With the Feds committing to slow the pace of rate hikes going forward, I think it’s fairly clear the bulk of the interest rate increases are behind us.

Sure, it probably isn’t the top, but I doubt we go significantly higher from here on out.

So for investors with spare cash, it would make sense to start locking in yield at these interest rates.

That said, I think fixed deposit interest rates will stay at these levels for a while, perhaps until mid to late 2023. And I will elaborate more on why I think so in this article.

I’ve been getting quite a few requests to update the Fixed Deposit article.

So here goes!

Best Fixed Deposit Interest Rates in Singapore yield 4.2% – Better than Singapore Savings Bonds or T-Bills for your cash? (December 2022)

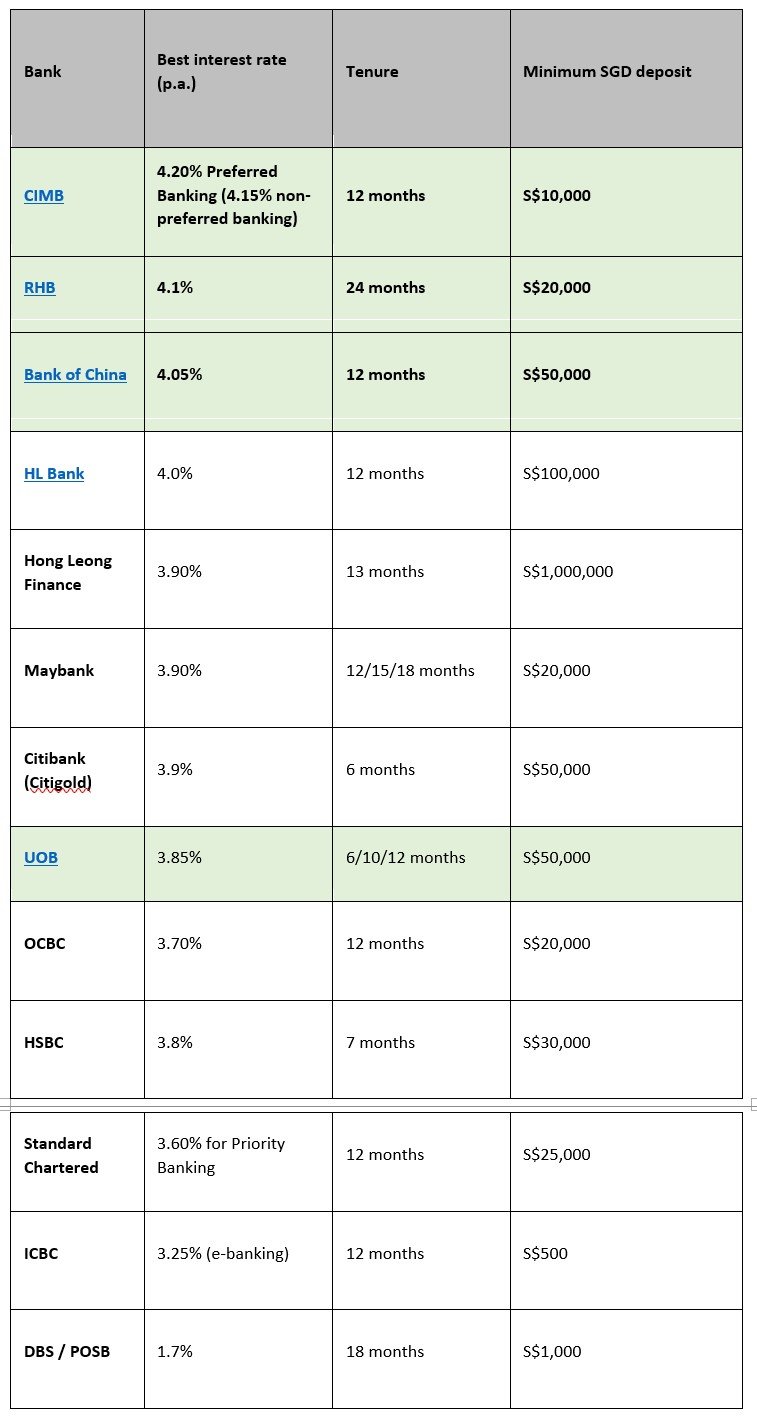

The full list of Fixed Deposit Interest rates is set out below.

But I’ll just make it simple for you.

