As some of you may know, my belief is that active investing may outperform passive investing this decade.

So when Saxo reached out to collaborate on a post on active investing, I was happy to share my views.

If I had $1 million to invest for the rest of this decade.

Adopting an active, multi-asset strategy, that is geographically diversified as a Singaporean investor.

How would I invest that money?

For this article, these are the guidelines I used:

- Active asset allocation strategy

- Multi asset (includes global equities, options, FX etc)

- Geographically diversified

Disclosure: This post is sponsored by Saxo. All views and opinions expressed in this post are from Financial Horse.

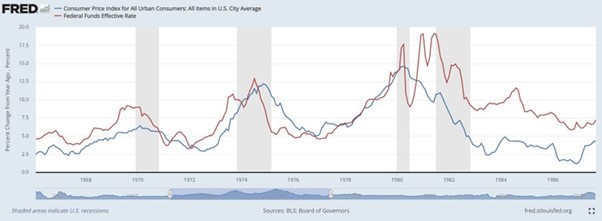

Why Active investing may outperform Passive this decade? Regime shift in Financial Markets?

Take a look at the long term chart of interest rates below.

Interest rates have been structurally going lower for the past 40 years.

And if you look at the chart below, you’ll realise that trend ended in 2020.

After 2020, for the first time in 40 years – interest rates have gone higher this cycle, than they went in the past cycle.

In other words – it’s possible that everything we knew about investing from the past 40 years, was because you had the tailwind of declining interest rates.

All of which may change going forward.

You hear about how investing greats like Stanley Druckenmiller think the S&P500 might be flat by the end of the decade (after volatile moves up and down this decade).

The 1970s played out this way.

Every time the Feds cut interest rates – inflation roared back, requiring a second tightening cycle.

It took 3 waves of tightening in the 1970s to end inflation for good, during which stocks went on a roller coaster ride.

Based on what we know today, you can’t rule out something similar happening this decade.

No doubt inflation is going down, but for inflation to stay down is not so straightforward.

Look at how speculative markets like Bitcoin are close to all time highs, and you get the sense that once the Feds actually start to cut, inflation may roar back.

So while the 2010s decade was just about capturing broad market exposure via passive ETFs – because the Fed QE and zero interest rates lifted all asset prices.

This decade looks very different.

This decade looks like one where there will be significant interest rate and inflation volatility – with lots of ups and downs in asset prices.

My view – I think this will be a golden decade for active investing, especially global macro investors.

How I may invest $1 million in 2024 – US Stocks, S-REITs, Commodities? (as a Singapore Investor)

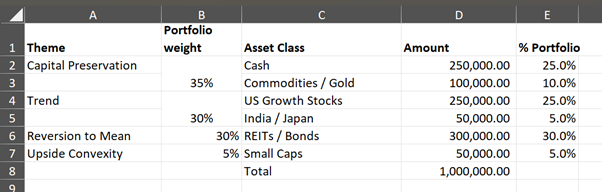

High level asset allocation for a more active investing strategy

If you want to build an active portfolio.

Broadly speaking, you want exposure to the four big quadrants of asset classes:

- Trend (momentum)

- Reversion to mean

- Upside convexity

- Capital Preservation

In investing – you always guard your risk first, and the upside will take care of itself.

So let’s start with capital preservation.

Capital Preservation – How much cash to hold as a Singapore Investor in 2024?

The million dollar question (no pun intended) is how much cash do I hold, vs how much do I invest.

Ultimately – that’s a question each investor needs to answer for himself.

Personally for this portfolio.

