A lot of you have asked about Chocolate Finance recently.

The long and short, is that Chocolate Finance offers:

- 4.5% yield guaranteed on first $20,000

- No lock up period – withdraw anytime

Anyone familiar with markets will know that if your 6 month T-Bill is yielding 3.70%, that’s your very definition of risk free rate.

If Chocolate Finance can offer 4.5% yield guaranteed with instant liquidity – surely there has to be some catch right?

The more I looked into Chocolate Finance, the more I found this to be quite a nuanced product that wasn’t as straightforward as it seemed at first glance.

So I wanted to share some views in this article.

Chocolate Finance is open for new signups again (as of July 2024)

As of July 2024 – Chocolate Finance is open for signups again!

Check out my latest review here.

Chocolate Finance is invite only, but if you’re keen to try it out you can use the referral link below:

https://share.chocolate.app/nxW9/ep4q7wxp

What is Chocolate Finance?

The FAQs from Chocolate Finance do a fantastic job of explaining what the product is.

I’ve extracted the key questions below, with emphasis (bolded) from me.

If you already know what Chocolate Finance is about, feel free to jump straight to my analysis below.

Chocolate Finance FAQs

“What is Chocolate Finance?

Chocolate Finance is a new place for your spare cash. Enjoy 4.5% p.a. return on your first S$20k and a target 3.5% p.a. on any amount thereafter. No lock-ins, no hoops to jump through.

What’s more, we take no fees and make no money until we deliver the target return.

How does Chocolate Finance generate these great returns?

Banks generate returns by investing your deposits mainly in mortgages and credit to get returns. Chocolate instead invests your money into a portfolio of fixed-income funds designed to optimise risk-adjusted returns based on duration, spread, and currency. This allows the portfolio to target a return of 4.5% p.a. for the first S$20k, and 3.5% p.a. thereafter.

See your returns daily in the app. What’s more, if the portfolio doesn’t make the target 4.5% p.a. for your first S$20k, we will top up the difference to ensure you enjoy the target return during the Qualifying Period.

We take no fee and make no money until we deliver the target return. Does it get any better than that?

Is Chocolate Finance SDIC insured?

Chocolate Finance is not a bank. Money in banks need SDIC protection because if the bank fails your money is gone. This is not the case for asset managers. With Chocolate Finance, funds are segregated and held separately by our fund managers’ custodians – HSBC and State Street. This means that if anything goes wrong with Chocolate, your money is still safe and protected. Think of it like a fireproof safe inside a house. Whatever is inside is safe even if the house burns down.

Is Chocolate Finance legitimate and regulated by MAS?

Yes, Chocolate Finance is absolutely legitimate! Chocolate Finance is a managed account service operated by Havenport Investments Pte Ltd, a Holder of a Capital Markets Services Licence regulated to perform fund management activities, dealing in capital markets products, and providing custodial services. Havenport Investments Pte Ltd is also an Exempt Financial Adviser regulated to perform financial advisory services in Singapore. Chocolate Finance is a brand licensed for use by Havenport from Chocolate Pte Ltd. Rest assured, Havenport Investments Pte Ltd is regulated by the Monetary Authority of Singapore (license number CMS100173) Chocolate Pte. Ltd is a registered Singapore private company and a member of both the Singapore Fund Administrators Association and the Singapore Fintech Association.

As there are no fees, how does Chocolate Finance make money?

Chocolate invests your savings in a portfolio of fixed-income funds. We only make money once you’ve made money. So naturally, it’s our number one priority to make the returns we’ve targeted for you. We make our money when the funds overperform.”

How long does this promotion last?

“The Qualifying Period shall run from 1 August 2023 to the earlier of:

- a) 30 June 2024, 2359 hours; or

- b) the date on which the Net Asset Value of the Chocolate Managed Accounts of all Customers meets or exceeds S$500,000,000.

Chocolate reserves the right to amend the Qualifying Period at any time, including with reasonable notice published in the Chocolate Mobile Application to shorten the Qualifying Period. Please refer to the Chocolate Mobile Application or www.chocolatefinance.com for the most current information and details on the Qualifying Period.”

