Back in September, I wrote a post rounding up the best Fixed Deposit Rates in Singapore.

Back then, the best Fixed Deposit accounts yielded 2.85% (I know…).

What a difference 2 months makes!

Fast forward to November – and the best Fixed Deposit pays 3.9% these days.

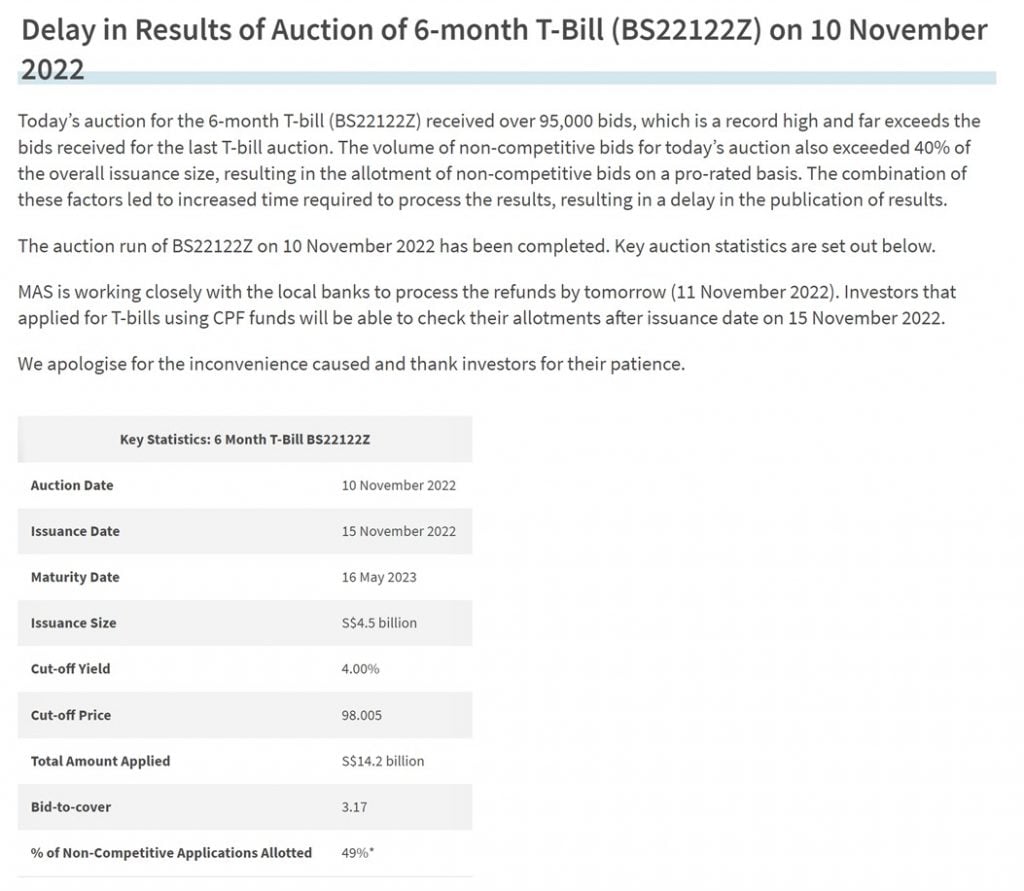

With the latest T-Bills yielding 4.0% and only seeing 49% allotment for non-competitive applications.

Suddenly Fixed Deposits aren’t looking so bad.

I’ve been getting quite a few requests to update the article on Fixed Deposits.

So here goes.