If you are comfortable with a foreign bank:

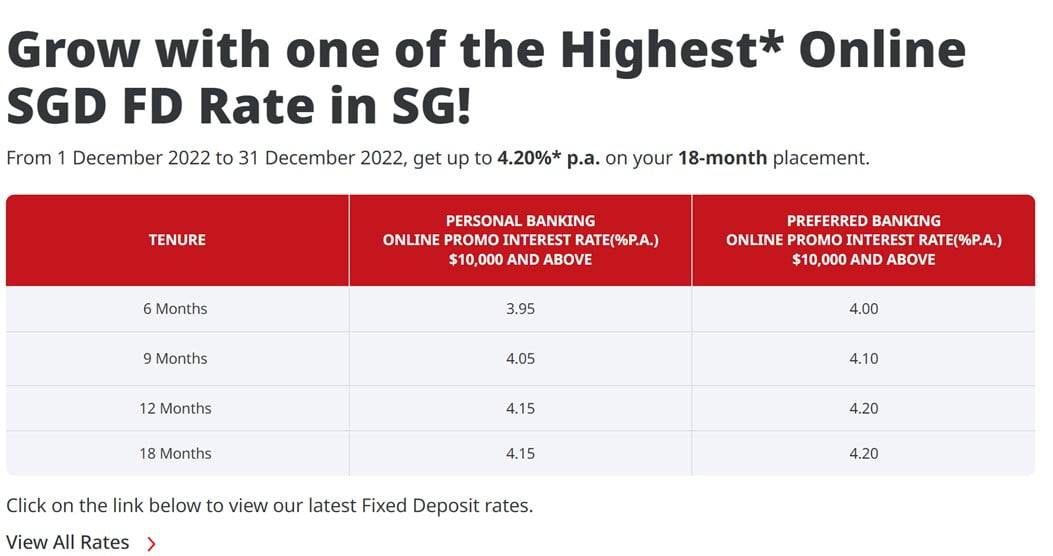

- CIMB offers up to 4.2% for preferred banking (4.15% for non-preferred banking)

