So earlier this week we did a poll asking if you preferred to read about (1) COVID-19 or (2) United Hamshire REIT IPO.

The answer was overwhelmingly in favour of (1), but there was quite a lot of interest in (2), so I decided to just do both anyway. We did an article on the United Hamshire REIT IPO yesterday (check it out here), which frees us up today to focus on the big one – COVID-19.

As we said last week, these are momentous times in financial markets. You guys have been with the blog since the start, and I owe it to you to share my honest opinion in a time like this. No qualification, no paywall bullshit. Just honest opinions from a fellow investor.

Whether you think I’m right or wrong, and what you choose to do with this, I leave it up to you entirely.

My only ask – if you agree with me, share this article. Share it with your friends or family who invest. Let’s get the information out there. I don’t want any unwitting investor to get caught up in what’s about to happen.

Basics: Impact on Financial Markets the past week

Let’s take a look at the impact on financial markets. I’ve tried to use the 5 year charts where possible, so that there is perspective.

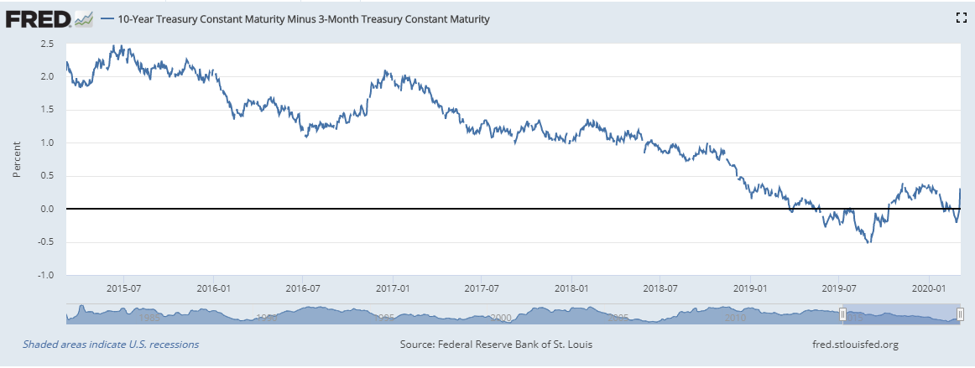

This is the 3s10s yield curve. It first inverted in the second half of last year, and again in Feb 2020. After the Fed cut rates this week, it’s been on a bull steepener (yield curve uninverts due to rate cuts on the short end), which is usually the last signal we get from yield curves before the recession.

Here’s the US high yield spread – the uptick at the end in Feb 2020 is why the Feds had to cut, and why they had to cut quick. Notice how quickly the high yield spreads blew out this time, as compared to late 2018 and 2016, the 2 other times where we came close to a recession this cycle.

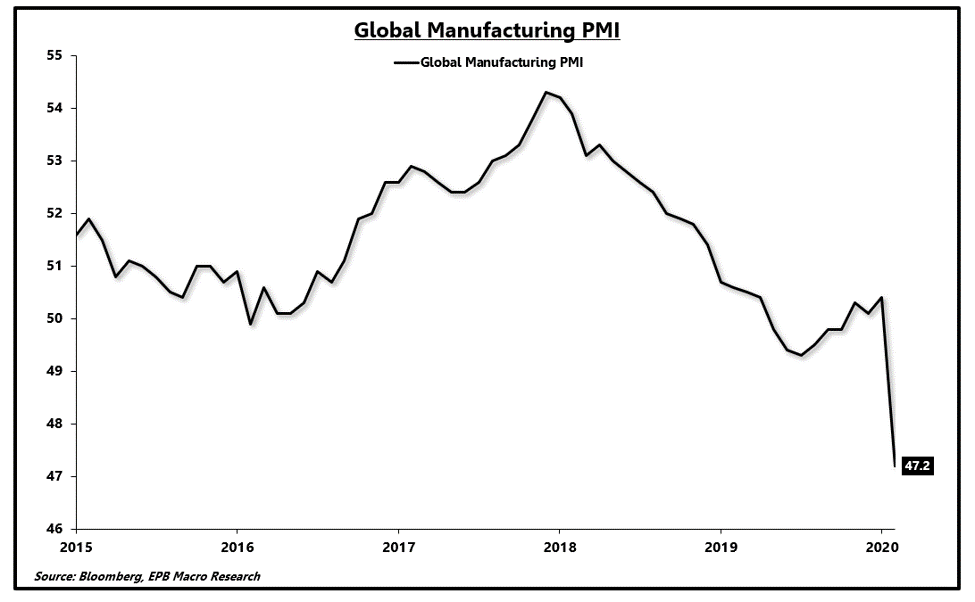

Global PMI is an absolute disaster. Anything below 50 is a contraction, so PMIs are firmly in contraction territory.

