It’s been a while since I did a macro post on Financial Horse.

I’ve also been getting quite a few queries on how to invest as a long term investor.

So let’s remedy that today.

4 Stages to a Bear Market

As shared a while back, there are 4 stages to a bear market:

- Stage 1 (Market Topping) – Bubble bursts, euphoria gives way to selling

- Stage 2 (Pricing in higher interest rates) – Asset prices decline to price in the higher risk free rate

- Stage 3 (Pricing in lower earnings) – Rising interest rates start to weigh on the economy, resulting in lower consumer spending and corporate earnings

- Stage 4 (Panic Deleveraging) – Investors flood for the exits, creating liquidity problems

Now every market is slightly different.

The more speculative crypto markets? I think you could argue they are in Stage 3 or Stage 4.

But traditional financial markets?

Best guess – we are only in mid to late Stage 2.

When to start buying stocks in 2023?

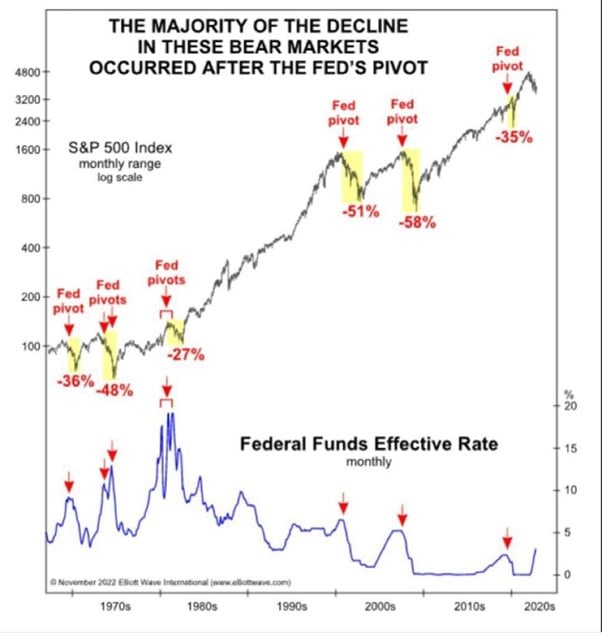

Now for the past 12 months, I have been saying that you want to keep a close eye for the “Fed Pivot” in 2022/2023.

But I want to add a bit of nuance to the discussion.

This cycle is different from any cycle we had the past 40 years, because of inflation.

The return of inflation, has changed the game.

Because for the first time in 40 years, central bankers cannot cut interest rates or implement QE, without considering what is the subsequent impact on inflation.

Will the Feds successfully tame inflation?

Let me break it down very simply.

When the Fed pivot does eventually come, how to invest next will depend on whether the Feds successfully tame inflation.

Or perhaps more accurately, whether the markets believe the Feds will successfully tame inflation.

Market believes the Feds will tame inflation

If the market believes the Feds will tame inflation – then you treat this cycle as no different from the past 40 years.

Think 2008, or 2020.

In such cases, the Fed pivot is just the start, and the market decline continues well after the Fed pivot, because earnings continue to decline from a slowing economy.

If this happens, you buy stocks when the money printing offsets the deleveraging.

Think March 2020 with unlimited QE, or 2009 with Fed QE.

Market does not believe the Feds will tame inflation

If the market does not believe the Feds will tame inflation – now you’ve got a real problem.

In the recent FOMC press conference Jerome Powell talks a lot about “Fed credibility”.

He talks about how it is easier to overtighten and cause a market crash – and then save the market with interest rate cuts and QE.

Than it is to undertighten and fail to solve inflation, only to have inflation come back later on. Which requires even more aggressive rate hikes down the road.

If you really think about it cynically, as an underpaid public official (relative to his estimated $50 million net worth), which would you as Powell pick:

- Prioritise the economy and pivot early – but risk getting the call wrong, in which case inflation comes back, and you get crucified for the mistake (going down as Arthur Burns 2.0)

- Prioritise inflation and pivot late – wait until there are clear signs of recession / financial contagion before pivotting. Whatever happens next you are absolved of blame, because you already tried your best and the economy couldn’t take higher rates

I leave you to decide which is more likely.