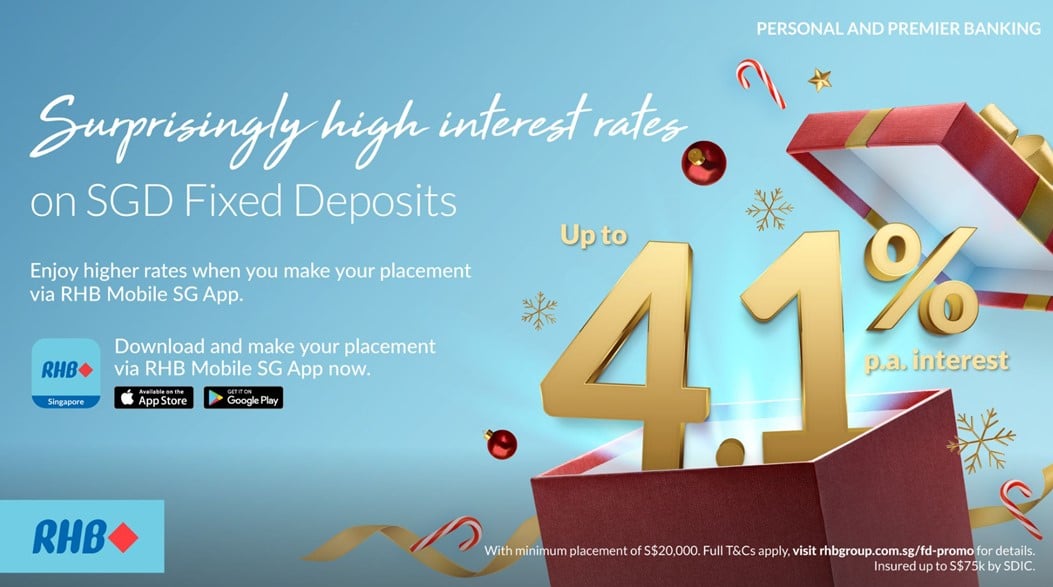

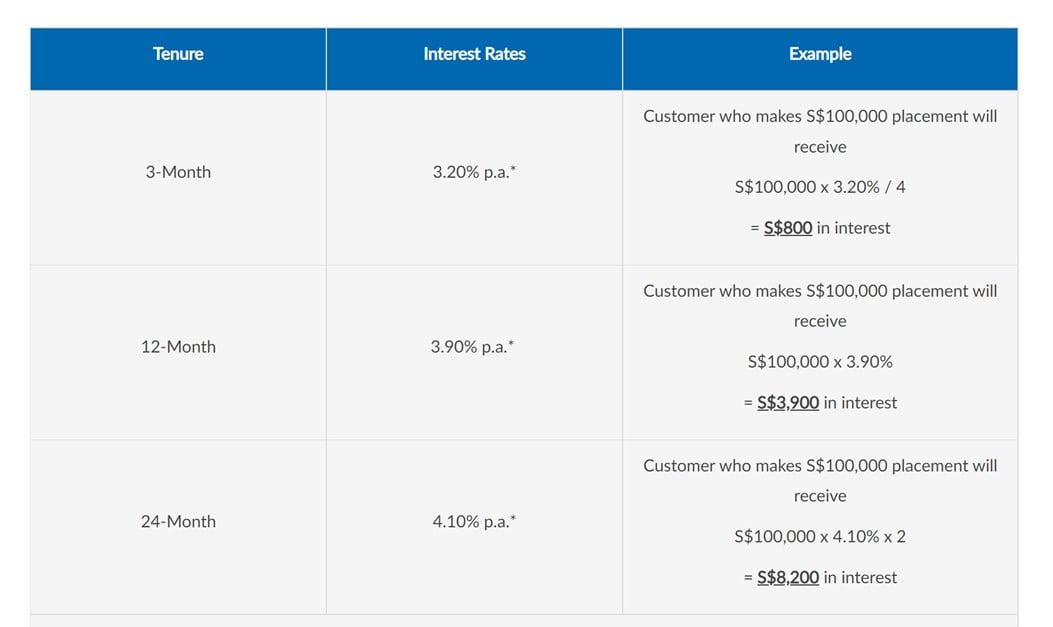

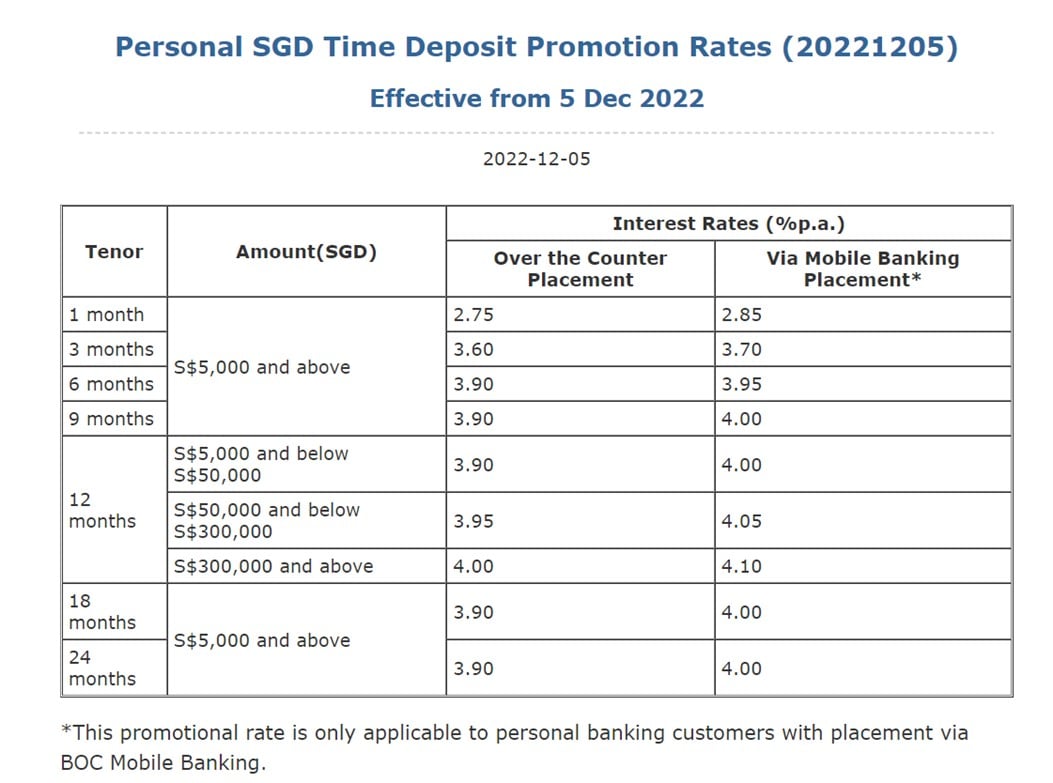

- Alternatively RHB offers 4.1% for 24 months, and Bank of China offers 4.05% for 12 months

If you prefer the peace of mind that comes with a local bank:

