Singapore Savings Bonds are starting to get interesting again!

With the rise in 10 year Singapore Government Bond yields (which SSBs track).

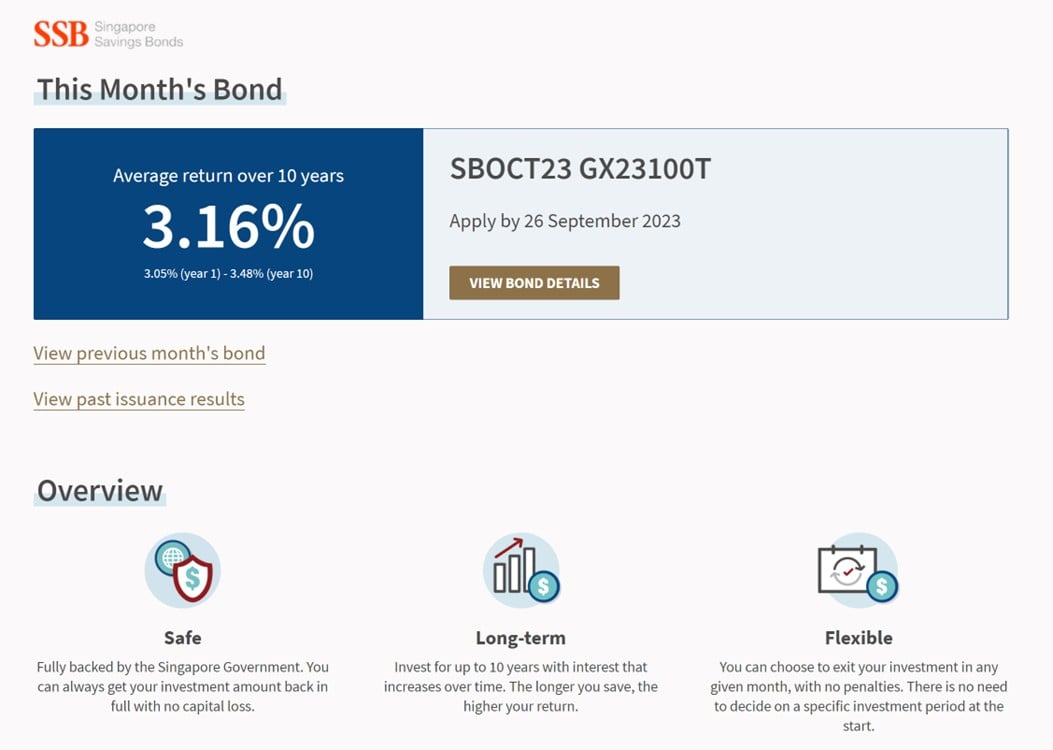

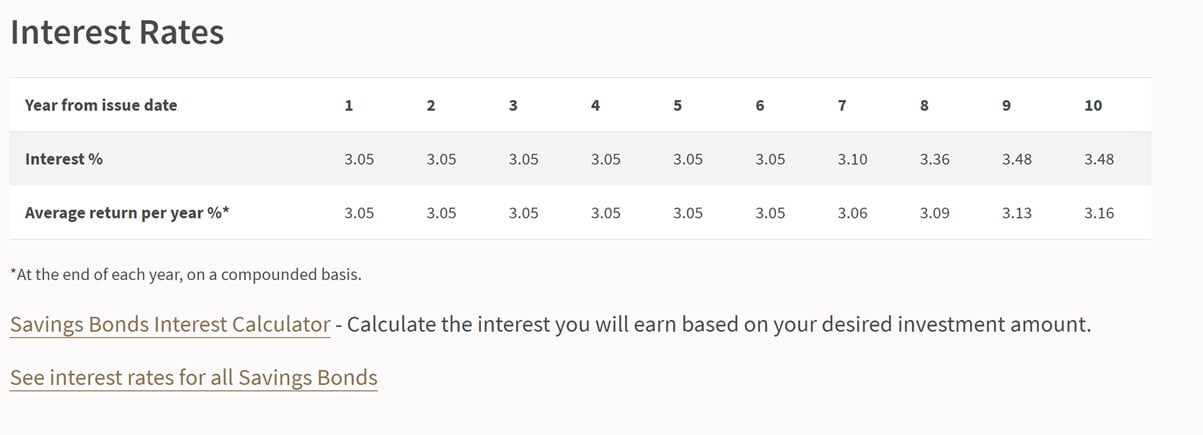

The latest Singapore Savings Bonds yield 3.16% over 10 years, which is the highest yielding SSBs for all of 2023.