All I would say, is that the danger if the Feds pivot too early, is that the market may realise that it is insufficient to tame inflation.

Then all hell will break loose.

In this outcome, you trade it just like you would any Emerging Market with an inflation problem. Think Weimar Germany, Indonesia in the Asian Financial Crisis and so on.

You buy at the point where the central bank throws in the towel, metaphorically speaking.

Traditionally that would be when the central bank gives up on the currency defence, and allows the currency to free float (drop 30%).

This cycle – it would probably be the point where the Feds give up on fighting inflation, and stimulate the economy despite inflation.

I hope for all our sakes we don’t come to that this cycle – but if it does, then yeah I agree you go all in at that point.

Which outcome is more likely?

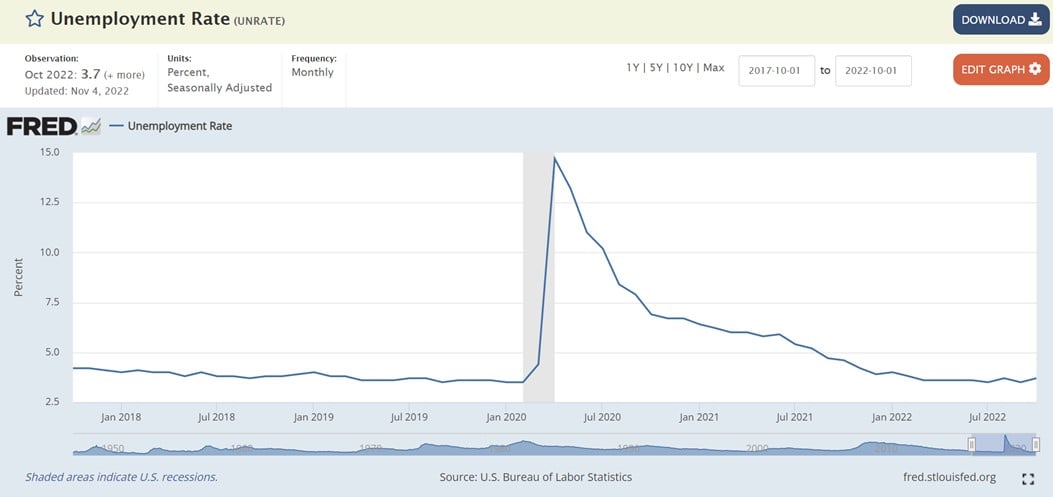

So the Feds have a dual mandate of maintaining (1) low unemployment, and (2) low inflation.

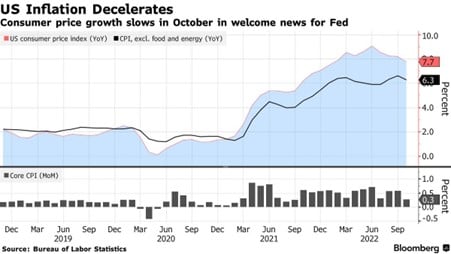

Unemployment right now is at 3.7%, close to 70 year lows.

Inflation on the other hand, is sitting close to 40 year highs.

So the Feds are getting an “A+++” on low unemployment, but they are close to criminally negligent on inflation.

And so of course they are acting aggressively to bring inflation down (official target of 2%).

The Dilemma of the Feds

But you see the problem here, is that the market is saying the Feds are going to pivot, when inflation is still at 7.7%, while unemployment is at 70 year lows.

But we already discussed that the Feds are doing very well on unemployment, but terribly on inflation.

And now that inflation is showing signs of coming down, why would they undo all their good work with a fed pivot.

Unless of course unemployment is going up, but it’s only ticking up very slowly:

The way I see it, at some point in this cycle, the Feds are going to have to make a choice.

They are going to have to choose between (1) fighting inflation, or (2) preventing a deep recession / financial market contagion.

But for now, (2) hasn’t happened.

Right now there is literally no trade-off to keeping interest rates at 5% to fight inflation.

So the Feds are free to keep prioritising fighting inflation.

And my view – talks of rate cut are too early.