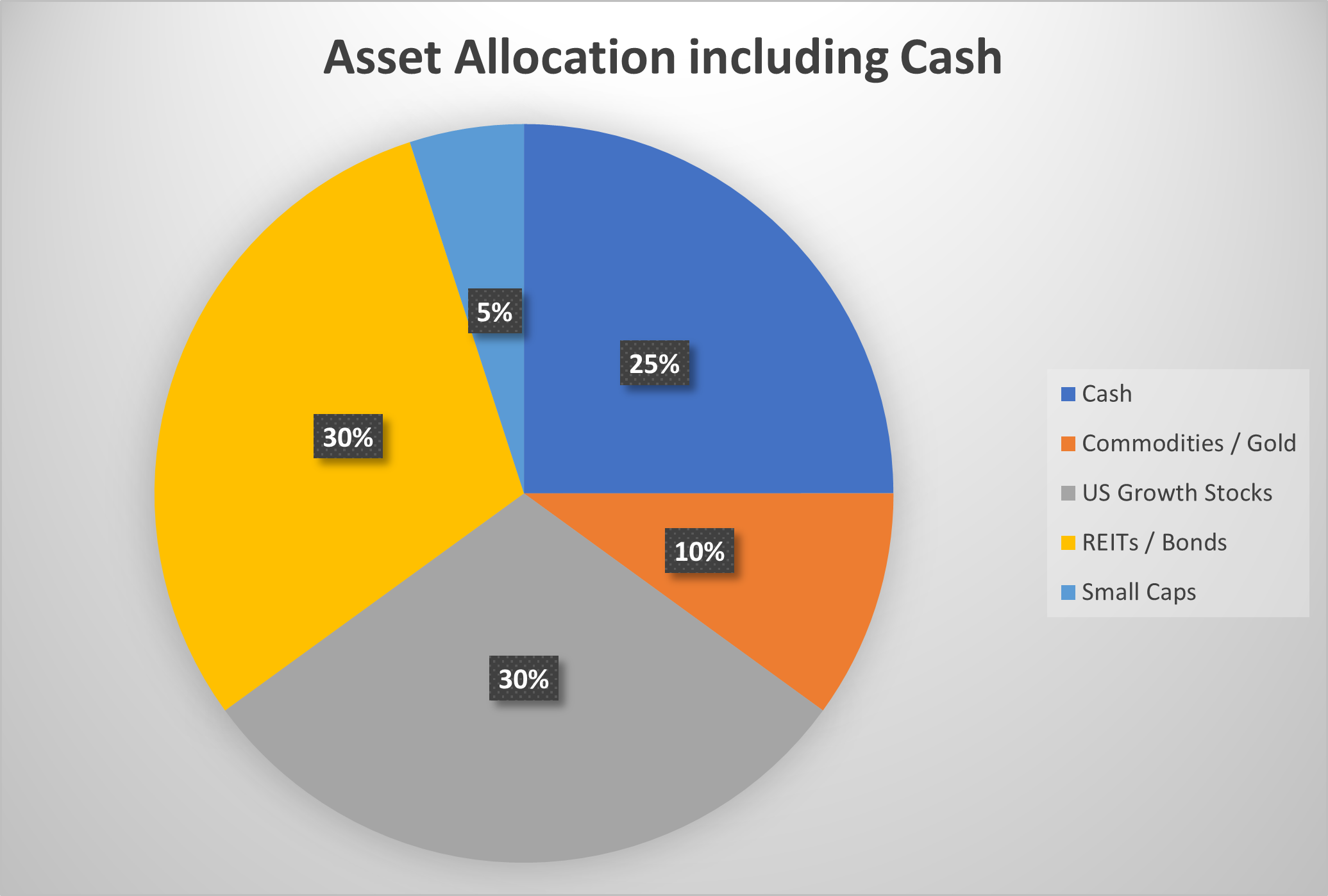

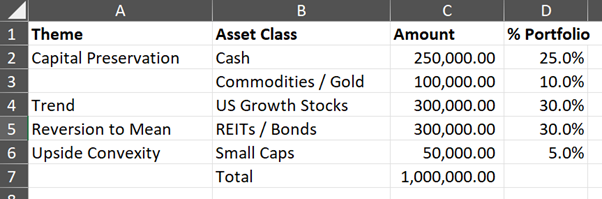

I settled on $350,000 allocated to capital preservation (35%).

$250,000 would be parked in cash – spread across T-Bills or money market funds.

When T-Bills are paying 3.80% risk free, and SGD money market funds pay close to 4.0% yields, and with global macro uncertainty, I want to allocate more cash this decade than I did the last decade.

Can commodities / gold preserve capital for Singapore Investors?

The remaining $100,000 I would park in a mix of commodities or gold.

I did think long and hard whether commodities / gold has a place in this portfolio.

The problem with cash is that if I am right, this decade is going to see structurally higher inflation.

And while cash pays a juicy 4% yield, just take a look at prices out there and it’s painfully obvious that “real inflation” (being prices I actually pay for a basket of goods).

Has gone up more than 4%.

And we’re not even at the phase of the cycle where the real money printing starts.

