Disclaimer: The following post is sponsored by MoneyOwl, all opinions and views expressed in this article are courtesy of Financial Horse.

There are 2 kinds of robo-advisors out there.

The first will be guys like Stashaway, Autowealth, Smartly etc that use publicly listed ETFs to build a portfolio for you.

Then there’s the second group with guys like MoneyOwl and Endowus that use Dimensional Funds to construct a portfolio.

I’ve been getting a number of queries on MoneyOwl recently, so let’s take a closer look at them.

Basics: What is MoneyOwl?

The onboarding process for MoneyOwl is no different from any other roboadvisor. You fill up your financial information, goals etc, and it generates a recommended asset allocation for you.

What is slightly different about MoneyOwl, is that:

NTUC Parentage – MoneyOwl is a joint venture between NTUC Enterprise and Providend. That may not mean a lot to the sophisticated guys out there, but you wouldn’t believe the number of conversations I have with investors who are reluctant to invest in REITs or ETFs because of the fear of losing all their money. Being able to mention “NTUC Social Enterprise”, works wonders in such situations.

Not everyone may agree with this, but the way I see it, the fact that NTUC Enterprise has a stake in MoneyOwl, lends a lot of legitimacy to MoneyOwl, especially for the newer investors or older folks.

Bionic – MoneyOwl calls themselves a “Bionic Advisor”. What this means, is that there is a human advisor on the other end that you can speak to anytime.

It may not seem like much now, but when the next liquidity event comes around, and the S&P500 is down 30% from highs and the newspapers are talking about widespread retrenchments, it actually really, really helps to be able to pick up the phone and speak to someone about your investments. If you’re that kind of investor, this benefit alone can justify the fees paid to MoneyOwl, and more.

How good are their human advisors? I spoke to one of them while preparing this article, and she was pretty knowledgeable in answering my questions about their bond funds. So read into that what you will!

MoneyOwl also says that they employ salary based advisors (rather than commission based advisors), to minimize possible conflicts of interest. That’s not a bad thing.

Investment Philosophy – According to MoneyOwl, their investment philosophy is:

“Successful investing for an individual is not about maximising returns or even maximising risk-adjusted returns (returns in return for the risk undertaken). It is about getting the best probability of meeting your financial goals so that you can achieve your life goals. With as little guesswork and as little stress as possible.

MoneyOwl has identified four keys to successful investing:

- Focus on asset allocation – do not take country, sector or firm-specific risks

- Go for market-based return – it is hard to consistently beat the markets through active management

- Keep costs low – the difference compounds big time, over time

- Stay invested for the long term – time in market, not time the market!”

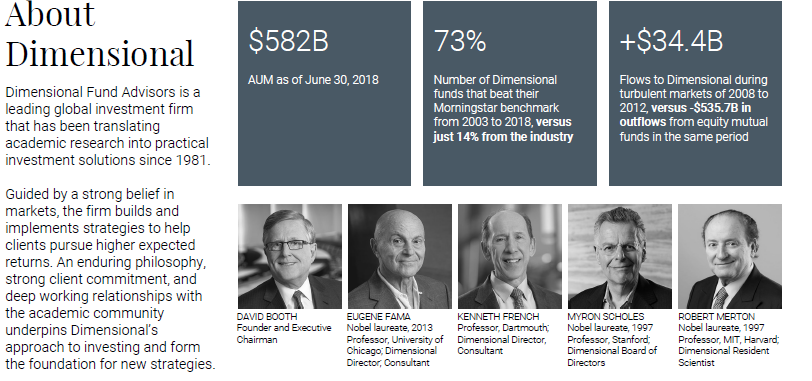

Basics: Dimensional Funds

Now apart from the points above, the main unique point about MoneyOwl, is that they use Dimensional Funds as their underlying funds.

Dimensional is a global fund manager that uses factor based investing.

Think about it this way. Most index funds out there are market capitalization weighted, which means that you’re investing more money in the large companies with a large market cap.

With Dimensional, the thinking is that over long periods of time, companies that are small, have low valuations, and high profitability (ie. small cap, value, high profitability stocks), outperform the index. So Dimensional funds will try to “tilt” the portfolio to give additional weightage to such stocks.

Unfortunately, over the past 10 years, due to an era of easy central bank liquidity, growth and large cap stocks has outperformed small cap and value, so the Dimensional funds style of strategy would have underperformed.

But of course, investing is always forward looking, so the key question is whether Dimensional will outperform going forward.

No one knows for certain, but my personal take, is that markets are ultimately cyclical. It’s like fashion. If you wait around long enough, what was popular in the 1990s will eventually become fashionable again. And if you take a long enough view on financial markets, small cap and value stocks may eventually make a comeback. And if they do so, they will come back with a vengeance.

