In last week’s article, I discussed an asset allocation with about 40% allocation to REITs.

The comments I got was… interesting:

“REITs can make money meh?”

“Buy REITs? Ask those who bought 3 years ago how much they lost.”

Investing is funny sometimes.

In 2021, when REITs were at all time highs – investors loved REITs.

Today when REITs are close to all time lows – nobody wants to touch REITs.

And everyone wants to buy banks when they are close to all time highs.

If there’s anything I’ve learned in investing.

It is that:

When the market is overwhelmingly bearish on an asset class, it’s worth taking a second look.

When the market is overwhelmingly bullish on an asset class, you’d better take a second look.

How I may invest $100,000 in REITs? (as a Singapore Investor in 2024)

So I wanted to use this article to relook my assumptions about REITs.

And to ask if I had $100,000 today.

Would I still use that money to buy REITs?

And if so, how?

What is the key risk for REITs today?

The key risk for REITs today is without a doubt – interest rates.

I’ve plotted the Nikko AM REIT ETF against the Singapore 10 year yield (inverted – orange) below.

You can see how REIT pretty much trade inversely to interest rates (although the past week or two this seems to have diverged).

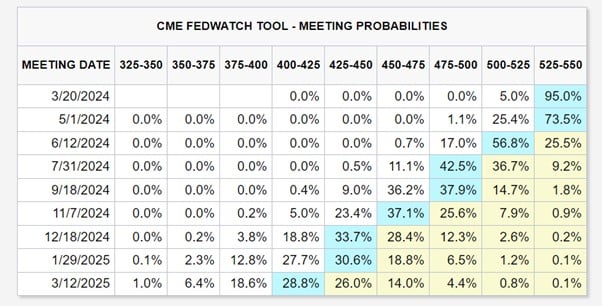

What are the possible futures for short term interest rates?

Let’s game out the 3 different scenarios moving forward (for short term interest rates):

- Interest rates go even higher

- Interest rates stay here for the next 12 – 18 months

- Interest rates go down

Based on what we know today, I think Scenario (1) is unlikely.

Jerome Powell has pretty much said he plans to cut rates in 2024, the uncertainty is over when exactly.

It’s not impossible of course, but you would need very bad inflation, and a very bold Jerome Powell in an election year.

More likely you’ll see either Scenario (2) or (3).

Is it possible for interest rates to stay high for the next 12 – 18 months?

The market is pricing in Scenario (3), with 4 interest rate cuts in 2024.

But I would hardly say it’s a done deal.

Look at how speculative markets like crypto are running rampant – and it’s fairly clear that financial conditions are very loose today.

Imagine Jerome Powell cuts interest rates on top of that.

That’s going to pour gasoline on the fire, and we may have a full speculative bubble on our hands.

Once that happens – how long before inflation comes back?

So I do think there is a risk of Scenario (2).

How would REITs perform in Scenario 2 – if interest rates stay high for the next 12 – 18 months?

Back in 2022 many of you asked me whether rental increases would be sufficient to offset interest rate increases for REIT.

My answer was no – because of how rapid interest rate increases were.

