A lot of readers have been asking about the best place to park excess cash right now.

Bank interest rates (or Singapore Savings Bonds) are absolutely horrible these days.

Just take a look at the latest August Singapore Savings Bonds rates:

| YEAR FROM ISSUE DATE |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

|

Interest,% |

0.27% |

0.35% |

0.49% |

0.64% |

0.81% |

0.99% |

1.19% |

1.39% |

1.58% |

1.76% |

|

Average p.a. return, %** |

0.27% |

0.31% |

0.37% |

0.44% |

0.51% |

0.59% |

0.67% |

0.76% |

0.85% |

0.93% |

0.27% for 1 year! What a disaster.

Long story short, we are in a low yield environment, and this isn’t likely to change for a few years.

So for excess cash that we have lying around, it pays to start exploring more creative, higher yielding accounts to park that cash.

I came across Singlife Account recently, and I had a very good experience with it, so I wanted to share this review with you guys.

Singlife Account Referral Code / Promo Code

Update: Singlife’s Paid Referral Programme has enjoyed a successful run and will come to a close as of 1 November 2020. Thank you for all your support! Upon the Effective Date of Termination (1 Nov 2020), all referees who have successfully in-forced their Singlife Account(s), by the Effective Date of Termination, will have up to fifteen business days (i.e. by 20 Nov 2020) to order and activate their Singlife Visa Debit Card to qualify for the S$10 bonus.

Basics: What is the Singlife Account?

According to the website, the Singlife Account is “an insurance savings plan. It is neither a bank savings account nor fixed deposit”

I’m reminded of the Deng quote about “Black cat or white cat, if it can catch mice, it’s a good cat.”

Because the way I see it, the Singlife Account is an account that you can put money in, get paid interest on, and take money out any time.

Sounds a lot like a bank account to me.

Whatever the case, Singlife Account pays way higher interest rates than a normal bank account, is SDIC backed, with instant withdrawals any time. Whether they call it a bank account or not, it sure sounds attractive to me.

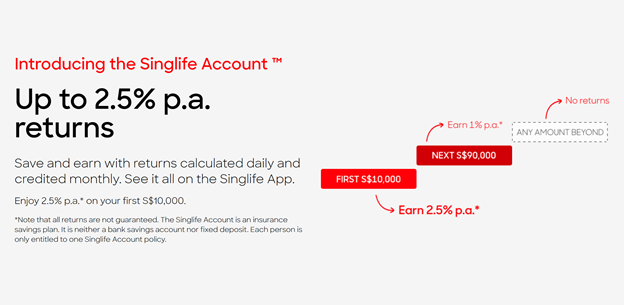

Interest Rates of up to 2.5% p.a.

Interest rates are set out above.

Basically:

- First S$10,000 – 2.5% pa (2.0% from 1 October)

- Next S$90,000 – 1.0% pa

- Beyond the first S$100,000 – no interest

First S$10,000 – 2.5% pa

The 2.5% on the first S$10,000 is really attractive. There’s just no other account on the market that comes close to this rate, especially when this is risk free and there is no lockup period.

If you’re prepared to go through the hassle of a new account, Singlife Account is worth it just for this 2.5% on the S$10,000 alone.

Nothing else on the market comes close.

Note: The interest rates will be revised to 2.0% on the first $10,000 from 1 October. This makes it less amazing, but it’s still very strong compared to the other alternatives on the market.

Next S$90,000 – 1.0% pa

The next S$90,000 pays 1.0%.

This isn’t amazing, but it’s still a lot higher than a lot of the competing accounts out there. CIMB Fastsaver for example pays 0.825% blended rate on S$100,000, so Singlife at 1% still beats them.

Beyond the first S$100,000 – no interest

There’s no interest beyond S$100,000, so don’t hold more than S$100,000 in your Singlife Account.

Update: As pointed out by a helpful reader – The interest is calculated on a daily basis but credited on a monthly basis.

Also, the minimum to open to account is $500, and minimum balance is $100. Once you withdraw fully, the policy is treated as surrendered, so your account will be closed. To reopen will be a reinstatement and subject to Singlife’s approval, so it may involve additional complexity.

