I recently shared how I would invest $1 million in dividend stocks for a 5% yield.

A lot of you asked:

Given $1 million today, how would I invest it, with no rules.

Not restricted to dividend stocks, or Singapore.

Just pure alpha.

With high inflation and rising interest rates, we’re facing one of the trickiest macro environments in our lifetimes.

How to invest $1 million into this market, in 2022, as a Singapore investor?

2 Different Portfolios: How I will invest $1 million in 2022 (as a Singapore Investor)

I’m going to share 2 portfolios.

The first will be using current market prices.

If I were to go out tomorrow and invest $1 million at today’s prices, how would I do it.

The second will be an ideal long term portfolio.

If I can invest countercyclically, and deploy the money over a 2 – 3 year period, how would I invest.

Rules for the $1 million portfolio

I know most of you want something simple and fuss free.

So the rules are:

- Long only (no shorting)

- Staying very big picture without excessive stock picking or market timing

At Today’s Prices: How I will invest $1 million in 2022

If I were to go out and invest $1 million tomorrow, this is the broad asset allocation I would use:

Breaking it down into individual names:

- Cash (or CPF / SSBs) $350,000

- Split amongst Cash, Singapore Savings Bonds and CPF-OA (depending on individual circumstances)

- Singapore Stocks $80,000

- DBS – $33,000

- UOB – $33,000

- OCBC – $34,000

- Singapore REITs $220,000

- CapitaLand Integrated Commercial Trust – $40,000

- Mapletree Commercial Trust – $40,000

- Ascendas REIT – $40,000

- Mapletree Industrial Trust – $40,000

- Lendlease REIT – $30,000

- CapitaLand China Trust – $30,000

- US Stocks $100,000

- S&P500 – $100,000

- China Stocks $60,000

- MSCI China ETF (2801) – $60,000

- Commodities $100,000

- Energy ETF (XLE) – $50,000

- Uranium ETF (URNM) – $25,000

- Copper ETF (COPX) – $25,000

- Precious Metals $70,000

- Gold (Physical or GLD) – $70,000

- Crypto $20,000

- BTC – $15,000

- ETH – $5,000

Why so much cash (35%)?

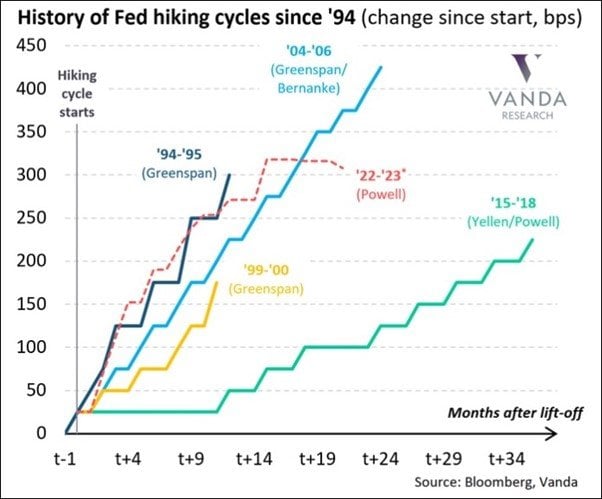

Inflation is at 40 year highs, and the Feds are projected to take us on the fastest hiking cycle in 25 years.

This is not a macro setup to go full risk on.

This is a macro setup to play defensive, and preserve capital until things blow over.

You can argue why not hold even more cash in that case, why bother investing at all?

And the answer is that (1) I could be wrong, and (2) inflation is very real.

A simple trip to NTUC tells you that regardless what the official CPI numbers say, inflation is already here.

Money in the bank does not hedge inflation, money in stocks / commodities / REITs does.

So the tricky part about investing today, is holding enough cash to be able to capitalise on any short term volatility, without holding so much cash that you are eroded away by inflation.

I used 35% cash for this mix, but really – only you can decide for yourself how much cash to hold.