China PMI data is below, and it’s the lowest print ever recorded. Ever. Worse than the depths of the financial crisis. And this is the second largest economy in the world.

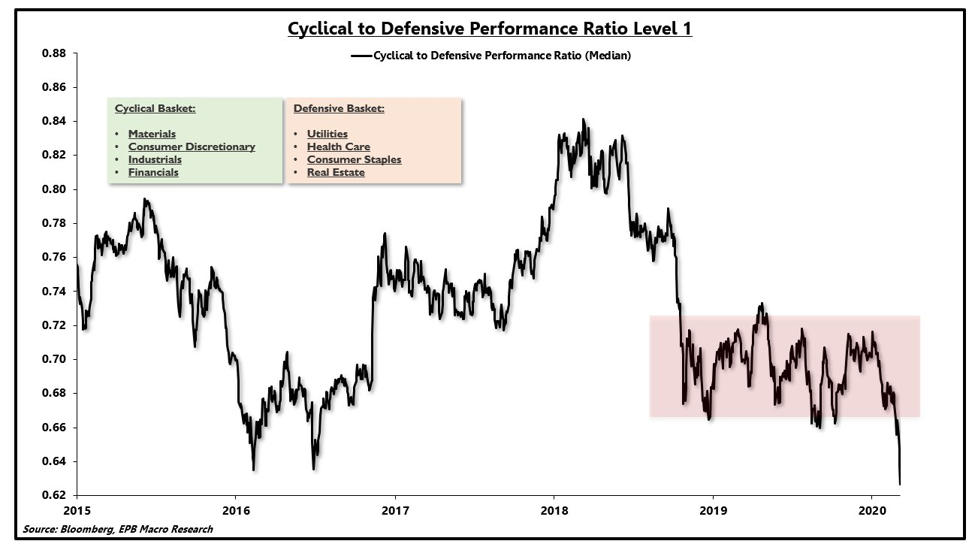

Stock market price action is also signaling possible recession, with cyclicals underperforming defensives. It’s not conclusive by itself of course, which is why we pair it with other data signals.

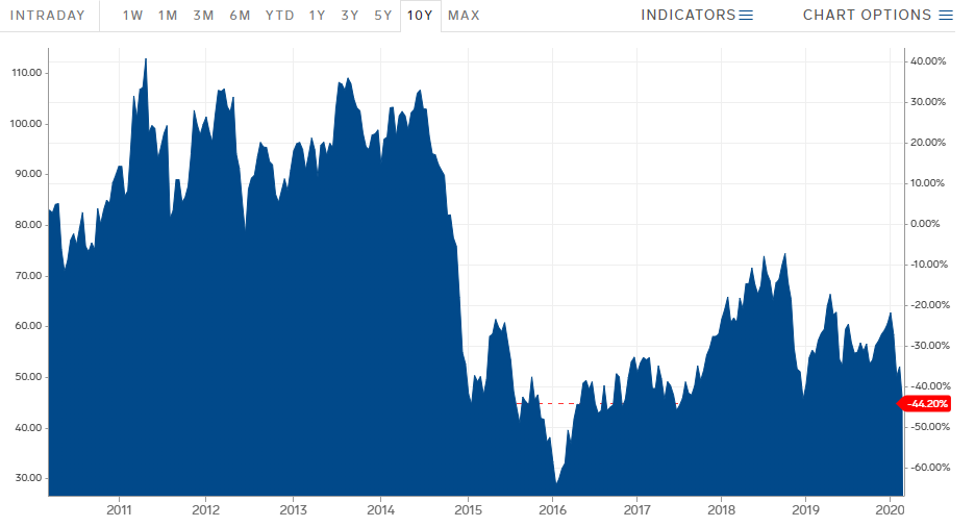

And if that’s not bad enough, the OPEC meeting yesterday ended without any decision on production cuts. This sent WTI Crude plunging to $42 per barrel. Without the production cut, and with a demand shock, oil probably goes even lower. And oil going lower is bad news for a lot of junk issuers in the US (Shale).