TLDR – 4.5% yield, but not SDIC insured

So to sum it up quickly:

- 4.5% yield on $20,000

- Instant liquidity – withdraw any time

- No minimum amount

- NOT Risk Free – Not SDIC insured or backed by the Singapore government

So… how does Chocolate Finance generate 4.5% returns with instant liquidity?

If your question is how does Chocolate Finance generate 4.5% returns with instant liquidity.

Well – I had the same question too.

The answer per their FAQS is that:

“Chocolate instead invests your money into a portfolio of fixed-income funds designed to optimise risk-adjusted returns based on duration, spread, and currency. This allows the portfolio to target a return of 4.5% p.a. for the first S$20k, and 3.5% p.a. thereafter.”

As to which fixed income funds they use:

“The Chocolate Managed Account is a new portfolio of fixed-income securities comprising a collection of funds. The portfolio is currently made up of Dimensional STIG SGD, UOBAM United SGD Fund, and Fullerton SGD Cash Fund. These may change at the sole discretion of the portfolio manager. In your Chocolate app, you will be able to see the information on each fund and the percentage of money allocated to them.”

Fair enough.

What is the exact asset allocation used by Chocolate Finance?

But this horse couldn’t contain his curiosity.

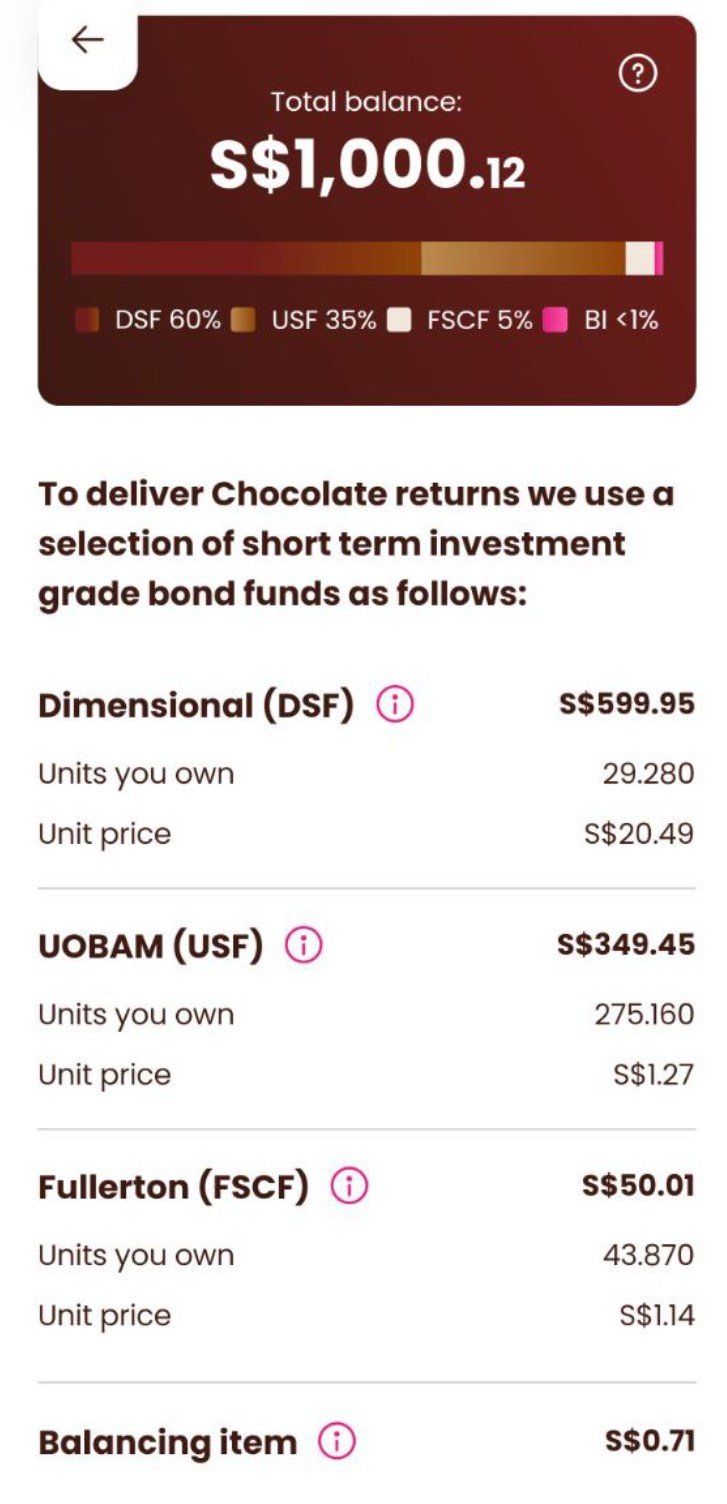

So I funded $1000 into a Chocolate Finance account just to see what the underlying asset allocation was.

Here’s what was allocated to me:

At a high level:

- Dimensional Global Short-Term Investment Grade Fixed Income Fund SGD – 60%

- UOBAM United SGD Fund – 35%

- Fullerton SGD Cash Fund – 5%

Let’s dig a bit deeper into each of these fixed income funds.