Long story short – just always keep a minimum of $100 inside to avoid any hassle with account opening down the road! 🙂

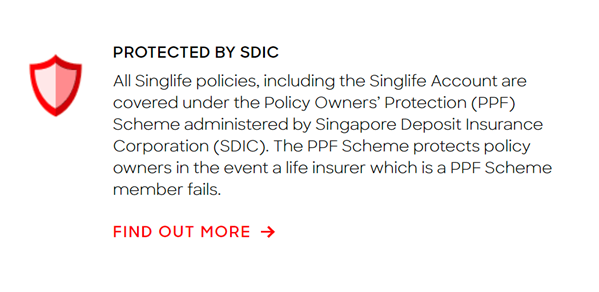

SDIC Insured – Risk Free

Taken from their FAQs (emphasis mine):

The Singlife Account is protected up to specified limits by the Singapore Deposit Insurance Corporation.

Singapore Life Pte. Ltd. (Singlife) is a registered member of the Policy Owner’s Protection Scheme. The PPF Scheme protects policy owners in the event a life or general insurer which is a PPF Schema member fails.

The PPF Scheme provides 100% protection for the guaranteed benefits of your life insurance policies up to the applicable caps. Coverage for your policy is automatic and no further action is required from you.

The PPF Scheme is administered by the Singapore Deposit Insurance Corporation (SDIC). To find out more, click here.

So basically, the Singlife Account is SDIC insured up to S$100,000, which makes it a very attractive place to park some cash risk free.

This is the same SDIC insurance that covers your bank account up to S$75,000.

No Lockup period – Transfer and withdrawal of money via FAST

There is absolutely no lockup period. You can transfer the money in and out as you please.

All transfers in and out are done via FAST transfer, so they are almost instantaneous.

My transfers in and out were reflected almost instantly in the Singlife Account / my bank account.

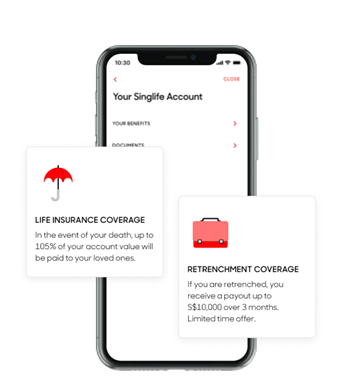

Extra Benefits (Life Insurance and Retrenchment Insurance)

I was using Singlife Account purely for the extra interest, but it also comes with some very nice benefits: (1) Life Insurance Coverage, and (2) Retrenchment Coverage.

(1) Life Insurance – If you die, they will pay out up to 105% of your account value to your loved ones

(2) Retrenchment Coverage – If you are retrenched, you receive a payout up to S$10,000 over 3 months

You get these benefits completely free of charge when you create and fund the account. When it’s a free service, it’s pretty hard to complain about it, so any benefit is just icing on the cake.

The full T&Cs are here.

Personally I hope I never need to cash out either of these though.

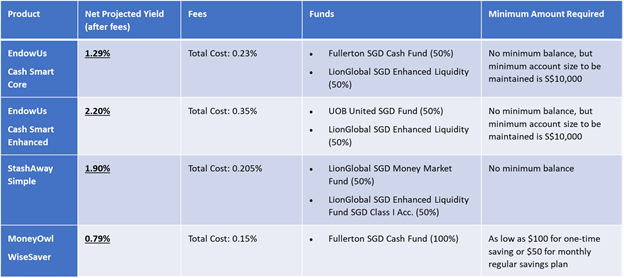

How does it compare with other Money Market Funds – EndowUs Cash, StashAway Simple, MoneOwl Wisesaver?

| Product | Net Projected Yield (after fees) | Fees | Funds | Minimum Amount Required |

| EndowUs Cash Smart Core | 1.29% | Total Cost: 0.23% | ·Fullerton SGD Cash Fund (50%) ·LionGlobal SGD Enhanced Liquidity (50%) | No minimum balance, but minimum account size to be maintained is S$10,000 |

| EndowUs Cash Smart Enhanced | 2.20% | Total Cost: 0.35% | ·UOB United SGD Fund (50%) ·LionGlobal SGD Enhanced Liquidity (50%) | No minimum balance, but minimum account size to be maintained is S$10,000 |

| StashAway Simple | 1.90% | Total Cost: 0.205% | ·LionGlobal SGD Money Market Fund (50%) ·LionGlobal SGD Enhanced Liquidity Fund SGD Class I Acc. (50%) | No minimum balance |

| MoneyOwl WiseSaver | 0.79% | Total Cost: 0.15% | ·Fullerton SGD Cash Fund (100%) | As low as $100 for one-time saving or $50 for monthly regular savings plan |

I’ve set out the rate for some other Money Market Funds above.

StashAway Simple and EndowUs Cash Smart Enhanced can offer you about 1.9% to 2.2%.

That’s still lower than the 2.5% on the first S$10,000 in SingLife, but better than the 1.0% on the remaining S$90,000.