So ultimately, my answer was that yes I wanted the allocation.

Commodities / gold may suffer in the short term, but I wouldn’t be comfortable running zero exposure.

How to invest in Commodities as a Singapore Investor?

In the commodities space I like oil, copper, and Uranium.

Oil – perhaps Exxon Mobil or Chevron in the US, or London listed Shell for no withholding tax on the dividend.

Copper – perhaps US listed Teck Resources or Freeport-McMoran.

Uranium – an ETF like URNM, or the biggest miners in US listed Cameco or London listed Kazatomprom.

The more adventurous investors could consider commodities futures, which you can access via Saxo.

Gold – Why I like both Gold and Commodities

I know many investors think Bitcoin is the superior version of gold today.

But I would see Bitcoin more as a momentum play.

Whereas Gold is more of a capital preservation play.

Personally I see an argument for owning both.

In a climate where the US can confiscate all your USD assets overnight, gold is one of those no-brainers for central banks looking to diversify away from USD.

How to own gold?

Physical gold if you see yourself holding for the next generation, an ETF like iShares Gold Trust (IAU) for cheaper transaction costs.

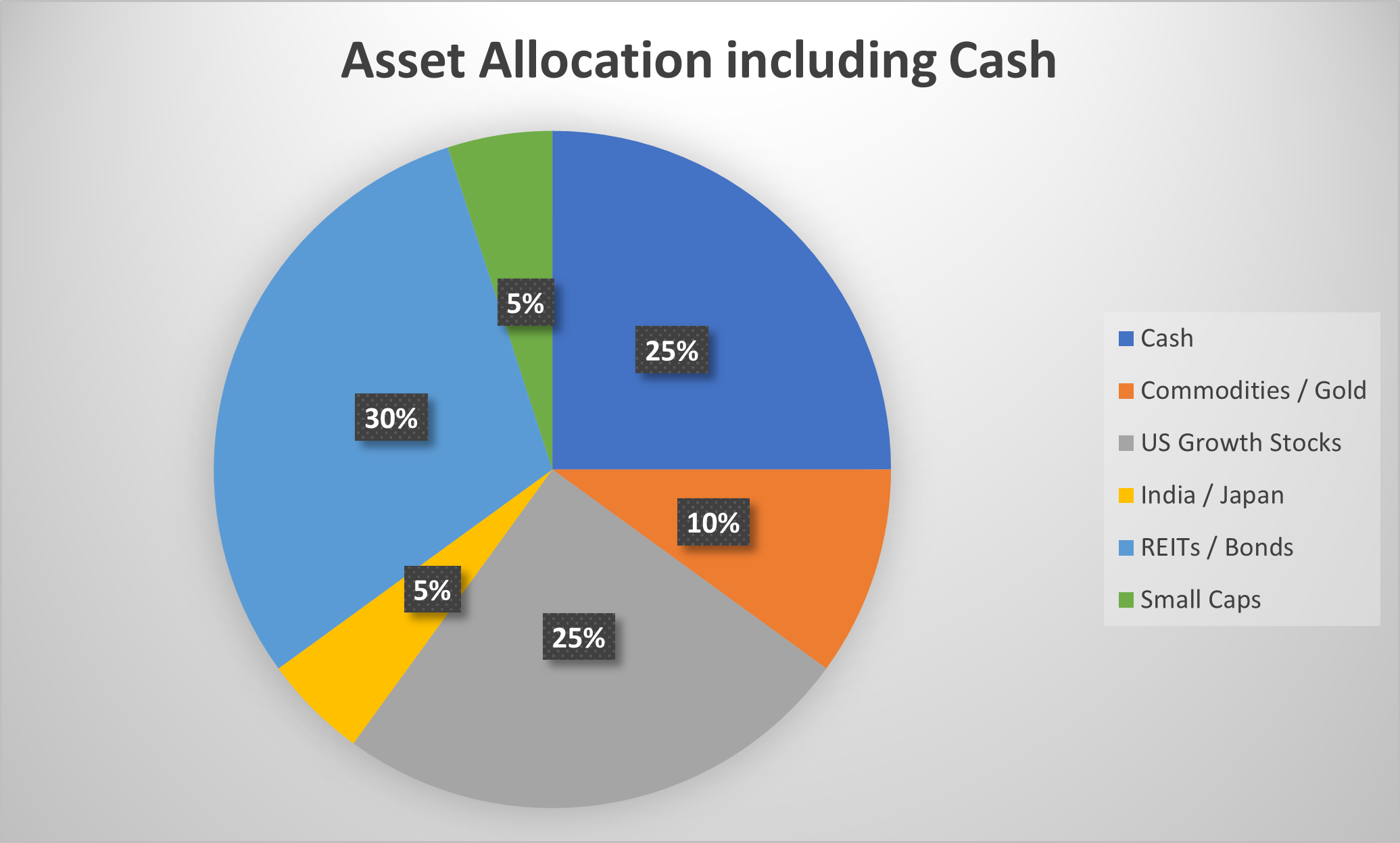

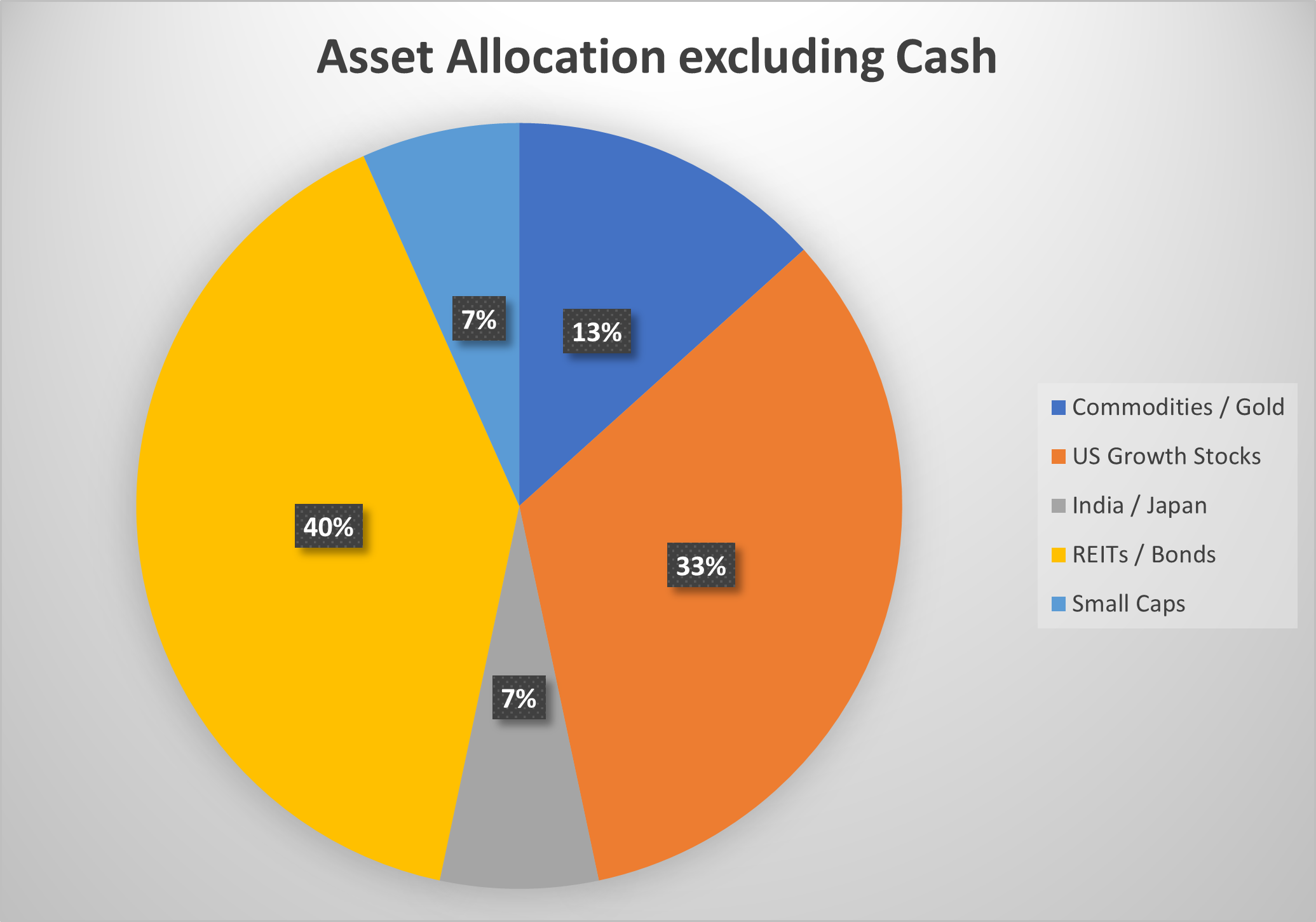

How I will invest $1 million in 2024 – Asset Allocation excluding Cash?