Why no fixed income, Endowus Income, Syfe Income?

Short answer – I think there is potentially more pain to come for fixed income (bonds).

The problem with fixed income in this market is that if we do get a prolonged period of higher rates and higher inflation, fixed income losses are going to be horrendous.

And all the diversification in the world isn’t going to help fixed income when global rates rise in coordination to combat inflation.

Which means fixed income gives you the same interest rate risk as equities, but without the capital gains potential that equities have (fixed income upside is capped at the coupon yield).

At this point in the cycle, I don’t see risk-reward for fixed income as attractive.

US Treasuries can be used as a tactical timing tool, but as a buy and hold, I would rather go all in to equities, and just hold enough cash to tide through the volatility.

And skip the fixed income.

Where to park the cash?

The rule is to park the cash anywhere that is risk-free and liquid, while earning the highest possible return.

DBS Multiplier account, Singlife, Singapore Savings Bonds, CPF-OA are all possible solutions.

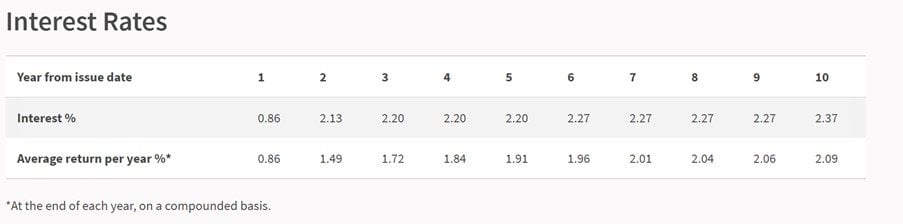

Latest Singapore Savings Bonds pay 0.86% for the first year and 2.13% for the second.

For the first time in a while, cash actually pays a decent return.

Be careful with money market funds like Endowus Cash Smart though – those things are not risk free, and there is potential for capital loss.

Am I buying commodities at a high?

Definitely possible.

But let’s flip it around – what if this is not the top for commodities?

What if over the next 5 years, in a world obsessed with re-onshoring manufacturing and prolonged supply chain disruptions – commodities continue their march upwards?

What would that do to your long tech long bonds portfolio?

To put it another way, if I am buying commodities at a high here, and inflation goes down after this – then the remaining 90% of this portfolio (except maybe gold) should do well.

And should offset the commodity losses.

But if this is not the high for commodities, then I’ll be glad I had that 10% allocation to commodities.

Which is kinda how asset allocation is supposed to work.

Why not short the market?

I get it.

Why not short the market, long the bottom, and make money trading the volatility.

As mentioned above, this is intended to be a long only portfolio.

So if you’re a skilled trader, by all means go ahead.

If you know how to do tail risk hedging, go ahead.

But I wanted this to be a simple portfolio that isn’t too hard to execute even for normal investors.

Which means long only, and no complex options play.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