That said though, if you’re looking to invest in Dimensional funds, you should be taking a longer term, 10 to 20 year kind of perspective. Because in the short term anything can happen, but in the longer term, there probably is a good chance that small cap and value may make a comeback.

Asset Allocation

MoneyOwl uses 3 different Dimensional Funds:

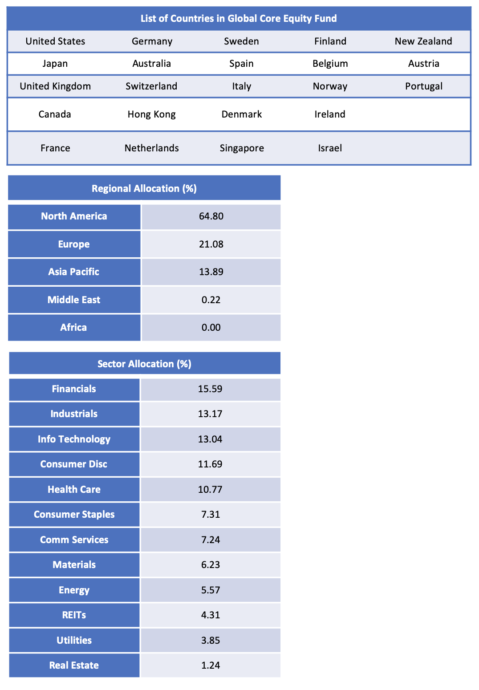

- Dimensional Global Core Equity Fund (SGD, Accumulation) – Developed market stock fund

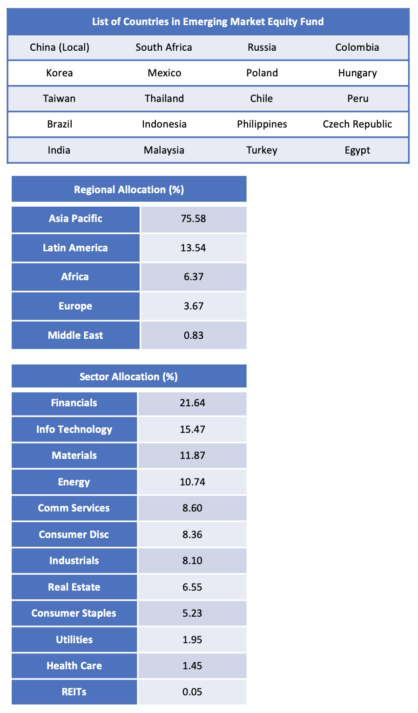

- Dimensional Emerging Market Large Caps Core Equity Fund (SGD, Accumulation) – Emerging market stock fund

- Dimensional Global Short Fixed Income Fund (SGD, Accumulation, Hedged) – Invests in short term high quality bonds globally. Hedged against the Singapore Dollar

The allocation of each fund is set out below.

Dimensional Global Core Equity Fund (SGD, Accumulation)

Dimensional Emerging Market Large Caps Core Equity Fund (SGD, Accumulation)

Dimensional Global Short Fixed Income Fund (SGD, Accumulation, Hedged)

Nothing noteworthy on the stock funds, they do what they’re supposed to do, which is to get exposure to Developed / Emerging Market stocks, with additional allocation to small cap and value stocks.

What is interesting though, is that the Dimensional Bond fund used by MoneyOwl is a short term bond fund with heavy exposure to Europe. Which is interesting because many European bonds are negative yielding these days, so you actually lose money if you hold them to maturity. When I queried MoneyOwl on this, they replied that:

“On the Europe exposure for our Bond fund, at the moment the yield curves in Europe are steeper than many of the other larger developed world bond markets. As such, Europe offers the possibility of higher expected total returns when capturing the roll-down on the yield curve, hence the significant current weight in the strategy (compared to the US or Japan for example). Dimensional does not have an approach of holding the bonds to maturity, hence the negative yields when holding the bonds to maturity does not apply.”

And:

“In fact for Dimensional, their definition of expected return does not depend on a market forecast of where yields go, but rather they base on information which can be directly extracted from market prices today. This “non-forecasting” approach is quite fundamental to their investment philosophy, as well as ours.

If the yield curve has a normal slope, the market price of a bond naturally increases as the bond rolls down the yield curve.

What Dimensional does is that they favour investing in steeper yield curves (where yields change the most over a particular period of time) and buying longer maturity bonds in that curve and realising the gains in bond price as it rolls down the curve. And at the moment, yield curves in Europe are steeper than many other of the larger developed world bond markets.”