What happened the past week in COVID-19 news?

Remember last week we talked about watching COVID-19 – because it all flows back to the virus situation? And that financial markets and the Feds merely respond to it, not the other way around?

Well the game changer this week was the discovery of community transmission of COVID-19 in the US. Once the US started testing, they started discovering cases of COVID-19 among persons who have no recent travel history to any of the infected regions. This meant that community spread has been taking place in the US for a while now. That’s bad – because it means that that contract tracing is going to be tough, because it’s hard to locate the original source.

If you think about this logically, this means that the US will probably need to take deep and sweeping measures to curb the spread of COVID-19. It’s probably not going to be as big as China’s shutting down of the country, but over the past week we’re already starting to see mass cancellation of events, companies implementing work from home, school shutting etc. This probably accelerates in the coming weeks.

I have no doubt the US gets this under control eventually. This is the US we’re talking about, not a developing third world nation. The problem is the economic cost of the measures taken. The longer it takes, the bigger the impact.

Same logic for the Eurozone, Korea and Japan. To a certain extent Iran as well, but Iran is less plugged in to the global economy – so the economic impact from Iran is not as big at this stage.

Emergency Rate Cut from the Fed

Btw the framework that we set out last week to analyse COVID-19’s impact on markets remains absolutely valid. If you haven’t seen it already, it’s well worth the read.

All we’re doing today is simply applying the framework to what is going on, and watching the impact play out in financial markets.

So on Tuesday the Federal Reserve cut rates by 50 bps. This was notable because it was the first unscheduled / emergency rate cut since 2008.

For the record, I think the rate cut was the right move, because even before the cut US high yield spreads were already blowing out. If Feds had waited until the scheduled meeting on 17 March to cut, the tightening conditions would have done more damage. That said, the way they cut, and the communication to markets, probably could have been improved, but hey, it’s always easy to criticize when you’re not in the limelight. So I’m not going to judge here.

The problem though, is that when the Feds cut 50 bps, it never ends there. In almost every case (actually it’s probably every case from what I remember) after a 50 bps cut, the Feds go on to cut further after. I don’t see any reason why that won’t be the case here. I think rates are going a lot lower, really quick. We could be at zero by end of the year.

The problem is because rate cuts don’t solve the virus, which is a demand and supply shock. All the rate cuts in the world are not going to get you to go out of your house and go on a holiday. So the rate cuts merely set us up for the recovery phase once COVID19 is contained, and helps loosen financial conditions so firms with cash flow impact can tide this through until the demand and supply shocks go away.

The big difference between China and the US though – is that China can force its companies to do things, the US can’t. So China can force banks not to call loans, it can force airlines to fly with no passengers, it can force factories to reopen. The US with its political structure cannot do that.

What happens next?

Now regular readers of Financial Horse will know that I am not a pessimistic horse.

There are guys out there who are always calling for a market crash or a recession. And if you call it for 10 years in a row, there’s just going to be one year that you get it right.

So I’m not like that. I’m an optimistic horse by nature, always believing that tomorrow will be a sunny day. And I’ve never made a recession call in the history of this blog.

But today, this horse is starting to seem some clouds gather on the horizon.

I do want to emphasize that these things are not an exact science.

Imagine it this way. You’re playing a card game. The dealer has 3 cards left in his hand. Because you’ve been counting the cards, you know that there is a 66.6% chance the next card will be an Ace. So you bet big on it. The dealer opens. The card is a 2 diamonds.

Does that mean your original call was wrong?

Absolutely not. Your original call was absolutely correct, but you still lost on probabilities. That happens sometimes. It’s just how life works.

But was the decision to bet big correct? Absolutely. Because you had an outsized chance to win. If you make such bets systematically, in the long run you’ll make money. So as long as you don’t bet the house, and you’re able to keep playing, you’ll win longer term.

It’s the same thing with markets. It’s all about shifting probabilities.

Just because there is a high probability of a recession happening, doesn’t necessarily mean a recession will happen. That’s really important to understand.

Is this the start of a market crash? Will we see a recession or market crash?

With that out of the way, let me share that my base case has now shifted towards a global slowdown and recession in certain parts of the world in 2020.

Why the big change when just last week I was undecided?

I think the game changer the past week was the confirmation of relatively widespread community spread in the US. This would require them to take fairly drastic and sweeping measures to address the spread, at some point in the future (already happening). At the same time, the Eurozone, Japan and Korea are struggling to contain their own outbreaks. And China just emerged from their outbreak, and is struggling to restart. That’s basically the G7 economies right there for you.