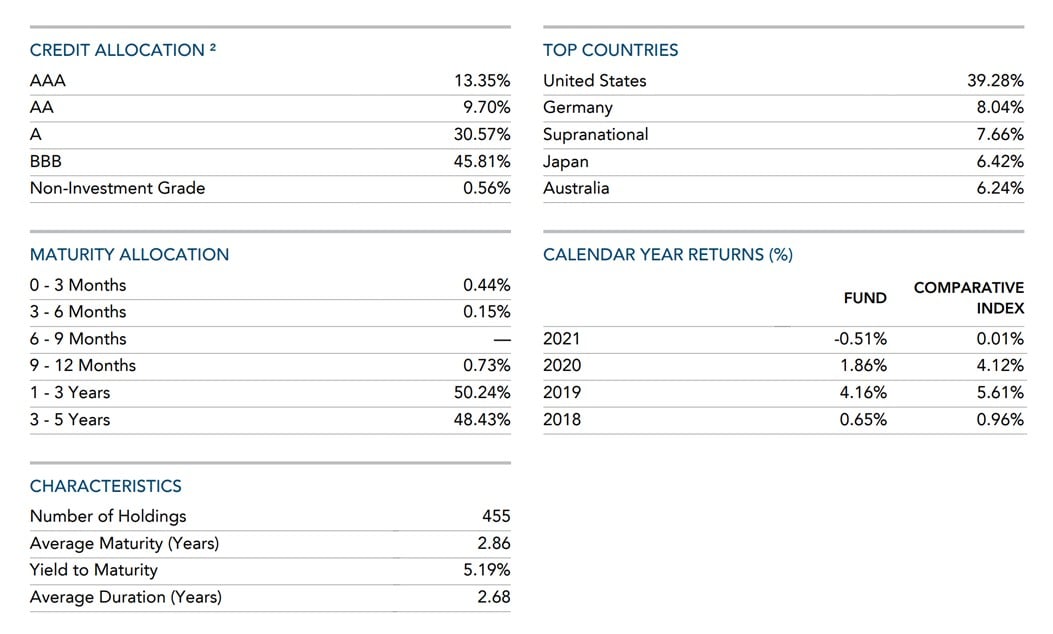

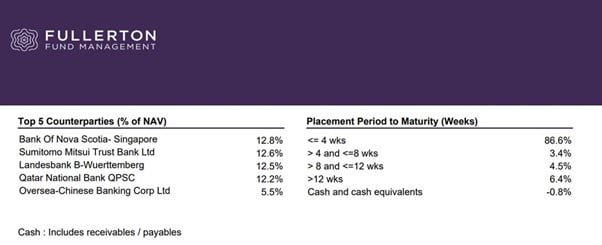

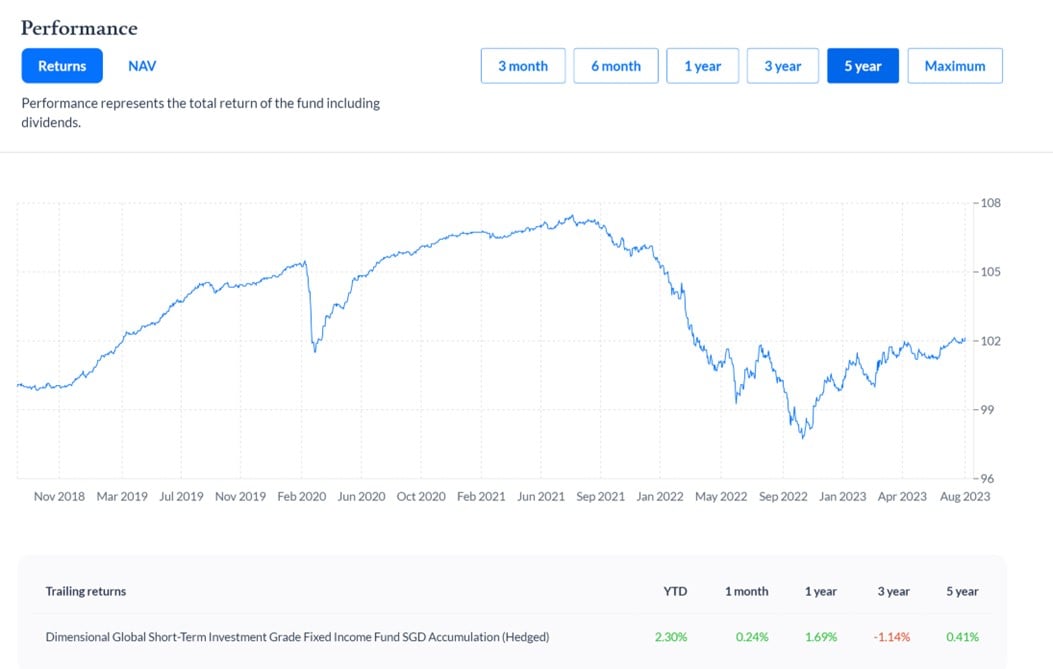

Dimensional Global Short-Term Investment Grade Fixed Income Fund SGD – 60%

I’ve extracted the key metrics of Dimensional Global STIG Fund below.

60% of the money goes into this Fund, so this is the key one to look at.

You’re looking at:

- 2.8 years average duration

- ~5% yield to maturity

- 40% allocation to US bonds

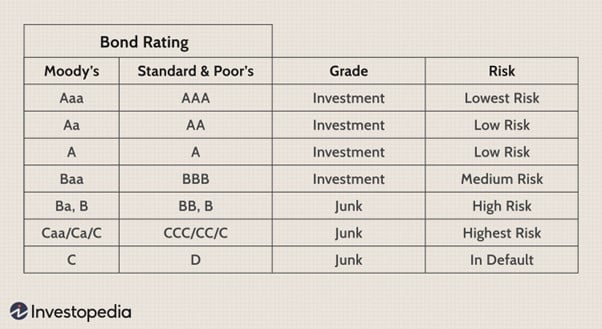

Interestingly – this Fund only has a 13% allocation to AAA Bonds.

It has a 30% allocation to A rated Bonds.

And a whopping 45% allocation to BBB rated bonds (just one level above junk).

I’ve extracted the credit rating scale below for reference.