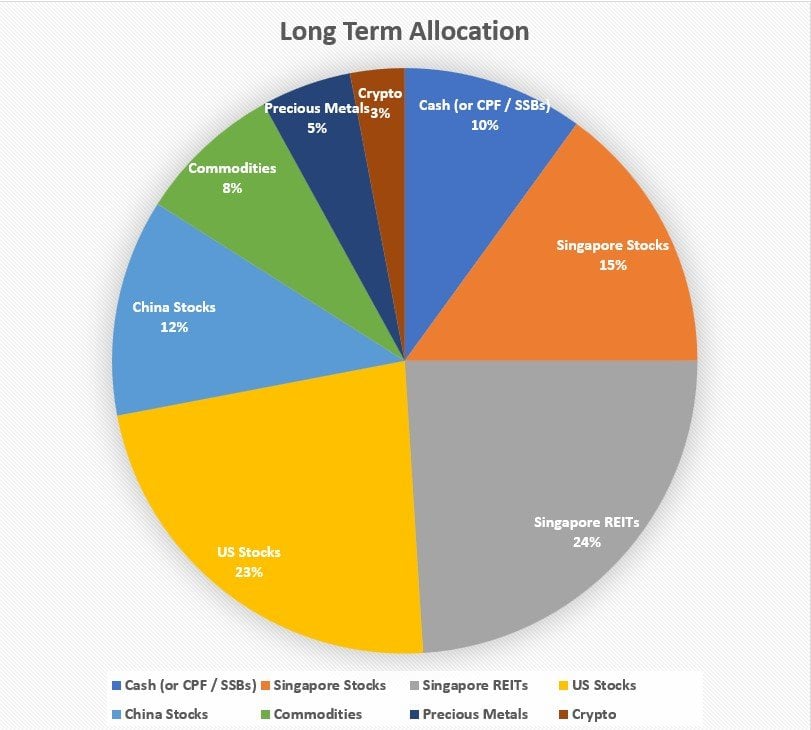

Long Term Asset Allocation: How I will invest $1 million in 2022

Now – assuming I can deploy the cash over a 2 – 3 year period, and invest countercyclically.

This is what I would go for:

And the breakdown:

- Cash (or CPF / SSBs) $100,000

- Split amongst Cash, Singapore Savings Bonds and CPF-OA (per individual circumstances)

- Singapore Stocks $150,000

- DBS – $80,000

- UOB – $35,000

- OCBC – $35,000

- Singapore REITs $240,000

- CapitaLand Integrated Commercial Trust – $60,000

- Mapletree Commercial Trust – $40,000

- Ascendas REIT – $40,000

- Mapletree Industrial Trust – $40,000

- Lendlease REIT – $30,000

- CapitaLand China Trust – $30,000

- US Stocks $230,000

- S&P500 – $100,000

- Semiconductors/Growth Stocks – $130,000

- China Stocks $120,000

- MSCI China ETF (2801) – $50,000

- China Growth Stocks – $70,000

- Commodities $80,000

- Energy ETF (XLE) – $40,000

- Uranium ETF (URNM) – $20,000

- Copper ETF (COPX) – $20,000

- Precious Metals $50,000

- Gold (Physical or GLD) – $50,000

- Crypto $30,000

- BTC – $20,000

- ETH – $10,000

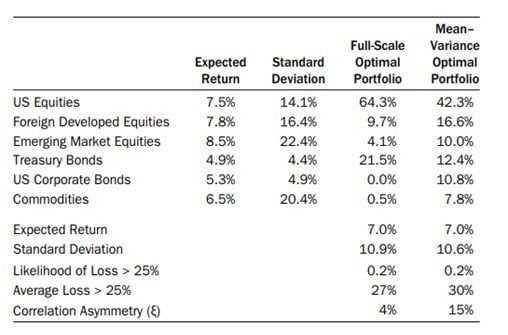

What is the right amount of commodities / stocks / REITs / cash?

So the problem is that almost every portfolio today is backtested using a 40 year regime of low inflation and falling interest rates (1980s till today).

If Larry Fink is right and the path going forward is one of deglobalisation, all those assumptions are now questionable.

If the future lies with moderate inflation and rising rates, every investor out there will need to relook their portfolios.

I have set out below some sample asset allocations, which I have used as the backbone of both portfolios above. I replaced the bonds with cash, US Equities with Singapore, and upped the REIT component for rental income.

But really, you want to reason from first principles here.

Think about how the world will change going forward. Think about your own risk appetite.

And build your asset allocation around it.

How much Growth vs Dividend?

The traditional thinking is that young investors want to overweight growth stocks like tech, cloud etc.

While older investors want to overweight dividend stocks for stability.

The only complexity is that if we do go into a prolonged period of high inflation and high rates, then dividend stocks may outperform growth stocks in the near to mid term.

So big caveat that your thinking on growth vs dividend should probably evolve as 2022 plays out, and the rate hike path + inflation path becomes clearer.