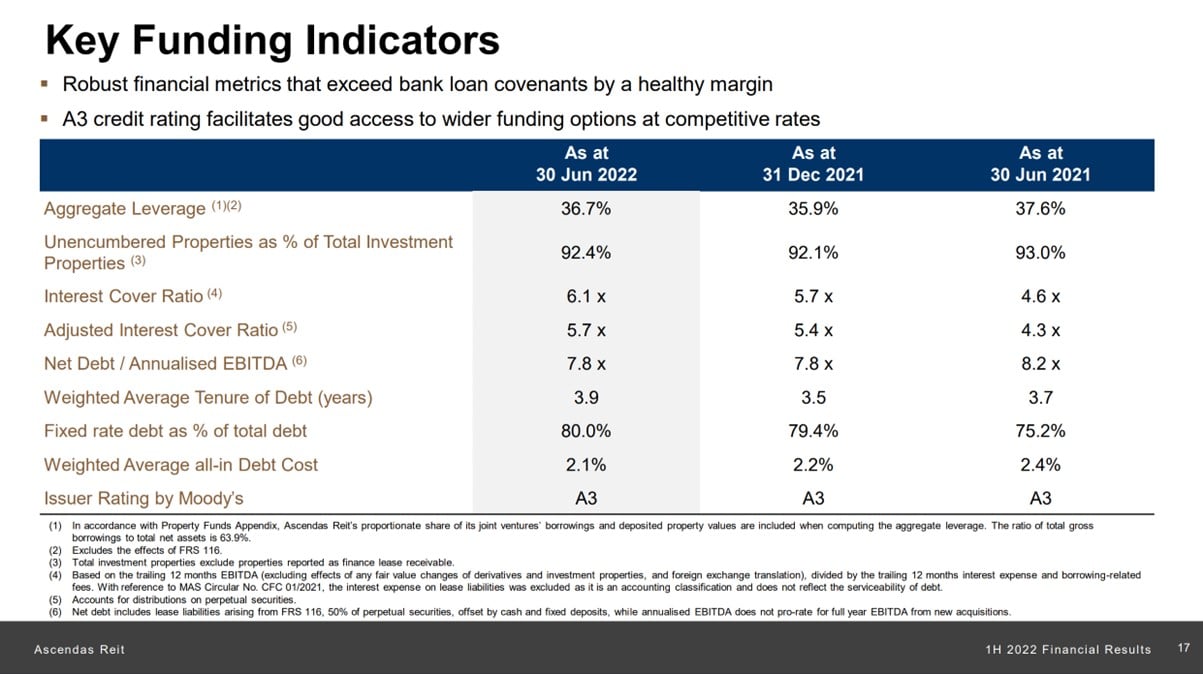

Let’s take Ascendas REIT as an example.

Back in June 2022, the average cost of debt was 2.1%.

The same cost of debt today is 3.5% – a whopping 66% increase in interest expenses over 18 months.

You need a massive increase in rental to offset that, which the economy simply cannot take.

But… is the bulk of the interest rate pain behind us for REITs?

Ascendas REIT has a weighted average tenure of the debt of 3.9 years.

And 20% of the debt is floating in nature.

This means that over the past 18 months, about 50% – 60% of the debt would have had to be refinanced at market interest rates – being the 20% floating debt that would have repriced immediately, and about 40% of the fixed rate debt that would have matured.

While over the next 18 months, about 30% of the debt is going to be refinanced at market interest rates which – worst case is going to stay at this level, and best case is going lower.

Let’s run some quick numbers.

Assuming worst case we see zero rate cuts for the next 12 – 18 months.

I could see that cost of debt stabilising around the 4.0% level.

Simplistically – that’s a 15% increase in financing costs, translating into a 6% drop in DPU.

I suppose what I’m trying to say is this.

Cost of debt going from 2.1% to 3.5% is a 66% increase in interest expense.

Cost of debt going from 3.5% to 4.0% is a 14% increase in interest expense.

Yes if interest rates stay high there will be pain for REITs.

But the pain may not be as drastic as the past 18 months.

Interest rates go down – good for REITs

What if interest rates do go down?

The Fed “Pivot” in late 2023 gave us a preview of market pricing in this scenario.

The Nikko AM REIT ETF jumped almost 16%.

That’s even before counting the dividends.

So in a true rate cut cycle, we may see pretty decent returns.

What is the risk-reward for REITs here?

This was what I wrote in FH Premium earlier this week:

Let’s take a mid cap REIT like Starhill Global.

Downside risk for REITs?

Let’s say I’m wrong, and interest rates stay high for the next 2 years.

Maybe we see 20% capital loss, and the REIT goes back to 0.38 which is the COVID bottom.

Throw in the dividend (current yield is 7%+ but let’s assume conservatively 6% yield due to higher interest expenses – pricing in a >15% DPU cut) – I’m probably sitting on a 8% loss over 2 years.

But don’t forget during these 2 years, if at any point I realise I am wrong, I can sell the entire position at market price and cut my loss.