Question isn’t how fast we hike or how high we go…

So for all the Fed Pivot bros obsessing over whether we are at 5.0% or 5.25% by June 2023.

Or whether we get there by May instead of June.

I think that’s just missing the point.

The question isn’t how fast the Feds hike, or how high they go.

The better question now – is how long do we stay at 5% interest rates.

If the Feds are truly serious about bringing inflation down, they may need to bring unemployment up to 5-6%.

Given the strong labour market and consumer spending, that could take up to 12 months – taking us to end 2023.

But with 5% interest rates, there’s also a real possibility of something breaking in financial markets before that.

And really – that’s the point I’m trying to make.

Before this is over, the Feds will need to choose between fighting inflation and avoiding a recession.

But until Powell is forced to make that choice, he can continue to prioritise the inflation fight, and try to get inflation down to the official 2% target.

Market for now, is expecting to have the cake and eat it. Bringing inflation down, while avoiding a deep recession.

That seems a tad optimistic to me.

Long story short – macro risk is still elevated.

2023 is going to be a wild year, as everything we discuss above continues to play out.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

How to invest $1 million in 2023?

Quite a few of you have reached out to ask for advice on how to allocate capital in this market.

Some of you are investing for 3 – 5 year periods, some for 20 year periods.

Some invest for a newborn child, some to save up for a house fund.

I cannot answer all these questions individually, but I wanted to share some high level views here.

Ask yourself if you are a (1) passive investor, or (2) active investor?

Probably the most important question.

Is to decide if you are a (1) passive investor, or (2) active investor?

Passive Investor

A passive investor is one happy to just track the market returns.

He is happy to put $1,000 a month into the same index fund, and keep buying for the next 20 years.

The S&P500 is down 15% this year, so the passive investor will be down 15% this year, and in fact is completely happy being down because he gets to average in cheaper.

Active Investor

An active investor does whatever it takes to outperform the market.

Don’t underestimate the amount of time and effort required to succeed in this.

And even after putting in all that effort, there’s no guarantee he/she outperforms the passive investor.

So ask yourself which one of the above you are, and then invest accordingly.

How I would invest $1 million in 2023 (as a Passive Investor)

If I were a passive investor, I wouldn’t bother with market timing.

I would just dollar cost average into the decline.

Anything happening the next 3 – 5 years, including the whole discussion above, is just noise really.

In fact I would be hoping prices continue to go down, because I’m averaging in for a 20 – 30 year period.

I probably wouldn’t buy it all at one go though, probably spread the money out over a few years.

A simple portfolio might look like this:

- $700,000 (70%) – All World ETF – IWDA (iShares Core MSCI World UCITS ETF USD (Acc))

- $300,000 (30%) Singapore – STI ETF, or stock pick if you hate the STI ETF (eg. DBS, UOB, OCBC, CICT, Ascendas REIT)

I know pure Indexers will argue for 100% IWDA, but I just think that as a Singapore based investor spending in SGD, it makes sense to overweight SGD assets.

But hey – it’s your money, you decide.

The more adventurous passive investors could also consider something like this, with more room to express your personal preferences:

- $400,000 (40%) US – S&P500 (SPY), NASDAQ (QQQ)

- $300,000 (30%) Singapore – STI ETF, or stock pick if you hate the STI ETF (eg. DBS, UOB, OCBC, CICT, Ascendas REIT)

- $300,000 (30%) Free play – China, European or Emerging Market ETFs (depending on personal preference)

Sidenote that for passive investors you should focus obsessively on costs.

Because every 0.5% on extra fees that you pay, is 0.5% less returns.

And over decades, that really makes a difference.

How I would invest $1 million in 2023 (as an active Investor)

As an active investor, you need to understand the entire Fed metagame that we discussed above – and have a view on it.

If you’re a long only investor, I would probably be in heavy cash, and buy in line with the analysis above.

I don’t deny there is value in this market though, so bottom up stock pickers can already start buying.

If you’re shorting this market, I would be very, very careful with market timing.

Bear market rallies are very real and very vicious, so don’t get too aggressive with your shorts.

What to buy in 2023 (as an active investor)?

If you’ve been following the macro discussion above, you will realise that what to buy will depend on what the world looks like when the Fed pivots.

