the fixed deposit interest rates from foreign banks stay high in the months ahead.

But the fixed deposit interest rates from local banks are unlikely to go up significantly.

We’ll see though.

In any case, the market has become much more realistic on the path of interest rates going forward.

As I’ve been saying since the start of the year, interest rates to stay high all of 2023, with a possible terminal US Fed Funds rate of close to 6%.

And that’s what the market is pricing in today – no interest rate cuts until 2024.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Fixed Deposit vs T-Bills – Which is a better buy?

My personal view – I see T-Bills as the much better buy vs Fixed Deposits.

And I’ve been putting money where my mouth is, because my cash from maturing fixed deposits is all being rolled over into T-Bills.

I don’t see that changing going forward.

Yes you do sacrifice the liquidity because T-Bills cannot be easily sold before maturity (whereas Fixed Deposits can be broken at the cost of forfeiting the interest).

But the higher yields of 3.89% makes it worth it in my view.

But you do want to plan around the illiquidity though, so you need to have some cash lying around in a high yield savings account or money market fund that you can access for daily spending needs.

Fixed Deposit vs Money Market Funds – Which is a better buy?

Money Market Funds are an interesting alternative to Fixed Deposit though.

If you use something like the Fullerton SGD Cash Fund, if fixed deposit interest rates stay at these levels you would expect the yields to come down to the 3.5% range as well (as they mostly invest in fixed deposits).

If you’re prepared to take on more risk you could probably get a 4%+ yield, but then you’re taking on risk of capital losses.

Money Market Funds have T+1 liquidity too.

Long story short – Money Market Funds could be as competitive as Fixed Deposits in terms of yield (even going higher if you are ok to take on more risk). With better liquidity than Fixed Deposits.

For the right kind of investor, money market funds could be an alternative to fixed deposits.

I shared my views on Fullerton SGD Cash Fund recently, so do check it out if you are keen.

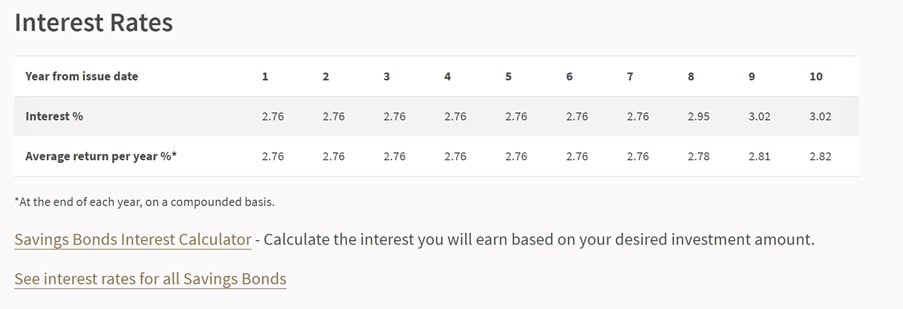

Fixed Deposit vs Singapore Savings Bonds – Which is a better buy?

Latest Singapore Savings Bonds interest rates are below.

Generally speaking you’re buying Singapore Savings Bonds to lock in interest rates of up to 10 years, and not so much for the short term yields.

You’re getting much better short term yields on either T-Bills or Fixed Deposits.

This article was written on 23 June 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 500 worth of fractional shares (expires 30 June)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- and fund $100 SGD

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

You continue to miss that Maybank pay interest up front for iSavvy FD accounts. This is a significant advantage over other banks FD accounts.

Thanks for the heads up.

What are your thoughts on upcoming 6 July Tbill rates?

Will write on this this weekend. 🙂