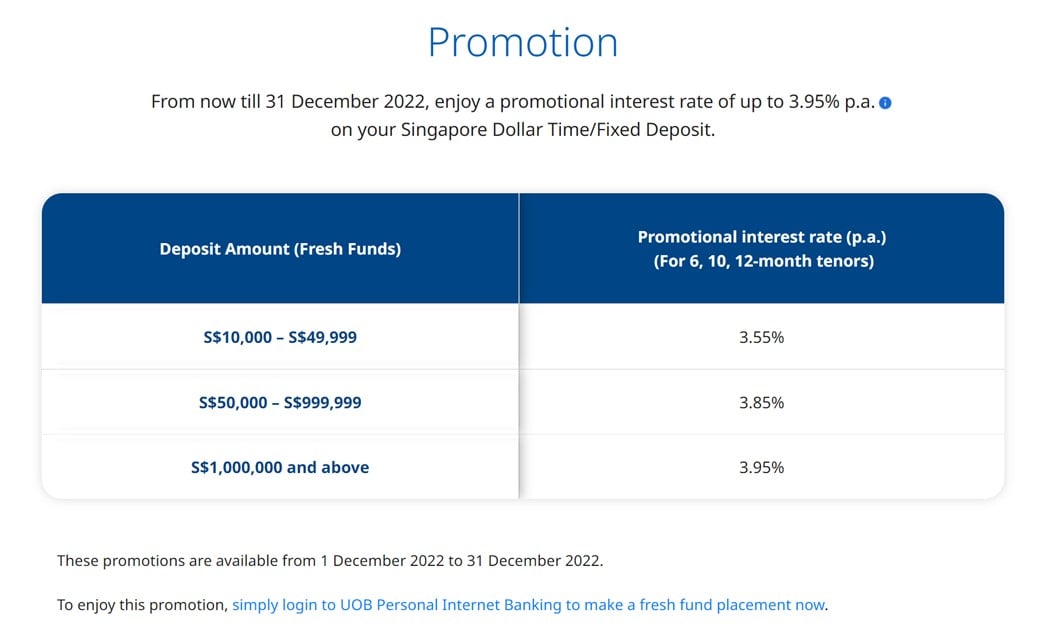

- UOB offers 3.85% for 6, 10 or 12 months

|

Bank |

Best interest rate (p.a.) |

Tenure |

Minimum SGD deposit |

|

4.20% Preferred Banking (4.15% non-preferred banking) |

12 months |

S$10,000 |

|

|

4.1% |

24 months |

S$20,000 |

|

|

4.05% |

12 months |

S$50,000 |

|

|

4.0% |

12 months |

S$100,000 |

|

|

Hong Leong Finance |

3.90% |

13 months |

S$1,000,000 |

|

Maybank |

3.90% |

12/15/18 months |

S$20,000 |

|

Citibank (Citigold) |

3.9% |

6 months |

S$50,000 |

|

3.85% |

6/10/12 months |

S$50,000 |

|

|

OCBC |

3.70% |

12 months |

S$20,000 |

|

HSBC |

3.8% |

7 months |

S$30,000 |

|

Standard Chartered |

3.60% for Priority Banking |

12 months |

S$25,000 |

|

ICBC |

3.25% (e-banking) |

12 months |

S$500 |

|

DBS / POSB |

1.7% |

18 months |

S$1,000 |

Here’s the same in picture form:

If you are comfortable with a foreign bank

CIMB Fixed Deposit – up to 4.20%

CIMB is probably the best Fixed Deposit rate available on the market right now.

For a 12 months tenure, you can get 4.2% with minimum deposit of $10,000.

Even if you’re not preferred banking, you can get 4.15% with minimum deposit of $10,000.

Fully SDIC insured up to $75,000 too.

If you want the best fixed deposit interest rate in Singapore right now, this is probably it.

RHB Bank

If you don’t want CIMB for some reason, RHB Bank is worth looking at too.

Especially if you’re looking at locking up your money for 24 months (2 years).

For a 24 month tenure, you’re getting 4.1%, with a minimum of $20,000.

The 12 month tenure is only 3.9% though, which is less attractive than other banks.

Bank of China Fixed Deposit – up to 4.10%

Bank of China is offering 4.1% on 12 months, with minimum of $300,000.

Okay I get that $300,000 is probably too large a sum for more investors.

In which case you can get 4.05% for 12 months – with a minimum of $50,000.

If you want to stick with a local bank

Now I know not everyone is comfortable with putting more than $75,000 in a foreign bank.

I’ll discuss this point in further detail below.

But for now, just know that if you want to go with a local bank, UOB is probably your best bet.