The problem with these money market funds though, is that:

- Not SDIC Insured – They are not SDIC backed. They are still very low risk though – and outside of a Lehman 2008 / March 2020 style, I think the chance of losing money in a money market fund are very low. But without the SDIC insurance, they cannot be viewed as zero risk. There is always a small chance that you may suffer capital loss from money market funds.

- Withdrawal takes a few days – Because it takes some time to credit and withdraw from the money market funds, you cannot get your money instantaneously. After submitting a withdrawal request, it will typically take around 3 business days to get the money back into your account.

- Rates are not fixed – The rates in the table above, are projected rates. They will change over time. And given we’re now living in an era where interest rates are zero bound, I’m pretty sure the rates in the table above are going down. Of course, you can argue the same thing for Singlife, and I do agree that eventually Singlife’s interest rates may come down as well. But for now they seem to be using the 2.5% rate as a way to entice new customers, so here’s hoping they keep it up for longer.

So again, the first S$10,000 in Singlife Account is amazing and better than these money market funds, but for the next S$90,000, there are alternatives out there.

Overall experience

I recently opened a Singlife Account and transferred some cash in, so I figured I would share my experience.

The onboarding is all online via the Singlife App. The app is very smooth and slick, something I liked a lot. There’s nothing I hate more than a slow and buggy app.

The onboarding process is also very smooth. You connect your Singpass account to pull information from MyInfo, fill up a few additional details, and the account is open.

Funding the account is via FAST. The initial crediting will create the account, so give it about an hour or two to process the first time.

Once the account is open though, all subsequent transfers and withdrawals are almost instant, which is amazing.

The Singlife Visa Debit Card is absolutely free, and allows you to withdraw money or spend from the card. It’s a condition for the referral bonus / promo code, so I requested for one.

It took about 1 or 2 weeks to arrive, which was pretty alright considering it’s the COVID period.

Once the Visa Debit card was here, activation was done via the app (instant activation).

All in all, the experience was very smooth, and the app is very quick.

I really liked the entire experience.

SingLife Account Referral / Promo Code

Singlife’s Paid Referral Programme has enjoyed a successful run and will come to a close as of 1 November 2020. Thank you for all your support! Upon the Effective Date of Termination (1 Nov 2020), all referees who have successfully in-forced their Singlife Account(s), by the Effective Date of Termination, will have up to fifteen business days (i.e. by 20 Nov 2020) to order and activate their Singlife Visa Debit Card to qualify for the S$10 bonus.

Closing Thoughts

I really like Singlife Account.

I don’t give FH Ratings for Accounts, but if I did, this would probably be a solid 4 Horse Rating for me.

It’s 2.5% p.a. risk free for the first $10,000 – and there’s just nothing on the market that comes close. So I would highly recommend Singlife Account even if just for the first S$10,000.

It’s a no brainer. As long as you’re prepared to take a few minutes to open a new account, you get that 2.5% interest risk free ($250 a year on S$10,000), and a nice $10 referral bonus. You can transfer the money out any time you want too.

The next $90,000 pays 1.0%. That’s decent but not amazing. If you try hard enough, you’ll probably be able to get better rates elsewhere.

I decided to put some spare funds in there because the 1% is still higher than the rates I was getting elsewhere, but I think the next $90,000 is really up to you.

If you think you can get better rates, then just park S$10,000 in this Singlife Account.

Either way, it’s a really good option to park some excess cash in the short term, while waiting for investing opportunities to open.

BTW – It’s the one year anniversary of the FH Course, so we’ve launched a big promo with discounted prices and freebies for both the FH Course and REITs MasterClass. Find out more here.

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Is the interest paid out on a monthly basis?

Yes, monthly basis.

Hi FH, your article was out at a perfect timing when i was researching more on this singlife account which was all the rage in the investing community, only hesitant due to capital protection but reading your post really persuaded me to open one.

I have a few questions.

1.regarding the bonus $10 , i followed your link and downloaded it on my iphone, how does it know im using your link? also input my first $500 via fast and applied for the card.

2. i understand there is 2.5% for first 10k but the * says that the returns are not guaranteed right? it could be way lesser then 2.5% projected?

Great, glad you found it useful! Added my comments below:

1) Yeah it’s not that obvious whether it’s triggered, I had the same problem myself too. But as long as you download via the link and open an account that way, it registers properly. That’s what happened for me and I got my referral bonus in the end.