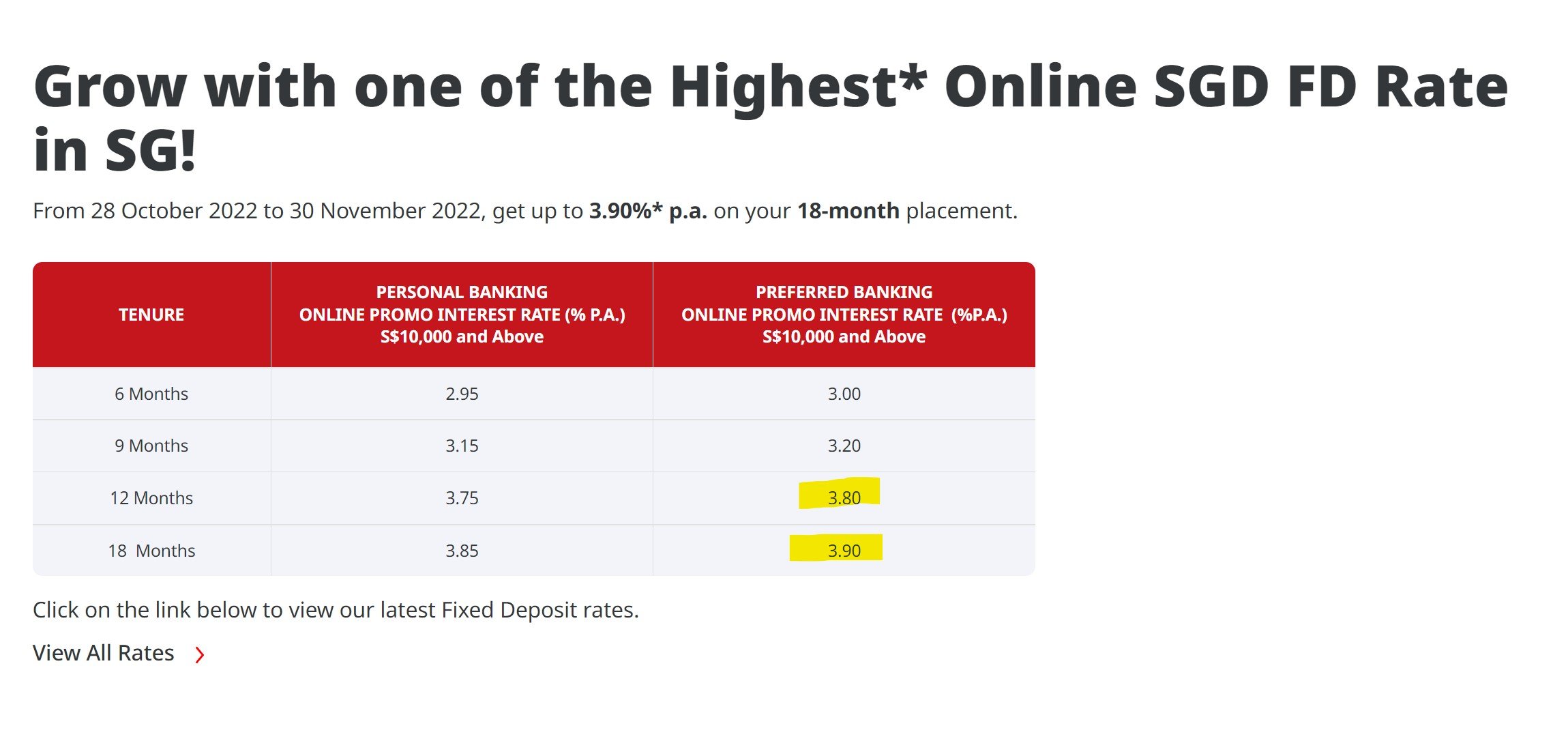

Best Fixed Deposit Rates in Singapore (November 2022)

Latest table of the best Fixed Deposit Rates in Singapore (November 2022) set out below.

Your 2 best options are:

- CIMB Bank (3.9% for 18 months, minimum deposit of $10,000)

- UOB Bank (3.7% for 12 months, minimum deposit of $50,000)

Sidenote that it seems you can also get 3.8% with DBS Bank for 5 months fixed deposit with a minimum of $20,000 (must use promo code “SR7M” when you sign up). However this doesn’t seem to be officially announced anywhere and was first uncovered by Chinese news, so I didn’t include it in the table below for now.

| Bank | Best interest rate (p.a.) | Tenure | Minimum deposit |

| CIMB | 3.9% 3.8% | 18 months 12 months | S$10,000 |

| UOB | 3.7% 3.4% | 12 months | S$50,000 S$10,000 |

| HL Bank | 3.5% | 12 months | S$100,000 |

| RHB | 3.4% | 12 months | S$20,000 |

| OCBC | 3.4% | 12 months | S$20,000 |

| ICBC | 3.25% (e-banking) | 12 months | S$500 |

| Citibank (Citigold) | 3.2% | 12 months | S$50,000 |

| HSBC | 3.2% | 12 months | S$30,000 |

| Hong Leong Finance | 3.18% | 18 months | S$20,000 |

| Maybank | 3.1% | 18 months | S$20,000 |

| Standard Chartered | 3.1% | 12 months | S$25,000 |

| DBS / POSB | 1.6% | 12 months | S$1,000 |

Benefits of Fixed Deposit

- Short Term Interest Rates are good

- SDIC Insured (up to $75,000)

- Liquidity

- No allotment limits

Short Term Interest Rates are good – 3.9% for 18 months, 3.8% for 12 months

Now CIMB’s fixed deposit rates are frankly very good.