I know some investors think that the $1 million portfolio should exclude cash.

So for the record – this is what asset allocation looks like once you take cash out:

Trend – Buy US Momentum / Growth Stocks as a Singapore Investor in 2024

The 2 biggest buckets of risk in this portfolio are – Trend (US Growth), and Mean Reversion (REITs / Bonds).

Let’s discuss the first bucket.

These are broadly

- AI stocks (eg. NVIDIA, AMD, Microsoft)

- FAANG

- GLP-1 (eg. Novo Nordisk, Eli Lilly)

- India / Japan

AI Stocks / US Tech has very strong momentum – but how will this end?

NVIDIA – the poster boy of the AI rally, is up 92% this year alone.

The problem when a stock goes parabolic like that.

It almost never ends with the stock going sideways.

The way it ends is that the stock goes up until there are no more buyers, and then it goes down.

As a passive investor, maybe you just buy the S&P500 and sit out the stock picking.

As an active investor – you need the exposure, but be careful of a reversal

But with an active strategy, the momentum is exactly what I want to get exposure to.

But I need to be very, very careful with the inevitable reversal.

Exit too early and I miss out on big gains.

Exit too late and I give up all my gains.

Timing the top exactly is a fool’s errand, so I’ll likely try to sell in tranches on the way up/down.

Other AI stocks will include names like Microsoft, AMD, Micron etc.

But I expect all of them to be highly correlated.

If NVIDIA goes down, they probably all go down.

GLP-1 Stocks have very strong momentum too

The other area with a lot of strong momentum, is the whole area of GLP-1 stocks.

For those of you who’ve heard of the weight loss drug Ozempic, this is exactly it.

This is a new class of drugs that was first approved to treat diabetes, before the world has discovered that they can be used as a weight loss drug.

Demand has been explosive – literally the creation of an entirely new industry (not that different from AI – with similar results in stock price).The 2 biggest names in this space are Copenhagen listed Novo Nordisk (which you can access via Saxo), and US listed Eli Lilly.

Charts for both below, they’re not too different from the parabolic AI charts above.

So if I want some diversification from AI, yet want exposure to strong momentum – this might be it.

That said the way these markets trades today, I have a nagging suspicion that if the AI rally ends, GLP-1 stocks may not be immune too.

India or Japan ETFs are another option to consider for strong momentum in 2024

What if you wanted some diversification from US growth stocks?

And yet you wanted exposure to a sector with very strong upwards momentum?

Here’s Japan’s TOPIX index – up 41% the past 12 months.

Alternatively, here’s India’s Nifty 50 Index – up 28% on a 12 month basis:

There has been a lot of capital outflow from China, and India and Japan are the 2 markets in Asia large enough to absorb all that flow.

While both countries, being US allies, are benefitting from the “friendshoring” movement as MNCs derisk from China.

How long can this rally continue?

I frankly don’t know – if it’s a structural run these things play out over years.

But just like with all momentum plays.

You can buy the US listed ETFs (iShares MSCI Japan of MSCI India), or the local listed ETFs (iShares TOPIX ETF listed in Tokyo).

The more adventurous can even stock pick individual names in India / Japan.

Saxo can provide you direct trading access to all of these markets.

Reversion to Mean – Buy S-REITs as a Singapore Investor in 2024

Whereas the trend basket above is all about buying stocks that are high but going higher.

The reversion to mean basket is about buying stocks that are very low – in the hopes that they bounce back.

As a Singapore investor, the big standout in this segment is – REITs.

Buy Singapore REITs for the $1 million portfolio?

Here’s Keppel DC REIT for example, the chart since 2021 has not been pretty.

As shared in recent articles – Personally I like the risk-reward for REITs at this point in the cycle.

The difference between REITs and momentum stocks – is that with REITs (a) valuations are much cheaper, and (b) I get paid a dividend.

The more REITs sell-off, the higher the dividend yield goes, which theoretically should provide some downside protection.

And if we do get interest rate cuts in the next 18 months, that’s just going to be icing on the cake.