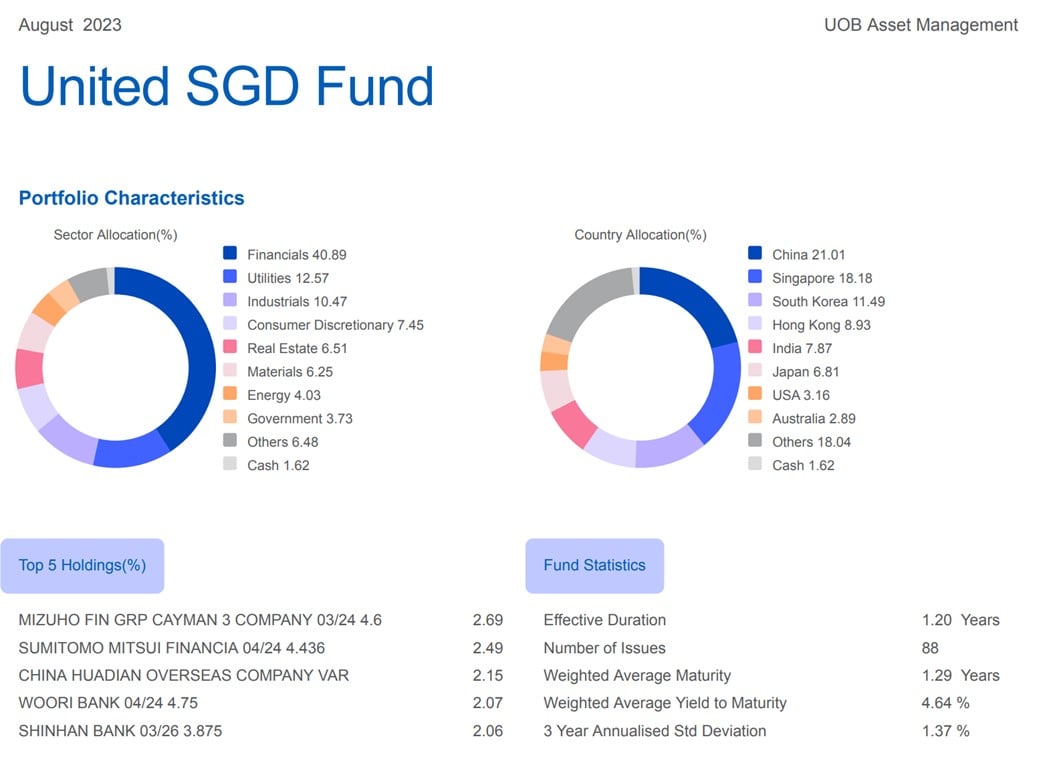

UOBAM United SGD Fund – 35%

Here’s the metrics for UOBAM United SGD Fund – where 35% of the money went.

You’re looking at:

- 1.2 years average duration

- 4.6% yield to maturity

- 21% exposure to China (followed by 18% to Singapore)

Fullerton SGD Cash Fund – 5%

And finally, 5% goes into Fullerton SGD Cash Fund.

I’ve covered Fullerton SGD Cash Fund in the past, so do check out my article for the full review.

Basically this is a low risk money market fund that deposits your money in <4 weeks fixed deposits.

Approximate yield of 3.5% – 3.8%.

What are the risks associated with Chocolate Finance’s Asset Allocation?

Taking a step back.

If you want to earn a higher yield on cash – there are 2 options:

- Take on more credit risk

- Take on longer duration (lock up period)

That looks like what Chocolate Finance is trying to go for here.

The only short duration money market fund they’re using is Fullerton SGD Cash Fund at 5% of the asset allocation.

The other 95% goes into longer duration bonds of 1-2 years duration.

And they’re also not risk free, so there is credit risk in exchange for the higher yield.

If you think about it this way – then there are 2 risks here:

- Default risk (of the underlying assets)

- Duration risk (if interest rates go up)

Default risk (of the underlying assets)

Let’s start with the simple one – Default risk.

The biggest allocation (45%) goes to Dimensional Global STIG Fund, of which 75% is allocated to A / BBB rated bonds.

Let’s say some of the underlying bonds default.

It’s not impossible to see capital losses for the Dimensional Global STIG Fund.

In that scenario Chocolate Finance guarantees your 4.5% for the first $20,000, so I suppose the question is whether Chocolate Finance will be able to cover the loss (we’ll discuss this below).

Duration risk? Asset Liability mismatch?

The next risk – is duration risk.

Also known as Asset Liability mismatch.

The most extreme example of this came with Silicon Valley Bank earlier this year.