2 big ways this impacts the economy.

Supply shock

2008 was a financial crisis, where the flow of money (credit) around the world froze up overnight. 2020 looks like a people crisis, where the flow of people around the world is going to freeze up.

Now people are a vital component in economic output (as labour), so when people can’t move, business activity and output drops.

The most obvious cases are manufacturing nations like China. Workers can’t get to work, factories shut, and output drops. China being shut for 1 month is going to cause supply chain disruptions across the globe.

The US though, isn’t like China where its primarily manufacturing driven. The US is more services and consumption driven.

But people being unable to move around the country also hurts a lot of business deals. No VC invests without meeting the founders in person first. No business owner does a big M&A without meeting in person.

Demand Shock

The airline, hospitality and tourism industry are going to be hit bad. It’s probably going to be worse than 2008 for them. And this is a big industry that hires lots of people. I expect lots of restructuring and asking crew to take unpaid leave in the coming months.

The oil sector looks like it’s going to be hit badly too. $40 oil isn’t going to cut it for many producers, and oil is probably headed lower. And unlike in 2015, it’s going to be tougher to raise credit this time. The oil sector affects lots of people’s livelihoods as well.

So that’s 2 big sectors that will be going through a rough patch simultaneously.

Then we have the global situation.

China’s reopening has taught us that the ramp-up after reopening is a slow one. When people go back to work, they’re still cautious, and they curb their spending. So a V shaped recovery looks unlikely here.

China’s services PMI plunged in February, and this may be repeated across the world soon. And don’t forget that services are not something that we’ll get back once COVID19 goes away. Think about it this way – All the restaurant meals you didn’t eat during this period because you were at home – are you going to eat them all back once the virus goes away? Probably not. So that’s real cash flow lost for the SMEs, that’s never coming back.

Same situation in Europe, but less dire (for now). Large parts of the economy are going to be shut over the next month or two. Think about all the lost revenue from closed doors football games, shut schools, cancelled conferences etc, that’s just never coming back.

Germany and Italy were on the brink of a recession before this, and I think this tips them over into recession. That’s going to be disaster for the European banks.

Any way to avoid a recession?

I think the one way that the above scenario fails to play out entirely, is if COVID-19 comes under control quick. Let’s say Japan, Eurozone, and the US manage to clear COVID-19 by end April, without taking drastic measures that hurt their economy.

Then maybe a coordinated monetary and fiscal stimulus from global central banks and governments avoids a global recession and slowdown.

Now I’m not a medical professional, but my read on COVID-19 so far based on observations and reasoning from base principles, is that COVID-19 is unlikely to go away that easily.

China had to shut their country for 2 weeks before the increase peaked, and then they persisted with the shutdown for another 2 weeks for good order. That’s how seriously they took this.

Hubei has been shut for about 1.5 months now, and we’re still seeing about 100 cases a day from family spread.

The containment here is going to be really tricky, and the US has only just started to ramp up testing.

I’m also worried about the less developed nations. Latin America, Middle East, Indonesia etc. I find it hard to believe that these nations have no problem on their hands, when the US and Eurozone are already in panic mode. It’s either these guys have fantastic healthcare detection systems (or no infected persons visit their country – which is unlikely), or more likely, they’re just not detecting the cases. And as we’ve learnt, the slower you react to COVID-19, the worse it hits you when it does.

Btw Sequoia just came out with a note to all startup founders telling them to hunker up for what is coming. This is one of the largest and most prestigious VC firms in the world, not ZeroHedge (I love you ZeroHedge, but your news can really be hyperbole sometimes).

And the last time Sequoia released a note like this? 2008.

What have I been doing?

I know that this reads like a pessimistic piece. In fact, I actually hope that the above doesn’t materialize, because the consequences will be dire.

But I’m a realist, and I need to interpret facts as I see them. And what I’m seeing is telling me that the risks of a global recession in 2020 have increased drastically.

Earlier on Monday, I penned a note to all Patron members saying that the coming stimulus rally could be used as a way to reduce equity positions.

Over the course of this week, after the brief rally in markets following the Fed emergency cut, I’ve been doing just that.

I’ve reduced equity allocation, and I’ve also taken the opportunity to derisk my portfolio and reposition more defensively. I’ve significantly reduced exposure in hospitality and cyclicals, and I’ve taken profit in certain other counters where I could. Of course, I haven’t exited completely because there’s always a chance I’m wrong.