2) Yes, it’s just like the DBS Multiplier rates. This is what it is for now, but they reserve the right to change down the road. Singlife seems to use this as a cheap way to get customers (vs DBS who doesnt really need the money / customers), so let’s hope it lasts longer. 🙂

Hi,

Is the debit card free for life or there are annual charges?

Thanks

No annual charges. 🙂

Dear Finance horse,

Any charges to close the account should they decide to reduce the first $10K interest drastically?

Thank you

No, you can close for free by withdrawing the money anytime: https://singlife.com/manage/no-lock-in/

Just to add: calculated on a daily basis but credited on a monthly basis.

Also, I think I read that if you withdraw fully, the policy (or account) is considered as surrendered. Since you can only have one Singlife account per lifetime. any application after a full surrender is considered a reinstatement and subjected to Singlife accepted it. There’s also minimum daily balance you need to maintain to earn the interest which is $100. So, if interest is reduced, can always move the money around but keep some or $100 in Singlife just to keep it “live” while waiting for it to be revised upwards again, rather than reinstating it. Just my two cents! :0)

That’s a good point, thanks for raising this! I’ll update the article. 🙂

Hi FH,

Thanks for the article and it’s really informative and useful as always.

According to the SDIC website, https://www.sdic.org.sg/calc/pop_calc, it states that we have to meet one of the 4 conditions, pasted in parentheses for ease of reference.

(a. you have a claim under a life insured policy which happened before the PPF Scheme member failed;

b. you have given notice to the life insurer that you want to surrender a life insured policy before the failure; or

c. if your policies have matured before the insurer fails; or

d. you have been receiving annuity payments,)

in order to be “entitled to be paid compensation for the guaranteed benefits payable under your life insured policy”.

In the event that Singlife defaults and we still have our capital in Singlife account, I don’t think we will meet any of the 4 conditions to be entitled for the compensation? Please correct me if my understanding is wrong.

Can I clarify that our capital is still guaranteed under SDIC and is risk free given above point.

Thanks in advance.

Hi Joe,

Thanks, glad you find it useful!

It is, but just give Singlife a call if you’re worried. They’ll be able to confirm.

I actually spoke to them on this and they confirmed in the affirmative. 🙂

Hi FH, Singlife invest the deposits/capital in their non participating fund; will the fund lose money? If the fund loses money; will my deposits/capital shrink because return is non guaranteed? SDIC doesn’t protect losses due to investment returns right? Thanks.

No, the principal amount is protected. The returns are 2.5% for now, but of course that can change in future.

SDIC will protect the principal amount, but the returns may drop from 2.5% if Singlife changes their policy.

This is not an investment style fund, so the conceptual basis is slightly different. Think of it more like a bond rather than an equity. 🙂

Hey FH, I have received my card and activated it. However the bonus is not reflected? Any advice?

That’s strange, I have been received a few referrals so the link definitely works. You can check with Singlife directly at [email protected] or +65 6911 1111, could be a tagging issue on their end.

terrible customer service …. I could not sign on because the internet of Singlife app hanged, my name is too long, the app cant accept, so I was stuck there, clicked and clicked without response….so seek help from Chat, but Chat pushed to whatapp, then whatapp pushed back to Chat….. ???? both told me to seek help from the other…. give up…

Why not just use a shorter name?

Singlife app have problem, I could not sign on as new customer, the app hanged, but the customer service is terrible..

Chat told me to look for Singlife whatapp, but whatapp push me back to Chat, both Chat and whatapp pushing me to each other???… ???? I give up ????

singlife said length of name is not a factor, the system has technical problem.

Ah in that case you do need to check with them. When I had issues their whatsapp customer service did reply quite quickthough.

used your refer code to install singlife, is 3.0 version, not the latest 3.5 version, can login…????

used your refer code to install singlife, is 3.0 version, not the latest 3.5 version, cannot login…????

I’ve updated the referral code, you can use this instead: https://app.singlife.com/NhGh7Eaqfab

Once you’ve installed the app, you can update it via playstore.

just tried again, still can’t login. contact Singlife Whatapp, but since one week ago, the tech staff trying to find excuses. the tech staff excuses are : my mobile phone not compatible, the version of app I installed not up to date ? my name too long ? all kind of excuses, more than one week still can’t solve the problems, I doubt he is a competence IT guy.

read the feedback in the Singlife app with horrors, many similar cases like me, and the tech guys replies were the same, told the customer to wait, and many like me have been waiting for weeks.

Singlife tech guys are paid to work, not to blame the customers

To be fair to them though, the sign up volume has been very high during this period. 🙁

Hi referred by singlife to see if my name is under your pending list for the referal bonus, able to pm? Thank you!