There’s no rule saying I need to hold onto the REIT even if facts change and interest rates look like they’re going higher.

Upside reward for REITs?

What is the upside if we get interest rate cuts?

Say conservatively a return to the mid 50s.

That’s a 15% capital gain.

Throw in the dividend yield, you’re looking at 27% returns.

So 8% loss if I’m wrong, 27% gain if I’m right.

If it was a 50-50 chance of each scenario that alone that would be a good trade with proper position sizing.

What are the other risks with REITs?

The other risk of course, is if the REIT runs into refinancing issues and the share price gets wrecked.

Look at names like Manulife REIT, or Keppel Pacific Oak for example.

In those cases you might see permanent destruction of shareholder value.

So picking the right REITs is crucial (see views on individual REITs in the FH Stock / REIT watch).

What would I look out for when picking REITs?

I want to stick to REITs with strong underlying real estate, good sponsor backing, and primarily Singapore exposure.

It’s hard to call what would happen to US or European real estate the next few years, so I want to stick primarily to Singapore real estate.

Strong balance sheet matters too (although most of the S-REITs today run very high effective leverage at >40%).

As long as you avoid any refinancing problems, as long as the REIT hangs in there, there is a chance of recovery on the other side of the rate cut cycle.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

I like the risk-reward for REITs, but it is by no means a sure-win investment

Just to be clear – I am not calling the bottom for REITs.

I frankly don’t know where the bottom is.

If interest rates stay at these levels, REITs will likely continue their painful grind down.

All I’m saying, is that I like the risk-reward, because I stand to make more if I am right, than what I lose if I am wrong.

I was accumulating REITs since the second half of 2023.

And over the past few weeks with the sell-off I actually ramped up the pace of buying.

REITs today are the second largest position in my portfolio after the momentum US AI stocks/crypto (my full portfolio breakdown is shared on FH Premium).

And depending on how the macro plays out, I may use sell-offs to further increase positions.

But do realise that if interest rates stay high, this whole sector is in for a world of pain, so don’t get too carried away on position sizing.

Position size it well, so that even if I’m wrong, I still live to fight another day

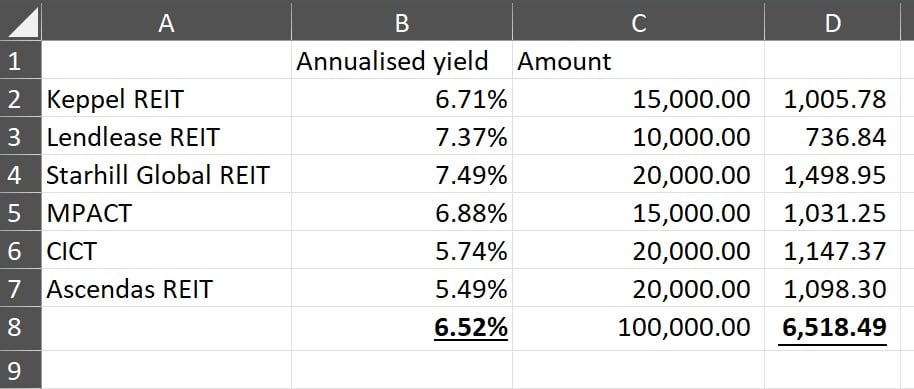

How I may invest $100,000 in REITs at 6.5% dividend yield? (as a Singapore Investor in 2024)

Based on my own personal risk appetite?

Hypothetically speaking, it might look something like the below:

- Keppel REIT

- Lendlease REIT

- Starhill Global REIT

- Mapletree Pan Asia Commercial Trust (MPACT)

- CapitaLand Integrated Commercial Trust (CICT)