And to be fair, this allocation has probably made money the past few months as European bond yields have gone even more negative (driving bond prices up).

MoneyOwl goes on to say that they’ll also consider adding in new bond funds in future if it meets their criteria:

“they will be looking at other suitable bond funds, possibly of a longer duration, but currently none are available which fulfil their criteria. Their criteria for bond funds are that (a) they have to be hedged back to SGD (otherwise the volatility of currency, being higher than that of bonds, will mean taking a different level risk from what is intended by the bond allocation); (b) they have to be non-forecasting in approach; (c) they should be low cost. Currently, only the Dimensional Short Fixed Income Fund fulfils all these criteria.”

So yeah… read into that what you will!

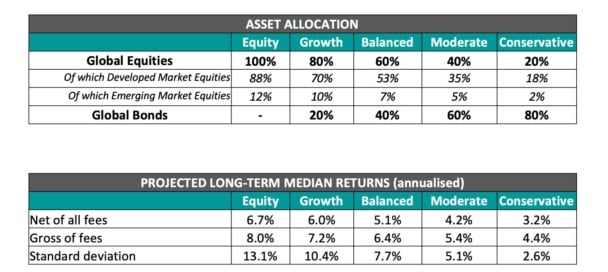

Asset Allocation

MoneyOwl offer 5 different portfolios which are a mix of the 3 Dimensional funds.

Note: Projected returns are based on the historical indices returns of Dimensional Global Core Equity Index, Dimensional Emerging Markets Adjusted Large Caps Index & FTSE World Government Bond Index 1-5 Years (hedged to SGD) from Jan 1994 to December 2017. Please note that past performance is no guarantee of future results.

Backtested Returns

I backtested the returns for MoneyOwl (highest risk setting) over a 20 year period, against EndowUs, the S&P500, and an all world index (my personal backtesting):

| Fund | Returns (annualised, 1994 to 2017) |

| MoneyOwl (Highest risk setting – 100% Equity) | 8.0% |

| Endowus (Highest risk setting – 100% Equity) | 8.0% |

| S&P500 | 9.55% |

| MSCI All Country World Index | 7.2% |

Couple of key takeaways:

S&P500’s performance is deceptive – The S&P500 had an amazing 9.55% return over this 20+ year period. However, the past 10 years saw the US emerge very strongly from the financial crisis, while the rest of the world continues to struggle. This explains why the S&P500 did so well relative to the all world index.

What is problematic though, is that from a historical perspective, whenever one country has a period of outperformance, it is typically followed by a period of underperformance. Applied to the S&P500, it may mean that it will underperform in the coming years.

The Dimensional Funds solve this by essentially being an all world index, so it will perform even if the US economy doesn’t do so great.

MoneyOwl’s portfolio outperforms the MSCI All Country World Index – On a historical basis though, the underlying Dimensional Funds do indeed outperform the MSCI All Country World Index over long periods of time (20 years plus).

MoneyOwl and Endowus have similar performance – Because MoneyOwl and Endowus use largely the same Dimensional Equity Funds, the performance is similar.

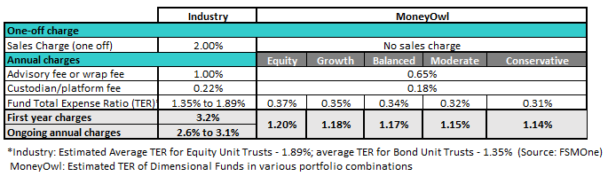

Fees

MoneyOwl vs Traditional Financial Advisory channels

Investing in Dimensional through MoneyOwl is cheaper than buying an actively-managed Unit Trust through a financial advisor.

Fees are massive because every 1.5% you’re paying, is 1.5% of returns you’re not getting. An actively-managed fund with these higher charges has to outperform MoneyOwl’s funds by 1.5% or more just to justify its fees, which is not an easy task.

MoneyOwl vs other Robos

| MoneyOwl | Endowus | StashAway | |

| Advisory Fee | 0.65% | 0.25% to 0.6% | 0.2% to 0.8%. |

| Platform Fee | 0.18% | None | None |

| Fund Expense | 0.31 – 0.37% | 0.43 – 0.55% | About 0.2% |

| Total | 1.14% – 1.20% | 0.68% – 1.15%

Note: the 0.68% is on a $5,000,000 portfolio. On S$200,000, it will be 1.03% to 1.15%. |

0.4% – 1.0% |

As it turns out, MoneyOwl’s fees are on the higher side as compared to EndowUs and StashAway. But objectively speaking, unless you are investing large sums (> S$200,000), the fees are all pretty close enough that you shouldn’t pick between them based purely on fees.

