Balloting results for Digital Core REIT IPO are out!

The full SGX announcement is here, but I’ll summarise quickly and share my takeaways.

Digital Core REIT IPO Balloting Results

Placement Tranche

The placement tranche for Digital Core REIT IPO was 253,682,000 Units (US$223 million).

It was 19.6 times subscribed.

All of the over-allotment units (53,406,000 units) went into the placement tranche.

That’s a very strong performance.

Public Offer / Retail Tranche

The public offer / Retail tranche was 13,352,000 Units (US$11.7 million).

Public offer was 16.1 times subscribed.

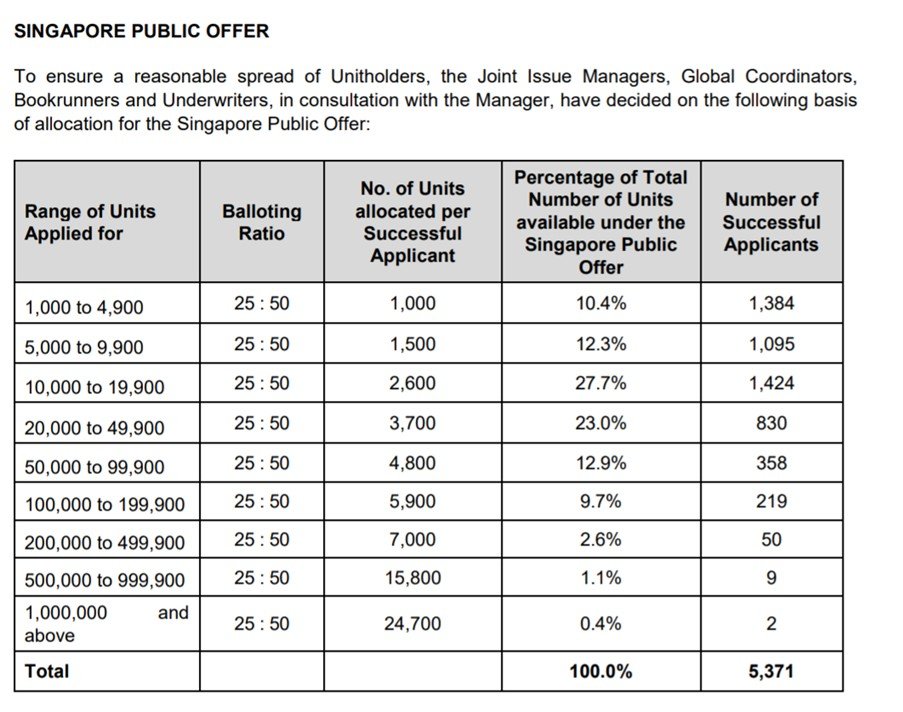

Balloting table is below, and to sum up:

- The bulk of the units went to the (1) 10,000 to 19,000 and (2) 20,000 to 49,000 units tranche

- 50% chance of getting 2,600 units (US$2,288) if you applied in the 10,000 to 19,0000 tranche

- 50% chance of getting 3,700 units (US$3,256) if you applied in the 20,000 to 49,9000 tranche

So 50% chance of getting across all tranches, exactly the same as Daiwa House Logistics Trust.

Maybe this is the new way of allocating IPOs.

Debrief of Digital Core REIT IPO

Results are very strong indeed.

The placement tranche being 19.6 times oversubscribed is a very strong show of confidence given the Daiwa House Logistics Trust IPO was only 4.9 times oversubscribed for the placement tranche.

Don’t forget the placement tranche for Digital Core REIT is bigger than that of Daiwa House Logistics Trust.

Public offer at 19.6 times subscribed is also quite a fair bit stronger than Daiwa House Logistics Trust IPO which was 9.5 times subscribed (although Daiwa House had a bigger public offer).

For me, I applied in the 20,000 to 49,900 range and I got 3,700 units, which isn’t too bad actually.

Trading commences on Monday at 12pm, would be interesting to see how Digital Core REIT trades post-IPO.

In case it wasn’t clear, my review of Digital Core REIT IPO was assuming a buy and hold investment.

REIT IPOs can’t really be used to flip these days, they are more as long term buy and hold yield instruments. And given how small the allocation is, you don’t make much even if it pops.

Criticism of Digital Core REIT IPO from another Blogger

An FH Reader shared the following article with me in the FH Telegram Group, titled “Why you should avoid Digital Core REIT IPO”.

I always welcome contrary opinions, so please do not hesitate to share such things with me.

To sum up the article, the writer argues that Digital Core REIT has:

- Poor upside in the short term due to locked in lease (6.2 years WALE)

- Low returns for Data Centre Asset Class

- High fees compared to Keppel DC REIT

- Poor record of US REIT listing

I’ll leave it to readers to decide if you agree with the blogger, but some comments from me are as follows:

1. Poor upside in the short term due to locked in lease (6.2 years WALE)

Yes but that’s how longer leases work.

Think of it this way, if you have a condo, and you decide to sign a 6-year lease instead of a 2 year lease.

The bad part is that if rental rates go up during the 6 years, you can’t benefit.

The good part is that if rental rates go down, or if vacancy rates go up, you’re protected because you already locked in the tenant and the price.

So long leases are a double edged sword, and this is working as intended.

For what it’s worth, data centers are supposed to be a stable asset class, kind of like a fixed income proxy.

So to me this is good.