If you recall:

- Silicon Valley Bank used customer deposits to buy long-term US Treasuries

- When interest rates went up, US Treasuries dropped in price

- This meant a mark to market loss (but no problem as long as the Treasuries were held to maturity)

- The problem came when depositors started to pull their funds en masse

- This forced Silicon Valley Bank to liquidate the Treasuries at market price (to meet redemptions), thereby crystallising the loss, and impairing their balance sheet

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Can the same thing happen with Chocolate Finance?

For the record, this was especially bad with Silicon Valley Bank because they bought US Treasuries at close to 1% yields and held them all the way up to 4%+ yields which meant a 20%+ capital loss.

Given that Chocolate Finance is buying 1-2 year bonds, and how we are already close to peak interest rates here – the impact from rising interest rates *should* not be as large.

I’ve extracted the price chart for Dimensional Global STIG Fund below.

You can see how the peak to trough loss during the 2021 – 2022 period was only around 8%.

And don’t forget that was a period where Fed Funds Rate moved from 0% to 5.5%.

You’re unlikely to see a similar magnitude of move going forward.

But I mean, never say never.

So… what is the risk here?

I suppose the risk here.

Is that due to credit default, or rising interest rates – the value of the underlying bond funds purchased by Chocolate Finance drops.

Customers with funds in Chocolate Finance start to withdraw.

In that scenario how does Chocolate Finance react?

Do they sell the underlying funds and lock in the loss?

Or do they pay out using the difference using their equity / cash on hand?

How much equity does Chocolate Finance have on hand?

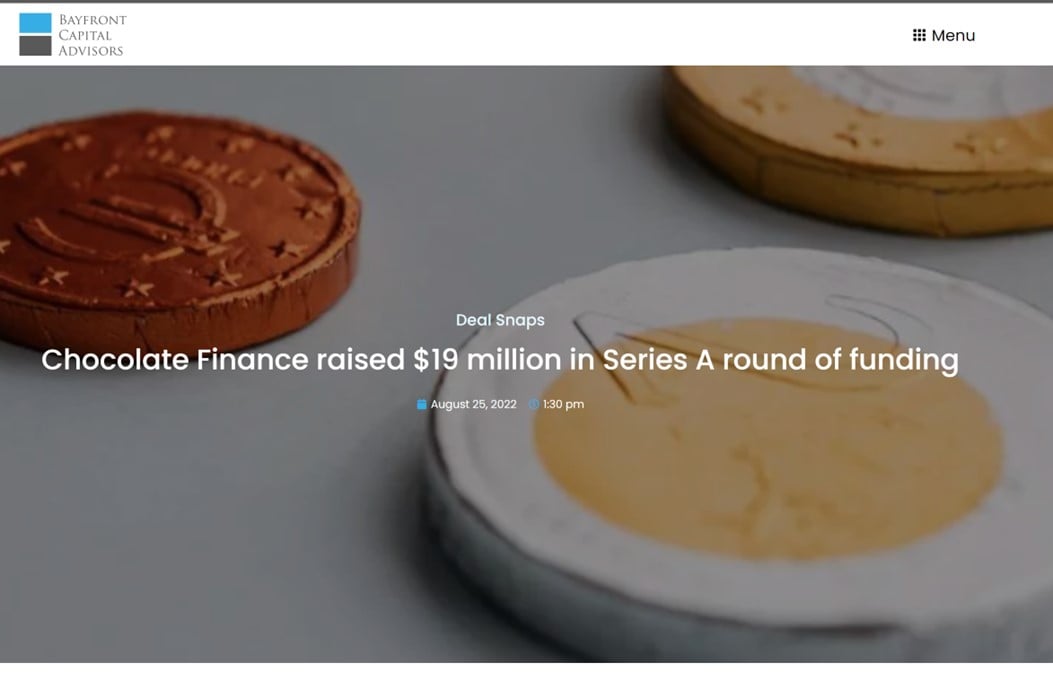

So I looked a bit more into Chocolate Finance.