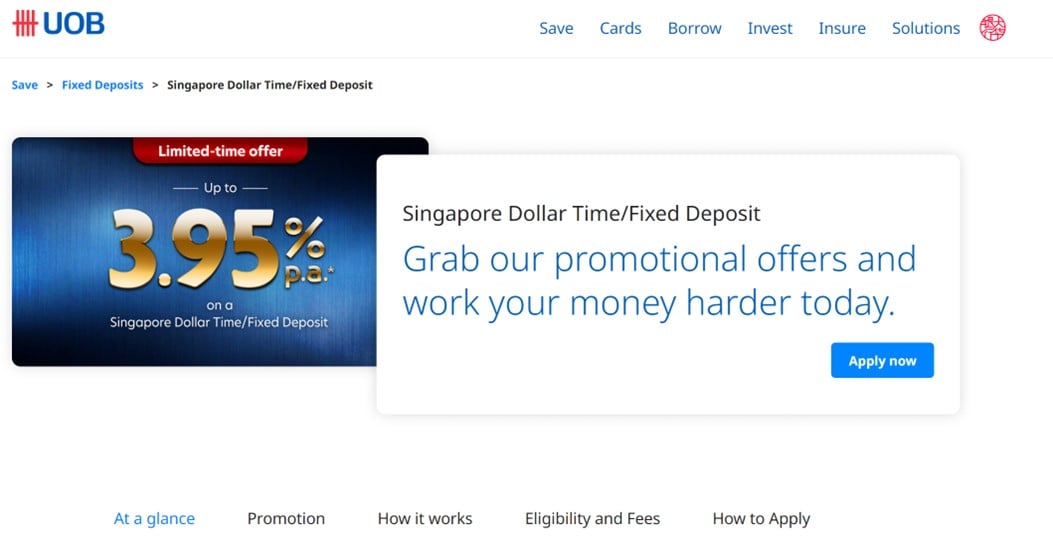

UOB Fixed Deposit – up to 3.95%

UOB offers 3.85% on 6, 10 and 12 month tenures.

With a minimum deposit of $50,000.

2 key questions that I get asked often on Fixed Deposits

Okay, on to the more interesting stuff.

There are 2 key questions that I always get asked:

- Is it safe to put more than $75,000 in a foreign bank?

- Will fixed deposit interest rates go even higher?

Let’s discuss each of them.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Is it safe to put more than $75,000 in a foreign bank?

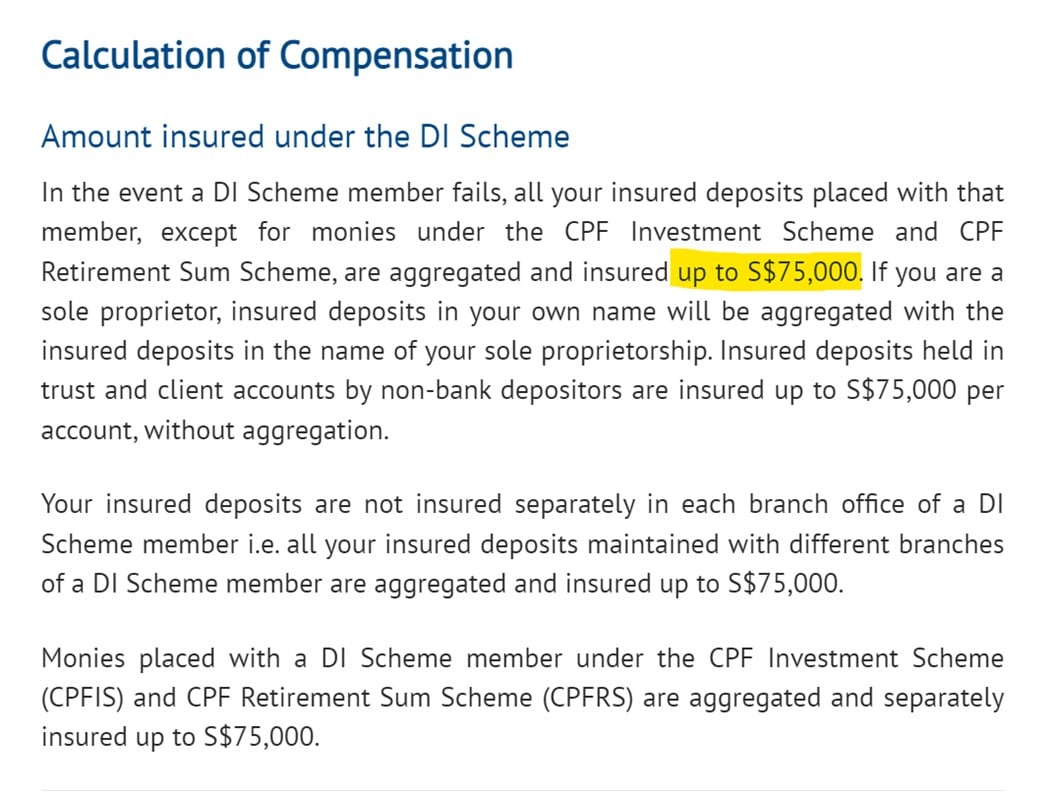

So the reason why this is a problem, is because of something called SDIC insurance.

How it actually works is a bit technical, but the long and short is that – if a bank goes bankrupt in Singapore, all customer deposits will be guaranteed up to $75,000.

This means that if you hold $50,000 with XXX foreign bank and it goes under, you get your full $50,000 back.

But if you hold $100,000 with XXX foreign bank and it goes under, you only get $75,000 back.

What is the risk of a foreign bank going under?

Let me just put it out there and say that I think the risk of a foreign bank going under in Singapore is low.

This isn’t 2008, and banks have cleaned up significantly since Lehman.

And MAS regulations are relatively stringent.

I don’t think it is likely a foreign bank will go under.

But is it impossible?

Definitely not.