What Singapore REITs I may buy for this $1 million portfolio?

I want to stick to REITs with strong underlying real estate, good sponsor backing, and primarily Singapore exposure.

It’s hard to call what would happen to US or European real estate the next few years, so I want to stick primarily to Singapore real estate.

Strong balance sheet matters too – although most of the S-REITs today run very high effective leverage at >40%.

As long as the REIT avoids any refinancing problems and hangs in there, there is a chance of capital gains on the other side of the rate cut cycle.

REITs I like include:

- Keppel REIT

- Lendlease REIT

- Starhill Global REIT

- Mapletree Pan Asia Commercial Trust (MPACT)

- CapitaLand Integrated Commercial Trust (CICT)

- CapitaLand Ascendas REIT

- Keppel DC REIT

You can read more of my views on REITs in this article.

Would I bet on interest rates going down in 2024/2025?

Another trade that I made in 2023 was call options on Treasury ETFs (TLT), as a way to bet on interest rates going down.

This trade played off well in 2023 when US 10 year yields went from 5.00% to sub 4.00%.

Where we are today, with the US 10 year at 4.1% I don’t think the risk-reward makes sense on this trade.

But if the 10 year goes above 4.5% this year, I may well put on this trade again using Jan 2026 call options on the TLT.

If the 10 year doesn’t go there, maybe I just buy REITs instead, as a proxy play on lower interest rates – while getting paid a dividend yield while I wait.

Upside Convexity – Buy stocks with high upside potential

Upside convexity is basically risking $1 to make $5 – $10.

No doubt this portion of the portfolio is meant to be highly risky and high probability of capital loss.

Which is why it is sized at only 5% of the overall portfolio:

The big category that comes to mind is small cap stocks.

Buy Small Cap Stocks as a Singapore Investor?

Because of the nature of these names, I don’t want to delve into specifics.

Just as an example, there are a lot of small mining companies and oil & gas companies listed in the US/London with a few hundred million to a few billion market cap.

Investors who are keen to invest in this industry are looking at a 3x to 5x return, if things go right (but of course, things can also go wrong).

For an active investing strategy, I may allocate a small amount into small cap stocks for upside convexity.

You don’t lose much if you’re wrong, but you make a lot if you’re right.

How I may invest $1 million in 2024 – Buy US Stocks, S-REITs, Commodities, T-Bills? (as a Singapore Investor)

I do want to caveat again, that this is meant to be an actively managed portfolio.

So while there is a high cash allocation at 25% that provides some stability.

The other large pillar of risk management comes in the form of active management.

The market may be in risk-on mode (although this may have changed the past few days/weeks).

But it doesn’t take a lot for all that to change.

A weak US unemployment number, a NVIDIA earnings miss, stronger than expected inflation – any of those can derail the current rally.

With this portfolio, almost 75% of the portfolio is allocated to risk assets that can swing wildly if there is volatility in capital markets.

And I would be watching the macro closely, to decide when to take profit in that 75%, or when to rotate into other asset classes.