- CapitaLand Ascendas REIT

- Keppel DC REIT

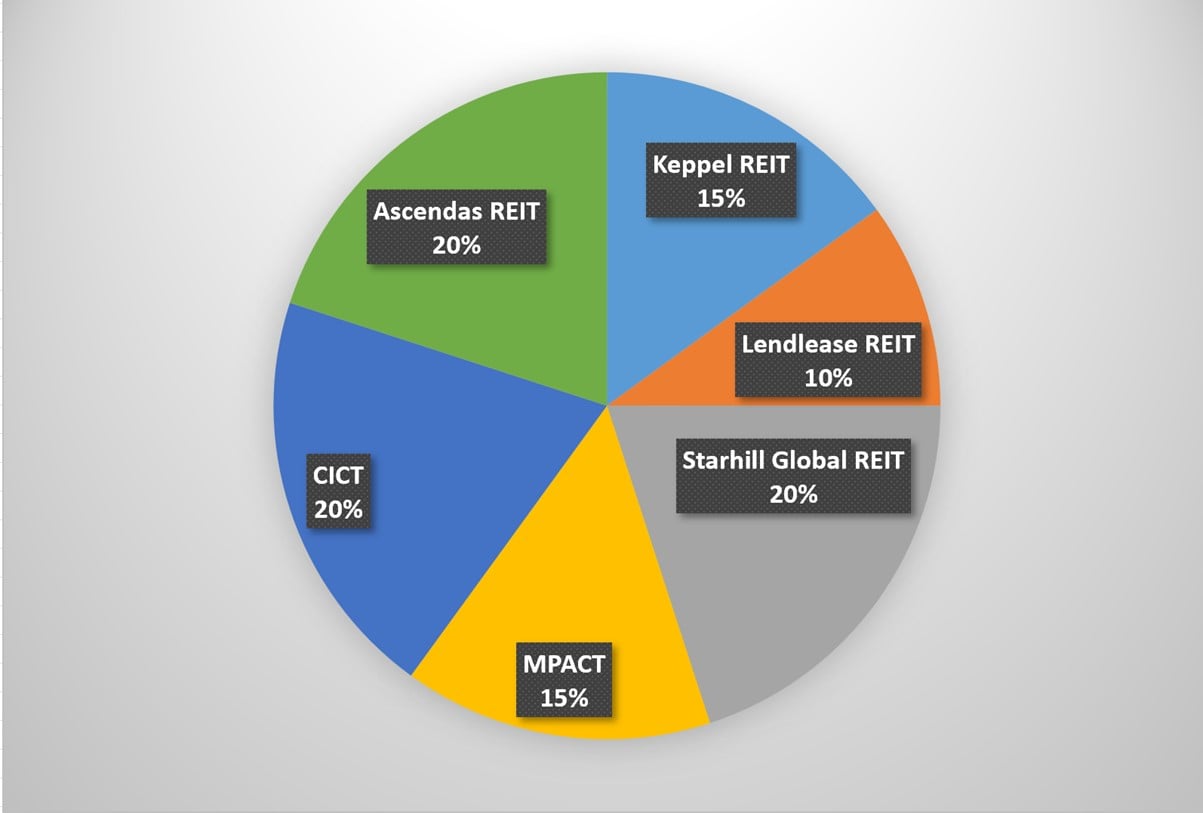

Assuming a broad 60-40 split between the blue chips and mid-caps gives us something like the below:

This gives fairly broad exposure to office, retail, industrial assets.

Exposure is primarily Singapore, although there will be some overseas exposure to Hong Kong (MPACT), Australia (Keppel REIT), Europe (Lendlease REIT, CICT, Ascendas REIT).

Sharing thoughts on the $100,000 REIT allocation

CICT and Ascendas REIT are the blue chip, “less risky” REITs.

That’s also why they trade at a lower yield – and probably won’t see as big capital gains even if we get interest rate cuts.

While Keppel REIT, Lendlease REIT, MPACT, Starhill Global are the more “risky” ones.

So you get a higher yield – and you’ll probably see bigger capital gains on the other side.

But if interest rates stay high you’ll probably see bigger losses from these REITs as well.

So broadly it’s about a 60-40 tilt in favour of the higher risk REITs, but feel free to amend accordingly based on risk appetite.

But don’t kid yourself though – if rates stay high the whole REIT portfolio is going to suffer.

There is no diversifying away the macro risk from interest rates.