The risk is low, but never zero.

Are Singapore banks “safer”?

Going by this logic, Singapore banks (DBS, UOB, OCBC) are technically not risk free either.

But I would say that in the unlikely event that they do go under, there is a good chance of MAS or the Singapore government coming in to bail them out, given potentially systemic risk to the Singapore economy.

And I suppose that Singapore banks are arguably “safer” in their risk management practices.

So with a Singapore bank you have these additional safeguards in place.

That might help you sleep at night, especially if this is your life savings.

So… Fixed Deposit in a Singapore Bank or foreign bank?

It really comes down to how kiasu you are.

And whether you’re fine to take on a slightly higher risk, for a slightly higher yield.

If you’re okay with a foreign bank you can get up to 4.2% with CIMB.

If you want to stick with a local bank you can get 3.85% with UOB.

What did I do for Fixed Deposits?

Personally for me I just chucked a whole bunch of cash into UOB’s Fixed Deposit at 3.85% for a 6 month tenure recently.

Reason being that I was topping up more than $75,000, and I wanted the peace of mind that came with a local bank.

When I’m putting money in Fixed Deposit, I want it to be as close to zero risk as possible.

If I wanted to take risk, I would be investing in financial markets.

And a more mundane reason was that I didn’t have an account with CIMB or RHB or Bank of China, and I was frankly too lazy to go down to the physical branch just for an extra 0.25% interest.

But hey – that’s just me.

I leave it for readers to decide what is best for their own situation.

Will fixed deposit interest rates go even higher?

The next big question – will fixed deposit interest rates go even higher?

I hear a lot of chatter about how we are at peak interest rates, and they will only drop from here.

What is my view?

My personal view (and for obvious reasons I could be wrong so do take this with a pinch of salt) is that:

Fixed deposit interest rates have not peaked yet. They might go slightly higher from here.

But the bulk of the interest rates increase is already behind us, so it would make sense to start locking in at these rates.

And I think fixed deposit interest rates will stay at these levels for a while, perhaps until mid to late 2023.

Why do I say this?

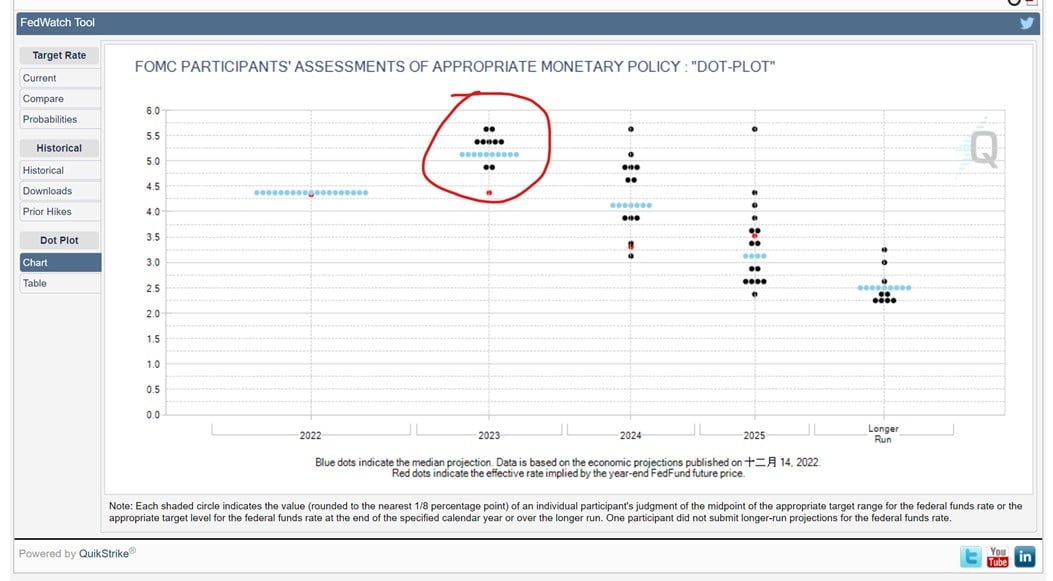

The latest Fed dot plot suggests a peak Fed Funds rate of 5 – 5.25% in 2023, and only coming down in 2024.

This would suggest a peak 6 month T-Bills in Singapore of about 4.5%, give or take 25 bps either way.

With latest T-Bills at 4.4% and 4.28%, we are already in that end game range, which suggest we are very close to peak interest rates here.

So I do think it makes sense to start locking in yields at these levels.

Although given that Feds will continue hiking the next few FOMC, we are probably not at peak rates yet.

Timing of rate cuts?