I don’t think the StashAway comparison is fair because MoneyOwl gives you exposure to Dimensional Funds, whereas StashAway uses plain vanilla ETFs that you can get via a simple Saxo account. The StashAway style robos are also not a true passive investment because they contain certain tactical biases in their asset allocation (they may overweight certain asset classes within their portfolio), so you do need to take some time out to evaluate each Robo individually to see whether you like their asset allocation.

Versus EndowUs though, both “Roboadvisors” offer similar exposure to Dimensional, but with MoneyOwl there is that “NTUC” parentage, and the ability to speak to a human advisor if you are in doubt over your investments. So it does depend on what is important to you.

Closing Thoughts: Should you invest in MoneyOwl?

Whether the StashAway style robo-advisors will outperform the MoneyOwl style robo-advisors going forward is a really tough question.

It’s a question that really goes to the heart of investing, on whether large cap stocks will continue to outperform, or will value stocks make a grand return.

And there are no easy answers for this. Many of the greatest investing minds around the world struggle with these questions, with no clear consensus.

My personal thought, is that if you’re prepared to take a longer term view (and I mean 10 to 20 years), there is a very strong case of value making a huge comeback. If it does, these Dimensional Funds are going to outperform.

Would I invest with MoneyOwl? To be honest, I actually really like the underlying Dimensional Funds. They’re run by people like David Booth (Chicago Booth business school is named after him) and a number of Nobel Laureates like Myron Scholes (who co-developed the Black-Scholes options pricing model) and Robert Merton. So these are really smart guys, and I wouldn’t want to bet against them, especially over extended periods of time.

For now, MoneyOwl (with EndowUs, Providend and a few other IFAs) are the main ways to access Dimensional Funds in Singapore. So if you do want to get exposure to Dimensional, they’re worth checking out as Dimensional does not sell its funds directly to retail clients.

What do you guys think? Would you invest with MoneyOwl? Share your thoughts in the comments section below! I respond personally to all comments!

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

Hi! Thanks for the write up.

Do you think investing in Dimensional funds would be a good idea in this current market? Or would it be more prudent to wait the bull run out? Bearing in mind the time in the market principle (which I’m entirely vested in).

Also, what are your thoughts on dollar cost averaging into these funds?

Hi, im 26 years old this year and currently putting in $100 a month into MoneyOwl. My time horizon is minimum 20 years and if i reach the 20 year mark, i may extend it even longer since this is mainly for retirement purposes.

Is it better to have a 100% equity portfolio or 80-20 portfolio for my MoneyOwl portfolio since my time-horizon is minimum 20 years? Currently, they give me a Balanced 60-40 portfolio.

Also, i’m 100% sure i won’t be pulling out anything till at least 50, even if the market crashes more than 50%.

I hope you can give me an honest answer and don’t worry haha, if anything goes wrong, i wont blame anyone also. I just wonder am i supposed to have a full equity portfolio since im definitely gonna be holding on no matter what for 20 years++?

Thanks!

It’s always tricky to advice without knowing your full financial situation.

But for me, if I were 25 today, I would probably want a broad 30 to 40% allocation to bonds in my net worth. So if I already have that separate from my MoneyOwl portfolio, that I’ll go 100% stocks. Otherwise I’ll use the 60-40.

Of course, that’s just my thoughts. 🙂

Hi Financial Horse, like you, everyone keeps talking about MoneyOwl these days and I dont want to just follow the crowd but to be more careful about my money. It is great that you laid out the pros and cons rather clearly. In your mind, what is one other negative and one other positive point that is important to you that you did not mention in your article? I’d love to dig deeper into your very clear mind…

I think the main point about MoneyOwl is that with Dimensional Funds, you’re making an implicit bet on the outperformance of value/small cap against growth/large cap. That hasn’t done well that past 10 years, so if I invest in DImensional today, I’m making a bet that over the next 20 to 30 years, there will be a “paradigm shift” in investing that marks the return of the value/small cap stocks.

My own take is that it is ridiculous to pay advisors, Robo or otherwise,1% or more annually to simply have them do asset allocation and rebalancing for you. The long term effects on returns are horrendous. You are far better off doing it yourself via plain vanilla ETFs and a low cost broker like Interactive Brokers. If you need advice on asset allocation, simply put a small sum say $1000-10000 into your preferred Robo-advisor, see the asset allocation they recommend for you and replicate it yourself for the rest of your assets using your own low cost broker. The point made on Dimensional funds may be valid but if you wanted a greater tilt towards value and small cap stocks, there are ETFs for that too. For example, VBR for Russell 3000 stocks. So you can approximate what Dimensional does at a lower cost. At the end of the day, if you believe John Bogle, cost is king. 1+% is far too high. 0.05% is better

I agree wih you. The cost is just too high and will erode the return. But for young folks with little capital to start off, I am not sure, may be a good starting platform?