That’s why the “current prices” portfolio has a 35% allocation to cash, to allow you the flexibility to make such adjustments.

What growth names to pick?

I deliberately left the section on semiconductors/growth stocks for US and China open.

Which individual names to pick will depend on (1) prices and (2) individual risk appetite / knowledge.

If I am investing over a 2 – 3 year horizon, I don’t know which growth stocks will be cheap next year.

I will invest opportunistically based on what sells off as the rate hike plays out.

If Cloudflare is cheap now, I will buy Cloudflare. If Paypal sells off next year, I will buy Paypal.

For those who are keen – you can view my Stock watchlist and Personal Portfolio (with weekly updates) on Patreon.

And don’t underestimate level of knowledge.

A semiconductor nerd like me may love to go deep into the weeds and analyse the difference between the latest AMD and Intel processors. But if that’s not your idea of fun on a Good Friday, you can just stick with an ETF like SOXX.

To each his own.

What if you have $2 million instead… or $5 million?

It’s funny what I write an article on how to invest $1 million, and the question I get is what if you have $2 million instead?

What I would say, is that unless you have a very lavish lifestyle, the more money you have, the less risk you need to take with your investments.

Think about it this way – if you have $1 million invested at a 5% yield, that’s $50,000 a year.

If you have $10 million, that’s $500,000 a year.

The more you have, the less risk you need to take.

It’s why the ultra-high net worth are happy to accept a 2-3% return in bonds.

So as portfolio value goes up, I would gradually dial back on the risk exposure.

DCA or Lump Sum? What is your level of investing knowledge?

This depends on how you come into the money.

If it’s a windfall (eg. inheritance) then you want to think about your level of investing knowledge.

If you have been investing in markets for years, and know your way around a yield curve and options ladder, then yeah of course go ahead and lump sum.

But if you’re new to investing, and don’t really have much confidence in your investing abilities, averaging in may make more sense.

For most people who work a day job and the income comes in at the end of each month, it would just make sense to dollar cost average.

This way, you invest gradually over time, and build up investing knowledge and competence over time.

It’s an indirect way of managing risk.

Why no European Exposure?

Okay I think this is more a personal choice.

You can swap out some of the US/Singapore stocks for European stocks if you want.

VGK is a pretty decent ETF for those who don’t want to stock pick.

The charts are not pretty though. The Ukraine war and soaring inflation will be tough for Europe.

Closing Thoughts: There is no right / wrong way to invest

Writing this article has taught me a key lesson.

One’s investing portfolio is like their home.

It needs to be unique, and tailored for you.

Just like I would never dream of telling you what your home should look like, I cannot tell you what your investment portfolio should look like.

Only you can answer that for yourself.

What I would say, is that the world is changing very quickly.

A lot of previously sacred concepts like low inflation and falling rates are now questionable.

The mere possibility of this, requires a significant rethink in how to allocate your money.

I have shared some possible asset allocations above. I do hope this helps you in your thought process, and trying to find the right portfolio for yourself.

I would say my personal asset allocation does generally track the above, but with significant variation on individual stock names as I do stock pick. If you are keen, you can view my full stockwatch and Personal Portfolio (with weekly updates) on Patreon.

As always, this article is written on 15 April 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi FH,

Interesting read on Sat morning as usual. On the allocation to comods. What is the best way for a SG retail investor to get exposure without explicitly buying a company like Exxon or Shell.

Thank you as always.

Interesting – why the aversion to buying Exxon or Shell? With an IBKR account (or Moomoo), it is very easy to get access to global shares.

If one sticks only with SG stocks, it will be names like Wilmar etc, which are far more limited.

Sorry, to be precise, the comods ETF you highlighted seems to US centric and geared to Copper and Uranium? Is there other options out there?

Yes, you can also get ETFs that track other commodities. There are European listed ones, but you cant get away from the fact that many of the big commodity players are US listed.

I picked these because I find these commodities the most attractive currently – oil, nat gas, copper, uranium.