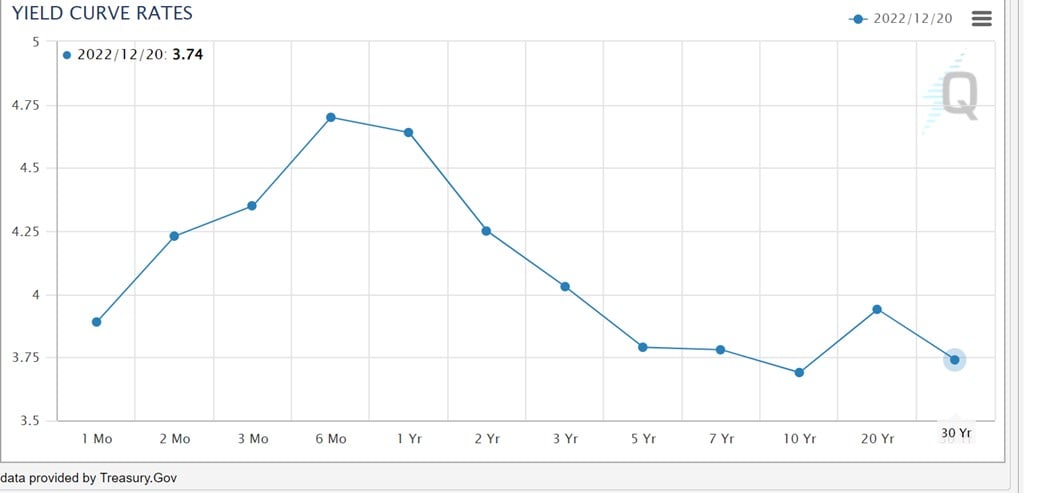

And timing wise – the futures curve is pricing in peak interest rates in 6 months to 1 year.

Which is about mid to late 2023.

I think that’s probably fair.

Long story short, I don’t think this is peak interest rates, but I think we are close.

The bulk of the interest rate increase is already behind us, and you may see interest rates stay at this level of so for the next 6 to 12 months before going down.

Whatever the case, if you’re an investor with spare cash, and you want to lock in some fixed deposit for the yield.

Now’s probably a good time, if you haven’t started already.

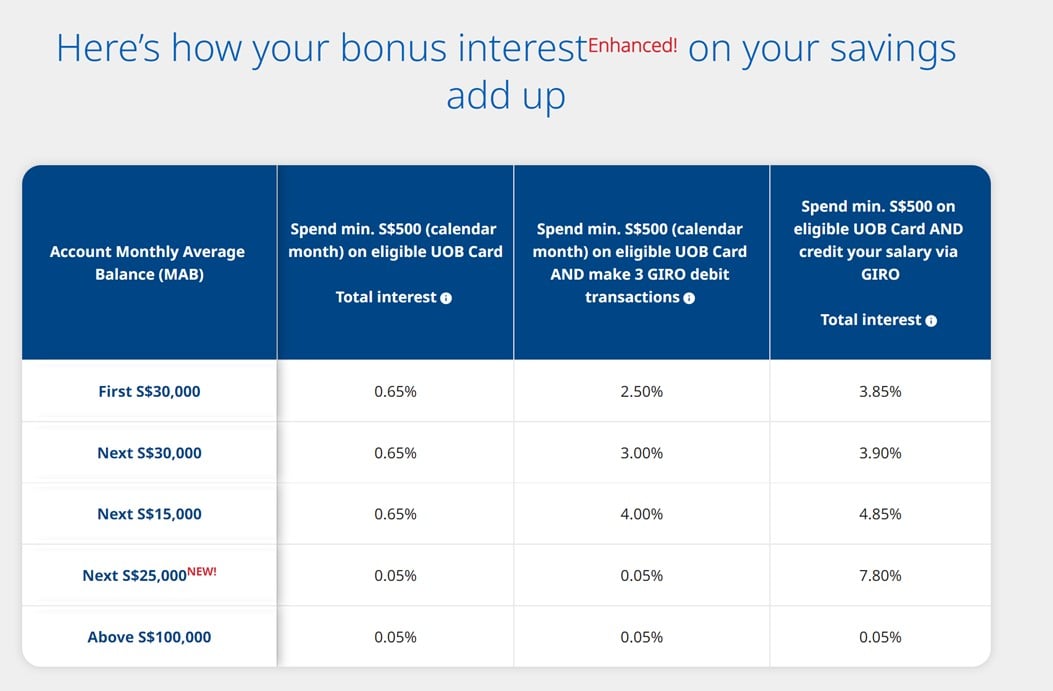

UOB One Account – up to 5% on $100,000

Just a final note that for those prepared to jump through a couple of hoops, the UOB One Account is a very fantastic deal.

If you spend a minimum of $500 on your UOB credit card, AND credit your salary via Giro.

You can get up to 5% effective interest on $100,000.

Don’t forget all this cash is fully liquid (can be transferred out any time with no lockup period).

And 5% is comfortably above latest T-Bill (4.28%) and Fixed Deposit (4.2%) interest rates.