I absolutely agree actually. And it’s why I dont use advisors for my own asset allocation.

But I guess not everyone feels these way, and some people prefer to just pay an advisor a small fee so they don’t have to worry about such stuff.

Robo fee needs to be 0.50% or less to be attractive, imo. Hope they lower in the future.

Agreed! The lower the fees the better. But because Singapore is a small market, it may be hard to any player to generate the economies of scale required to lower fees to the extent that we see in the US.

Agreed. The average busy person might not have the time or discipline to do this. So a monthly contribution makes sense vs idle money in the bank in the long run.

I have two questions.

First, are these funds srs eligible? If so, it would make sense as we can’t get international stock exposure via etfs on the sgx (srs only allows stocks listed in Singapore 🙁 )

Second, how are small cap stocks that eventually evolve into large caps treated? The problem with small cap etfs is that when they increase beyond a certain size, they migrate out of the index. This limits the upside from small caps which turn out to be multi baggers.

Agreed!

On your questions:

1. Not that I know of actually, only StashAway is SRS eligible for now.

2. Yep you’re right, that’s my understanding as well. Of course, they need to grow to a really large size before this becomes an issue. And it can be negated by buying both a small cap and a large cap index. Eg. The Russell 2000 + S&P500. Ultimately, you can’t have your cake and eat it, that’s just how passive indexing works. 🙂

Hi, I have a question. Looking at your table, Moneyowl “balanced” portfolio, projected annualised return is 5.1% (nett of all fees). First State Bridge (an example of a balanced unit trust) has 10-year annualised return of about 6% (bid-to-bid return as no sales charge nor platform fees when buying on Phillip Securities Poems.) So I don’t understand why people say unit trust cost is high and so returns will be lower. Can you please help me understand? Thank you.

That’s a really good question. I think the biggest points here is that these are historical returns, and nobody knows the future returns. If the Unit Trust can guarantee 6% returns going forward, and I know for certain that MoneyOwl will have 5% returns, then of course the Unit Trust makes sense.

But in reality, nobody knows that the future performance will be like, so there’s a bit of a judgment call there. And if you leave out performance, the only thing we know for certain will be fees – fees are constant regardless of performance.

So fees and performance will need to be evaluated hand in hand. If you can keep fees down and get the same underlying exposure, it becomes a no brainer. 🙂

Hey dear, thanks for the post! The more robo or automated advisory solutions are out there, the more choice consumers will have of course!

Btw, FYI, Dimensional Funds are available via ALL IFAs in Singapore since like 2 years. So If one has an independent financial advisor or asset manager, one can get access without signing up for a robo advisor at all.

Factor investment methodology developed by Fama and a few others is more than 25 years old and major factors are statistically significant. However, value factor was underperforming for quite awhile and continues to outperform in a recession vs growth tech stocks. The reason for that in my view is “passive investment” proliferation as a strategy for past 20+ years since Vanguard. In effect, passive is actually an active strategy, just agnostic of the price of the underlying asset. Since the liquidity event this March, I believe we will see a demise of “passive” as we know it. Reasons?

– passive is driven by large amount of US Baby Boomer Generation savings going into assets. This cohort is retiring now and withdrawing funds instead. So we will see outflows from passive strategies.

– passive is driven by 40+ years of credit expansion which lifted all boats and inflated bubbles in absolutely all asset classes you can think of – real estate, equity, bonds, alternatives

– passive strategy of buying at any price in a volatility event turns into a strategy of selling at any price – we saw a bit of it back this March

– passive buys assets without any regard for price or value of the investment derived by careful fundamental analysis – most likely the reason of value underperformance and reason for severe levels of auto correlation in the markets – i.e. buy the dip mentality..

So I would say robo advisors in their pure form won’t survive. Bionic ones – most likely still remain.

I did analysis of investment models and functionality of more than 16 different robos both in HK and Singapore, which includes Smartly, Stashaway, etc and did a ranking of all of them. My research was 100% independent and sponsored by a private banking consultancy firm Synpulse that truly wanted to understand what’s going on in this area. Some summary can be found on my LinkedIn profile here – https://www.linkedin.com/pulse/top-4-robo-advisors-asia-elena-okhonko/

If you or your readers are interested in details of the research and would like to read the entire white paper, can ping me privately on inkedin.