You may also note that 3.16% is comfortably above CPF-OA’s 2.5%, and this is risk-free cash the next 10 years – which really helps to put things in perspective.

Singapore Savings Bonds yield 3.16% over 10 years, 3.05% for the first 6 years

The main reason why Singapore Savings Bonds haven’t been so attractive the past 9 months or so is because of the highly inverted yield curve.

But the SGS yield curve has steepened noticeably of late – primarily due to a drop in 6 month T-Bills yields, coupled with a rise in the 10 year yields.

You can see this steepening below, which is a very classic late cycle move (and indicates we are very late in this interest rate cycle).

This has made Singapore Savings Bonds more attractive vs short term options like Fixed Deposits or T-Bills.

Latest Singapore Savings Bonds yield 3.05% for the first 6 years.

And go as high as 3.48% in year 9 and 10, for an average of 3.16% over 10 years.

Why I am buying Singapore Savings Bonds?

Simple answer.

I see Singapore Savings Bonds as cash, with a 1 month liquidity.

Any time I need the money back, I can get it at the start of the next month.

And yield wise Singapore Savings Bonds are more attractive than other cash options – for example GXS which is fully liquid only pays 2.68% now.

Other higher yield options like money market funds (or Chocolate finance) are technically not risk free, while Singapore Savings Bonds are fully backed by the Singapore government.

And the higher yielding options like Fixed Deposit or T-Bills don’t allow you to get the money back ahead of maturity without some kind of penalty.

The other big benefit with Singapore Savings Bonds of course, is that you lock in interest rates for 10 years.

If interest rates are going to get slashed in 2024, this gives you the option of holding onto higher yielding cash options.

Best way to buy / redeem Singapore Savings Bonds?

Quite a few of you have reached out to ask about what is the best way to buy / redeem Singapore Savings Bonds, so I wanted to share some thoughts on this.

Next month’s Singapore Savings Bonds are likely to be even better

First off, do note that there is a good chance that next month’s Singapore Savings Bonds will be even more attractive.

You can look at the Singapore 10 year yield below, and average yields in September look to be even higher.

In fact if you ask me, I think there’s a fairly good chance the Singapore Savings Bonds the next few months are all quite attractive, given the steepening yield curve.

Will you get full allotment of Singapore Savings Bonds?