Or more specifically – what inflation looks like.

If the Feds succeed in their quest to tame inflation for good, I think you could just run the same playbook you ran the past 10 years.

Heavy Tech, REITs, banks.

The problem is if inflation is not contained, or if the costs of taming inflation are so high (think deep recession or financial market contagion).

Such that the Feds are forced to accept a higher level of structural inflation.

In that case you want to run a more inflationary playbook, heavy on banks (but watch bad debts if we get a recession), commodities, energy or energy services, industrials etc. Think old world boring value stocks with strong cash flow.

Which are we more likely to see – Structural Inflation or not?

Predicting which is more likely requires understanding how a million things will play out between now and the Fed pivot.

We talked about how complex the world is last week, and not underestimating second and third order effects.

So I would caution against trying to predict too far out in time.

Just be patient, let the market play out, and respond accordingly.

Gun to my head, I will think that eventually the costs of taming inflation will prove so high (think deep recession or financial market contagion), that the Feds are forced to accept a higher level of structural inflation.

I don’t think the 2% inflation target is realistic, but hey – what do I know.

In which case a hypothetical portfolio I might run in 2023 might look like this:

- $300,000 (30%) – REITs (only if prices hit my fair value targets)

- Mapletree Industrial Trust

- Mapletree Logistics Trust

- Mapletree Pan Asia Commercial Trust

- Ascendas REIT

- CapitaLand Integrated Commercial Trust

- Frasers Centerpoint Trust

- Lendlease REIT

- $200,000 (20%) – Banks

- DBS, UOB, OCBC

- JP Morgan, Citibank

- $300,000 (30%) – Commodities

- Shell, Exxon, ConocoPhillips

- Peabody Energy

- Schlumberger

- XLE, XME ETF if lazy to stock pick

- $200,000 (20%) – stock pick (likely long term tech)

- 20% free to stock pick, there are names in tech ecosystem and semiconductor that I really like from a long term 5 – 10 year perspective, and will be looking to pick them up on the decline. You can check out the FH Stock Watch for the full list.

BUT – it depends on pricing…

I do want to emphasise though, that what names I buy, will depend very much on where prices go in 2023.

For example if banks don’t drop but REITs are massacred, I might move all the bank allocation into REITs.

And if REITs don’t hit my fair value targets, I’m happy buying less REITs.

A sidenote on REITs – Pricing is everything

Just a quick sidenote on REITs.

I know a lot of you love REITs and are monitoring REITs very closely, so I just wanted to share some quick views.

I think many investors are underestimating what a prolonged period of higher interest rates could do to REIT prices.

There’s already early signs of liquidity getting sucked out of the Commercial Real Estate market.

Once liquidity goes, the only sellers in Commercial Real Estate become forced sellers, and with significantly higher financing costs, most buyers are unprepared to pay anywhere close to the prices we saw earlier this year.

So the longer interest rates stay up, the more you will start to have true price discovery, in what can be quite an illiquid asset class.

All while refinancing costs start to add up, cap rates move up, and investors demand a higher yield (due to higher risk free rates).

I’m not saying that REITs are not a good buy, I’m just saying that in a climate like that, what REITs you buy, and the price you buy at, become absolutely crucial.

An investor buying CICT at $2.5 can lose money, while an investor buying CICT at $1.5 can make money. On the same REIT.

You can see my full REIT watchlist on Patreon together with my price targets if you are keen.

Stay Nimble…

Which is why again – I emphasise staying nimble and flexible.

Don’t be dead set on what you want to buy. Or at what price.

Let the market play out, watch how central banks respond, and watch how market prices move.

Then decide accordingly.

This market is unprecedented in 40 years because of inflation, and that’s a massive wildcard you absolutely need to keep an eye on.

I’ve been saying this since Jan 2022

For the record, everything I’m sharing in this article is in line with the framework I’ve been sharing on Patreon, week after week.

So if you find this article helpful for you, please do consider signing up for the Patreon subscription. Most of the regular macro updates have moved there.

At S$15 a month you get the premium weekly market updates like this one.

At S$25 a month you get my full stock and REIT watchlist, and at S$40 a month you get my full personal portfolio.