I have enough risk in the rest of my growth portfolio, I don’t need my REITs to trade like a meme stock.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

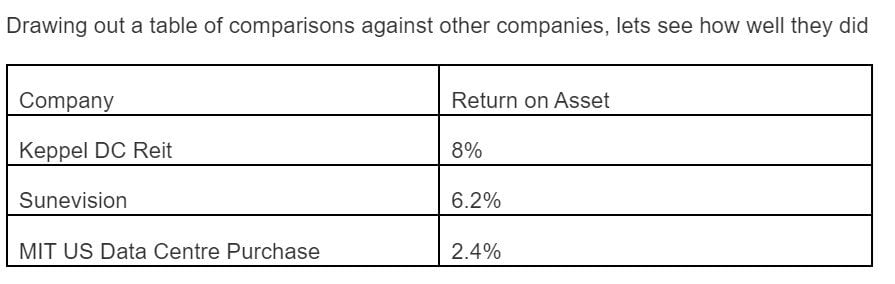

2. Low returns for Data Centre Asset Class

Writer compared the 4.5% return on assets for Digital Core REIT against other data centre REITs:

Real estate is a local business though, so the data centres for Digital Core REIT can only be compared with other US data centres.

Not fair to compare European data centres with US data centres, just like you can’t compare a house in Malaysia with a house in Singapore.

If you look at the numbers that Mapletree Industrial Trust used when acquiring US data centre assets, they are also in a similar range.

Likewise the big boy US data centre REITs like Digital Realty and Equinix are trading at 2-3% yields.

Sure you can argue that US data centres as an asset class are overvalued, but you could also argue the same for most asset classes today.

3. High fees compared to Keppel DC REIT

Not a fair comparison to use Keppel DC REIT as a benchmark because Keppel DC REIT’s assets are not in the US.

Cost is different for each country, and each location.

You can also argue that each sponsor has a different value add (and accordingly cost). This is not a commodity business.

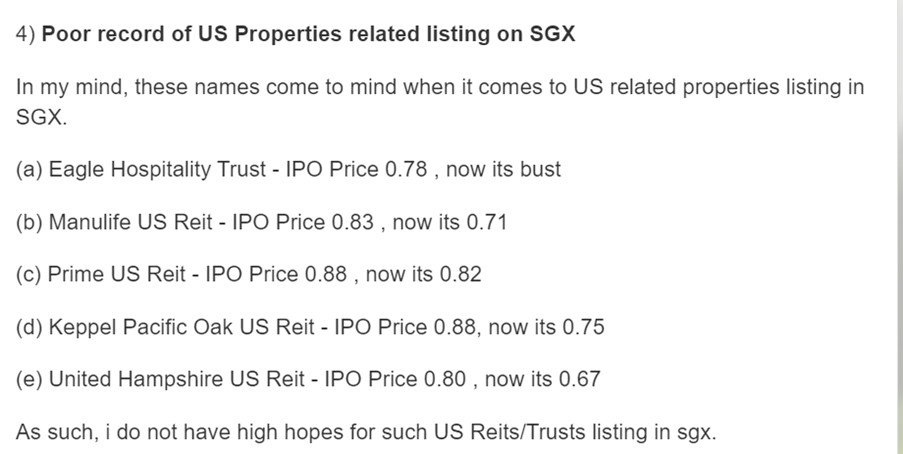

4. Poor record of US REIT listing

You can see the numbers below:

Don’t disagree with this.

US REITs have had a pretty bad track record on the SGX so far.

You could argue some of it is due to COVID, but I think the REITs need to take some of the blame too. Some of the other US REIT have really not done well.

But ultimately, each REIT needs to be evaluated on its own merits.

In any case, I always welcome alternative opinions, helps me to avoid blind spots.

It’s what makes a market after all.

Love to hear what you think! Did you subscribe for Digital Core REIT IPO?

As always, this article is written on 3 Dec 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with and fund $2000.

Get 1 free Apple share (worth $200) you’re new to and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

So how long do you plan to hold this for? What do you think will be the dividend payout?

Same as with my other REITs. Will hold until the fundamentals change, when I need the cash, or when I think they are overvalued.

Whether a long WALE is good is a function of future rent expectations and the manager’s ability to secure strong future rental reversions.

True, agree with this.

Agree. A dovish & contrarian set of views is required to ensure the market stays strong, stable and growing. Right now, the scales are heavily tilted to dovish.. hence a return to mean will be an impending disaster.

I also managed to get a small allocation. Congrats fellow shareholder!

Don’t quite understand why a REIT IPO is not meant to be a flip though. Cuz most of the value is extracted via a longer-term time horizon in your view?

Because these are in a way fixed income proxies. You can flip them for maybe a 5 – 10% capital gain if you’re lucky, but based on the allocation amount that’s not a productive use of the time.

Whereas if you hold longer term, you can get the distribution gains + capital gains, which to me is the point of the REIT. Of course if your goal is to just flip it, don’t let this article stop you!

I see I see. No.. planning to hold it until the point where the valuation isn’t attractive hah.. Simply curious on the thinking. Thanks!

What do you think is a good price limit for it to be worth it to pick it up in the open market?

Once it starts trading you will need to look at the technicals – opening price, post-IPO price action etc to make the decision. Not just on fundamentals alone.

Before IPO we dont have all this info, hence it was a pure fundamentals based analysis.

How is it that I subscribed to 50,000 – 99,900 range but I got zero allocation?

It’s a 50% chance to get allocated, so guess you were unlucky. 🙂

Hi, do you recommend collecting dividend in SGD or USD for this counter? Will there be any disadvantage if choose SGD for convenience? Also what will you choose?

Well it really depends on personal preference.

You can take the USD if you plan to use the USD for other reasons. Or if you dont want to bother with the hassle you can just accept SGD.

Usually I just take SGD as I can’t be bothered with the hassle of USD for such a small amount.

If you do elect to take USD, do note to follow up with CDP so they don’t auto convert the USD to SGD for you. You can refer to the steps here: https://www.sgx.com/cdpfaqs