Note: My portfolio is available on Patron (on a % basis) for those who are interested.

That said, short term the markets look too oversold. Nothing goes to hell in a straight line, and even if we have a global recession, prices are likely to still rally short term. That could be an opportune time to derisk, if one is so inclined.

Of course, what to do with your portfolio is up to you entirely. I could be wrong, and this could turn out to be the best buying opportunity since Dec 2018. I leave it up to you to decide.

Closing Thoughts

There’s an analogy in markets that I really like. It’s about picking up pennies in front of a steam roller.

It’s an image that has always fascinated me, picturing investors scrambling about hurriedly to pick up pennies for a profit, trying to avoid the steamroller and its fatal consequences.

It feels a lot like that to me now.

Sure, if COVID-19 goes away by April markets rally 10 to 20%. But if it doesn’t go away, all hell is going to break loose. Does the risk-reward make sense?

In particular, I’m very worried about:

- Eurozone banks – They just broke a 30 year trendline this week, and negative interest rates coupled with soaring NPLs spells disaster

- Energy markets – $40 oil is bad news

- Transport / Hospitality / Tourism – Global travel in 2020 is likely to be severely curtailed

And I’m worried about:

- Banks – Rates are likely to drop real quick from here on out, so banks are going to get hit with a double whammy of higher NPLs and lower NII – expect dividend cuts going forward. US Bank stocks (even big names like JP Morgan) are in a bear market, down 20% from highs. And I absolutely agree with this price move.

- Consumer discretionary – Discretionary spending is likely to get curtailed

- Commodity markets – Looks like a deflationary bust may be coming

But hey, let’s hope I’m all wrong about this. Let’s hope that in 2 months time, Financial Horse turns out to just be a hyperbole horse. I’m actually hoping that this happens.

Whether you think I’m right or wrong, and what you choose to do with this, I leave it up to you entirely. My only ask – if you agree with me, share this article. Share it with your friends or family who invest. Let’s get the information out there. I don’t want any unwitting investor to get caught up in what’s about to happen. These are real people, with real livelihoods and savings on the line. Share the information with them, and let them evaluate for themselves on the right action for their portfolio.

As always, this article was written on 7 March, and will not be updated going forward. My latest thoughts are always shared on Patron for those who are interested.

What do you think? Am I overreacting?

I welcome all thoughts and sharing here. What am I missing? Share your comments below!

Do like and follow our Facebook Page. We share great links and infographics there.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Join our Facebook Group to continue the discussion, we have a great community of people who want to help each other become better investors. Everyone is welcome!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors. We genuinely think it’s the highest quality and best value investment course out there today!

I too agree there will be a recession. I just do some accumulation like OCBC, Far East HT, and HL Fin

Thanks for sharing!

Hi oppa!

When the US companies start to progressively announce their earning reports in the upcoming months, will the stock prices fall even more? Or has the expected fall in earnings been factored in already?

In other words… Some stocks which I am interested in have already fallen in price. Will they fall even further as we know that the ongoing virus situation will be having an impact on their earnings?

Good question, wish I knew the answer! You will need to analyse each stock individually, there will not be a blanket answer to this question. Some stocks may have fallen too far, and some stocks may have barely even started the fall.

Excellent write up, I couldn’t agree more. Curious to learn about your hedges, I’ll look that up on Patreon. Thanks FH!

To be clear I don’t think a recession is a done deal, it’s just that latest evidence has tipped the balance of probabilities in favour of a recession for now. Who knows – in 2 weeks it could be clear that COVID-19 is a non-issue. 😉

Hey FH! Great article!

You mentioned in a previous article that a good time to buy the dip is 2 weeks after drastic actions are taken by countries to curb the virus. Does it still stand with your current stance that a recession is incoming?

Yes – no change to buy signal. I will probably adjust the time I use to average in (after buy signal triggered), because this doesn’t look like a V shaped recovery for now. But let’s see, if governments can clean this up quickly, things can still rebound v quick.

To add – the longer this drags on, the greater the damage to the underlying economy, and the slower the recovery. That said, I still think this is ultimately a COVID19 issue, so once the virus goes away, the problem goes away, and we move to recovery phase. The problem is that it doesn’t look like govts will get a grip on this so quick.

Thank you for the reply! Big fan of your articles here!