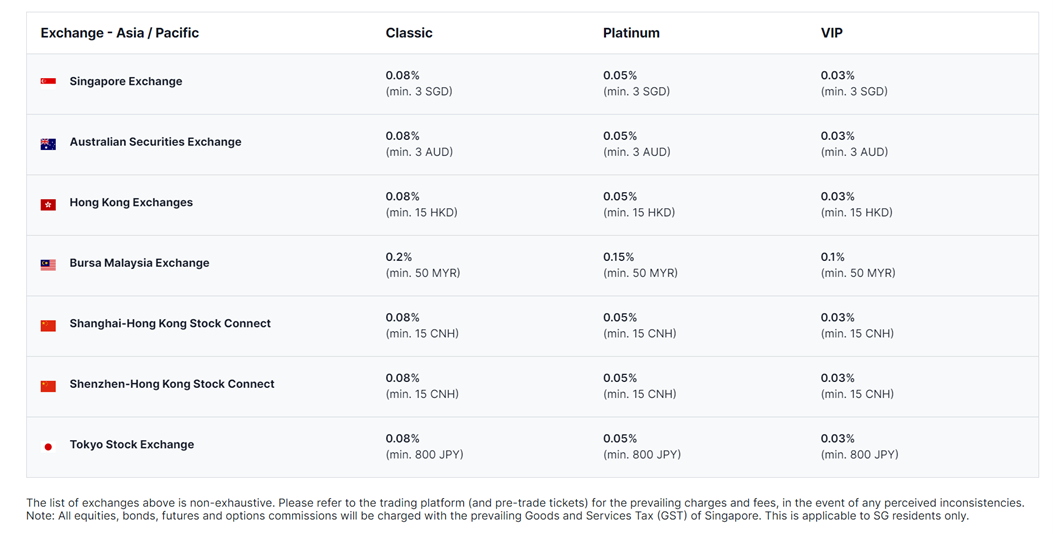

Saxo’s new simplified pricing (effective 4 March 2024)

Saxo has just released a new simplified pricing structure.

Fees as low as 0.08% (minimum 1 USD) for US trades, and 0.08% (minimum 3 SGD) for SGX trades.

No hidden charges – no platform fee, no custody fees (when opted into securities lending).

Earn interest on uninvested cash.

With market-leading competitive FX rates of 0.25%.

And access to almost any exchange you could want – US, London, Europe, Canada, Singapore, Australia, Hong Kong, Malaysia Tokyo and more.

With the recent revamp, Saxo’s pricing is now very competitive. When you take total trading costs into consideration, Saxo is can be even cheaper than low-cost brokers.

Saxo also offers margin lending if you wish to get leverage on your stocks and ETFs, and they have also improved margin lending rates with their new pricing

I really like the new simplified pricing, and may use Saxo as one of my main brokers moving forward.

Sign up for a Saxo account here.

Saxo Sign up Promotion (until 30 June 2024)

New users can also get a free upgrade to platinum – this means even cheaper fees and the opportunity to earn interest on uninvested cash.

All you need to do is fund a minimum of 1 SGD from now until 30 June 2024.

You just need to:

- Open a new account

- Fund at least SGD 1 from now until 30 June 2024

This promotion also applies to users who previously opened a Saxo account but have not funded it.

So those of you who already have an account, but have not funded it, this is the time to act!

Sign up for a Saxo account here.

Terms and conditions apply.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor. Past performance is not necessarily indicative of future performance.

So commodities as an inflationary hedge right?

Why copper though? Is gold not sufficient?

Gold / Commodities are slightly different – there are certain conditions where gold would do well and commodities would not, and vice versa.

Personally I would probably own both, the only question is how much allocation to each.

Great post, thanks.

Am aware this is a sponsored post. Some good valid takeaways which is much appreciated and yes, this is a portfolio that needs to be managed actively and not merely to be left dormant. Was talking to an insurance agent friend of your above post and she said to allay any fears of managing the portfolio or concerns that interest rates may go up/down, she suggested buying an annuity using the $1 mil, thereby getting a regular income stream yearly and best of all, a death benefit that will preserve/grow the capital. She said it’s a kiasu-sure win approach and guaranteed won’t lose money. Would like to get your thoughts pls.

Well leaving aside the obvious point that asking an insurance agent where to park your cash is a bit like asking your barber if you need a hair cut (not to mention there is some conflict of interest given they earn the highest commissions on certain products).

I think the problem with an annuity is what investment returns are you going to get (net of fees)?

Did the friend share what kind of investment returns you would be looking at for the life of the annuity? And is it guaranteed (risk free), or does it depend on market conditions (ie. it can fluctuate).

Much will depend on the answer to these questions.

Great analogy – had a good laugh over it. RoR is industry standard 3.55% pa which is easily out rivaled by other financial instruments and investments. If it’s a windfall, I like to be able to use some of the money rather than lock it in the annuity (as bad as CPF). Thanks for the tip!

Ah I see, 3.55% is indeed on the low side.

I mean not saying it’s a bad product, but it really depends on what you’re looking for as an investor. Do you want the protection / safety, or do you want the returns.

Tx for yr article again. On reits, I intend to buy now when it’s low and sell when it’s higher. The profit will be spread over x years before re entering into reits again for the dividend. What is yr advice on a safe x when planning on this strategy?

I think that’s the wrong way to approach this question.

The question should be at what point does the risk-reward for holding REITs no longer make sense (at which point you can consider selling). And if you sell, where does the cash go into instead, for more attractive risk-reward.

Because it doesnt matter what you want, the market will still play to its own tune. Better to adjust your thinking to suit the market.