You’re looking at:

- 3.9% for 18 months with minimum of $10,000

- 3.8% for 12 months with a minimum of $10,000

Putting things into perspective, the latest December Singapore Savings Bonds only pay 3.26% for 12 months (vs 3.8% for CIMB’s Fixed Deposit).

While the latest round of T-Bills only pay 4.0%.

And non-competitive applications only see 49% allotment.

Don’t forget T-Bills are also very different product where it is not easy to get your money back before maturity.

And these are 6 month T-Bills, which means that after 6 months the interest rates you get will depend on market interest rates at that time (which could have easily gone up or down).

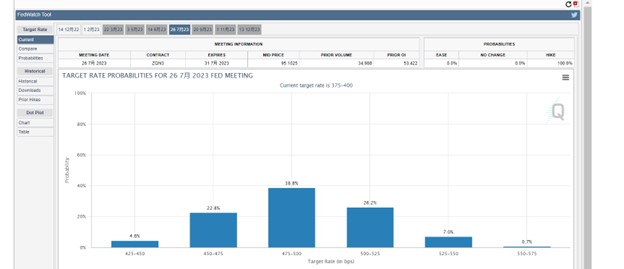

Will interest rates go up further?

Many of you ask how high fixed deposit interest rates will go this cycle.

After this week’s dovish CPI print, markets are now pricing in a peak Fed Funds Rate of 4.75 – 5.25%.

It’s debatable if futures markets are pricing this right given Powell explicitly talked about a higher terminal rate, but let’s run with this for now.

Assuming SGD strength, and a lower peak for 12 month SGD fixed deposits.

I think realistically you’ll probably see 12 month SGD fixed deposits top out anywhere from 4.0% – 4.75% this cycle.

With the best Fixed Deposit rates at 3.9%, we’re getting very close to the end-game range.

Sure, if you wait a couple months interest rates probably go even higher, but I think at these kind of rates it probably makes sense to start deploying already.

Don’t be penny wise pound foolish here.

If your cash is earning 0.05% in a savings account, do you really want to fret over whether you’re getting 3.9% or 4.1%?

SDIC Insured (up to $75,000)

Fixed Deposits are classified as bank deposits, so they are SDIC insured up to S$75,000.

Basically you can pick any bank that you want from the list above, and the amount you deposit is absolutely risk free up to S$75,000.

If you want to go beyond $75,000 you can stick with a local bank

If you want to go beyond S$75,000, and you’re worried about the solvency of some of the smaller banks, then you could just stick with a local bank.

UOB is paying 3.4% for 12 months with a $10,000 minimum.

And that rate goes up to a very attractive 3.7% if you deposit $50,000.

Those are pretty solid interest rates.

Sidenote that it seems you can also get 3.8% with DBS Bank for 5 months fixed deposit with a minimum of $20,000 (must use promo code “SR7M” when you sign up). However this doesn’t seem to be officially announced anywhere and was first uncovered by Chinese news, so I didn’t include it in for now.

What happens if you need your Fixed Deposit money back early? (Ie. Is there liquidity?)

The good part about Fixed Deposit is that if you really want your money back before maturity – you can break the fixed deposit early for a small penalty fee.

The penalty usually takes the form of a lower interest rate.

Every bank has a slightly different policy on the penalty though, so it is best to check with the specific bank you are depositing with.

Do note that the legal T&Cs usually contain a clause stating that the bank has the discretion to not allow you to withdraw your monies early.

But in my experience this is very rarely exercised (outside of a financial crisis), and you *should* be able to get your money back with a small penalty fee.

This is probably the biggest benefit over T-Bills in my view, where it is very tough to sell the before maturity as a retail investor.

So yes, with T-Bills you do get a higher interest rate, but you’re sacrificing the liquidity.

No Allotment Limits for Fixed Deposit (can go down to the bank)

Unlike Singapore Savings Bonds where you’re looking at $10,500 a month allotment.

Or T-Bills where you’re looking at 49% allotment for non-competitive, and need to struggle with auction mechanics for a competitive bid.