Very good deal if you can hit the requirements.

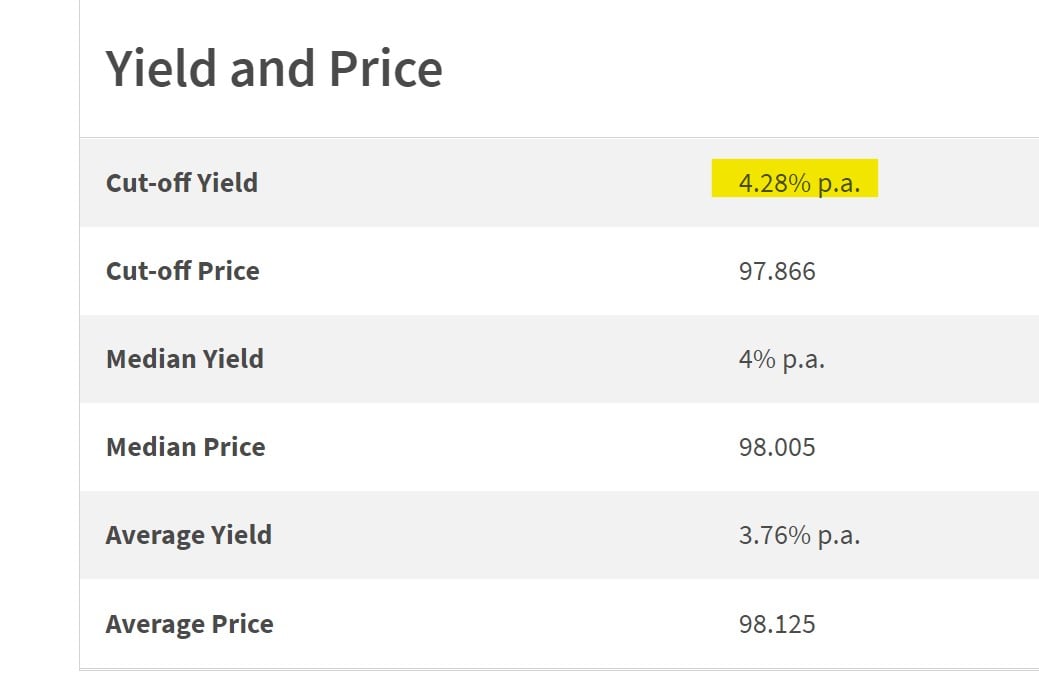

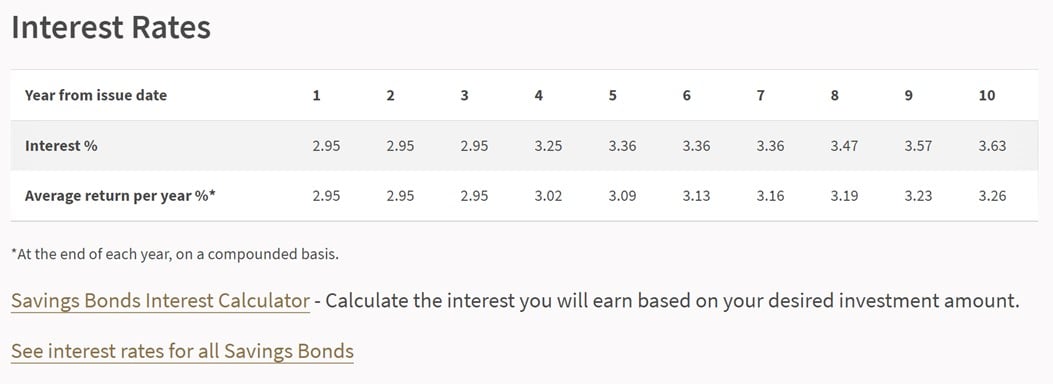

Fixed Deposit compared versus Singapore Savings Bonds and T-Bills

As a comparison, latest T-Bills are at 4.28%:

While Singapore Savings Bonds are at 2.95% for the first 3 years.

So Fixed Deposits actually fare very favourably relative to both T-Bills and Singapore Savings Bonds.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there

Hi!

Thanks for this article.

If I prefer to bank with the local banks only, then is there any point in putting money in a Fixed Deposit, compared to just investing in the T Bills which have a similar holding period and have a higher yield now?

Thanks!

Well the advantage of fixed deposit is that if you really need the money back, you can ask the bank to break the fixed deposit early for you (for a small penalty fee).

You wont have this option with T-Bills, which may be a lot harder to exit before maturity.

So it really depends on how much you value this option. If you have no plans to break the fixed deposit early at all, sticking with T Bills probably works.

Very valuable information. Thanks for sharing.

No worries, hope it helps!

Thank you! Happy New year!

Happy new year to you too!