Don’t be penny wise pound foolish.

Think about how much you may have lost this year.

And how much you will lose in the next 12 months if you start buying too early.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Would you add a few percentage points to blue chip crypto (Btc/Eth)?

Since we are not sure how things play out in this environment. Hmmm, on second thought, maybe it can be more broadly classified as alternatives (art/watch/wine)

Yes that’s perfectly fine. Although as a very volatile investment, I leave it up to each investor to decide on the right position sizing.

I do think it should be viewed as a standalone asset class apart from art/watch/wine though. Crypto has gotten to the point where it does trade differently from other asset classes.

If the Fed funds rate reaches 5%, what do you think SORA would be?

Not an easy call – the transmission mechanism from Fed Funds -> SORA is not straightforward.

Gun to my head, I would say if FFR hits 5%, you could see SORA at 4.5% +/- 50bps each way.

Thanks, I used SORA 3.5% when estimating REIT future interest expenses. ~ 17-30% DPU decrease by 2027.

Better a rough estimate than no estimate 🙂

Oh I get what you mean.

If you’re modelling for a 3 – 5 year period, then I agree 3.5% is probably a more realistic number.

4.5% is probably a short term peak, but not sure how it will stay there.

Dear FH

Thanks very much once again

Agree with your views

My bet is that 2% target will be compromised as to get there would mean a lot of pain plus a lot of time

Unemployment at even 4.5% with poor earnings will move the needle and the fed will buckle up as popular sentiment will get increasingly hostile

Certainly, there will be market/financial credit events as well

The current market has factored in only a terminal rate of 5% and not more than that. Additionally, an earnings recession has not been factored in as per my calculations

This means that

– Markets will test new lows or retest the June/Oct levels at least if the rates go higher than 5 for certain plus fall further if the feared earnings recession materialised in Q4 numbers itself in very early 2023

– If earnings hold up , which is unlikely and the fed STOPS raising rates beyond 5% preferring to watch for a couple of months data- then the markets will stay at this level at least

The subsequent catalyst will be earnings only. If they start to go down steadily, the SPY will touch 3500 for certain!

A very tricky market to navigate indeed and my plan of action would be to

– regularly take small trading profits whenever feasible

– shore up cash position

– Buy good blue chips at pullbacks and hold , especially dividend payers

– take risks with REITS at set prices at at least a 3% spread to the SGS 10 year( currently 3.2 and might fall)

– Buy the SG banks at each market correction

The banks, to a great extent, will hedge the REIT risk and vice versa – Plus their weighted combined yield at 5%, albeit at risk to market forces, has stood the test of time so far !

Ultimately, it will be a long battle that might end only in 2024/25

The battle started early 2020 with the pandemic

Best wishes

Garudadri

Great comment as always Garudadri, agree with most of your views.

Some points to add:

1. Agree that the 2% inflation target will be dropped in time. Key question is how much pain do we need before we get to that point.

2. Personal view is that terminal this cycle is probably in the 5 – 5.5% range. Could be wrong but I dont think we will go much higher than that, but the key question is how long we stay there.

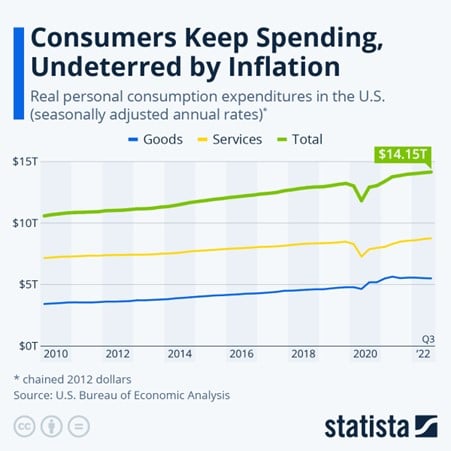

3. Consumer spending is still holding up well for now due to the strong labour market driving wage increases. But if labour starts to roll over, consumer spending may start to dip – in which case we will see the impact on corporate earnings.

4. Agreed that this market calls for a more active style strategy. Timeline wise, 2023 looks to be very volatile, and broadly agree that a more realistic end target is 2024.