With Fixed Deposit you can do everything the simple and old-fashioned way, by going down to the bank (or Internet Banking).

With no allotment limits as well.

You want to put $2 million in Fixed Deposit in UOB – world’s your oyster.

Don’t underestimate this point.

There is a certain segment of the population who really value the ability of going down to the bank to manage their Fixed Deposit, and not having to mess around with internet banking or competitive / non-competitive bids.

If this is you, Fixed Deposits might make sense by itself.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Drawbacks of Fixed Deposit

Couple of minor drawbacks with Fixed Deposit:

- Slightly lower interest rates vs T-Bills

- SDIC Insured up to $75,000 only

- Cannot be held up to 10 years

Points (1) and (2) have been discussed above.

Fixed Deposit interest rates are higher than Singapore Savings Bonds, but lower than T-Bills.

And Fixed Deposit is SDIC insured up to $75,000 only – so if you plan on holding more than $75,000 you’ll probably want to go with a local bank.

Sure I get the chance of a foreign bank in Singapore going under is low, but with FTX blowing up the past week, sometimes you want to be safe rather than sorry.

Cannot be held up to 10 years

One notable drawback with Fixed Deposit is that you only lock in the interest rates for the duration that you bought.

So if you bought a 12 month Fixed Deposit at 3.8%, you get that 3.8% for 12 months only.

What interest rate you get after the 12 months, is wholly up to the mercy of the markets.

Same problem with T-Bills.

Whereas with Singapore Savings Bonds, you’re locking in the higher interest rates for potentially up to 10 years.

Even if the Feds cut to zero in 2023, you still enjoy the higher interest rates.

Pretty big point to note.

Fixed Deposit vs Singapore Savings Bonds vs T-Bills / Singapore Government Securities – Which to pick?

To sum up the pros and cons of each instrument:

| Singapore Savings Bonds | T-Bills | Fixed Deposit | |

| Short Term Interest Rates (< 18 months) | Low | Good | Average |

| Risk Free | Yes | Yes | Up to $75,000 SDIC insured |

| Allocation Limit | Poor | Average | Good |

| Liquidity (ability to exit before maturity) | Good | Poor | Average |

| Ability to lock in interest rates long term | Good | Poor | Average |

What am I doing – Fixed Deposit vs T-Bills vs Singapore Savings Bonds?

As I’ve said many times, for me in 2022/2023 – liquidity is king.

With interest rates going to 5.0% by mid 2023, I think at some point in the next 12 – 18 months something is going to break.

You already see the signs of stress building in the system, from the leverage unwind.

You see the BOJ intervening with the Yen, the UK Gilt fiasco that ended with Liz Truss’s resignation, Credit Suisse, FTX this week, and so on.

The tide is going out, and when it does, we’ll be able to see who’s been swimming naked.

So far it’s been at the fringes, but at this unwind spreads, bigger players will get hit.

In a climate like that, I prize liquidity very highly.

And I am happy to accept a slightly lower yield on my cash, as a cost of that liquidity.

So my favourite instrument for my cash remains Singapore Savings Bonds, for the ability to redeem any time with accrued interest (you get the cash back at the start of the following month).

And I keep some cash in a high yield savings account like Trust Bank (up to 1.5% on $75,000), Singlife or DBS Multiplier, as I do need the instant liquidity for daily needs.

T-Bills have real liquidity issues, so I would probably only use it if I don’t see myself needing the funds for 6 months or more.

Fixed Deposit could come in handy to plug the gap.

So sequence wise it will be:

- Minimum cash in savings account

- Max out Singapore Savings Bonds each month

- T-Bills / Fixed Deposit for higher yield at the expense of liquidity

- Rest in savings account as liquidity

But hey – that’s just me.

The exact mix and allocation will have to depend on each investor, to find the right balance between yield and liquidity.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi FH, thank you for writing so many useful articles. I have a question :what is your take on China Taiping’s i-Save, which is offering

Guaranteed Total Returns of 11.36% 3-year total return (3.65% p.a.) of Single Premium.

Capital Guaranteed and covered by SDIC.

Death benefit of 105% of Single Premium from the 12th policy month onwards.

Thank you.

Probably not a product I would use myself because of the 3 year duration. But really depends on each investor.

i tried https://www.foodiesg.com/archives/52459 it works , nice 🙂

Great! Glad it helps