It turns out they just raised $19 million in funding last year – so they do have some funds to cover the losses (if required).

Led by Sequoia India too, which is very impressive:

Singapore-based fintech startup Chocolate Finance raised $19 million in Series A funding. Led by Sequoia India, this round witnessed the participation of Prosus Ventures, Orion Advisors, Credit Saison, Global Founders Capital, Dara Holdings, Ion Pacific and ChocVen.

FYI that at this moment, Chocolate Finance guarantees the 4.5% yield until the earlier of (a) June 2024, or (b) they hit $500 million in assets.

Who is the founder of Chocolate Finance?

In case you were wondering, the founder of Chocolate Finance is a very experienced guy, who previously founded Singlife as well.

I extract his bio below for reference:

“Mr. Walter de Oude is the Founder of Chocolate Finance. He served as Founded Director of Singapore Life. He also served as its Group Chief Executive Officer and Deputy Chairman. He served as Deputy Chairman at Aviva Singlife Holdings and Board Member at Singlife Philippines. He served as a Board Member at RailsBank. Prior to Singapore Life, he joined HSBC Insurance (Singapore) in 2007 as Chief Actuary and Head of Products and was appointed as the chief executive officer in June 2010. He holds a Bachelor’s in Economic Science from the University of Witwatersrand. He is also a fellow of the Faculty of Actuaries, Edinburgh.”

My Views on Chocolate Finance?

I was a big fan of GXS a month or two back because GXS Bank was SDIC Insured.

Sure their business model of paying 3.48% yield with instant liquidity probably wasn’t sustainable, but given that all deposits are SDIC insured up to $75,000 it didn’t bother me one bit.

And now you have Chocolate Finance paying 4.5% yield with instant liquidity, which is even better than GXS Bank.

With Chocolate Finance though, it’s important to note that this is not SDIC insured (unlike bank deposits), nor is it backed by the Singapore government (unlike T-Bills or Singapore Savings Bonds).

So for the avoidance of doubt – Chocolate Finance is NOT a risk free product.

What is the risk I am taking on here?

What exactly is the risk I am taking on, I’m not very sure myself.

I suppose it’s a mix of credit default / duration risk, to the extent that Chocolate Finance’s equity is wiped out.

What is the chance of this risk materialising?

Frankly I have no clue.

It will depend on Chocolate Finance’s asset allocation and how it changes over time, their risk management practices, how much money they can raise, how quickly customers pull funds and so on.

Not easy to evaluate.

At the end of the day though, this is a cash management product.

I could spend all that effort to monitor the risk in play, or I could just chuck the money into a 3.70% risk free T-Bill and sleep soundly at night.

Will I leave my money with Chocolate Finance?

In the spirit of full disclosure, I have a Chocolate Finance account – which I funded with $1000 for the purposes of this article.

I’ll probably leave those funds there, just to see how this plays out.

But I probably won’t be funding more money in.

When it comes to my cash, I usually want it to be risk free – which in my books means (a) SDIC insured, (b) backed by the Singapore government, or (c) held by one of the 3 local banks.

I’m happy to take risk in my equity investments – where I’m risking money for unlimited upside.

But when it comes to cash, where I take on risk just for a 0.8% spread vs the risk free, I’m not so sure if that makes sense.

Would love to hear what you guys think though.

Do you have money with Chocolate Finance?

Do you think the 4.5% yield on cash is the last remaining “free lunch” in today’s market?

This is a premium article that I originally wrote in response to queries from Patrons. Releasing it to the public as it may be helpful for others out there as well.

If you enjoy content like this, do sign up as a Patreon for my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning.

This article was written on 31 August 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 800 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 800 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Qns on Chocolate Finance:-

1. Is interest credited daily?

2. If I withdraw after say 1 month, will I earn the interest for that 1 month?

3. Is the 4.5% pa interest dependent on a minimum tenure of investment?

Rgds

My replies below – but do note the risks I flagged in this article.

1. Yes

2. Yes

3. Subject to their T&Cs – until mid 2024 or 500m NAV, further discretion to change terms and so on