For this REIT portfolio – Is the goal dividend yield, or capital gains? Passive, or active investing?

Dividend yield for this REIT portfolio is decent at 6.5% yield.

But I would say for this REIT portfolio my main focus would be the capital gains – as a proxy play on interest rates.

And I would expect to be quite active with this portfolio.

If we get a meaningful rally with interest rate cuts and this portfolio rallies 15 – 20%?

I may just take the profit and walk.

I worry that the next phase after this is for the return of inflation, and consequently higher interest rates.

If I have money in the bag, no need to risk it.

What if I am wrong and it looks like the Feds may need to hike again / keep rates here for a while?

I may take the loss and cut the entire position.

Or I might sell the more risky REITs, and only keep the blue chip REITs.

So that’s how I would be approaching a REIT portfolio like this, and I will share updates on FH Premium when I buy / sell REITs.

I think this decade will see significant volatility in interest rates, and I think a more active approach to REITs may outperform a pure passive approach.

My portfolio is split into 2 today – momentum (US Stocks) and mean reversion (REITs)

My portfolio is broadly split into 2 parts today.

On one end I have the highly momentum driven plays.

This is mainly made up of AI semiconductors, US Tech, Bitcoin/Ethereum/alt-coins.

On the other hand, I have the very oversold, mean reversion plays.

Mainly S-REITs with heavy emphasis on Singapore real estate, for the reasons shared above.

Combined these 2 make up almost 70% of my portfolio today (full portfolio breakdown shared on FH Premium).

What’s the biggest risk I face with this REIT / US Growth stock portfolio?

This also means the biggest risk I face today is interest rates staying high.

If interest rates stay high, probably that entire 70% is not going to do well.

How do I protect myself against that?

2 ways:

Healthy Cash Allocation

I continue to maintain comfortable cash levels.

This is because of (a) elevated macro risk, and (b) cash pays you almost 4% risk free these days (whether it’s UOB One, money market funds or T-Bills).

So even if I am wrong on everything I talked about above, at least that cash I have set aside is still generating ~4% yield risk free.

How much cash is enough – each investor has to answer that for himself.

You can see my cash levels on FH Premium.

More active approach to investing

If you want to run exposure to US momentum plays – AI, FAANG, Bitcoin/Ethereum.

I think you have to realise that when a chart goes parabolic like that, it will end poorly at some point.

With the kind of exposure I am running to US momentum plays.

The million dollar question is when to sell.

Sell too early you sit out on the gains.

Sell too late you give up all your gains.

So the other protection with the portfolio I suppose, comes from more active management.

Will I be able to pull it off?

Let’s see.

Whatever the case, I share regular updates on FH Premium as and when I make changes to my portfolio, including any changes to macro views.

The past 18 months have been one hell of a ride, I don’t expect the next 18 to be any different.

This article was written on 8 March 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

“Exposure is primarily Singapore, although there will be some overseas exposure to Hong Kong (MPACT), Australia (Keppel REIT), Europe (Lendlease REIT, CICT, Ascendas REIT).”

-> So the only 100% pure Singapore Reit must be then: Starhill GLOBAL Reit 🙂

FH, I read the banking article as well. In both you want expect a US i.r. cut. I disagree with that view.

The more Powell reduces, the more buying power the USD loses. US needs only 100 days for one trillion of new debt – would you take these treasuries for less %?

I expect a world in which financially healthy nations will lower i.r. as their currencies go stronger and unhealthy ones will (have to) rise them.

I know that all these tv people think Powell will cut, but in my view he can’t. We are not in business as usual anymore. The west is dead. Trust is gone. The ADR were stolen, pipelines bombed and now they steal the Russian reserves. I mean how low is that all? How desperate must one be to act so free of any honour? Cheers!

I fully understand where you’re coming from.

The question is what asset class would do well in the scenario you described? Probably only cash.

Hence I continue to hold healthy cash levels.

While my own belief is that Powell will cut in 2H24. In investing you want to hope for the best, but prepare for the worst.

Ensure that your portfolio is covered for both scenarios.