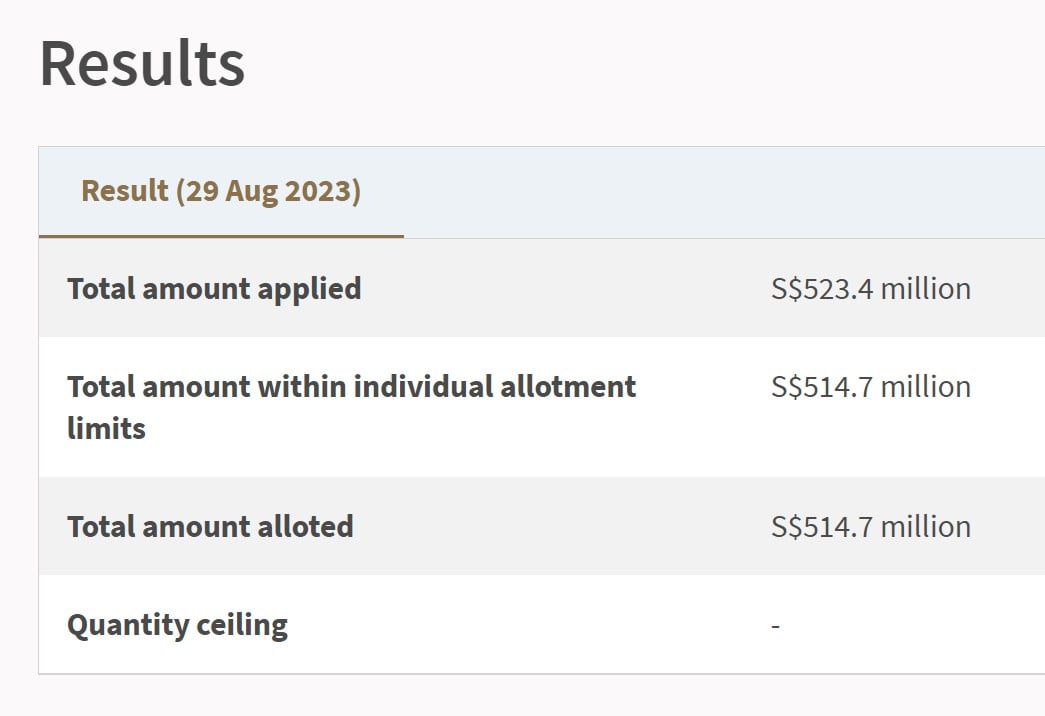

All Singapore Savings Bonds in 2023 have seen full allotment as they were undersubscribed (because T-Bills and Fixed Deposits were too attractive).

Even for the most recent September SSBs – you’re looking at full allotment for whatever amount you apply for (up to the $200,000 allotment limit).

Will this change going forward?

I think you’ll probably still see full allotments for this month’s Singapore Savings Bonds.

But the rest of the year, really depends on how much more attractive they get.

So… apply now or wait?

Which raises the question – should you apply for Singapore Savings Bonds now, or wait a couple of months before applying?

I mean it’s ultimately your decision.

The way I see it though, Singapore Savings Bonds are a very low stakes investment because you can redeem them any time.

So if you have spare cash lying around and not earning a lot of yield – there’s really no harm in applying now to earn the interest for a couple months and lock in the rates (and allotment) first.

then depending on what changes the next few months you can always just redeem and get the cash back then – to buy the newer SSBs or whatever other investment.

The only cost is the $2 application fee and the time spent (doesn’t take more than a few minutes tops via internet banking).

How do you know which Singapore Savings Bonds to redeem?

A lot of you also which Singapore Savings Bonds you should redeem to buy the new SSBs.

The easy answer, is that if the SSBs you own yield less than this month’s SSBs, it’s a no brainer.

The tricky part of course, comes in 2 scenarios:

- Your old SSBs have a lower short term yield (1-2years), but a higher long term yield (5 years and beyond)

- Your old SSBs have a yield very close to the current SSBs

In the first scenario, I would say a bird in hand is worth two in the bush.

I would probably just redeem them and get enjoy the higher short term yield.

In the second scenario, I would say if the yields are close enough (say 0.1 – 0.2% difference).

Then it’s probably not worth the time and effort, and I would probably just wait the next few months until the differential gets bigger.

But like I said, there’s no right or wrong here.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Note that you can redeem and buy SSBs in the same month if you are at $200,000 cap

On that note – I do want to clarify a technical point that many of you ask about.

Let’s put it this way.

If you are at close to the SSB allotment limit – for eg. $180,000 in SSBs today.

You can actually submit a redemption request for $50,000 in SSBs this month.

And apply for another $70,000 in SSB this month.

And get the full $70,000 in SSBs.

So you don’t need to *waste* one month in between redeeming and buying new SSBs.

Buy you must have the cash on hand

The only catch is that you need to have the cash on hand to do this trick.

So in the example above – the $70,000 is deducted from your account at the time of application.

You cannot use the $50,000 from the redeemed SSBs to buy SSBs this month (as the $50,000 only comes in the start of the next month).

If you don’t have the cash on hand, then you just have to wait for the 1 month gap.

There’s actually a whole FAQ on this on the MAS website:

Yes. You can redeem your holdings in SSB and apply for a new bond in the same month, provided you are within your total Individual Limit of S$200,000.

However, you must ensure that there is sufficient money in your bank account at the point of application as your redemption proceeds will only be returned to you by the end of the second business day of the following month from when you submitted the redemption application.

Anyone 18 and above can buy $200,000 worth of Singapore Savings Bonds

Note also that every person above 18 can apply for Singapore Savings Bonds up to the $200,000 limit (as long as you have a CDP account).

I know some investors who are maxxed out and want to use their children’s name to buy more.

So there’s that option available.

Application Timeline for Singapore Savings Bonds

If you’re keen to apply for the Singapore Savings Bonds – do apply by 9pm on 26 September.

Same timing for redemption of Singapore Savings Bonds.

Love to hear what you think!

Are Singapore Savings Bonds starting to get more attractive vs T-Bills and Fixed Deposits?

This article was written on 15 Sep 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

– Get up to USD 800 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 800 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.